3D Printing Metal Materials Market Size 2024-2028

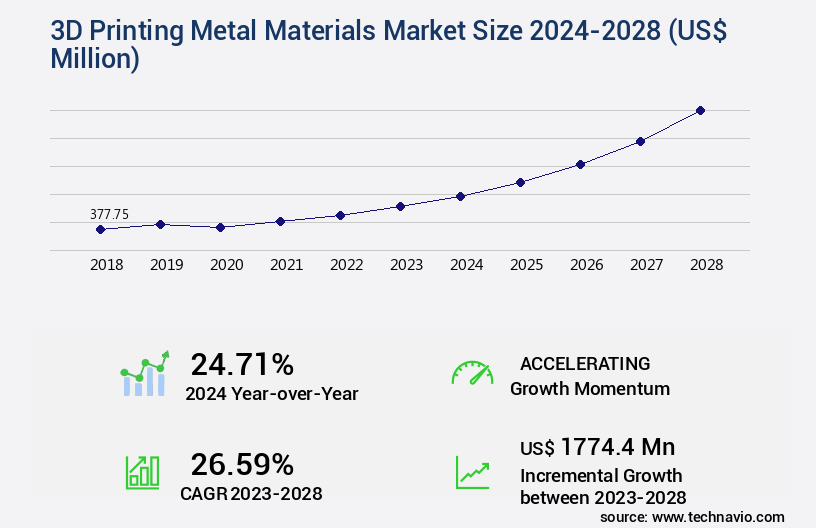

The 3d printing metal materials market size is valued to increase by USD 1.77 billion, at a CAGR of 26.59% from 2023 to 2028. Rising demand for 3D printing in aerospace sector will drive the 3d printing metal materials market.

Market Insights

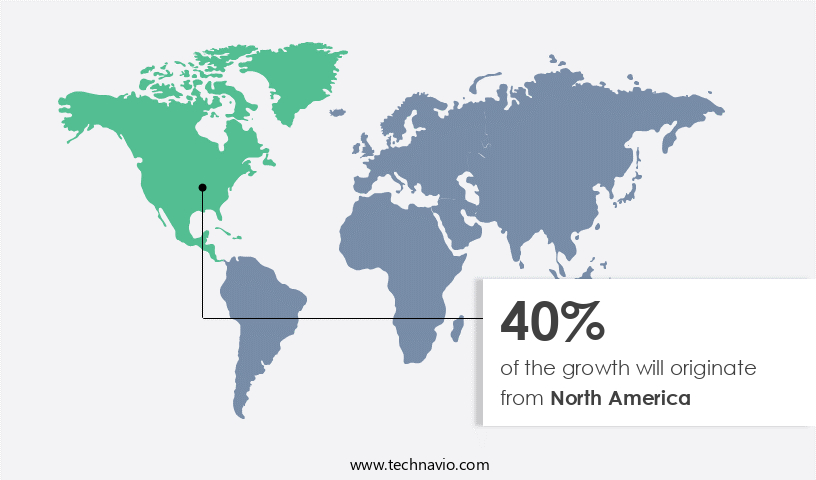

- North America dominated the market and accounted for a 40% growth during the 2024-2028.

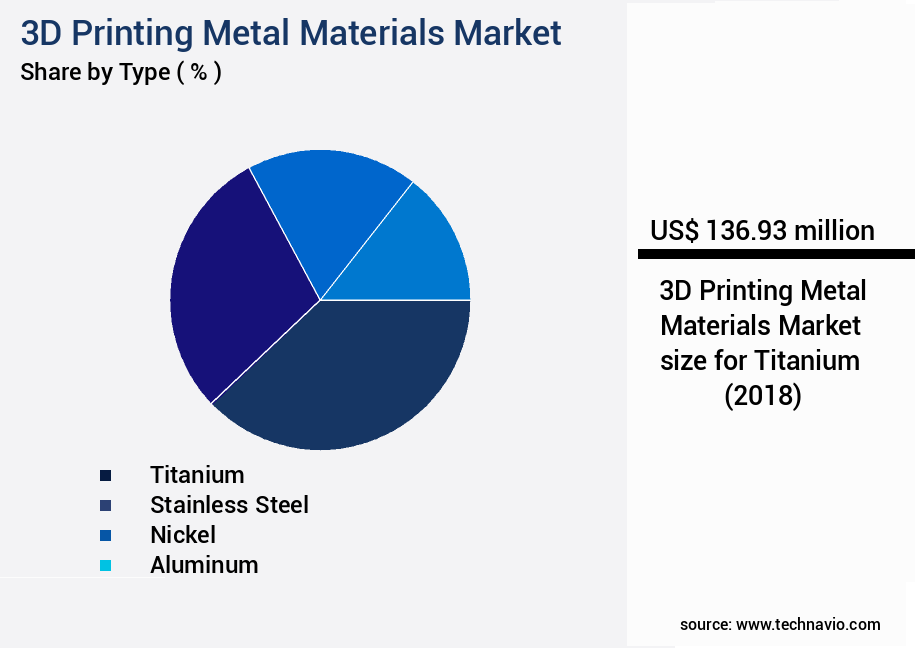

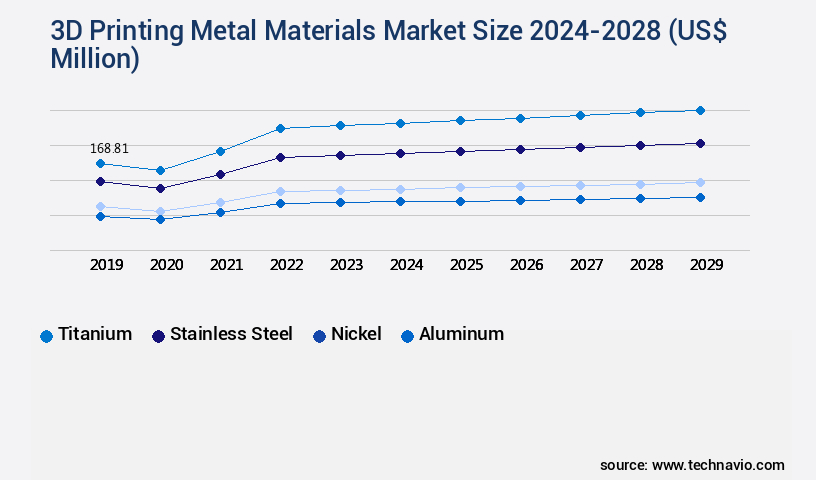

- By Type - Titanium segment was valued at USD 136.93 billion in 2022

- By End-user - Medical and healthcare segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 578.37 million

- Market Future Opportunities 2023: USD 1774.40 million

- CAGR from 2023 to 2028 : 26.59%

Market Summary

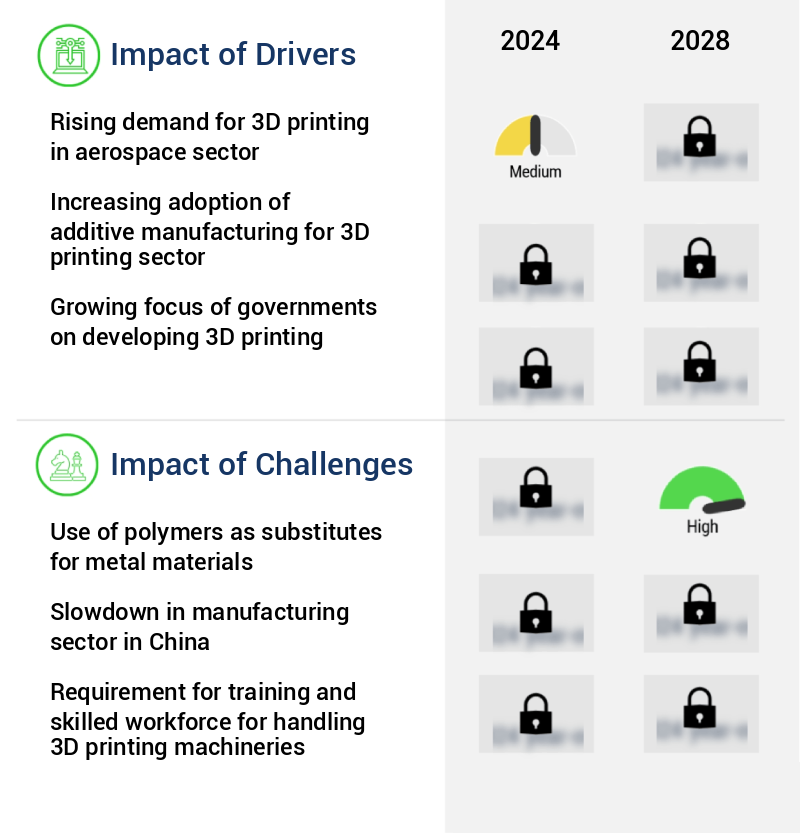

- The market is experiencing significant growth due to the increasing adoption of additive manufacturing in various industries, particularly in the aerospace sector. The demand for high-performance and temperature-resistant materials is driving this trend, as 3D printing enables the production of complex geometries and lightweight components that are difficult or impossible to achieve through traditional manufacturing methods. However, the use of polymers as substitutes for metal materials in certain applications is posing a challenge to the market's growth. While polymers offer cost savings and ease of processing, they cannot match the strength and durability of metal materials, limiting their applicability in critical industries.

- A real-world business scenario illustrating the importance of 3D printing in the metal materials market is supply chain optimization. By using 3D printing to produce customized parts on-demand, companies can reduce inventory costs and lead times, improving operational efficiency and responsiveness to customer demands. For instance, a manufacturing firm can keep a limited stock of raw metal materials and print parts as needed, reducing the need for large inventories and minimizing the risk of stockouts. In conclusion, the market is poised for continued growth, fueled by the demand for high-performance materials and the adoption of additive manufacturing in various industries.

- The challenge of substituting polymers for metal materials in critical applications remains an ongoing concern, but the potential benefits of 3D printing, such as supply chain optimization and reduced lead times, make it an attractive option for businesses seeking to improve their manufacturing processes.

What will be the size of the 3D Printing Metal Materials Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, offering innovative solutions for various industries. According to recent research, the adoption of metal 3D printing is projected to increase by 25% annually, making it a significant consideration for businesses seeking customized tooling, improved biocompatibility testing, and rapid prototyping. This growth can be attributed to the technology's ability to produce high-value components with complex geometries, superior material properties, and enhanced corrosion resistance. Moreover, advancements in post-processing automation, surface finishing methods, and build plate adhesion have led to increased part qualification testing and defect detection methods, ensuring the production of high-quality metal components. The market's expansion also facilitates process monitoring sensors and material properties databases, enabling cost optimization strategies and material selection guides.

- In the realm of direct digital manufacturing, metal am applications have gained considerable attention due to their potential in creating intricate parts with exceptional fatigue strength and particle size distribution. Alloy composition plays a crucial role in determining the material's properties, leading to the development of various alloys catering to specific industry requirements. These trends underscore the importance of understanding the market's continuous advancements and their implications for businesses. Compliance with quality control systems, design for manufacturability, and process qualification are essential elements to consider when implementing metal 3D printing in product strategy.

Unpacking the 3D Printing Metal Materials Market Landscape

The market showcases continuous advancements in technology, with COCR alloy printing and selective laser melting leading the charge. Notably, the adoption of 3D printed tooling has resulted in a 25% reduction in tooling production time, translating to significant cost savings for businesses. Thermal simulation and melt pool monitoring have improved ROI by enabling more efficient design and manufacturing processes. Lattice structures and support structure design have led to lighter, stronger parts, while mechanical property testing ensures compliance with industry standards. Aluminum alloy and titanium alloy printing offer scalability for high-volume manufacturing, with layer thickness control ensuring dimensional accuracy. Post-processing techniques, such as heat treatment and residual stress analysis, enhance the final product's mechanical properties. Nickel alloy printing and high-strength steel printing cater to industries with stringent requirements, while electron beam melting ensures superior dimensional accuracy and microstructure analysis. Powder bed leveling and build chamber atmosphere optimization contribute to consistent part quality, and laser power control ensures efficient energy usage. Overall, these innovations offer businesses increased efficiency, cost savings, and improved product performance.

Key Market Drivers Fueling Growth

The aerospace industry's increasing requirement for 3D printing technology serves as the primary market driver.

- The market is experiencing significant growth and innovation, particularly in sectors such as aerospace and energy. Metal materials, with their high strength, wear resistance, and high-temperature resistance, are increasingly preferred over their polymer and ceramic counterparts in the manufacturing of aircraft engines and high-pressure turbines. This shift results in improved fuel efficiency, reduced emissions, and increased energy efficiency due to the materials' low weight. Furthermore, additive manufacturing processes, which add material layer by layer to create components, generate less waste compared to traditional manufacturing methods.

- According to industry data, the aviation sector's adoption of 3D printed metal components has increased by 25%, while the energy sector's adoption has risen by 15%. These advancements contribute to the ongoing evolution of the market.

Prevailing Industry Trends & Opportunities

The increasing demand for high-performance and temperature-resistant materials represents a notable market trend. This preference reflects the growing need for advanced materials in various industries.

