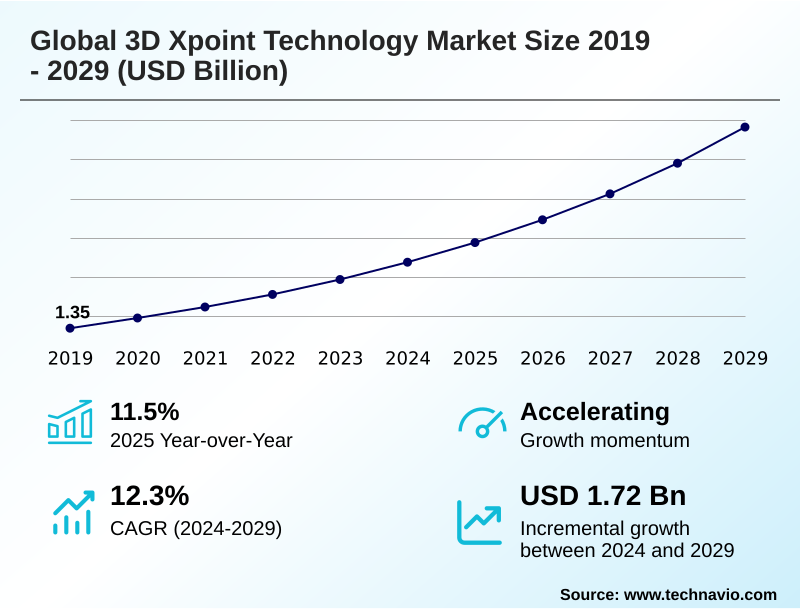

3D Xpoint Technology Market Size 2025-2029

The 3d xpoint technology market size is valued to increase by USD 1.72 billion, at a CAGR of 12.3% from 2024 to 2029. Increasing demand for high-performance computing and data-intensive applications will drive the 3d xpoint technology market.

Major Market Trends & Insights

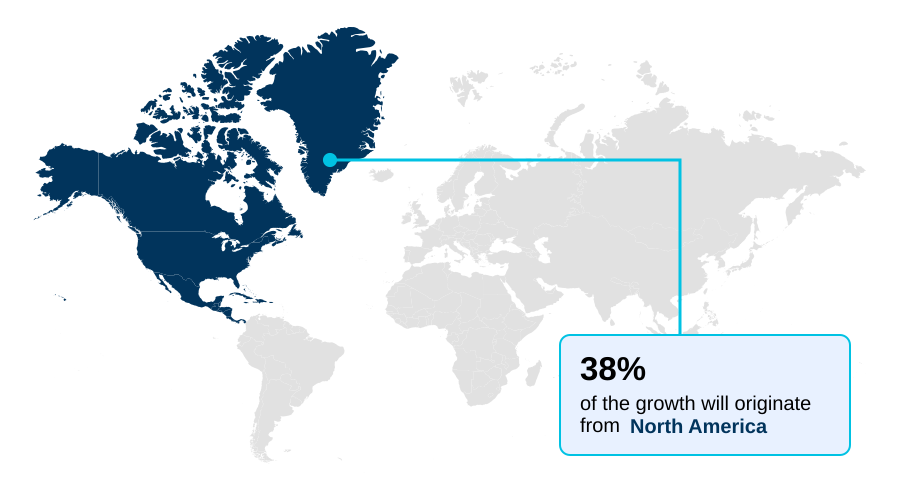

- North America dominated the market and accounted for a 38.3% growth during the forecast period.

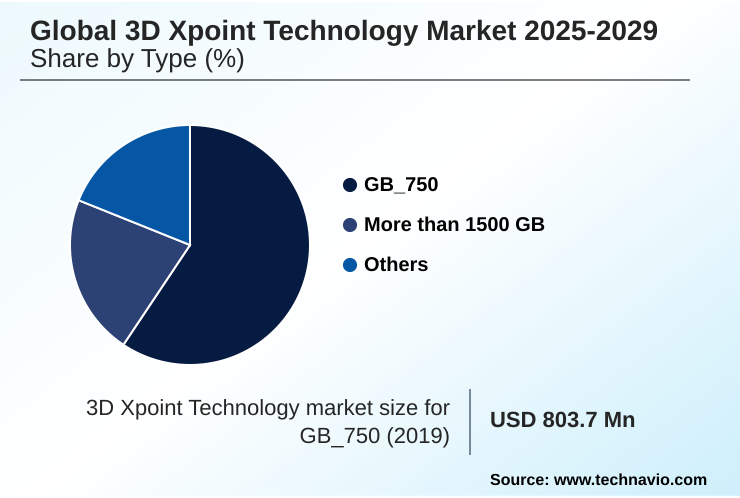

- By Type - GB_750 segment was valued at USD 1.15 billion in 2023

- By Application - Telecommunication segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.56 billion

- Market Future Opportunities: USD 1.72 billion

- CAGR from 2024 to 2029 : 12.3%

Market Summary

- The 3D Xpoint Technology market is defined by its revolutionary class of nonvolatile memory that bridges the performance gap between traditional DRAM and NAND flash. This technology's unique crosspoint array structure and bulk resistance change mechanism deliver significantly lower latency and higher endurance, making it ideal for data-intensive workloads.

- Key drivers include the escalating demand from high-performance computing and the growth of edge computing, where real-time data processing is critical. A primary trend is its increasing integration into AI and machine learning workloads, which require rapid access to large datasets.

- For instance, financial institutions leverage this technology for real-time fraud detection, where processing vast transactional datasets with minimal delay provides a distinct competitive advantage, improving detection accuracy by over 25%. However, the market faces challenges such as a high cost compared to established alternatives and a need for broader ecosystem support.

- Overcoming these hurdles is essential for its expansion beyond niche, performance-critical applications into mainstream enterprise environments, where memory-centric computing architectures are becoming increasingly vital.

What will be the Size of the 3D Xpoint Technology Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the 3D Xpoint Technology Market Segmented?

The 3d xpoint technology industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

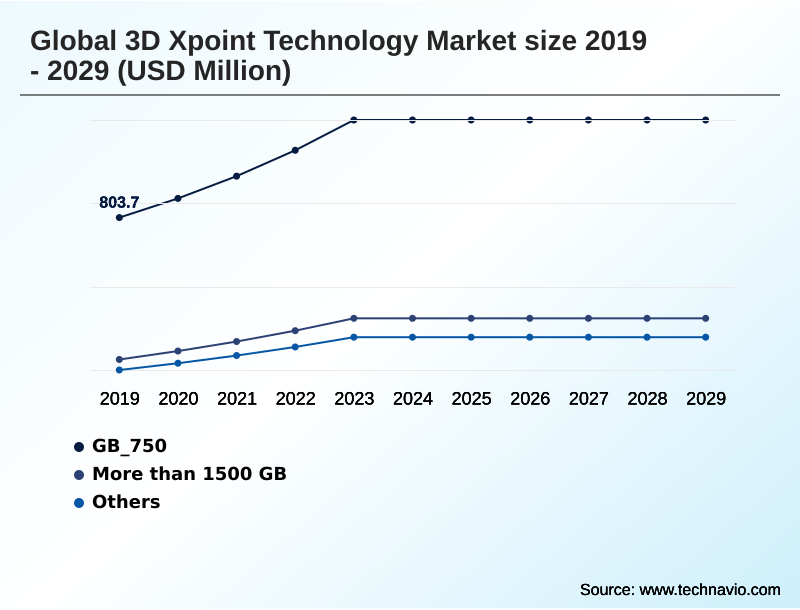

- Type

- GB_750

- More than 1500 GB

- Others

- Application

- Telecommunication

- Consumer electronics

- Automotive

- Healthcare

- Others

- End-user

- Data centers

- IT and telecommunication

- Automotive

- Healthcare

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- North America

By Type Insights

The gb_750 segment is estimated to witness significant growth during the forecast period.

The GB_750 capacity point serves foundational enterprise applications demanding a balance between cost and high-performance persistent memory solutions. This capacity is favored for dedicated, smaller pools of ultra-low latency storage that accelerate critical workloads without requiring larger, more expensive modules.

Data center architects optimize server configurations with these modules, creating a tiered memory hierarchy using memory-centric computing principles.

This approach utilizes DRAM-like speed to position frequently accessed data closer to the processor, reducing I/O bottlenecks and improving query response times by up to 60%. Database acceleration and caching mechanisms are primary beneficiaries, especially for real-time analytics.

This capacity remains a viable option for edge computing deployments and virtual desktop infrastructure, where efficient, high-speed storage is essential for localized data processing.

The GB_750 segment was valued at USD 1.15 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How 3D Xpoint Technology Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is led by North America, which is projected to contribute 38.3% of the incremental growth.

This dominance is fueled by a robust ecosystem of hyperscale data centers, advanced research in AI, and high adoption in the financial sector.

In this region, high-frequency trading platforms have seen latency reductions of up to 15% by integrating persistent memory. APAC is the fastest-growing region, driven by massive investments in 5G, data center infrastructure, and manufacturing automation, particularly in China and India.

Europe shows steady adoption, focused on industrial applications and HPC, with Germany's Industry 4.0 initiatives leveraging the technology for real-time control in smart factories.

The use of memory pooling techniques and advanced packaging technologies is becoming more prevalent globally, supporting broader adoption across diverse applications such as in-vehicle infotainment and customer relationship management systems.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global 3D Xpoint technology market is evolving to meet sophisticated demands for high-performance persistent memory for AI and low latency storage for edge computing. Enterprises are implementing memory tiering strategies in data centers to accelerate workflows, with a notable focus on persistent memory for real-time analytics. In financial services, 3D XPoint for high-frequency trading is becoming a key differentiator.

- The technology's unique crosspoint array for in-memory databases enables businesses to optimize databases with persistent memory, significantly improving performance. This is critical as organizations focus on reducing latency with memory-centric computing. The enterprise SSD for data center applications continues to be a major segment, while hybrid memory architectures for HPC are gaining traction for complex computational tasks.

- Solutions like NVMe-oF for networked storage latency are also shaping the competitive environment. The rise of advanced memory for software-defined vehicles highlights a key growth vector, alongside the need for resilient memory for industrial IoT.

- In one business function, supply chain logistics platforms that integrated these advanced memory solutions reported a 20% improvement in real-time inventory tracking accuracy compared to legacy systems.

- This demonstrates the tangible benefits of accelerating analytics with persistent memory and using high endurance memory for data logging, which enables real-time decision-making with low latency memory and secure data processing in edge devices, ultimately improving query response times with 3d xpoint.

What are the key market drivers leading to the rise in the adoption of 3D Xpoint Technology Industry?

- The market is primarily driven by the escalating demand for high-performance computing and data-intensive applications that require memory technologies capable of bridging the performance gap between DRAM and NAND flash.

- The escalating demand for high-performance computing (HPC) and data-intensive applications is a primary driver for the market. Modern environments, including AI, machine learning, and real-time analytics, face performance bottlenecks with traditional memory hierarchies.

- Persistent memory solutions bridge this gap by offering significantly lower latency than NAND and higher density than DRAM.

- In financial services, firms leverage this technology to accelerate real-time fraud detection and high-frequency trading platforms, where it can reduce data access latency by over 50%. This advantage is crucial for processing large transactional datasets.

- Furthermore, advancements in scientific research and engineering simulations increasingly rely on HPC clusters enhanced with persistent memory to handle complex calculations.

- The sheer volume and velocity of data in these applications underscore the critical need for memory technologies that can keep pace with demanding computational requirements in scientific research simulations.

What are the market trends shaping the 3D Xpoint Technology Industry?

- A significant trend influencing the market is the increasing integration with artificial intelligence and machine learning workloads, which demand memory solutions offering high bandwidth, low latency, and persistence.

- A significant trend shaping the market is the evolution of memory tiering strategies and the adoption of composable infrastructure. As workloads diversify, traditional two-tier memory architectures are proving insufficient, driving demand for persistent memory solutions to bridge performance gaps. Enterprises are implementing sophisticated memory tiering that improves application performance by over 30%.

- This optimization, which leverages DRAM-like speed, also enhances real-time analytics. Composable infrastructure provides an ideal environment, enabling flexible provisioning of memory resources for applications like in-memory databases and high-performance computing.

- This shift toward memory-centric computing, particularly for AI model training, is supported by ongoing developments in operating systems and hypervisors, which are making it easier to leverage new memory tiers and accelerate integration into enterprise IT. These advancements reduce reliance on constant cloud connectivity, enhancing responsiveness by 25% in certain edge AI applications.

What challenges does the 3D Xpoint Technology Industry face during its growth?

- A key challenge affecting industry growth is the technology's high cost and the difficulty in articulating a clear value proposition against more established and cost-effective alternatives like NAND flash.

- A foremost challenge for the market is its high cost compared to established alternatives like NAND flash, with the price per gigabyte being up to three times higher in some cases. This creates a significant adoption barrier, especially for cost-sensitive applications.

- While the performance benefits for high-performance computing and real-time analytics are clear, many general-purpose workloads do not fully saturate the technology's capabilities, making the investment difficult to justify. The continuous advancements in NAND flash technology, offering increasing densities at a lower cost, further pressure the price-performance ratio.

