Urology Devices Market Size 2025-2029

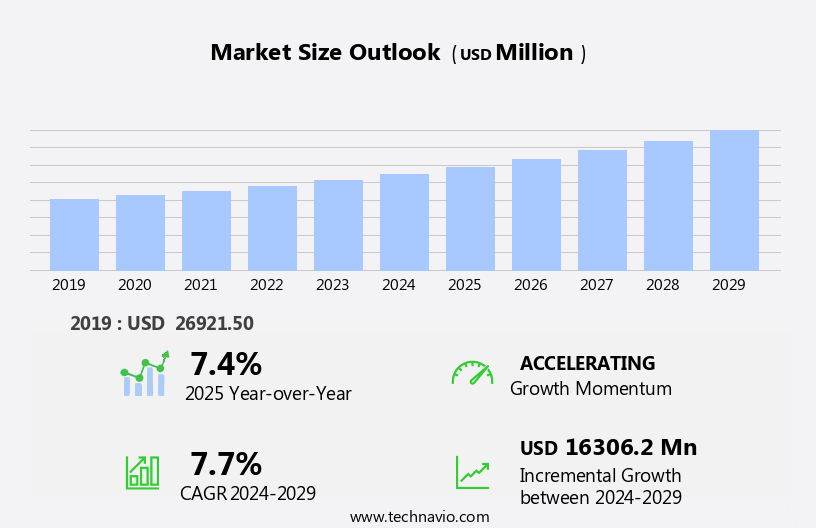

The urology devices market size is forecast to increase by USD 16.31 billion at a CAGR of 7.7% between 2024 and 2029.

- The market is experiencing significant growth, driven primarily by the increasing prevalence of urological diseases such as kidney stones, prostate cancer, and urinary tract infections (UTIs).. According to the World Health Organization, over 12% of the global population is affected by urological conditions, making it a substantial public health concern. Additionally, the rising demand for urinary incontinence devices and kidney stone therapeutics is further fueling market expansion. This trend, coupled with an aging population and rising healthcare expenditures, is fueling market expansion. Innovative technologies, such as robotic-assisted surgery and minimally invasive devices, are transforming the urology landscape. These advanced solutions offer numerous benefits, including reduced invasiveness, shorter hospital stays, and quicker recovery times. Furthermore, they enable improved precision and accuracy, leading to better patient outcomes. However, the market's growth potential is tempered by several challenges.

- Regulatory hurdles impact adoption, as stringent regulatory requirements and lengthy approval processes can significantly delay product commercialization. Additionally, supply chain inconsistencies and high production costs pose significant challenges for market participants. Addressing these challenges through strategic partnerships, cost optimization, and regulatory compliance will be essential for companies seeking to capitalize on the market's opportunities. This market includes consumables such as catheters and disposable sheaths, urodynamic systems for evaluating bladder function, and urology robotic systems for performing minimally invasive surgeries.

What will be the Size of the Urology Devices Market during the forecast period?

- The market encompasses a diverse range of technologies, from wearable sensors for monitoring urinary patterns to advanced procedures for urological oncology and genitourinary medicine. One significant trend is the integration of personalized therapy and precision medicine, which includes neurogenic bladder treatment and voiding dysfunction management. Bladder augmentation and nerve sparing surgery are key areas of focus, with advancements in artificial intelligence and big data analytics enabling more effective patient care. Meanwhile, minimally invasive procedures such as percutaneous nephrolithotomy and holmium laser enucleation are gaining popularity due to their reduced recovery time and improved patient outcomes. Technological advancements, such as insufflators and advanced endoscopy devices, continue to shape the market, enabling more precise and effective treatments. Ureteral stents and nephrostomy tubes are essential for managing ureteral obstructions and kidney issues.

- In the field of male infertility, urethral slings and microsurgical techniques are being used to address urethral strictures and pelvic floor disorders. Interstitial brachytherapy and tumor ablation are increasingly utilized for treating various urological cancers. Remote monitoring and real-time data analysis are transforming patient care, allowing for more effective management of conditions such as urinary retention and vesicoureteral reflux. Urological oncology and genitourinary medicine continue to be major areas of innovation, with advancements in minimally invasive procedures and targeted therapies. The integration of AI and big data analytics is enabling more accurate diagnoses and personalized treatment plans, ultimately improving patient outcomes and quality of life.

How is this Urology Devices Industry segmented?

