Underground Gas Storage Market Size 2026-2030

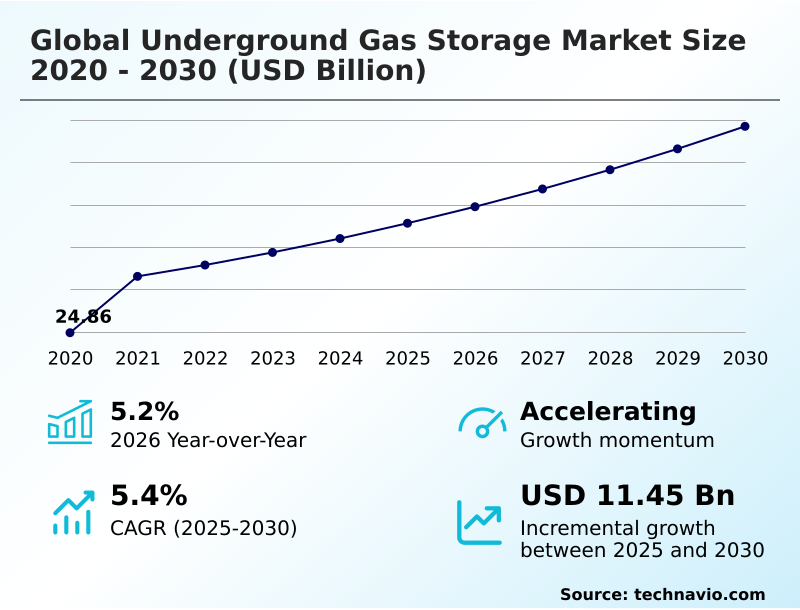

The underground gas storage market size is valued to increase by USD 11.45 billion, at a CAGR of 5.4% from 2025 to 2030. Increasing need for energy security and supply reliability will drive the underground gas storage market.

Major Market Trends & Insights

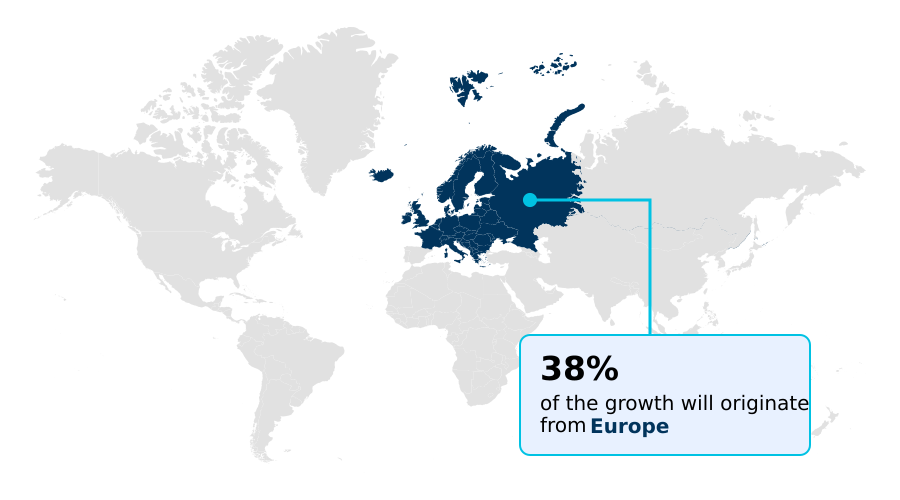

- Europe dominated the market and accounted for a 38.2% growth during the forecast period.