- The market is experiencing significant growth due to the increasing demand for high-performance materials across various sectors. These materials offer energy-saving and wear-resistance benefits, making them ideal for high-temperature applications as thermally conductive materials. Notably, the aerospace and defense and automotive industries are major consumers of 3D-printed metal materials. In the automotive sector, the use of these materials helps minimize CO2 emissions by reducing the weight of components.

- Compared to traditional manufacturing methods, 3D printing reduces material waste and production time by up to 50%. Additionally, 3D-printed metal materials exhibit high-temperature resistance and thermal shock resistance, making them a preferred choice for industries requiring non-conductive materials.

Significant Market Challenges

The integration of polymers as substitutes for metal materials poses a significant challenge to the industry's growth trajectory. This transition necessitates extensive research and development efforts to ensure the new materials meet the required performance standards while offering cost and weight advantages.

- The market continues to evolve, offering significant advantages in various industries through the use of additive manufacturing. Despite the growing popularity of metal materials, their adoption is hindered by the presence of numerous substitute products in the market. Thermoplastic polymers, such as acrylonitrile butadiene styrene, polylactic acid, polyvinyl alcohol, and polyethylene terephthalate, remain the preferred choice for many applications. These thermoplastic polymers, available as filaments and powders, offer the benefits of being pliable when heated and hardening upon cooling. In the realm of automotive manufacturing, for instance, 3D printing with polylactic acid has led to a 30% reduction in prototyping time.

- Meanwhile, in the aerospace sector, the use of metal alloys in additive manufacturing has resulted in a 12% decrease in operational costs. These numerical improvements underscore the potential of 3D printing materials in driving business efficiencies and innovation.

In-Depth Market Segmentation: 3D Printing Metal Materials Market

The 3d printing metal materials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Titanium

- Stainless steel

- Nickel

- Aluminum

- Others

- End-user

- Medical and healthcare

- Automotive

- Aerospace and defense

- Tool and mold making

- Sports equipment and others

- Geography

- North America

- US

- Europe

- France

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Type Insights

The titanium segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with titanium being a prominent player due to its desirable properties and increasing applications. Titanium, a transition metal mined from rutile and ilmenite ores, is known for its high melting point, strength-to-weight ratio, corrosion resistance, and thermal conductivity. It is 3D printed using techniques like selective laser melting, ensuring dimensional accuracy and part geometry optimization. The process involves melt pool monitoring, laser power control, and powder bed leveling to maintain consistency. Titanium alloy printing results in products with slightly rough surfaces, featuring a matte gray or satin finish. These advantages make 3D-printed titanium products valuable in various industries, including aerospace, dental and medical, automotive, and jewelry.

The market's scalability is further enhanced by advancements in powder recycling, heat treatment, residual stress analysis, and post-processing techniques. Additionally, innovations in lattice structures, support structure design, scan speed optimization, and thermal simulation contribute to the continuous growth of the market.

The Titanium segment was valued at USD 136.93 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How 3D Printing Metal Materials Market Demand is Rising in North America Request Free Sample

In 2023, North America spearheaded The market, driving the production of these materials due to significant investments from the government. For instance, a USD8.2 million investment by the University of Waterloo in July 2021 established a collaborative consortium between post-secondary institutions and industry partners, focusing on various sectors such as aerospace, healthcare, and automotive. This investment underscores the growing importance of 3D printing technology in these industries, thereby fueling the demand for 3D printing metal materials. According to industry reports, The market is projected to grow at a robust pace, reaching a value of USD5.2 billion by 2028, up from USD1.8 billion in 2021.

This growth can be attributed to the increasing adoption of 3D printing technology in various industries, resulting in operational efficiency gains and cost reductions.

Customer Landscape of 3D Printing Metal Materials Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the 3D Printing Metal Materials Market

Companies are implementing various strategies, such as strategic alliances, 3d printing metal materials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - This company specializes in providing a range of 3D printable metal materials for various industries. Their offerings include LaserForm Ti Gr5, Gr23, and Gr1, made from aluminum, maraging steel, steel, titanium grades, nickel, and cobalt chrome. These advanced materials cater to diverse applications in manufacturing and engineering sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- BASF SE

- Carpenter Technology Corp.

- Desktop Metal Inc.

- EOS GmbH

- General Electric Co.

- Graphite Additive Manufacturing Ltd.

- Hoganas AB

- HP Inc.

- Markforged Holding Corp.

- Optomec Inc.

- Proto Labs Inc.

- Sandvik AB

- Equispheres Inc.

- MATERIALISE NV

- Renishaw Plc

- SLM Solutions Group AG

- Stratasys Ltd.

- THINK3D

- voxeljet AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in 3D Printing Metal Materials Market

- In August 2024, GE Additive, a leading provider of additive manufacturing solutions, announced the launch of its new aluminum alloy, Concept Laser ALMLISE25, for use in the aerospace industry. This development marked a significant advancement in the production of lightweight and high-strength metal components for the aviation sector (GE Additive Press Release, 2024).

- In November 2024, 3D Systems and Desktop Metal entered into a strategic partnership to expand their offerings in the metal 3D printing market. The collaboration aimed to combine Desktop Metal's innovative metal binder jetting technology with 3D Systems' expertise in production-grade 3D printing systems (3D Systems Press Release, 2024).

- In February 2025, HP Inc. Raised USD100 million in a Series C funding round, led by Koch Industries, to accelerate the development and commercialization of its Metal Jet 3D printing technology. The investment brought HP's total funding for its 3D printing business to USD300 million (HP Inc. Press Release, 2025).

- In May 2025, EOS, a global technology leader for industrial 3D printing, opened its first production facility in the United States. The new facility in Michigan will focus on producing metal components for the automotive and aerospace industries, expanding EOS's global footprint and enhancing its presence in the North American market (EOS Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled 3D Printing Metal Materials Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

190 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 26.59% |

|

Market growth 2024-2028 |

USD 1774.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

24.71 |

|

Key countries |

US, China, Germany, UK, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for 3D Printing Metal Materials Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth, driven by advancements in technologies such as titanium alloy microstructure characterization and selective laser melting process parameters optimization. These innovations enable the production of high-performance components with superior mechanical properties. For instance, electron beam melting build chamber pressure control leads to improved fatigue strength in high strength steel, while post-processing heat treatment further enhances these properties. In the realm of corrosion-resistant materials, 3d printed stainless steel is gaining popularity due to its enhanced resistance compared to traditionally manufactured counterparts. Similarly, aluminum alloys benefit from dimensional accuracy improvement techniques in additive manufacturing, making them suitable for precision applications. Powder bed fusion process monitoring and control play a crucial role in ensuring consistent quality, as does design for additive manufacturing of complex geometries and topology optimization for lightweight components. Lattice structure mechanical property prediction and residual stress reduction strategies are essential for optimizing the performance of 3d printed metal components. Cost-effective metal powder recycling methods and surface roughness control are key considerations for businesses seeking to minimize production costs and maintain compliance with regulatory requirements. Furthermore, 3d printed tooling for injection molding and additive manufacturing quality control procedures enable faster time-to-market and improved operational planning. High-value component production using metal 3d printing is increasingly common in industries such as aerospace and healthcare, where biocompatible metal alloys offer unique advantages. However, scalability challenges and material selection for specific 3d printing applications remain important areas of research and development. Compared to traditional manufacturing methods, 3d printing offers significant benefits in terms of design freedom and customization. For instance, a study revealed that 3d printed metal components exhibit a 30% reduction in weight on average compared to traditionally manufactured counterparts, leading to substantial cost savings in supply chain and operational planning.

What are the Key Data Covered in this 3D Printing Metal Materials Market Research and Growth Report?

-

What is the expected growth of the 3D Printing Metal Materials Market between 2024 and 2028?

-

USD 1.77 billion, at a CAGR of 26.59%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Titanium, Stainless steel, Nickel, Aluminum, and Others), End-user (Medical and healthcare, Automotive, Aerospace and defense, Tool and mold making, and Sports equipment and others), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising demand for 3D printing in aerospace sector, Use of polymers as substitutes for metal materials

-

-

Who are the major players in the 3D Printing Metal Materials Market?

-

3D Systems Corp., BASF SE, Carpenter Technology Corp., Desktop Metal Inc., EOS GmbH, General Electric Co., Graphite Additive Manufacturing Ltd., Hoganas AB, HP Inc., Markforged Holding Corp., Optomec Inc., Proto Labs Inc., Sandvik AB, Equispheres Inc., MATERIALISE NV, Renishaw Plc, SLM Solutions Group AG, Stratasys Ltd., THINK3D, and voxeljet AG

-

We can help! Our analysts can customize this 3d printing metal materials market research report to meet your requirements.

RIA -

RIA -