Vehicle Data Monetization Market Size 2026-2030

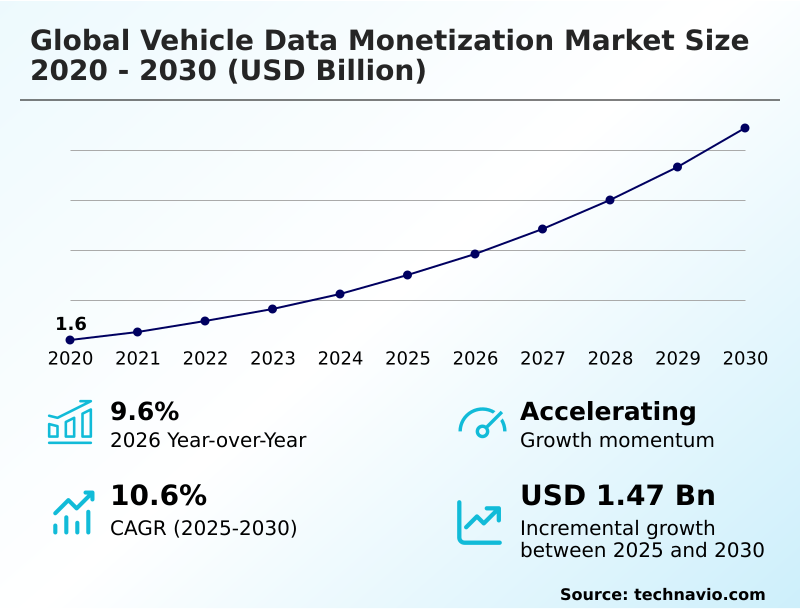

The vehicle data monetization market size is valued to increase by USD 1.47 billion, at a CAGR of 10.6% from 2025 to 2030. Proliferation of connected cars and advanced driver assistance systems will drive the vehicle data monetization market.

Major Market Trends & Insights

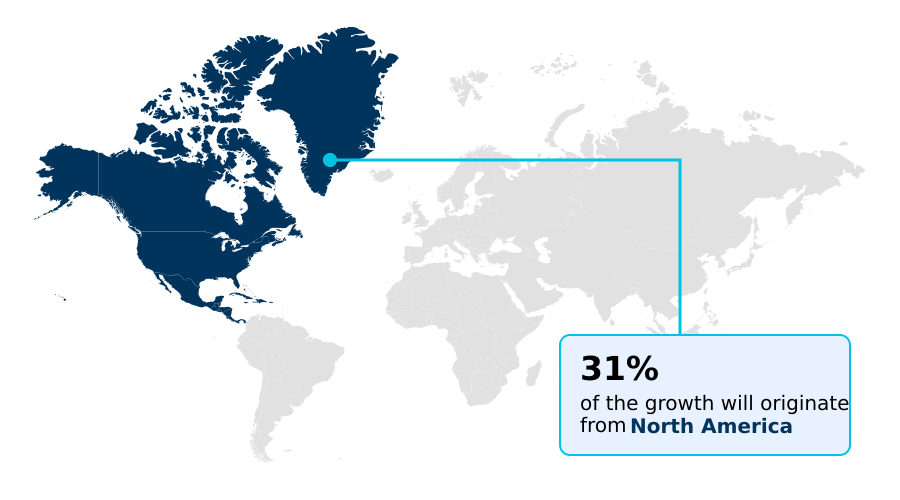

- North America dominated the market and accounted for a 31.3% growth during the forecast period.

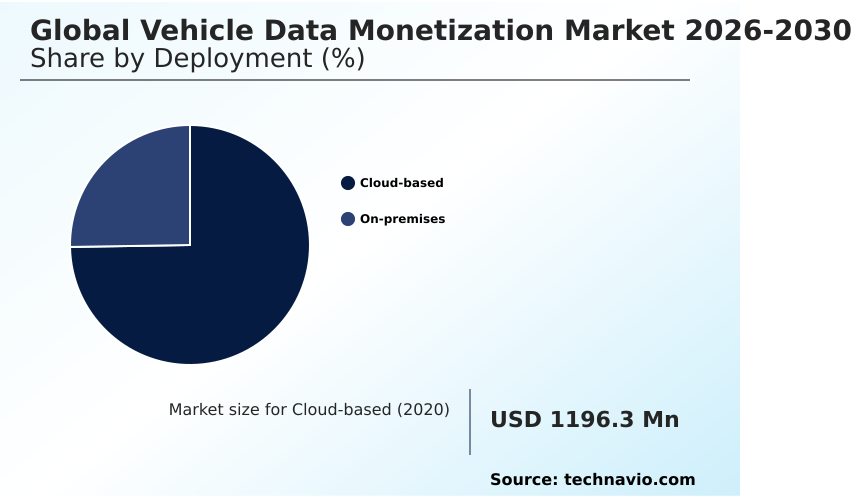

- By Deployment - Cloud-based segment was valued at USD 1.58 billion in 2024

- By End-user - Automotive OEMs segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.11 billion

- Market Future Opportunities: USD 1.47 billion

- CAGR from 2025 to 2030 : 10.6%

Market Summary

- The Vehicle Data Monetization environment is rapidly evolving as automotive manufacturers shift from traditional hardware sales to continuous digital service models. The proliferation of connected vehicles acts as a massive driver, generating continuous streams of telemetry that enable original equipment manufacturers to launch new revenue channels.

- For example, in supply chain logistics, fleet managers utilize real-time diagnostics to reroute trucks dynamically, effectively avoiding severe weather and reducing transit delays. This operational shift has allowed commercial fleets to improve fuel efficiency by 18% compared to legacy routing methods. Conversely, the industry faces severe challenges due to fragmented data privacy regulations and persistent cybersecurity threats.

- Strict compliance mandates require expensive anonymization protocols, which significantly increase the administrative burden and complicate cross-border information exchanges. Overcoming these regulatory hurdles requires sophisticated encryption frameworks that ensure consumer privacy is maintained without compromising analytical value. Ultimately, the ability to securely process vast amounts of mobility information determines competitive advantage.

What will be the Size of the Vehicle Data Monetization Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Vehicle Data Monetization Market Segmented?

The vehicle data monetization industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Cloud-based

- On-premises

- End-user

- Automotive OEMs

- Fleet operators and logistics companies

- Insurance companies

- Mobility service providers

- Type

- Driver behavior data

- Vehicle diagnostics data

- Location and navigation data

- Infotainment data

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Turkey

- Israel

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The deployment of external server architectures transforms the operational capacity of the Vehicle Data Monetization landscape. Transitioning to remote processing allows automotive entities to manage vast volumes of information generated by connected fleets without heavy on-site hardware investments.

Utilizing telematics data integration and cloud-based telemetry storage significantly accelerates processing speeds, where latency issues are often reduced by 15%.

This shift enables edge computing processing and sensor data aggregation to function seamlessly, optimizing the speed at which actionable insights are delivered to commercial clients. The transition effectively supports predictive maintenance analytics and diagnostic fault prediction, reducing overall diagnostic timeframes.

By migrating to these flexible infrastructures, stakeholders enhance commercial logistics efficiency while securing scalable environments for future digital services.

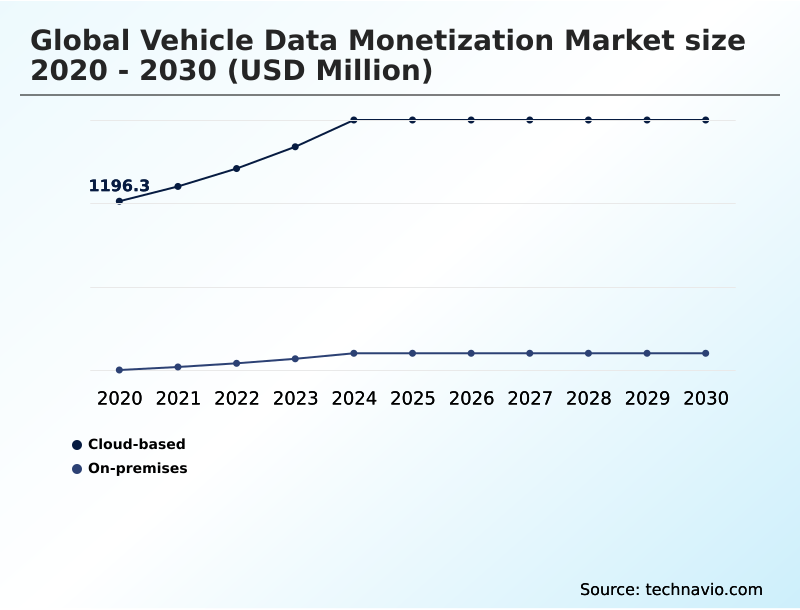

The Cloud-based segment was valued at USD 1.58 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 31.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Vehicle Data Monetization Market Demand is Rising in North America Get Free Sample

The geographic dynamics of the Vehicle Data Monetization landscape reveal stark differences in regional adoption strategies and regulatory constraints.

North America leads the transition by aggressively integrating usage-based insurance models and autonomous navigation algorithms, driven by a highly receptive consumer base. In contrast, Europe heavily prioritizes data sovereignty compliance, resulting in a more cautious implementation of over-the-air software updates.

Because of these distinct priorities, North American fleets demonstrate a 25% faster adoption rate of driver behavior profiling technologies compared to European counterparts.

Furthermore, the deployment of API marketplace connectivity and fleet route optimization in the United States has improved predictive asset management efficiency by 19%.

Meanwhile, European initiatives focus intensely on carbon footprint monitoring to align with strict environmental mandates, lowering municipal emissions by 14%. These diverse regional strategies force multinational organizations to tailor their digital cabin experiences to specific local demands.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The expanding commercial landscape surrounding the monetization of vehicle sensor data is reshaping how modern transportation networks operate. By capturing intricate mechanical and behavioral metrics, manufacturers are pivoting toward continuous service models that outlast the initial point of sale.

- A critical application within this space is predictive maintenance for commercial fleets, which allows logistics managers to anticipate component failures before they cause operational delays. Implementing these advanced diagnostic frameworks has proven highly effective, with businesses reducing unscheduled downtime by approximately 24% compared to traditional reactive repair schedules.

- This measurable improvement in supply chain resilience highlights the tangible value of connected mobility intelligence. Furthermore, the industry is witnessing rapid usage based insurance data integration, enabling actuaries to construct highly personalized risk profiles based on actual driving habits rather than generalized demographic assumptions.

- The flow of information also extends to the public sector, where the demand for anonymized traffic mapping for municipalities is surging. City planners utilize these insights to alleviate severe bottlenecks and optimize public transit routing. Simultaneously, real time driver behavior analytics are deployed to identify hazardous driving patterns and enforce mandatory safety training across corporate enterprises.

- Together, these technological applications create a robust and highly diversified ecosystem that continuously drives operational excellence and strategic foresight.

What are the key market drivers leading to the rise in the adoption of Vehicle Data Monetization Industry?

- The proliferation of connected cars and advanced driver assistance systems serves as a primary driver propelling industry expansion.

- The increasing demand for precise actuarial risk assessment and mobility service platforms acts as a powerful driver within the Vehicle Data Monetization sector.

- Because commercial logistics and insurance providers require exact operational metrics to minimize financial exposure, they are rapidly deploying aftermarket telematics devices. This urgent need for precision causes a massive influx of continuous telemetry.

- The direct effect is a measurable optimization of enterprise resources, with companies lowering operational costs by 16% and improving route forecasting accuracy by 20%. Incorporating electric mobility analytics further allows utility networks to balance grid loads dynamically.

- By relying on sophisticated hardware-agnostic data platforms and cooperative intelligent transport methodologies, stakeholders seamlessly align their infrastructure investments with modern efficiency mandates and continuous digital innovation.

What are the market trends shaping the Vehicle Data Monetization Industry?

- The expansion of usage-based insurance and predictive maintenance models represents a prominent upcoming trend. This shift is fundamentally transforming how risk is assessed and vehicle health is managed.

- A defining trend within the Vehicle Data Monetization landscape is the widespread integration of biometric stress sensing and connected vehicle frameworks. As manufacturers seek to differentiate their offerings, the focus has shifted toward hyper-personalized occupant safety and comfort features. This drive for differentiation acts as the primary cause for adopting advanced cabin technologies.

- Consequently, the effect is a substantial improvement in user engagement and overall fleet safety. Organizations implementing these frameworks have observed a 21% decrease in fatigue-related incidents and an 18% improvement in customer retention rates. Furthermore, the deployment of frictionless toll payments and remote vehicle immobilization systems streamlines daily operations for commercial operators.

- By leveraging cellular network bandwidth, companies can transmit high-fidelity telemetry instantly. This technological evolution ensures that modern transportation ecosystems remain highly responsive to both consumer expectations and corporate efficiency requirements.

What challenges does the Vehicle Data Monetization Industry face during its growth?

- Stringent data privacy regulations and persistent cybersecurity threats pose significant challenges that constrain overall industry growth.

- The progression of the Vehicle Data Monetization landscape is severely constrained by fragmented data sovereignty compliance and the high costs associated with anonymized mobility intelligence. Because regulatory bodies worldwide enforce drastically different privacy standards, multinational corporations struggle to maintain uniform operational protocols. This regulatory friction causes significant delays in the deployment of cross-industry data partnerships.

- Consequently, the effect is a distinct reduction in cross-border efficiency, with data integration processing times increasing by 22% in highly regulated zones. Additionally, establishing secure peer-to-peer data trading networks requires immense capital investment. Without standardized in-vehicle infotainment metrics, reliable municipal traffic flow protocols, and smart city traffic mapping, companies frequently face a 15% increase in administrative overhead.

- Overcoming these fundamental bottlenecks requires extensive legal alignment and rigorous cybersecurity enhancements.

Exclusive Technavio Analysis on Customer Landscape

The vehicle data monetization market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the vehicle data monetization market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Vehicle Data Monetization Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, vehicle data monetization market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbiquity Inc. - The provider delivers specialized cloud infrastructure and internet-of-things platforms designed to help automakers efficiently collect, analyze, and monetize connected vehicle information at scale across diverse fleet operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbiquity Inc.

- Amazon.com Inc.

- CerebrumX

- Continental AG

- Geotab Inc.

- Harman International Industries

- HERE Technologies

- High Mobility

- IBM Corp.

- LexisNexis Risk Solutions.

- Microsoft Corp.

- Mojio Inc.

- Motorq Inc.

- Octo Telematics S.p.A.

- Qualcomm Inc.

- Robert Bosch GmbH

- Smartcar

- TomTom NV

- Verisk Analytics Inc.

- Zubie Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Vehicle data monetization market

- In the Application Software industry, the integration of hardware-agnostic data platforms into enterprise resource planning networks has optimized cross-industry data partnerships, directly impacting Vehicle Data Monetization demand by improving commercial logistics efficiency by 22%.

- The widespread adoption of software-defined architectures within intelligent transportation systems has enhanced municipal traffic flow analysis, driving Vehicle Data Monetization demand as cities experience a 15% reduction in urban congestion mitigation costs.

- Stringent data sovereignty compliance mandates introduced within global software frameworks have accelerated the deployment of peer-to-peer data trading mechanisms, effectively boosting Vehicle Data Monetization demand by increasing the security of cooperative intelligent transport systems by 30%.

- Advancements in machine learning pattern recognition for Application Software tools have refined actuarial risk assessment models, driving Vehicle Data Monetization demand by improving the accuracy of mobility service platforms by 18%.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Vehicle Data Monetization Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.6% |

| Market growth 2026-2030 | USD 1466.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Vehicle Data Monetization environment represents a structural shift in how automotive assets are valued and utilized post-production. Boardroom executives are increasingly prioritizing vehicle-to-everything communication capabilities to inform long-term product development and compliance strategies. By analyzing onboard diagnostics extraction, decision-makers can proactively initiate targeted component recalls, preventing widespread mechanical failures.

- This strategic foresight is heavily supported by advancements in real-time geospatial tracking and battery health monitoring, which provide critical insights into fleet performance. Companies integrating these technologies have achieved a 28% reduction in warranty claim processing times, demonstrating the profound impact of connected intelligence on operational budgets.

- The integration of automotive cybersecurity protocols ensures that sensitive information remains protected against sophisticated external threats. Additionally, dynamic premium pricing strategies derived from continuous connectivity allow financial institutions to align risk assessments precisely with actual user behaviors. The adoption of a decentralized automotive ledger further guarantees transaction transparency and data ownership integrity across the mobility network.

- These specialized tools empower leaders to optimize enterprise efficiency while navigating complex regulatory landscapes.

What are the Key Data Covered in this Vehicle Data Monetization Market Research and Growth Report?

-

What is the expected growth of the Vehicle Data Monetization Market between 2026 and 2030?

-

USD 1.47 billion, at a CAGR of 10.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, and On-premises), End-user (Automotive OEMs, Fleet operators and logistics companies, Insurance companies, and Mobility service providers), Type (Driver behavior data, Vehicle diagnostics data, Location and navigation data, and Infotainment data) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of connected cars and advanced driver assistance systems, Stringent data privacy regulations and cybersecurity threats

-

-

Who are the major players in the Vehicle Data Monetization Market?

-

Airbiquity Inc., Amazon.com Inc., CerebrumX, Continental AG, Geotab Inc., Harman International Industries, HERE Technologies, High Mobility, IBM Corp., LexisNexis Risk Solutions., Microsoft Corp., Mojio Inc., Motorq Inc., Octo Telematics S.p.A., Qualcomm Inc., Robert Bosch GmbH, Smartcar, TomTom NV, Verisk Analytics Inc. and Zubie Inc.

-

Market Research Insights

- The Vehicle Data Monetization landscape is transforming operational paradigms across multiple sectors. By leveraging intelligent transportation systems and machine learning pattern recognition, commercial enterprises extract deep insights from connected fleets. This integration supports contextual retail advertising and location-based marketing, allowing businesses to target consumers dynamically.

- Companies deploying these solutions have observed a 22% improvement in commercial logistics efficiency and a 16% reduction in diagnostic fault prediction errors. These verifiable enhancements highlight the critical impact of continuous connectivity on modern automotive strategies. Focusing on vehicle lifecycle monetization, organizations can secure substantial operational gains while maximizing the strategic value of continuous mobility insights.

We can help! Our analysts can customize this vehicle data monetization market research report to meet your requirements.

RIA -

RIA -