Water Coolers Market Size and Growth Forecast 2026-2030

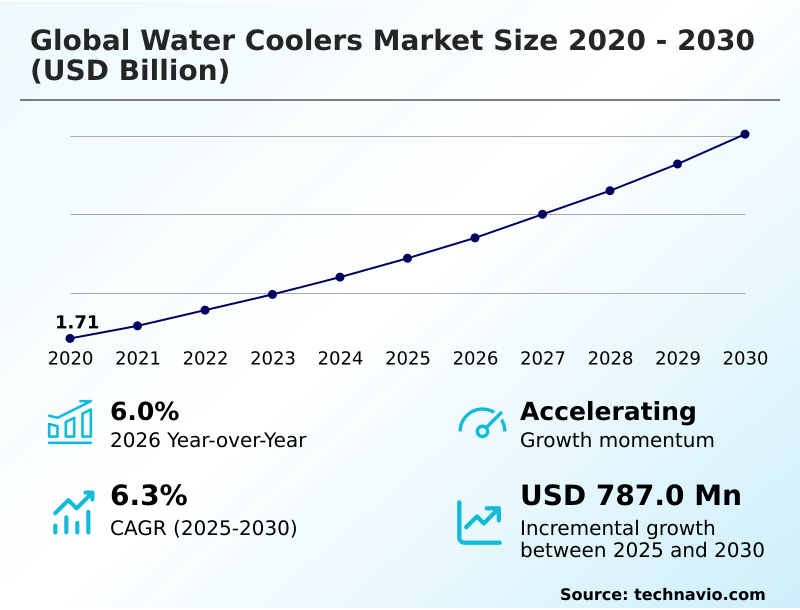

The Water Coolers Market size was valued at USD 2.22 billion in 2025 growing at a CAGR of 6.3% during the forecast period 2026-2030.

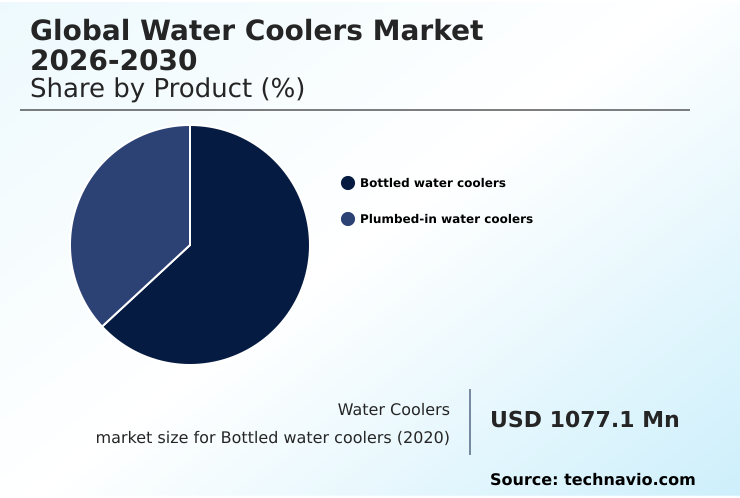

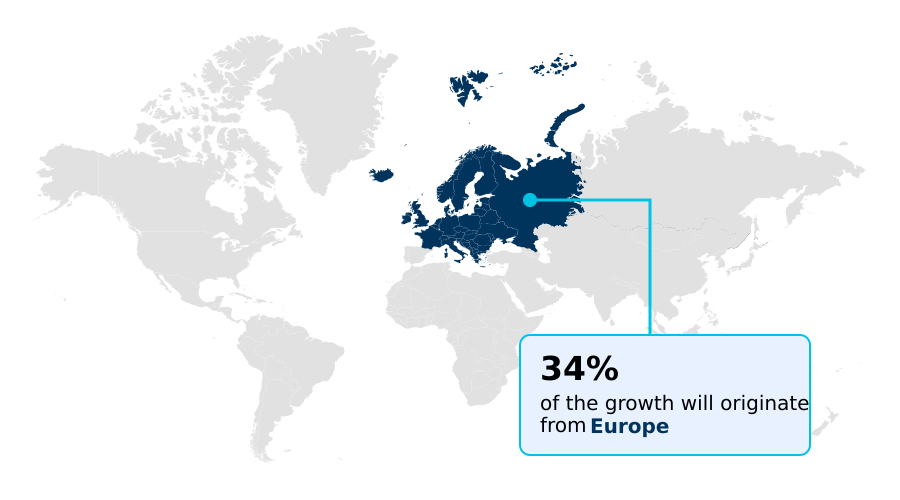

Europe accounts for 34.1% of incremental growth during the forecast period. The Bottled water coolers segment by Product was valued at USD 1.29 billion in 2024, while the Commercial segment holds the largest revenue share by Application.

The market is projected to grow by USD 1.30 billion from 2020 to 2030, with USD 787 million of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Water Coolers Market Overview

The water coolers market is evolving beyond simple hydration, driven by demands for sustainability and advanced water treatment. Corporate wellness programs now routinely specify high-performance integrated purification systems as a standard workplace amenity. A key driver is the transition toward point-of-use systems that eliminate plastic waste. For instance, a large corporate campus in Europe, aligning with EU Green Deal objectives, replaced its fleet of bottled dispensers with a network of plumbed-in systems. These IoT-enabled dispensers feature multi-stage filtration, including reverse osmosis filtration and UV sanitization, providing real-time data analytics on consumption and quality back to the central building management systems. This strategic shift not only reduced the facility's carbon footprint but also lowered operational expenditures associated with water delivery and storage. This move toward intelligent, networked public hydration infrastructure is indicative of the broader market direction, where connectivity and purification performance are paramount. The market is projected to grow by USD 787.0 million between 2025 and 2030.

Drivers, Trends, and Challenges in the Water Coolers Market

Strategic decision-making in the water coolers market hinges on a complex interplay of upfront capital versus long-term operational expenditures, particularly evident in the point-of-use vs bottled water cooler TCO analysis.

A facility manager for a large hospital, for instance, must evaluate the high initial investment for a network of plumbed-in systems against the recurring costs and logistical burdens of a bottled water service. The adoption of IoT integration for remote water cooler management allows for predictive maintenance and filter replacement scheduling, significantly improving operational efficiency and hygiene.

Furthermore, the challenge of advanced filtration for emerging water contaminants like PFAS necessitates investment in systems with nanotechnology filtration or reverse osmosis, moving beyond standard carbon block filters. This is compounded by the need to comply with evolving energy efficiency standards for commercial appliances, such as those outlined in Australia's GEMS program.

The use of sustainable materials in water cooler manufacturing is also becoming a key vendor qualification criterion, especially for corporations with ESG mandates. Finally, navigating regulatory compliance for direct potable reuse systems, as seen with Arizona's Aquifer Protection Permit rule, requires dispensers with robust, multi-stage purification capabilities to ensure safety at the tap.

This landscape shows a market where technological sophistication and regulatory adherence are inextricably linked.

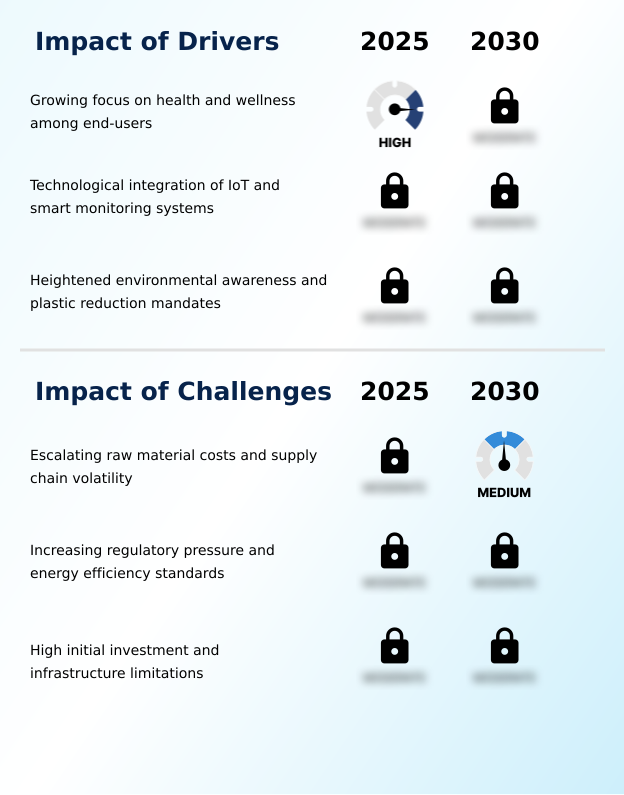

Primary Growth Driver: A growing focus on health and wellness among end-users is a key driver for the market.

The market's growth is fundamentally driven by a global focus on sustainability and health.

The urgent need for single-use plastic reduction is accelerating the transition from bottled delivery models to permanent public hydration infrastructure, particularly bottleless water coolers and point-of-use systems.

This shift is reinforced by corporate sustainability initiatives, where the carbon footprint of water logistics is under intense scrutiny. Consequently, businesses are prioritizing plumbed-in systems that offer advanced water treatment on-site.

The growing emphasis on workplace wellness initiatives further fuels this trend, with employers investing in high-quality hydration to support employee health and productivity.

The integration of IoT technology in these systems enhances operational efficiency, providing data that supports both sustainability reporting and maintenance scheduling, making it a cornerstone of modern corporate wellness programs.

Emerging Market Trend: The expansion of premium, multi-functional, and high-capacity dispensing systems defines a primary market trend.

Key trends are reshaping product design, moving beyond basic chilling to encompass integrated wellness and sustainability features. The market is seeing a diversification toward multi-functional dispensing, with high-end commercial units now offering sparkling water dispensers and ambient options alongside traditional hot and cold. This premiumization aligns with corporate wellness programs aimed at enhancing the workplace environment.

Technologically, the adoption of smart sensing capabilities is enabling features like touchless dispensing, which has become a standard for hygienic hydration solutions. Furthermore, advancements in nanotechnology filtration are addressing growing concerns over water purity, with systems now capable of advanced PFAS removal at the point of use.

This shift toward more sophisticated, integrated purification systems is a direct response to consumer and commercial demand for higher safety standards and enhanced user experience.

Key Industry Challenge: Escalating raw material costs and supply chain volatility present a key challenge to industry growth.

The primary challenges facing the market are rooted in supply chain economics and intensifying regulatory pressures. Persistent supply chain volatility has led to escalating costs for critical raw materials like metals and polymers, directly impacting profit margins for manufacturers of both commercial and residential water coolers.

This forces a difficult choice between absorbing costs or raising prices, which can dampen demand. Simultaneously, governments are imposing stricter energy efficiency standards, such as Australia's GEMS Determination 2025, and environmental mandates.

While these regulations promote sustainability, they require significant R&D investment and can increase the total cost of ownership for end-users, creating a barrier to adoption, particularly for advanced point-of-use water purification systems that already carry a high initial investment.

Explore Full Market Dynamics Analysis Request Free Sample

Water Coolers Market Segmentation

The water coolers industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Product Segment Analysis

The bottled water coolers segment is estimated to witness significant growth during the forecast period.

The global water coolers market is segmented by product, application, distribution channel, and geography.

The bottled water coolers segment continues to hold a significant market position, accounting for over 60% of the market in 2024, favored for its minimal setup requirements and flexibility in environments without direct plumbing access.

These systems, including modern bottom-loading water coolers, provide essential hygienic hydration solutions.

However, a notable shift is occurring toward point-of-use systems as procurement decision-makers conduct total cost of ownership analyses that favor the long-term economic and environmental benefits of bottleless alternatives.

