US Cochlear Implants Market Size 2025-2029

The US cochlear implants market size is forecast to increase by USD 415.5 million at a CAGR of 11.8% between 2024 and 2029.

- The Cochlear Implants Market in the US is driven by the rising prevalence of hearing loss, affecting an estimated 48 million Americans. This significant population presents a substantial market opportunity for cochlear implant providers. Technological advancements continue to shape the industry, with innovations in sound processing, wireless connectivity, and battery life extending the capabilities of cochlear implants. However, regulatory challenges pose a significant hurdle for market growth. Stringent regulatory requirements and lengthy approval processes can delay product launches and increase costs for manufacturers.

- Companies must navigate these complexities to bring new products to market and maintain a competitive edge. To capitalize on market opportunities and effectively address challenges, industry players should focus on continuous innovation, strategic partnerships, and robust regulatory compliance.

What will be the size of the US Cochlear Implants Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The Cochlear Implants market in the US is witnessing significant advancements, driven by the quest for improved quality of life for individuals with sensorineural hearing loss. Sound quality and tinnitus relief are key focus areas, with device manufacturers continually enhancing features to meet evolving patient needs. Surgical planning and therapy efficacy are critical components of the implant process, with mapping strategies and auditory processing playing essential roles in optimizing performance. Neural interface and patient satisfaction are also paramount, as is the design of electrode arrays for effective signal transmission and data acquisition.

- Clinical trials and long-term follow-up studies are ongoing to assess device programming and rehabilitation efficacy. Cochlear anatomy, implant activation, and post-operative care are also crucial aspects of the market, with adverse events and speech intelligibility remaining areas of concern for patients and healthcare providers alike.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Unilateral

- Bilateral

- Type

- Adult

- Pediatric

- End-user

- Hospitals

- Specialty clinics

- Ambulatory surgical centers

- Geography

- North America

- US

- North America

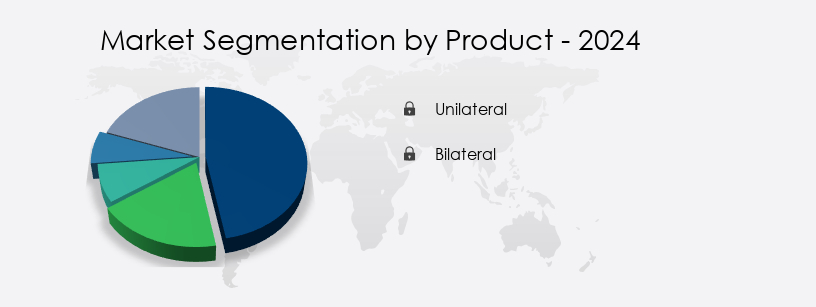

By Product Insights

The unilateral segment is estimated to witness significant growth during the forecast period.

Unilateral hearing loss, characterized by impairment in one ear while the other maintains near-normal hearing, affects approximately 60,000 individuals annually in the US according to the American Psychiatric Association Diagnostic and Statistical Manual of Mental Disorders. For those experiencing severe-to-profound hearing loss in one ear, unilateral cochlear implants have emerged as a viable solution. These implants offer significant advantages, particularly for patients with better hearing in one ear or those opting for a single implant due to financial constraints, insurance coverage, or surgical considerations. The market for unilateral cochlear implants in the US is thriving, driven by leading manufacturers offering advanced systems designed to optimize speech perception and sound clarity.

These systems incorporate various technologies such as auditory brainstem response testing to ensure implant candidacy, neural response telemetry for precise electrode placement, and implant mapping for individualized settings. Bilateral cochlear implants, while beneficial for individuals with bilateral hearing loss, may not be suitable for everyone. Unilateral implants offer an alternative, allowing patients to maintain their residual hearing in the normal ear and improving overall communication abilities. The implant longevity, a critical factor, is typically around 10-15 years, with advancements in technology continually extending this period. During cochlear implant surgery, electrical stimulation parameters are meticulously adjusted to optimize auditory nerve stimulation, while implant mapping ensures the best possible speech perception.