The urology devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- KFTD

- UI management devices

- BPH treatment devices

- Urolithiasis treatment devices

- Other

- End-user

- Hospitals and ASCs

- Dialysis centers

- Homecare and clinics

- Product Type

- Instruments

- Consumables and disposables

- Urodynamic equipment

- Robotic and advanced systems

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

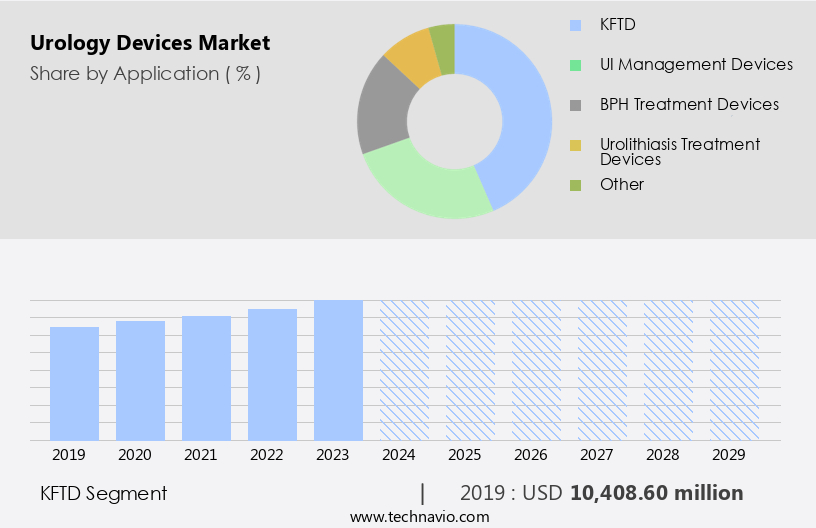

The KFTD segment is estimated to witness significant growth during the forecast period. The market encompasses a range of innovative technologies and treatments, including surgical robotics, urological implants, prosthetic devices, and urological pharmaceuticals. In the realm of cancer care, bladder cancer treatments utilize advanced technologies like robotic surgery and laparoscopic procedures. Urological research and diagnostics employ techniques such as CT scans, MRIs, and ultrasound imaging to detect and monitor conditions like kidney stones and urinary tract infections. This segment also includes infusion pumps, ureteral access sheaths, and nephrostomy tubes. Medical device regulations ensure the safety and efficacy of urological instruments, such as surgical drapes, biopsy needles, and urological instrumentation. Male sexual health solutions include tissue sealing devices, laser therapy, and artificial urinary sphincters. Dialysis devices, including hemodialysis and peritoneal dialysis systems, play a crucial role in managing end-stage renal diseases. Urology devices undergo rigorous testing and validation to meet these standards. The market continues to evolve, driven by technological advancements, research, and regulatory requirements.

The KFTD segment was valued at USD 10.41 billion in 2019 and showed a gradual increase during the forecast period. Urological instruments, including dialysis disposable devices, forceps, scissors, and retractors, are essential components of urological procedures. Female pelvic health focuses on continence devices and urodynamic testing. Urological procedures like transurethral resection and radiofrequency ablation are minimally invasive, reducing recovery time and complications. Healthcare providers leverage endoscopic surgery and ambulatory surgical centers for efficient patient care. Urological consumables, such as surgical staplers, surgical clamps, and surgical gowns, support these procedures. Robotic surgery and prostate cancer treatments have gained significant attention in recent research. Prostate biopsy, benign prostatic hyperplasia, and urology clinical trials are ongoing to advance patient care. Antibiotics and anti-inflammatory drugs are essential urological pharmaceuticals for managing various conditions. CE marking ensures compliance with European Union medical device regulations, enabling global market access.

Regional Analysis

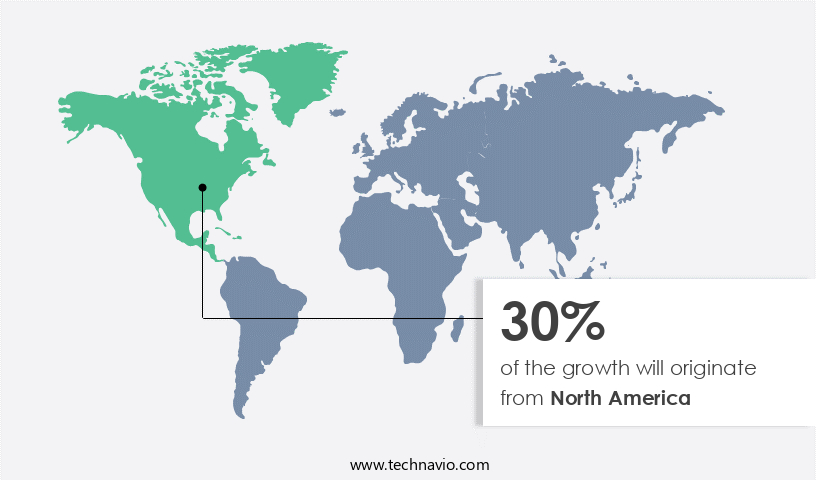

North America is estimated to contribute 30% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is currently leading the global industry in terms of revenue. Key players, including Fresenius Medical Care, Olympus Corporation, C.R. Bard, and Boston Scientific, significantly contribute to this region's growth due to their strong market presence and strategic initiatives, such as expanding product lines and reorganizing sales forces. The increasing prevalence of urology diseases, associated risk factors like diabetes, hypertension, and obesity, and the availability of advanced technologies and favorable reimbursements are driving market demand in North America. Urological conditions, such as bladder cancer, kidney stones, and urinary tract infections, continue to impact a significant population.

To address these conditions, companies are innovating with urological implants, prosthetic devices, surgical robotics, and minimally invasive surgical techniques like laparoscopic surgery and robotic surgery. Urological diagnostics, including CT scans, MRI scans, and urodynamic testing, aid in early detection and effective treatment. Incorporating laser therapy, transurethral resection, and endoscopic surgery into their offerings, companies cater to various urological procedures. Urological pharmaceuticals, including anti-inflammatory drugs, play a crucial role in managing symptoms and promoting healing. Furthermore, continence devices, surgical drapes, and urology consumables support efficient healthcare delivery. The female pelvic health segment is gaining traction, with solutions addressing urinary incontinence and female pelvic organ prolapse.

Male sexual health is another focus area, with treatments for erectile dysfunction and prostate cancer. Regulatory bodies, such as the FDA, ensure medical device regulations are met, ensuring patient safety. Clinical trials and research in urology contribute to the development of new technologies and therapies, further fueling market growth. Ambulatory surgical centers and specialized urology clinics facilitate accessible and cost-effective care. Biopsy needles, urological instrumentation, and surgical staplers and clamps are essential tools for urological procedures. Radiofrequency ablation and tissue sealing devices offer minimally invasive alternatives to traditional surgical methods. Artificial urinary sphincters and surgical gowns cater to the unique needs of urological patients.

The market's dynamic nature is driven by continuous innovation, increasing awareness, and the growing need for effective urological solutions.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Urology Devices market drivers leading to the rise in the adoption of Industry?

- The rising incidence of urological diseases serves as the primary catalyst for market growth in this sector. The market encompasses surgical robotics, bladder cancer treatments, urological implants, prosthetic devices, tissue sealing devices, and urological diagnostics. Kidney disease, a non-communicable disease, affects around 850 million people worldwide, with an estimated 37 million individuals in the US. CDC reports suggest that 15% of US adults are affected by kidney disease. This condition can progress and lead to kidney failure or end-stage renal disease (ESRD), necessitating regular renal replacement therapy, such as dialysis, for over two million patients globally.

- Urological research focuses on improving diagnostics, laparoscopic surgery, and male sexual health. Medical device regulations ensure the safety and efficacy of these devices. Urologists and healthcare providers utilize these advanced technologies to enhance patient care and outcomes.

What are the Urology Devices market trends shaping the Industry?

- The emergence of innovative technologies is a significant market trend that is mandated for businesses to adapt and stay competitive. This includes the integration of artificial intelligence, automation, and advanced data analytics to streamline operations and enhance customer experiences. Urology devices have witnessed significant advancements, leading to the development of superior quality and safe solutions for various urological conditions. One notable innovation is the UroLift System, introduced by NeoTract (now a Teleflex company). This minimally invasive treatment for Benign Prostatic Hyperplasia (BPH) is unique as it does not involve the removal of prostate tissue, minimizing the risk of sexual dysfunction. Traditional treatments like Transurethral Resection of the Prostate (TURP) have been associated with ejaculation problems and erectile dysfunction. By addressing this concern, UroLift System has emerged as an attractive alternative for individuals seeking effective BPH treatment while preserving their sexual function.

- Moreover, the integration of advanced technologies such as laser therapy, ultrasound imaging, CT scans, MRI scans, and urological pharmaceuticals, has significantly improved diagnostic accuracy and treatment efficacy for various urological procedures, including the management of urinary tract infections. The anti-inflammatory drugs used in conjunction with these technologies further enhance the therapeutic potential. Continuous efforts towards research and development ensure the market remains dynamic and responsive to the evolving needs of patients and healthcare providers.

How does Urology Devices market faces challenges face during its growth?

- The urology devices industry faces significant challenges due to the presence of limitations and risk factors associated with these technologies, which can hinder its growth. These challenges must be addressed in a professional and knowledgeable manner to ensure continued industry progression. Urology devices play a crucial role in the diagnosis and treatment of various urological conditions, such as kidney stones and prostate cancer. These devices include surgical drapes, surgical gowns, surgical clamps, surgical staplers, continence devices, and ureteroscopes. Ureteroscopes are essential for the removal of kidney stones and the diagnosis of ureteral anomalies. However, their semi-critical nature requires stringent sterilization procedures to prevent infection transmission. The fragile fibers of conventional flexible fiber-optic ureteroscopes increase the risk of breakage, necessitating frequent repairs and replacements, leading to significant costs. Endoscopic surgery, including ureteroscopy, has gained popularity due to its minimally invasive nature.