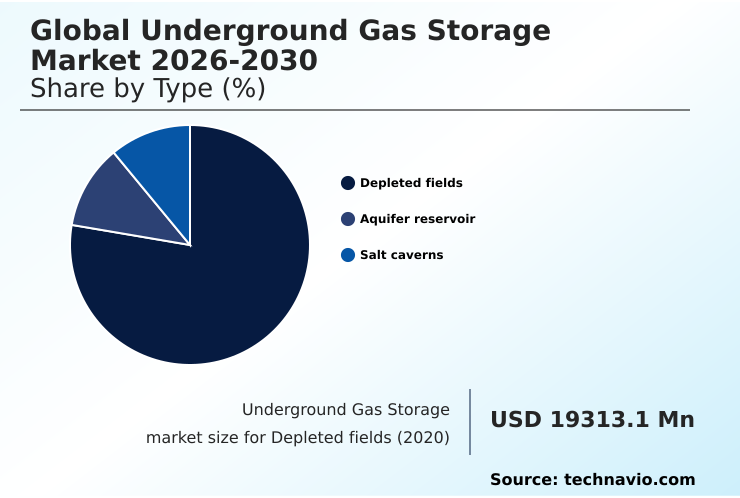

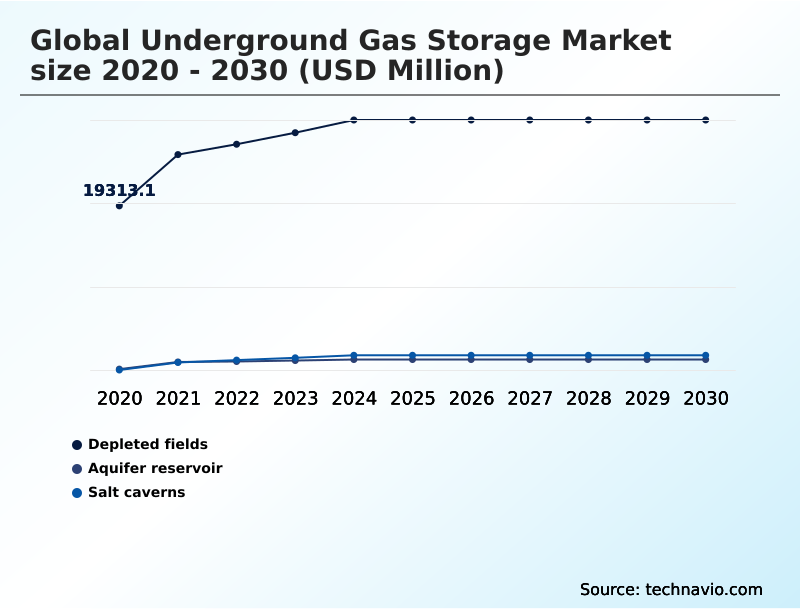

- By Type - Depleted fields segment was valued at USD 27.99 billion in 2024

- By Product - Natural gas segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 24.39 billion

- Market Future Opportunities: USD 11.45 billion

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The underground gas storage market remains a critical component of energy infrastructure, fundamentally enabling the management of supply and demand imbalances. Its importance is magnified by the increasing need for energy security and the global push to integrate intermittent renewable sources into the power grid.

- Key drivers include the necessity for seasonal demand balancing, particularly for winter heating loads, and the provision of grid stability services to support gas-to-power infrastructure. A prominent trend involves the strategic pivot toward hydrogen readiness validation and multi-gas compatibility, repurposing assets like salt caverns for future energy carriers.

- For instance, a utility provider leverages its working gas capacity in depleted gas reservoirs not only for seasonal arbitrage but also as a strategic gas reserve to ensure uninterrupted fuel for its power plants during unexpected pipeline disruptions, thereby ensuring operational efficiency optimization.

- However, the industry faces challenges related to the high capital costs of asset modernization programs and navigating stringent regulatory frameworks for new developments.

What will be the Size of the Underground Gas Storage Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Underground Gas Storage Market Segmented?

The underground gas storage industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Depleted fields

- Aquifer reservoir

- Salt caverns

- Product

- Natural gas

- Hydrogen

- Others

- End-user

- Power generation

- Residential and commercial

- Industrial

- Others

- Geography

- Europe

- Germany

- Italy

- The Netherlands

- North America

- US

- Canada

- Mexico

- APAC

- China

- Australia

- Japan

- Middle East and Africa

- Turkey

- Saudi Arabia

- UAE

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- Europe

By Type Insights

The depleted fields segment is estimated to witness significant growth during the forecast period.

Depleted fields are the most established form of underground gas storage, leveraging former production reservoirs for new utility. These sites benefit from well-documented geological traits, including proven caprock integrity and known reservoir pressure monitoring parameters, which significantly de-risk development.

Existing infrastructure, from wells to pipelines, can often be repurposed, reducing initial capital outlay.

While their geomechanical stability is understood, they offer lower injection and withdrawal rates compared to other options, making them optimal for seasonal demand balancing rather than high-frequency balancing.

The reuse of assets is a key economic driver, with some operators reporting up to a 20% increase in capital efficiency on conversion projects compared to greenfield developments.

This segment’s maturity provides a reliable foundation for regional energy supply chain resilience.

The Depleted fields segment was valued at USD 27.99 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 38.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Underground Gas Storage Market Demand is Rising in Europe Get Free Sample

The geographic landscape of the underground gas storage market is defined by regional energy priorities and geological potential.

In Europe, the focus is on meeting security of supply mandates through strategic gas reserves, with facilities in Germany and Italy optimizing cushion gas volume to maximize deliverable capacity.

North America leverages its vast depleted gas reservoirs and salt cavern storage to support a dynamic energy market, including growing LNG exports. Here, digital twin modeling has improved forecast accuracy for gas deliverability by over 18%.

Meanwhile, the APAC region, led by China, is rapidly expanding its underground storage to manage seasonal demand, with new projects achieving operational status 20% faster than historical averages due to streamlined construction and commissioning processes.

Each region adapts its use of floating storage regasification units (FSRUs) and pipeline line pack to complement its primary underground storage strategy.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic development of the underground gas storage market is increasingly focused on future-proofing assets while managing legacy infrastructure. The economic viability based on seasonal spreads remains a core consideration, but the conversation has expanded. For instance, the role of storage in national energy strategy now includes preparing for a decarbonized future.

- This involves detailed assessments of repurposing depleted fields for hydrogen and advancing underground hydrogen storage in salt caverns. The latter requires overcoming technical hurdles like hydrogen embrittlement in steel well casings, a key focus of current research. Simultaneously, operators are managing wellbore integrity for aging storage assets, where new methane leakage mitigation technologies have proven critical.

- These modern systems can reduce fugitive emissions by over 80% compared to older facilities. The planning for new capacity involves complex choices, such as evaluating the cost of cushion gas in aquifer storage versus the high capital investment for the solution mining for salt cavern creation.

- The goal of balancing the grid with gas-fired peaker plants is driving demand for high deliverability storage for LNG export and domestic peak shaving with high-cycle salt caverns. The entire value chain, from managing seasonal demand with depleted reservoirs to exploring underground storage for synthetic methane, is undergoing a transformation.

- This shift is supported by advanced tools like a digital twin for reservoir pressure management to ensure the geomechanical stability of storage formations. Furthermore, the push for environmental stewardship has intensified the regulatory permitting for new storage facilities, while also creating opportunities for CCUS in deep saline aquifer formations.

What are the key market drivers leading to the rise in the adoption of Underground Gas Storage Industry?

