Wine And Spirits Market Size 2026-2030

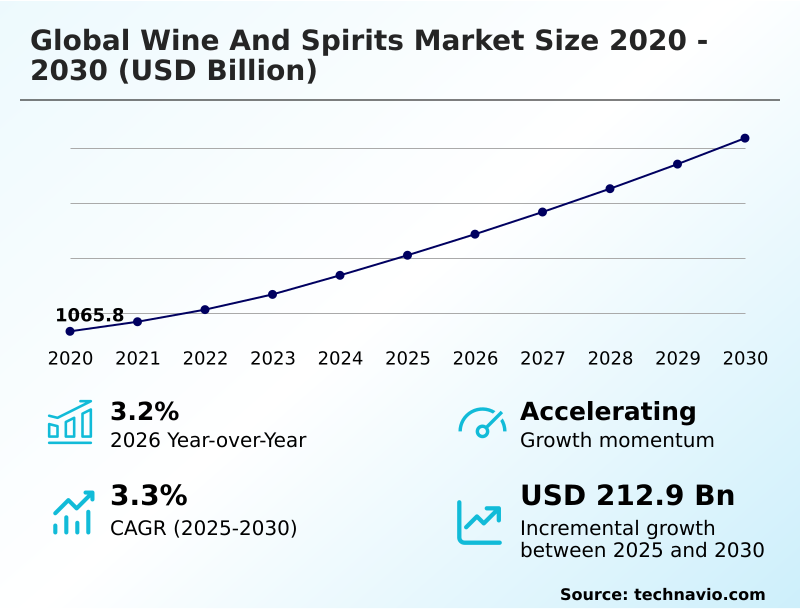

The wine and spirits market size is valued to increase by USD 212.9 billion, at a CAGR of 3.3% from 2025 to 2030. Increased demand for craft drinks will drive the wine and spirits market.

Major Market Trends & Insights

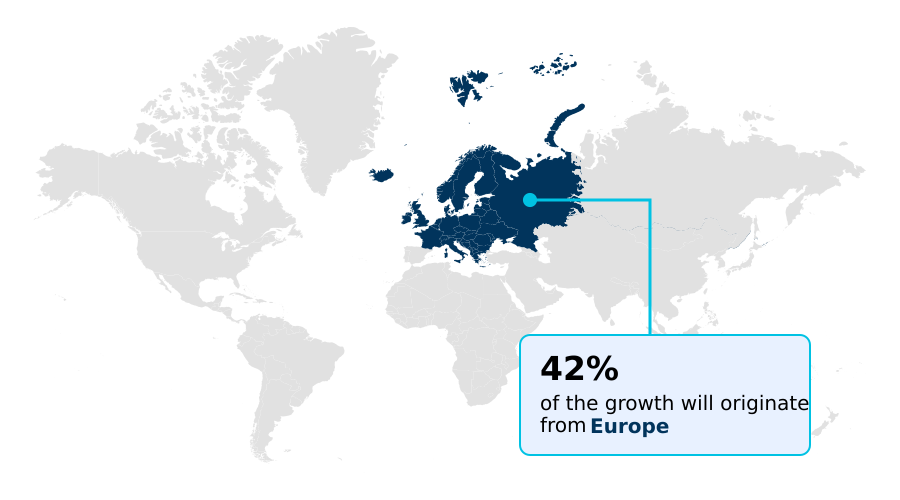

- Europe dominated the market and accounted for a 41.5% growth during the forecast period.

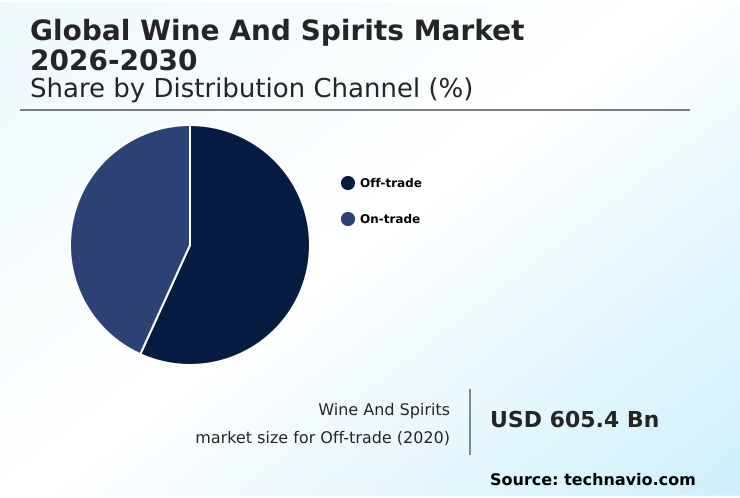

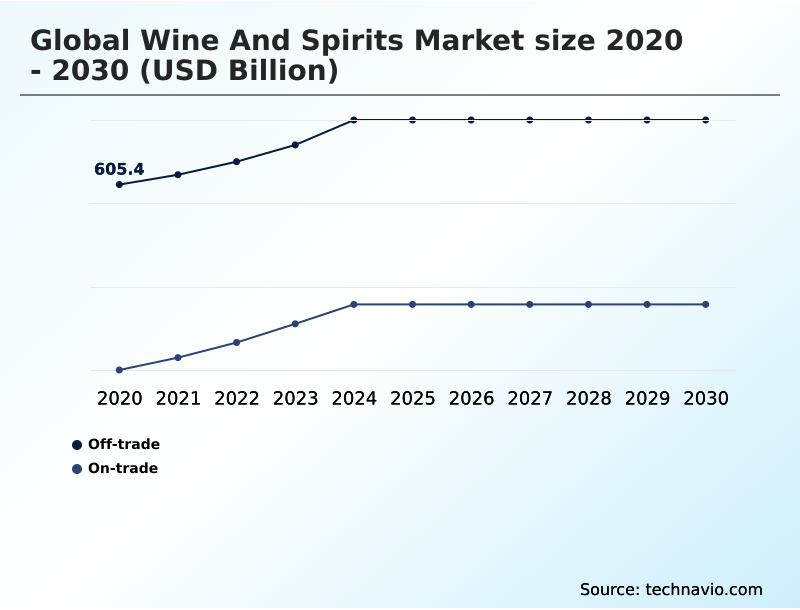

- By Distribution Channel - Off-trade segment was valued at USD 655.9 billion in 2024

- By Type - Spirits segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 351.2 billion

- Market Future Opportunities: USD 212.9 billion

- CAGR from 2025 to 2030 : 3.3%

Market Summary

- The wine and spirits market is undergoing a significant transformation, driven by the dual forces of premiumisation and diversification. Consumers are increasingly seeking products with strong product provenance, leading to a surge in demand for offerings from craft distillery and boutique winery operations that prioritize artisanal production methods and unique flavor profiling.

- This shift is compelling larger players to innovate beyond traditional portfolios, embracing everything from non-alcoholic spirits to ready-to-drink (RTD) cocktails. Technology plays a pivotal role, with advancements in viticulture practices and fermentation techniques improving quality and consistency.

- For instance, a producer might leverage data analytics for supply chain optimization, using predictive models to manage inventory of aging spirits and align production schedules with forecasted demand for specific appellation systems, thereby reducing holding costs and minimizing stockouts.

- Concurrently, the industry navigates challenges from evolving regulatory compliance and the growing moderation movement, compelling brands to invest heavily in brand storytelling and experiential marketing to maintain consumer engagement and fortify brand equity in a competitive landscape. This dynamic environment requires a strategic focus on both packaging innovation and efficient distribution agreements to capture discerning consumer segments.

What will be the Size of the Wine And Spirits Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Wine And Spirits Market Segmented?

The wine and spirits industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Off-trade

- On-trade

- Type

- Spirits

- Wine

- Packaging

- Glass bottles

- Cans

- Tetra packs

- Miniatures

- Kegs

- Geography

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- Europe

By Distribution Channel Insights

The off-trade segment is estimated to witness significant growth during the forecast period.

The off-trade channel, encompassing retail sales for off-premise consumption, is a cornerstone of the wine and spirits market. This segment, driven by evolving consumer preferences, includes supermarkets, liquor stores, and increasingly, e-commerce platforms that facilitate direct-to-consumer (DTC) sales.

The premiumisation trend is highly visible here, with shelf space dedicated to small batch production and artisanal brands that build significant brand equity.

Retailers are adapting their pricing strategy and distribution agreements to accommodate a diverse product mix, from ready-to-drink (RTD) cocktails to premium non-alcoholic spirits.

Digital marketing and sophisticated inventory management are critical for success, with some platforms reporting that private label brands now capture over 15% of sales in certain high-demand categories through targeted online promotions.

The Off-trade segment was valued at USD 655.9 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 41.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Wine And Spirits Market Demand is Rising in Europe Get Free Sample

The geographic landscape is defined by regional specificities in taste and regulation.

Europe, which contributes over 41% of incremental growth, remains a hub for traditional production, where established appellation systems and geographic indications (GI) dictate quality standards for products often subject to extended oak barrel aging and malolactic fermentation.

North America is a center for innovation in premium spirits, where charcoal filtration and cask strength expressions are gaining traction, with e-commerce platforms driving a 15% year-over-year increase in sales for this segment.

In APAC, the expansion of travel retail and duty-free sales channels is introducing a wider array of international brands.

Effective supply chain logistics and robust distribution agreements are crucial for navigating complex import regulations and securing intellectual property rights across these diverse markets, while techniques like cold stabilization and spirit proofing ensure product consistency.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The modern alcoholic beverage industry is a complex ecosystem where a brand's success is determined by a multitude of interconnected factors. The fundamental impact of terroir on wine quality remains a cornerstone of premium viticulture, yet the impact of climate change on viticulture is forcing producers to adapt.

- Concurrently, the rise of artisanal production is evident, though craft distillery startup costs present a significant barrier to entry. For those who succeed, the benefits of oak barrel aging for whiskey are crucial for developing complex flavors. In terms of market access, there's a clear divergence between on-trade versus off-trade sales channels.

- Firms that develop effective e-commerce strategies for wine brands and navigate direct-to-consumer wine shipping laws often report customer acquisition costs up to 20% lower than those relying on traditional retail. Technology's influence is pervasive, with the answer to how technology is changing wine production found in everything from automated fermentation to advanced analytics.

- The role of yeast in wine fermentation is being optimized, while new distillation techniques for craft gin are creating novel flavor profiles. This premiumisation strategy in the spirits industry is also fueling the growth drivers for ready-to-drink cocktails. However, brands face significant hurdles, including regulatory challenges in alcohol advertising and the need for robust strategies for preventing counterfeit alcohol.

- Understanding the consumer perception of organic wine and effectively marketing craft spirits to millennials are key to capturing emerging demographics, all while managing persistent supply chain challenges for imported spirits and evolving non-alcoholic spirit market trends. The importance of brand storytelling in wine marketing cannot be overstated in this crowded field.

What are the key market drivers leading to the rise in the adoption of Wine And Spirits Industry?

- A key driver propelling market growth is the heightened consumer demand for craft drinks, which emphasize authenticity and distinctive flavor profiles.

- The market is significantly driven by the consumer quest for authenticity and unique experiences, fueling the rise of the craft distillery and boutique winery.

- These smaller players emphasize artisanal production, leveraging specific terroir influence and sensory analysis to create distinctive products. The vibrant cocktail culture, influenced by global lifestyle trends, encourages constant new product development.

- Innovators are experimenting with unique yeast strains, maceration techniques, and aging methods, resulting in complex flavor profiling that commands premium pricing.

- Brands that successfully tap into this demand see tangible results; for instance, limited-edition releases often sell out 50% faster than standard offerings.

- A well-defined market entry strategy focused on this segment can yield a higher return on investment, as consumers demonstrate a clear preference for products with a compelling narrative and artisanal roots.

What are the market trends shaping the Wine And Spirits Industry?

- The increasing dependence on technology throughout the value chain is emerging as a defining market trend, shaping competitiveness and efficiency from production to distribution.

- Emerging trends are reshaping the market, with sustainability at the forefront. A growing consumer focus on product provenance and transparency is driving the adoption of organic certification and biodynamic farming. This aligns with broader health and wellness trends, influencing everything from viticulture practices to final packaging innovation.

- Producers leveraging track and trace solutions for their supply chain optimization report a 25% reduction in verification time for authenticity checks. The implementation of advanced fermentation techniques and distillation process monitoring has also improved resource efficiency by up to 15%.

- Brands that successfully weave these elements into their brand storytelling and consumer engagement strategies are building stronger connections, particularly through experiential marketing events that highlight their commitment to sustainable packaging and responsible production methods.

What challenges does the Wine And Spirits Industry face during its growth?

- Campaigns against alcohol consumption present a significant challenge, influencing regulatory landscapes and shifting consumer attitudes toward moderation.

- Navigating the complex web of market challenges is critical for sustained growth. Strict regulatory compliance remains a primary concern, with evolving advertising regulations and excise duties creating an unpredictable operating environment. These rules directly impact both the on-trade channel and off-trade sales.

- The growing moderation movement pressures producers to clearly label alcohol by volume (ABV) and sugar content, while the market for products with a lower proof rating expands. Internally, firms face the threat of market consolidation through mergers and acquisitions (M&A), which intensifies competition. Externally, robust measures for counterfeiting prevention are essential, as illicit products can erode brand trust.

- Companies that proactively adapt, for example by diversifying with low-ABV options, have seen up to a 10% faster growth in that sub-segment compared to those that do not.

Exclusive Technavio Analysis on Customer Landscape

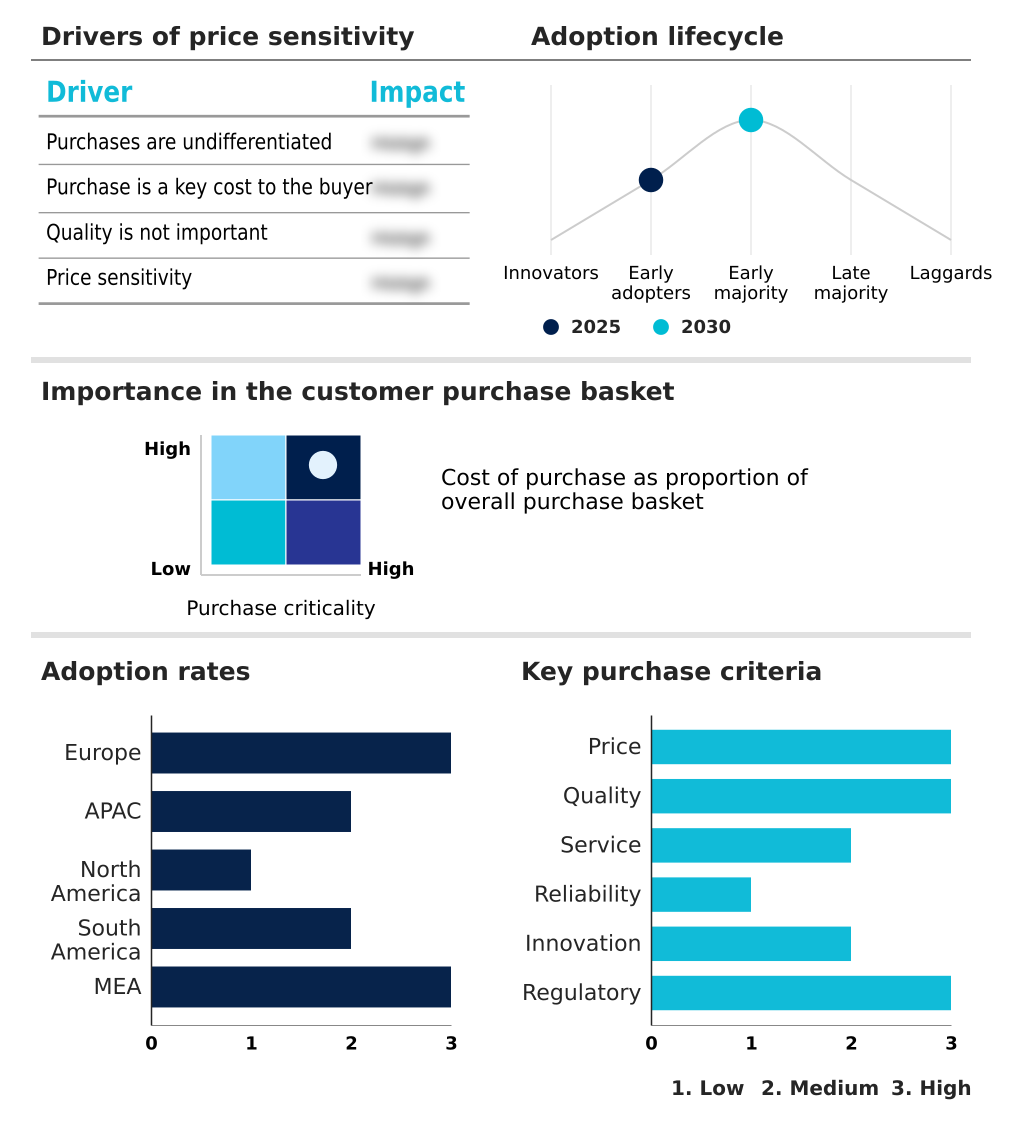

The wine and spirits market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wine and spirits market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Wine And Spirits Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, wine and spirits market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anheuser Busch InBev SA NV - A comprehensive portfolio of spirits and beer is offered, strategically focused on building brand equity within premium and super-premium categories for a diverse consumer base.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anheuser Busch InBev SA NV

- Bacardi and Co. Ltd.

- Bayadera Group

- Brown Forman Corp.

- Campari Group

- Constellation Brands Inc.

- Diageo PLC

- E. and J. Gallo Winery

- Familia Torres

- Globus Spirits Ltd.