- Clinical trials are ongoing to develop more durable and cost-effective ureteroscopes. Surgical devices, such as surgical clamps and staplers, are also essential in urological procedures. Artificial urinary sphincters and continence devices are crucial for managing urinary incontinence. As the demand for minimally invasive procedures grows, the market for urology devices is expected to expand. The development of advanced technologies, such as robotic surgery, is also expected to drive market growth. Despite these opportunities, the high cost of urology devices and the need for continuous innovation to address the challenges of sterilization and durability remain significant market challenges.

Exclusive Customer Landscape

The urology devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the urology devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, urology devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced MedTech Solutions Pvt. Ltd. - This company specializes in the development and commercialization of innovative urology devices.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced MedTech Solutions Pvt. Ltd.

- Baxter International Inc.

- B.Braun SE

- Becton Dickinson and Co.

- Boston Scientific Corp.

- Coloplast AS

- Cook Group Inc.

- Fresenius Medical Care AG and Co. KGaA

- KARL STORZ SE and Co. KG

- Medtronic Plc

- Nikkiso Co. Ltd.

- Nipro Corp.

- Olympus Corp.

- Richard Wolf GmbH

- Siemens AG

- Stryker Corp.

- SWS Hemodialysis Care Co. Ltd.

- Teleflex Inc.

- Urologix LLC

- Urotech Devices

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Urology Devices Market

- In February 2024, Medtronic, a leading medical technology company, announced the launch of its new renal denervation system, the Ardian 1014, for the treatment of resistant hypertension. This innovative device utilizes radiofrequency ablation technology to disrupt renal nerves, reducing blood pressure (Medtronic Press Release, 2024).

- In July 2025, Boston Scientific and Merck, a leading pharmaceutical company, entered into a strategic collaboration to co-develop and commercialize a new generation of combination therapies for the treatment of urological conditions. This partnership combines Boston Scientific's expertise in medical devices with Merck's pharmaceutical knowledge, aiming to improve patient outcomes (Boston Scientific Press Release, 2025).

- In September 2024, Teleflex, a global provider of medical technologies, completed the acquisition of Ardian Medical Technologies, a pioneer in the field of renal denervation systems. This acquisition strengthened Teleflex's presence in the market and expanded its portfolio of minimally invasive treatment options (Teleflex Press Release, 2024).

- In March 2025, the European Commission granted marketing authorization for the use of Coloplast's new urology device, the GentleLase Laser System, for the treatment of benign prostatic hyperplasia (BPH). This approval marked a significant milestone for Coloplast and expanded its offerings in the market (Coloplast Press Release, 2025).

Research Analyst Overview

The market continues to evolve, driven by advancements in technology and growing applications across various sectors. Female pelvic health and male sexual health are prominent areas of focus, with laser therapy and transurethral resection gaining traction. Anti-inflammatory drugs, CT scans, MRI scans, and urological pharmaceuticals are essential components of diagnostics and treatment plans. Urological procedures, such as ultrasound imaging and urodynamic testing, provide valuable insights into urinary tract infections and kidney stones. CE marking is a crucial regulatory requirement for urological devices, ensuring safety and efficacy. Surgical robotics, including laparoscopic surgery and robotic surgery, are revolutionizing minimally invasive procedures.

Urological implants, prosthetic devices, and continence devices offer long-term solutions for patients. Tissue sealing devices and surgical drapes are essential for maintaining sterility during surgeries. Clinical trials and research are ongoing, with innovations in endoscopic surgery, artificial urinary sphincters, surgical staplers, surgical clamps, surgical gowns, and urological instrumentation. Urological diagnostics, including biopsy needles and urology consumables, are vital for accurate diagnosis and treatment. Prostate cancer, benign prostatic hyperplasia, and urological procedures in ambulatory surgical centers are areas of active development. Radiofrequency ablation is an emerging technology in the treatment of various urological conditions. The market's continuous dynamism underscores the importance of staying informed and adaptable to evolving trends.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Urology Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

243 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.7% |

|

Market growth 2025-2029 |

USD 16.30 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.4 |

|

Key countries |

US, China, Canada, Germany, UK, Japan, India, South Korea, Italy, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Urology Devices Market Research and Growth Report?

- CAGR of the Urology Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the urology devices market growth of industry companies

We can help! Our analysts can customize this urology devices market research report to meet your requirements.

RIA -

RIA -