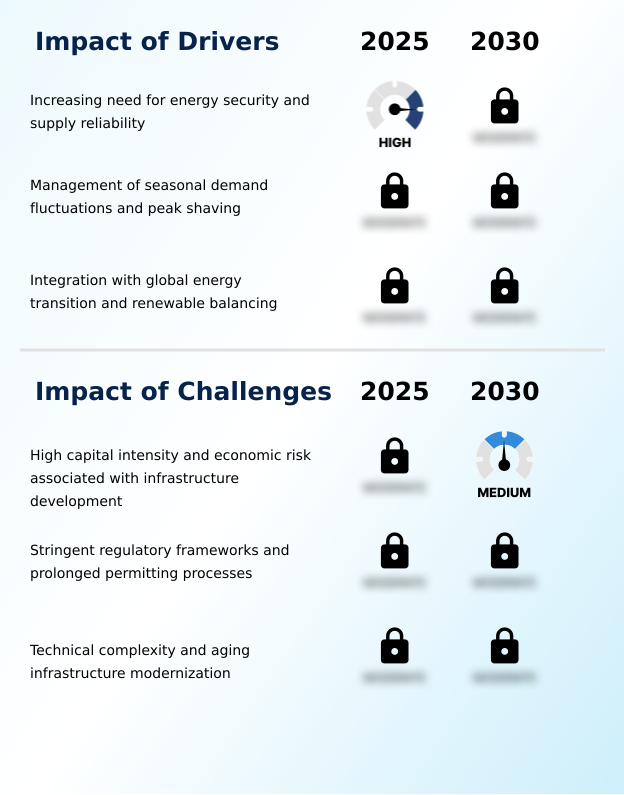

- The increasing need for energy security and supply reliability is a key driver of market growth.

- Market growth is fundamentally driven by the need for energy security and grid stability in a shifting energy landscape. The imperative to manage seasonal price spreads and ensure a reliable supply for gas-to-power infrastructure underpins the value of underground storage.

- As the penetration of intermittent renewables increases, the role of ancillary service provision from high-deliverability storage has become critical; facilities are now able to respond to grid fluctuations up to 40% faster than a decade ago.

- This capability for intermittent renewable balancing is a significant factor attracting new investment. Furthermore, mandatory inventory levels and national security mandates in key regions are compelling the expansion of working gas capacity.

- This strategic development ensures that a buffer is available to counter supply disruptions, with some regions now holding strategic gas reserves equivalent to 30 days of peak consumption.

What are the market trends shaping the Underground Gas Storage Industry?

- The accelerated integration of digitalization and artificial intelligence in asset management is an upcoming market trend. This shift is poised to optimize operational efficiency and enhance predictive maintenance capabilities across the sector.

- Key trends are reshaping the underground gas storage market, primarily through digitalization and decarbonization initiatives. The adoption of predictive maintenance analytics is improving asset performance, with some operators reporting a 15% reduction in unscheduled downtime. This focus on operational efficiency optimization is critical for managing both legacy assets and new developments.

- Concurrently, the industry is advancing toward multi-gas compatibility, with significant investment in hydrogen readiness validation. Pilot projects for underground hydrogen storage in salt caverns are demonstrating the technical feasibility of repurposing infrastructure, a key component of long-duration energy storage strategies.

- This transition is supported by a heightened focus on environmental compliance, where the deployment of satellite-based methane monitoring has enhanced leakage detection accuracy by over 30%, reinforcing the sector's commitment to sustainable operations and meeting stringent security of supply mandates.

What challenges does the Underground Gas Storage Industry face during its growth?

- The high capital intensity and economic risk associated with infrastructure development pose a key challenge to industry growth.

- Significant challenges constrain the pace of development in the underground gas storage market, led by high capital intensity and regulatory hurdles. The financial risk of new projects is substantial, as economic viability is often tied to volatile seasonal energy prices.

- Navigating the stringent regulatory permitting for new storage facilities can add years to project timelines, with approval processes in some jurisdictions now taking up to 50% longer than a decade ago. Modernizing aging infrastructure presents another major hurdle, as ensuring the geomechanical stability of decades-old depleted reservoirs requires significant and ongoing investment.

- These asset modernization programs can consume over 60% of a facility's annual capital budget. Finally, technical complexities, such as the potential for hydrogen embrittlement in steel infrastructure when considering conversion for hydrogen storage, require new engineering solutions and add to the overall project risk and cost.

Exclusive Technavio Analysis on Customer Landscape

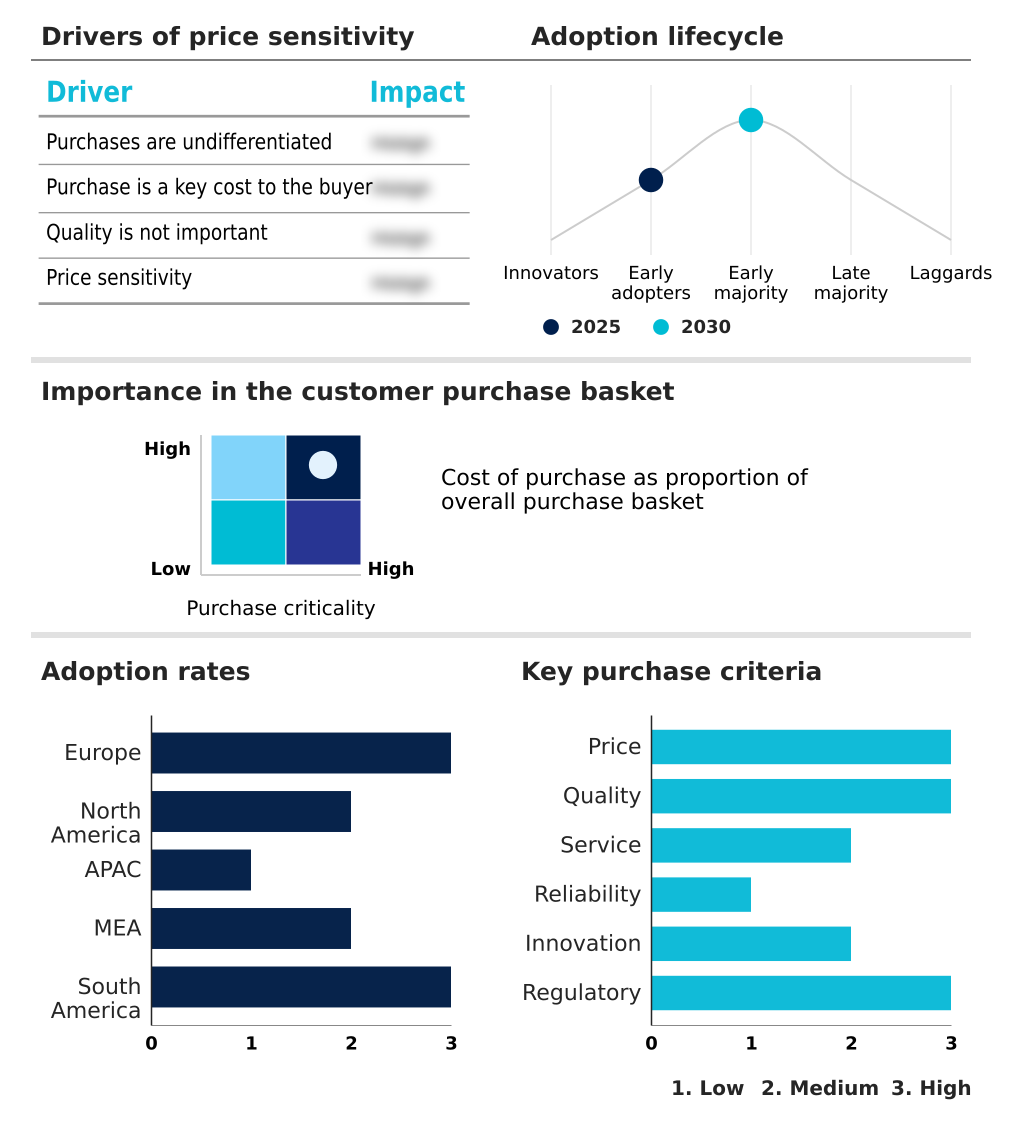

The underground gas storage market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the underground gas storage market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Underground Gas Storage Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, underground gas storage market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Atmos Energy Corp. - Analysis points to specialized offerings in seasonal storage and flexible gas supply services, leveraging underground facilities to ensure market balance and supply reliability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atmos Energy Corp.

- Boardwalk Pipelines LP

- Centrica Plc

- Dominion Energy Inc.

- DTE Energy.

- Enagas SA

- Enbridge Inc.

- Energy Transfer LP

- Equinor ASA

- Kinder Morgan Inc.

- National Fuel Gas Company

- NiSource Inc

- OMV AG

- ONEOK Inc.

- RWE AG

- SSE Plc

- TC Energy Corp.

- The Williams Co. Inc

- Uniper SE

- WEC Energy Group Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Underground gas storage market

- In September 2024, Enagas SA completed a feasibility study confirming the potential to increase its underground storage capacity by 15% to bolster Spain's role as a European energy hub.

- In November 2024, The U.S. Department of Energy announced a new funding initiative to support the modernization of aging underground gas storage infrastructure, focusing on methane leak detection and prevention technologies.

- In January 2025, STORAG Etzel initiated the first commercial-scale hydrogen filling in its salt caverns in Germany, marking a pivotal step in repurposing existing infrastructure for clean energy carriers.

- In March 2025, Sempra Infrastructure officially commenced construction of its Phase 1 LA Storage facility in Cameron Parish, Louisiana, a project designed to expand salt cavern capacity for the growing Liquefied Natural Gas export market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Underground Gas Storage Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 11452.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.2% |

| Key countries | Germany, Italy, The Netherlands, France, UK, Spain, US, Canada, Mexico, China, Australia, Japan, South Korea, India, Indonesia, Turkey, Saudi Arabia, UAE, Israel, South Africa, Argentina, Brazil and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The underground gas storage market is undergoing a strategic transformation, driven by the dual mandates of ensuring current energy security and preparing for a decarbonized future. Boardroom decisions are increasingly centered on long-term capital allocation for asset modernization, weighing the costs of maintaining geomechanical stability in aging depleted gas reservoirs against investing in new salt cavern storage.

- This is complicated by the push towards hydrogen readiness, where managing the risks of hydrogen embrittlement and ensuring caprock integrity for a different gas composition are paramount. Operators are leveraging advanced technologies like digital twin modeling to optimize injection and withdrawal rates and ensure wellbore integrity.

- The viability of projects often hinges on managing cushion gas volume to maximize working gas capacity, a critical factor in both seasonal demand balancing and providing high-frequency balancing for grids with intermittent renewables. The integration of LNG regasification and even floating storage regasification units (FSRUs) with underground assets highlights a move toward a more flexible and interconnected system.

- This strategic pivot is evident in projects focused on CCUS and synthetic methane storage, where facilities implementing new reservoir pressure monitoring technologies have demonstrated a 20% improvement in operational safety compliance.

What are the Key Data Covered in this Underground Gas Storage Market Research and Growth Report?

-

What is the expected growth of the Underground Gas Storage Market between 2026 and 2030?

-

USD 11.45 billion, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Depleted fields, Aquifer reservoir, and Salt caverns), Product (Natural gas, Hydrogen, and Others), End-user (Power generation, Residential and commercial, Industrial, and Others) and Geography (Europe, North America, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing need for energy security and supply reliability, High capital intensity and economic risk associated with infrastructure development

-

-

Who are the major players in the Underground Gas Storage Market?

-

Atmos Energy Corp., Boardwalk Pipelines LP, Centrica Plc, Dominion Energy Inc., DTE Energy., Enagas SA, Enbridge Inc., Energy Transfer LP, Equinor ASA, Kinder Morgan Inc., National Fuel Gas Company, NiSource Inc, OMV AG, ONEOK Inc., RWE AG, SSE Plc, TC Energy Corp., The Williams Co. Inc, Uniper SE and WEC Energy Group Inc

-

Market Research Insights

- The dynamics of the underground gas storage market are shaped by the critical need for energy infrastructure resilience. Strategic infrastructure asset management is shifting, with a focus on asset modernization programs that improve performance; facilities adopting predictive maintenance analytics have seen a 15% reduction in unplanned outages.

- The commercial landscape is heavily influenced by seasonal price spreads, which dictate the profitability of storage operations. In response to stricter security of supply mandates, operators are enhancing capacity, leading to a 10% average increase in deliverable volumes from key facilities over the past two years.

- This push for reliability is essential for supporting both industrial consumers and providing crucial grid stability services in an evolving energy mix.

We can help! Our analysts can customize this underground gas storage market research report to meet your requirements.

RIA -

RIA -