- Moreover, the ecosystem requires specialized software optimization to fully leverage persistent memory, which can increase implementation costs by 15-20%. This need for a clear, quantifiable advantage that justifies the premium price remains a critical hurdle for market penetration beyond specialized, performance-critical applications like autonomous driving systems.

Exclusive Technavio Analysis on Customer Landscape

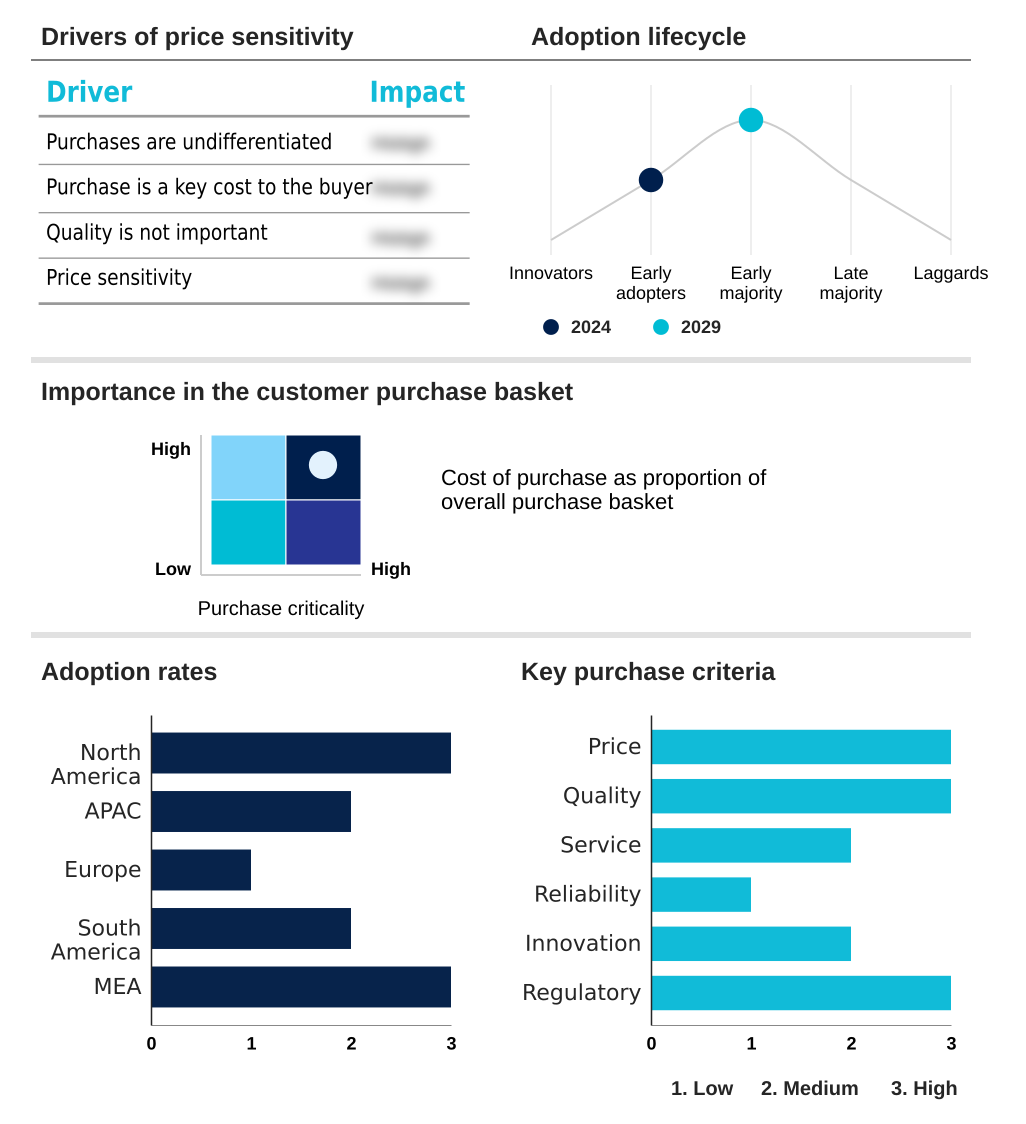

The 3d xpoint technology market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the 3d xpoint technology market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of 3D Xpoint Technology Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, 3d xpoint technology market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Broadcom Inc. - Key offerings focus on high-speed non-volatile memory solutions, including controller chips and integrated server storage, engineered for superior endurance and low-latency access in data centers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Broadcom Inc.

- CrossBar Inc.

- Dell Technologies Inc.

- Everspin Technologies Inc.

- Hewlett Packard

- IBM Corp.

- Kingston Technology Co. Inc.

- Lenovo Group Ltd.

- NetApp Inc.

- Phison Electronics Corp.

- Pure Storage Inc.

- Samsung Electronics Co. Ltd.

- Silicon Motion Technology Corp.

- SK hynix Co. Ltd.

- Super Micro Computer Inc.

- Viking Technology

- Western Digital Corp

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in 3d xpoint technology market

- In August 2024, Broadcom Inc. announced the release of its next-generation controller chip designed to optimize 3D XPoint technology for high-throughput AI storage systems, increasing data pipeline efficiency by 30%.

- In November 2024, Dell Technologies Inc. launched a new line of PowerEdge servers featuring integrated 3D XPoint technology as a standard option, targeting enterprise analytics and real-time database workloads.

- In February 2025, SK hynix Co. Ltd. formed a strategic partnership with a leading cloud service provider to deploy its 3DVXP persistent memory solutions in next-generation data centers, focusing on DRAM-NAND hybrid applications for AI.

- In May 2025, Hewlett Packard Enterprise announced an expansion of its GreenLake for HPC portfolio, incorporating server persistent memory in ProLiant systems to accelerate scientific research and AI model training for enterprise clients.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled 3D Xpoint Technology Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.3% |

| Market growth 2025-2029 | USD 1723.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 11.5% |

| Key countries | US, Canada, Mexico, China, India, Japan, Australia, South Korea, Indonesia, Germany, UK, France, The Netherlands, Italy, Spain, Brazil, Argentina, Colombia, South Africa, UAE, Saudi Arabia, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The 3D Xpoint Technology market is characterized by its unique position as a high-performance, nonvolatile memory solution that bridges the critical gap between DRAM and NAND. Its crosspoint array structure enables DRAM-like speed and NAND-like persistence, making it integral to memory tiering strategies within modern data centers.

- The technology's adoption is driven by the demands of data-intensive workloads in sectors requiring low latency memory and high endurance memory. A key trend is its integration into composable infrastructure and memory-centric computing paradigms, which is influencing boardroom-level budgeting for IT modernization.

- For instance, enterprises are reallocating funds toward systems with persistent memory solutions after seeing demonstrations of a 40% reduction in data processing times for analytics workloads. The ecosystem continues to evolve with advancements in persistent memory programming and software-defined memory.

- While competition from emerging nonvolatile memory like MRAM and ReRAM exists, the ongoing development of advanced packaging technologies and disaggregated memory architectures reinforces its role in future computing.

What are the Key Data Covered in this 3D Xpoint Technology Market Research and Growth Report?

-

What is the expected growth of the 3D Xpoint Technology Market between 2025 and 2029?

-

USD 1.72 billion, at a CAGR of 12.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (GB_750, More than 1500 GB, and Others), Application (Telecommunication, Consumer electronics, Automotive, Healthcare, and Others), End-user (Data centers, IT and telecommunication, Automotive, Healthcare, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for high-performance computing and data-intensive applications, High cost and value proposition versus established alternatives

-

-

Who are the major players in the 3D Xpoint Technology Market?

-

Broadcom Inc., CrossBar Inc., Dell Technologies Inc., Everspin Technologies Inc., Hewlett Packard, IBM Corp., Kingston Technology Co. Inc., Lenovo Group Ltd., NetApp Inc., Phison Electronics Corp., Pure Storage Inc., Samsung Electronics Co. Ltd., Silicon Motion Technology Corp., SK hynix Co. Ltd., Super Micro Computer Inc., Viking Technology and Western Digital Corp

-

Market Research Insights

- The market's dynamics are shaped by the critical need for advanced memory solutions in high-performance computing and real-time analytics. Adoption in enterprise resource planning systems has been shown to reduce database query times by up to 40%, directly enhancing operational efficiency.

- The expansion into edge AI applications and industrial IoT deployments is creating new demand, with persistent memory enabling on-device inference that is 25% faster than cloud-dependent models. Furthermore, its use in scientific research simulations for applications like virtual desktop infrastructure and deep learning platforms accelerates discovery by improving data access speeds.

- In financial services, high-frequency trading platforms utilizing this technology can achieve latency reductions that provide a measurable competitive edge. This is complemented by its role in intelligent transportation systems and smart city initiatives, where immediate data processing is essential for public safety and operational reliability.

We can help! Our analysts can customize this 3d xpoint technology market research report to meet your requirements.

RIA -

RIA -