This dynamic is most pronounced in the commercial sector, which dominates market demand, while the residential segment shows increasing adoption of more compact countertop water coolers.

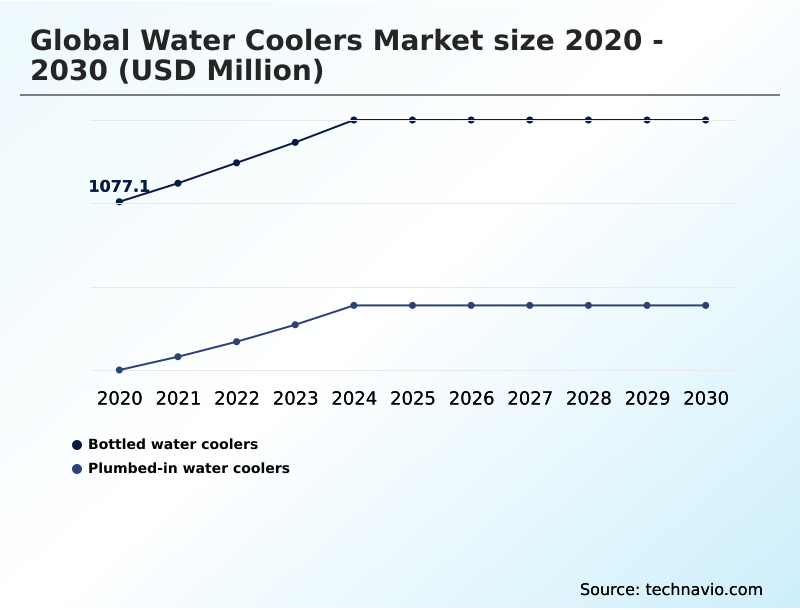

The Bottled water coolers segment was valued at USD 1.29 billion in 2024 and showed a gradual increase during the forecast period.

Water Coolers Market by Region: Europe Leads with 34.1% Growth Share

Europe is estimated to contribute 34.1% to the growth of the global market during the forecast period.

The geographic landscape of the water coolers market is diverse, with APAC poised to contribute the highest growth, driven by rapid urbanization and increasing health awareness in countries like India and China.

Europe is expected to contribute 34% of the market's growth, where stringent regulations such as the European Green Deal and a focus on single-use plastic reduction are accelerating the adoption of sustainable hydration solutions and plumbed-in systems.

In North America, which accounts for a significant market share, there is a strong trend toward residential water coolers and home water purification, driven by concerns over municipal water quality and an emphasis on wellness.

In Australia, the GEMS program's Commercial Ice-makers Determination 2025 reflects a broader regional push for energy-efficient appliances, influencing the design of high-capacity cooling units and other commercial water coolers.

Customer Landscape Analysis for the Water Coolers Market

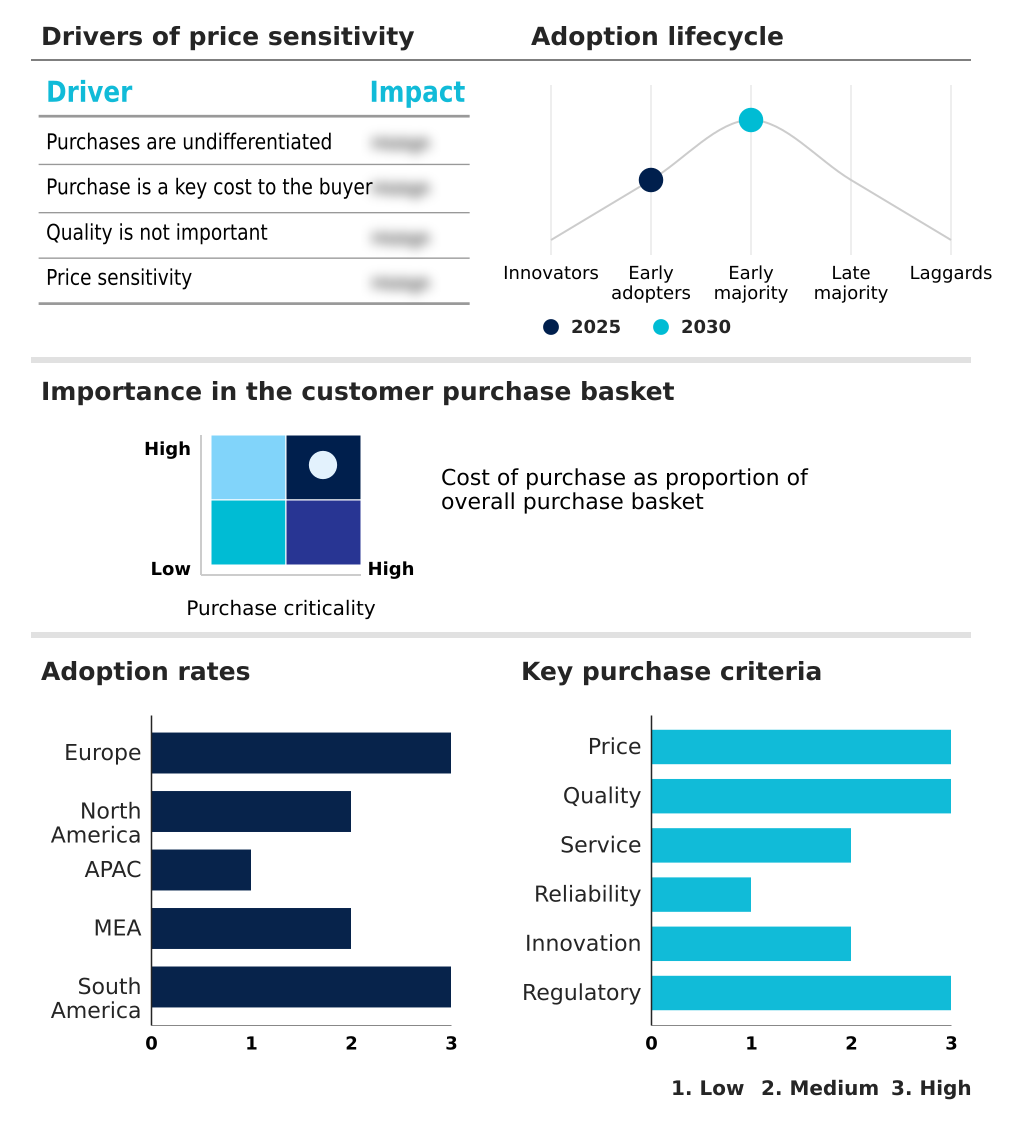

The water coolers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the water coolers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Water Coolers Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the water coolers market industry.

AB Electrolux - An established portfolio of water coolers includes tabletop and floor-standing models, addressing diverse commercial and residential appliance needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Electrolux

- Blue Star Ltd.

- Breville Group Ltd.

- Carrier Global Corp.

- Clover Co. Ltd

- Culligan International Co.

- Elkay Manufacturing Co.

- Haier Smart Home Co. Ltd.

- Honeywell International Inc.

- JNOD Group

- KENT RO Systems Ltd.

- LAMO Electrical Appliance Group

- Midea Group Co. Ltd.

- OASIS International

- Olansi Healthcare Co. Ltd.

- Pure Water Systems Inc.

- Sunrise Aquacooler

- Voltas Ltd.

- Waterlogic Holdings Ltd.

- Whirlpool Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Water Coolers Market

- In February, 2025, Blue Star Ltd. introduced a specialized range of water coolers in India that employ R290 refrigerant, a move designed to reduce the global warming potential of its cooling systems in line with international environmental standards.

- In March, 2025, Primo Water Corp. entered into a strategic technical alliance with Siemens to incorporate advanced sensor arrays and IoT capabilities into its high-capacity water dispensing units for corporate clients.

- In March, 2025, Culligan Quench, a subsidiary of Culligan International Co., expanded its North American service capabilities by acquiring Stonybrook Water Co., a Massachusetts-based supplier of point-of-use water and ice appliances for the commercial sector.

- In March, 2025, the Arizona Department of Environmental Quality finalized its Aquifer Protection Permit rule, a regulatory change that facilitates direct potable reuse of treated water and is expected to drive demand for advanced end-user purification systems from companies like Pure Water Systems Inc.

Research Analyst Overview: Water Coolers Market

From an analyst perspective, the water coolers market is at an inflection point where total cost of ownership and ESG compliance are steering capital investment. Boardroom decisions increasingly favor point-of-use systems, despite higher upfront costs, due to their alignment with corporate sustainability goals and the elimination of recurring bottled water contracts.

This is not merely a cost-saving measure but a strategic response to regulatory pressures like the EU's F-gas regulations, which mandate a shift toward eco-friendly refrigerants and energy-efficient compressors. The integration of BLDC motors and advanced power-saving modes is becoming standard.

For instance, a multinational corporation evaluating a refresh of its global office infrastructure must now weigh the operational benefits of IoT-enabled dispensers—offering remote maintenance monitoring and consumption data—against the complexities of a multi-regional rollout.

The market's growth, with Europe contributing over 34% of the forecast period's expansion, is directly tied to this convergence of technological readiness and regulatory imperative, making advanced water treatment and sustainable hydration solutions central to modern facility management.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Water Coolers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.3% |

| Market growth 2026-2030 | USD 787.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.0% |

| Key countries | France, UK, Germany, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Water Coolers Market: Key Questions Answered in This Report

-

What is the expected growth of the Water Coolers Market between 2026 and 2030?

-

The Water Coolers Market is expected to grow by USD 787 million during 2026-2030, registering a CAGR of 6.3%. Year-over-year growth in 2026 is estimated at 6.0%%. This acceleration is shaped by growing focus on health and wellness among end-users, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Bottled water coolers, and Plumbed-in water coolers), Application (Commercial, and Residential), Distribution Channel (Offline, and Online) and Geography (Europe, North America, APAC, Middle East and Africa, South America). Among these, the Bottled water coolers segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Europe, North America, APAC, Middle East and Africa and South America. Europe is estimated to contribute 34.1% to market growth during the forecast period. Country-level analysis includes France, UK, Germany, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is growing focus on health and wellness among end-users, which is accelerating investment and industry demand. The main challenge is escalating raw material costs and supply chain volatility, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Water Coolers Market?

-

Key vendors include AB Electrolux, Blue Star Ltd., Breville Group Ltd., Carrier Global Corp., Clover Co. Ltd, Culligan International Co., Elkay Manufacturing Co., Haier Smart Home Co. Ltd., Honeywell International Inc., JNOD Group, KENT RO Systems Ltd., LAMO Electrical Appliance Group, Midea Group Co. Ltd., OASIS International, Olansi Healthcare Co. Ltd., Pure Water Systems Inc., Sunrise Aquacooler, Voltas Ltd., Waterlogic Holdings Ltd. and Whirlpool Corp.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Water Coolers Market Research Insights

Market dynamics are increasingly shaped by technological integration and heightened hygiene standards. The demand for sensor-based dispensing and touchless water coolers has become a core expectation in commercial settings, reducing physical contact points and supporting public health objectives. This shift is compelling manufacturers to integrate advanced smart sensing capabilities for both user interaction and internal diagnostics.

Concurrently, the ability to ensure water purity at the final point of delivery is critical. Systems now incorporate sophisticated water quality monitoring tools that provide assurance to end-users, a key factor in both commercial and residential water coolers.

These intelligent systems are often designed to integrate with building management systems, allowing facility managers to oversee performance and maintenance schedules efficiently across an entire fleet of assets, thereby improving operational efficiency.

We can help! Our analysts can customize this water coolers market research report to meet your requirements.

RIA -

RIA -