- Hite Jinro Co. Ltd.

- LVMH Moet Hennessy

- Pernod Ricard SA

- Sula Vineyards Ltd.

- Suntory Beverage and Food Ltd.

- Thai Beverage Public Co. Ltd.

- The Wine Group LLC

- Treasury Wine Estates Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Wine and spirits market

- In May 2025, Piccadily Agro Industries Ltd. launched Cashmir, a premium small-batch organic vodka, to differentiate its brand in crowded spirits categories and target discerning consumers.

- In January 2025, Gallo announced an exclusive distribution agreement with Spritz Society to expand the brand's retail presence in major US grocery and retail stores, aiming for a nationwide rollout.

- In November 2024, Suntory Osaka Spirits and Liqueurs Craft Distillery was awarded the 2025 Liqueur Producer Trophy at the International Wine and Spirit Competition, highlighting product excellence and innovation.

- In September 2024, Indri Single Malt Indian Whisky expanded its global footprint by launching its limited-edition City Series in Dubai Duty Free, targeting affluent international travellers in key travel retail channels.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wine And Spirits Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 287 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.3% |

| Market growth 2026-2030 | USD 212.9 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.2% |

| Key countries | Germany, UK, Russia, France, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Brazil, Argentina, Chile, South Africa, Nigeria, UAE, Egypt and Saudi Arabia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The wine and spirits market exhibits continuous evolution, driven by a pronounced premiumisation trend and diversification into non-alcoholic spirits and ready-to-drink (RTD) cocktails. At the core, production excellence hinges on mastering the distillation process and specific fermentation techniques, including malolactic fermentation, while managing critical variables like yeast strains and sugar content.

- For boardroom strategy, the shift toward sustainable packaging and organic certification is no longer optional; it is a key decision impacting brand equity. Companies achieving third-party biodynamic farming validation report a 15% increase in consumer trust metrics.

- The journey from raw material to consumer involves meticulous viticulture practices, a defined vinification process, and precise aging methods like oak barrel aging, often within controlled appellation systems. Product integrity is maintained through cold stabilization, charcoal filtration, and other filtration methods, with final spirit proofing determining the alcohol by volume (ABV) and proof rating.

- The distinction between a craft distillery and a large-scale operation often lies in small batch production and unique maceration techniques.

- The entire system relies on resilient supply chain logistics, from sourcing glass bottle packaging to managing on-trade channel and off-trade channel distribution, including direct-to-consumer (DTC) sales, all while ensuring clear product provenance through sensory analysis and communicating value propositions like cask strength or the results of fortification process to a discerning consumer.

What are the Key Data Covered in this Wine And Spirits Market Research and Growth Report?

-

What is the expected growth of the Wine And Spirits Market between 2026 and 2030?

-

USD 212.9 billion, at a CAGR of 3.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Off-trade, and On-trade), Type (Spirits, and Wine), Packaging (Glass bottles, Cans, Tetra packs, Miniatures, and Kegs) and Geography (Europe, APAC, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, APAC, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increased demand for craft drinks, Campaigns against alcohol consumption

-

-

Who are the major players in the Wine And Spirits Market?

-

Anheuser Busch InBev SA NV, Bacardi and Co. Ltd., Bayadera Group, Brown Forman Corp., Campari Group, Constellation Brands Inc., Diageo PLC, E. and J. Gallo Winery, Familia Torres, Globus Spirits Ltd., Hite Jinro Co. Ltd., LVMH Moet Hennessy, Pernod Ricard SA, Sula Vineyards Ltd., Suntory Beverage and Food Ltd., Thai Beverage Public Co. Ltd., The Wine Group LLC and Treasury Wine Estates Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by shifting consumer preferences and lifestyle trends, forcing a re-evaluation of traditional business models. The moderation movement and health and wellness trends are not just niche concerns; they are compelling new product development toward lower-alcohol and premium non-alcoholic options.

- Success hinges on a sophisticated market entry strategy, supported by robust distribution agreements and a nuanced pricing strategy. E-commerce platforms have become critical, with data showing that targeted digital marketing campaigns can achieve a 25% higher conversion rate compared to broad-based advertising.

- Furthermore, implementing advanced track and trace solutions for counterfeiting prevention not only secures intellectual property rights but has also been shown to improve supply chain optimization, reducing losses by up to 10%. This environment favors agile companies that leverage brand storytelling and experiential marketing to foster direct consumer engagement.

We can help! Our analysts can customize this wine and spirits market research report to meet your requirements.

RIA -

RIA -