Post-surgery, patients undergo auditory training and rehabilitation protocols to maximize the benefits of the implant. Dynamic range, frequency selectivity, and noise reduction are essential features for effective speech perception. Signal processing algorithms, such as temporal resolution and microphone technology, enhance sound localization and music perception. Wireless communication and speech coding strategies enable seamless connectivity and customization. Despite advancements, challenges persist, including surgical complications and device failure rate. However, ongoing research focuses on improving electrode array design, acoustic coupling, and electroacoustic stimulation to address these concerns. In summary, the unilateral cochlear implant market in the US continues to evolve, offering innovative solutions for individuals with unilateral hearing loss.

Manufacturers invest in research and development to improve implant performance, ensuring better patient outcomes and enhanced quality of life.

The Unilateral segment was valued at USD 290.40 million in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the US Cochlear Implants Market drivers leading to the rise in adoption of the Industry?

- The increasing prevalence of hearing loss serves as the primary market driver.

- The Cochlear Implants market in the US is driven by the increasing prevalence of hearing loss among the population. According to the National Center for Health Statistics (NCHS), approximately 60.7 million Americans, or 15.5% of the adult population, experienced hearing loss in 2020. This number increases with age, affecting 31.1% of individuals aged 65 years and older and 40.3% of those aged 75 years and older. Presbycusis, or age-related hearing loss, is the most common type among older adults. Cochlear implants, a medical device used to restore hearing in individuals with severe to profound hearing loss, offer a viable solution.

- The implant consists of an external audio processor, which converts sound into electrical signals, and an electrode array that stimulates the auditory nerve. The device also includes features such as auditory brainstem response testing, surgical complications monitoring, implant mapping, neural response telemetry, and implant longevity assessment. Advancements in technology have led to improvements in auditory nerve stimulation and implant longevity. However, surgical complications remain a concern. Bilateral cochlear implants, which involve the implantation of two devices in both ears, have gained popularity due to their ability to provide better spatial hearing and improved speech recognition.

- In conclusion, the Cochlear Implants market in the US is driven by the increasing prevalence of hearing loss, particularly among older adults. The market offers various technological advancements, including auditory brainstem response testing, neural response telemetry, and implant mapping, to improve the efficacy and safety of the implants. However, surgical complications remain a challenge that requires ongoing research and development efforts.

What are the US Cochlear Implants Market trends shaping the Industry?

- The trend in the market is shaped by technological advancements. It is essential to stay informed about the latest innovations to remain competitive.

- The Cochlear Implants market in the US is witnessing significant growth due to advancements in technology. Innovations in this field are expanding the capabilities of cochlear implants, improving patient outcomes, and enhancing the overall user experience. For instance, MED-EL USA's SONNET 3 audio processor, recently approved by the FDA, is a testament to this progress. This lightweight and compact behind-the-ear processor offers seamless wireless direct streaming of music and calls from compatible devices, eliminating the need for additional accessories. Moreover, advancements in habilitation protocols and acoustic coupling techniques are contributing to better rehabilitation outcomes. Patients are now able to perceive a wider dynamic range, leading to improved speech and music perception.

- These advancements are making cochlear implants more accessible and beneficial for a broader range of individuals with hearing loss. Furthermore, research in the field of cochlear implants continues to focus on enhancing the user experience and optimizing patient outcomes. This includes ongoing studies on music perception, speech perception, and auditory training methods. The ultimate goal is to provide individuals with hearing loss with the most natural and effective hearing solution possible.

How does US Cochlear Implants Market face challenges during its growth?

- The growth of the industry is significantly impacted by regulatory challenges, which represent a key hurdle that professionals must navigate.

- The cochlear implants market in the US is subject to regulatory challenges that significantly impact market dynamics. Cochlear implants are classified as Class III Medical Devices by the US Food and Drug Administration (FDA), necessitating rigorous pre-market approval (PMA) processes. Manufacturers must conduct extensive clinical trials to demonstrate safety and efficacy, which can delay product launches. One of the primary regulatory hurdles is the protracted FDA approval process. Signal processing algorithms, temporal resolution, microphone technology, wireless communication, speech coding strategies, and electroacoustic stimulation are critical components of cochlear implant technology. However, the regulatory scrutiny of these aspects can add to the approval timeline and cost.

- Moreover, the FDA's stringent quality standards and post-market surveillance requirements further complicate the market entry process. These challenges necessitate significant investments in research and development, manufacturing, and regulatory compliance, potentially impacting the competitiveness of cochlear implant providers. In conclusion, the regulatory landscape in the US cochlear implants market presents significant barriers, influencing market growth and dynamics. Manufacturers must navigate these challenges to bring innovative and effective cochlear implant solutions to market, ensuring improved sound localization and implant candidacy for those with severe hearing loss.

Exclusive US Cochlear Implants Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Bionics AG

- Cochlear Ltd.

- Envoy Medical Corp.

- MED EL Medical Electronics.

- Medtronic Plc

- Oticon Medical AS

- ZHEJIANG NUROTRON BIOTECHNOLOGY CO. LTD.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cochlear Implants Market In US

- In January 2024, Cochlear Limited, a global leader in implantable hearing solutions, announced the FDA approval of its new Nucleus CI632 Cochlear Implant System. This advanced technology offers improved sound processing and wireless connectivity, enhancing the hearing experience for recipients (Cochlear Press Release, 2024).

- In March 2024, Advanced Bionics, a leading cochlear implant manufacturer, entered into a strategic partnership with the University of California, San Francisco (UCSF) to advance research and development in cochlear implant technology. The collaboration aims to explore new technologies and improve outcomes for recipients (Advanced Bionics Press Release, 2024).

- In April 2025, Med-El, a leading European cochlear implant manufacturer, secured a significant investment of ⬠100 million from its parent company, Sonova Holding AG. The funding will support the expansion of its production capacity and the development of new technologies (Med-El Press Release, 2025).

- In May 2025, the FDA granted marketing authorization for the new Cochlear Baha 6 Max Sound Processor, which offers advanced features and improved connectivity for individuals with conductive, mixed, or single-sided sensorineural hearing loss. This expansion of Cochlear's product portfolio strengthens its position in the US market (Cochlear Press Release, 2025).

Research Analyst Overview

The Cochlear Implants market in the US continues to evolve, driven by advancements in technology and expanding applications across various sectors. Auditory training and habilitation protocols are integral components of the implant process, ensuring optimal patient outcomes. Cochlear implant surgery, a critical stage, is continually refined through the development of new surgical techniques and implant longevity. Dynamic range and acoustic coupling are essential factors in speech perception and music perception, which are continually improving through signal processing algorithms, neural response telemetry, and implant mapping. Rehabilitation outcomes are enhanced by advancements in electrical stimulation parameters, speech processors, and hearing rehabilitation.

The market's ongoing dynamism is also reflected in the evolving nature of cochlear implant technology. Microphone technology, wireless communication, and speech coding strategies are among the areas undergoing significant advancements. Electrode array design, implant candidacy assessment, and electrical stimulation techniques are also subjects of ongoing research and development. Moreover, cochlear implant technology's continuous evolution is evident in the emergence of new features, such as noise reduction, frequency selectivity, and device failure rate reduction. These advancements contribute to the overall improvement of patient experiences and outcomes. In summary, the Cochlear Implants market in the US is characterized by continuous innovation and evolution, driven by advancements in technology and expanding applications across various sectors.

The focus on enhancing patient outcomes, improving speech and music perception, and refining surgical techniques and rehabilitation protocols is a key trend shaping the market's future direction.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cochlear Implants Market in US insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

151 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.8% |

|

Market growth 2025-2029 |

USD 415.5 million |

|

Market structure |

Concentrated |

|

YoY growth 2024-2025(%) |

11.0 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -