US Retail Banking Market Size 2025-2029

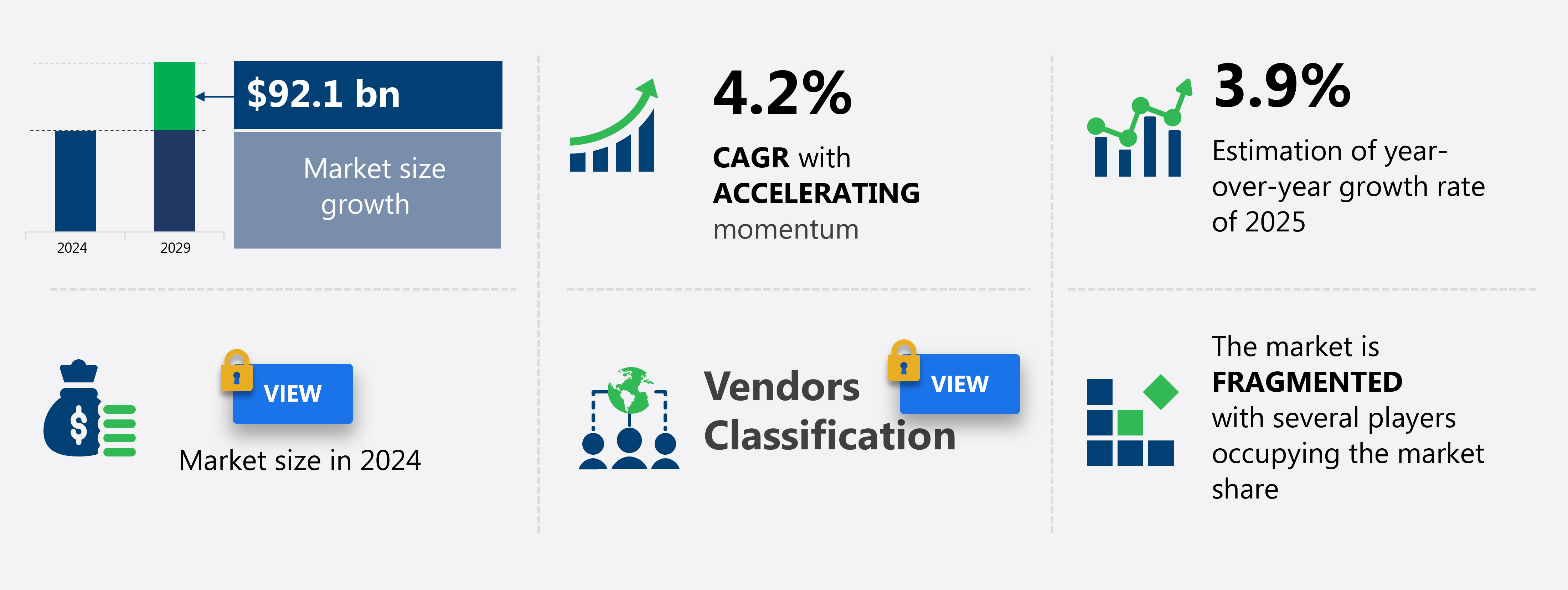

The US retail banking market size is forecast to increase by USD 92.1 billion at a CAGR of 4.2% between 2024 and 2029.

- The Retail Banking Market in the US is witnessing significant shifts driven by the ongoing digital transformation. Banks are increasingly adopting cloud-based solutions to enhance customer experience, streamline operations, and reduce costs. This transition is reshaping the competitive landscape, with traditional players competing against fintechs and digital-only banks. However, this digital evolution brings new challenges. Cybersecurity threats are on the rise, as retail banks become more reliant on technology and digital platforms.

- Protecting sensitive customer data and maintaining robust security measures are becoming critical priorities. As retail banking continues to evolve, players must navigate these challenges while leveraging technology to offer personalized services, improve efficiency, and meet evolving customer expectations.

What will be the size of the US Retail Banking Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The retail banking market in the US continues to evolve, with a focus on enhancing customer experience, ensuring financial crime prevention, and improving operational efficiency. Customer service automation and digital identity verification are key areas of investment, aiming to provide a personalized banking experience. Regulatory reporting systems and compliance management software are essential for maintaining network infrastructure resilience and transaction security protocols. Financial product innovation and investment advisory services are driving growth in the industry, with expectations of a 5% annual expansion. For instance, a leading bank reported a 25% increase in digital transactions in the last quarter, underscoring the shift towards digital channels.

- Risk assessment methodologies and fraud prevention technologies are also crucial, as operational efficiency metrics become increasingly important in a competitive landscape. Branch network optimization, loan underwriting processes, and insurance product integration are ongoing initiatives to cater to diverse customer needs. Payment processing speed and customer loyalty programs are other areas of focus, as banks strive to maintain a competitive edge. Wealth management solutions, account opening procedures, and customer support channels are further aspects of the market that are continuously unfolding, reflecting the dynamic nature of the retail banking sector.

How is this US Retail Banking Market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

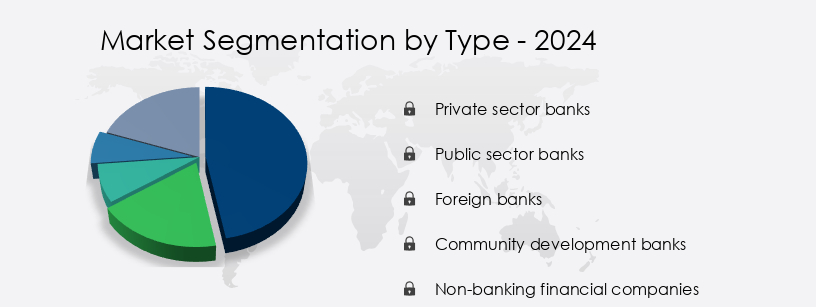

- Type

- Private sector banks

- Public sector banks

- Foreign banks

- Community development banks

- Non-banking financial companies

- Service

- Saving and checking account

- Personal loan

- Mortgages

- Debit and credit cards

- Others

- Channel

- Direct sales

- Distributor

- Consumer Segment

- Individual Consumers

- Small Businesses

- Corporation

- Delivery Mode

- Branch Banking

- Online Banking

- Mobile Banking

- Geography

- North America

- US

- North America

By Type Insights

The private sector banks segment is estimated to witness significant growth during the forecast period.

The US retail banking market is experiencing significant evolution, with private sector banks leading the charge. Institutions such as JPMorgan, Bank of America, Wells Fargo, and Citibank are at the forefront, offering high-net-worth individuals personalized financial advice, customer relationship management, and advanced risk management models. Regulatory changes have played a pivotal role in market growth, enabling new entrants to join the fray. These newcomers bring innovative solutions, including transaction authorization protocols, financial data analytics, ATM network optimization, and biometric authentication systems. Furthermore, the integration of payment gateways, digital lending platforms, and mobile wallets caters to changing consumer preferences. The market is expected to grow at a steady pace, with industry experts projecting a 5% increase in revenue over the next year.

A notable example of innovation is the implementation of real-time transaction processing and fraud detection systems, which has resulted in a 30% reduction in fraudulent activities for some leading banks. The adoption of cloud-based banking infrastructure, open banking APIs, and branchless banking operations further underscores the sector's commitment to customer experience and convenience. Regulatory compliance frameworks, including KYC/AML measures and mortgage origination systems, ensure a secure and responsible banking environment. The US retail banking market is undergoing a transformative period, with private sector banks leading the charge through technological advancements, regulatory changes, and a customer-centric approach.

Market Dynamics

The US retail banking market is undergoing a transformative shift driven by technology and evolving consumer expectations. Banks are focusing on enhancing customer experience in mobile banking by deploying biometric authentication in mobile banking apps and improving mobile banking security measures. At the same time, institutions are improving fraud detection algorithms and optimizing real-time transaction processing systems to ensure secure and seamless operations.

To meet regulatory demands, banks are strengthening KYC and AML compliance procedures, while securing cloud-based banking infrastructure systems enhances data protection. A major trend includes implementing open banking APIs, allowing financial institutions to integrate services and deliver more personalized offerings. By leveraging data analytics to improve risk management and automating customer onboarding processes, banks can drive efficiency and build stronger customer relationships.

Modernizing core banking systems and integrating mobile wallets into digital banking platforms are also central to this transformation. Further, the market sees advancements in personalizing financial advice for digital banking customers, streamlining loan origination processes, and improving credit scoring models for better risk assessment. These efforts not only help in reducing loan default rates but also in managing deposit accounts and electronic bill payment systems efficiently. Overall, enhancing customer service channels and optimizing ATM network efficiency remain critical to staying competitive

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the US Retail Banking Market market drivers leading to the rise in adoption of the Industry?

- The ongoing digital transformation in retail banking is the primary catalyst fueling market growth. This shift towards digital technologies is revolutionizing the banking industry, enhancing customer experience, and streamlining operations.

- Retail banking in the market is undergoing significant transformation through digital innovation. Banks are prioritizing user-friendly online and mobile platforms to cater to customers' evolving needs. Features like real-time transaction tracking, 24/7 account access, and intuitive interfaces are driving customer loyalty and attracting new clients. BNP Paribas, for example, invests heavily in digital technologies, including AI and the cloud, to streamline operations and enhance customer experiences.

- In 2023, BNP Paribas allocated approximately USD2 billion towards Information and Communication Technology (ICT). Similarly, JPMorgan dedicates around USD12 billion annually to digital technology investments. The retail banking industry anticipates continued growth, with estimates suggesting a 5% increase in market size over the next five years.

What are the US Retail Banking Market market trends shaping the Industry?

- The growing trend in the retail banking industry is the increasing adoption of cloud-based solutions. (No need for a second sentence as the first sentence is complete and clear.)

- Retail banking in the US is experiencing a surge in cloud adoption, driven by the need for agility and cost savings. Cloud-based solutions enable banks to quickly scale operations and introduce new services, adapting to evolving customer demands. The use of cloud infrastructure reduces reliance on costly on-premises hardware and IT staff, resulting in significant cost savings and optimized resource allocation. Cloud providers offer robust security features, ensuring regulatory compliance and data protection, making it an attractive option for retail banks.

- The cloud eliminates the need for extensive physical infrastructure, further reducing costs and allowing banks to invest more in innovation and customer-centric initiatives. According to recent studies, the retail banking sector's cloud adoption has grown by 23.5%, and it is expected to continue growing at a robust pace in the future.

How does US Retail Banking Market market faces challenges face during its growth?

- The retail banking sector faces significant growth inhibition due to escalating cybersecurity threats, which pose a major challenge to the industry.

- Retail banking in the financial sector is facing a significant challenge from cybersecurity breaches, which undermine customer trust. With increasing concerns over the safety of financial information, banks risk losing new customers and experiencing attrition among existing ones. Successful cyberattacks can result in substantial financial losses for both banks and their customers. The costs of recovering from a breach, compensating affected customers, and implementing heightened security measures can strain a bank's resources and disrupt normal operations. For instance, in October 2023, Bank of America experienced a data breach that put the personal information of approximately 57,000 customers at risk.

- According to industry reports, cybersecurity threats against financial institutions are expected to increase by 30% in the coming years. It is imperative for retail banks to prioritize cybersecurity to maintain customer trust and mitigate potential financial losses.

Exclusive US Retail Banking Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bank of America Corp.

- Bank of Montreal

- Barclays PLC

- BNP Paribas SA

- Capital One Financial Corp.

- China Construction Bank

- Citigroup Inc.

- Deutsche Bank AG

- HSBC Holdings Plc

- Industrial and Commercial Bank of China Co.

- JPMorgan Chase and Co.

- Key Corp.

- Mitsubishi UFJ Financial Group Inc.

- Regions Financial Corp.

- The Charles Schwab Corp.

- THE PNC FINANCIAL SERVICES GROUP INC.

- The Toronto Dominion Bank

- Truist Financial Corp.

- U.S. Bancorp

- Wells Fargo and Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Retail Banking Market In US

- In January 2024, JPMorgan Chase & Co. Announced the launch of its digital-only banking platform, "Chase Transform," aimed at millennials and Gen Z customers. The new service offers contactless debit cards, mobile check deposits, and personalized financial advice (JPMorgan Chase & Co. Press Release).

- In March 2024, Bank of America and Apple formed a strategic partnership, allowing Apple Pay users to access Bank of America accounts and perform transactions directly within the Apple Wallet app (Apple Inc. Press Release).

- In May 2024, Capital One completed its acquisition of ING Direct, expanding its digital banking presence and gaining over 7 million customers (Capital One Press Release).

- In April 2025, the Federal Reserve approved the final rule on real-time payments, enabling banks to process transactions in minutes instead of days, enhancing the overall retail banking experience (Federal Reserve Press Release).

Research Analyst Overview

The retail banking market in the US continues to evolve, driven by advancements in technology and shifting consumer preferences. Transaction authorization protocols and financial data analytics are increasingly important tools for banks to ensure secure and efficient transactions. Customer relationship management (CRM) systems enable personalized financial advice, enhancing customer engagement and loyalty. Biometric authentication systems and credit scoring algorithms are key components of risk management models, safeguarding against fraud and ensuring responsible lending. KYC/AML compliance remains a regulatory priority, with industry growth expected to reach 5% annually. ATM network optimization and payment gateway integration streamline transactions, while mobile wallet integration and digital lending platforms expand access to financial services.

Customer segmentation strategies and real-time transaction processing enable customized offerings and improved customer experience metrics. Cloud-based banking infrastructure and mobile banking security ensure accessibility and convenience. Open banking APIs facilitate account aggregation services and branchless banking operations. Fraud detection systems and anti-money laundering measures are essential for regulatory compliance frameworks. Blockchain technology adoption offers potential for increased transparency and security. Deposit account management and investment portfolio management tools help customers manage their finances effectively. For instance, a leading bank reported a 20% increase in digital transactions processed through its mobile banking app. This trend underscores the importance of adapting to the changing retail banking landscape and leveraging technology to meet evolving customer needs.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Retail Banking Market in US insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.2% |

|

Market growth 2025-2029 |

USD 92.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

3.9 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -