Aggregates Market Size 2025-2029

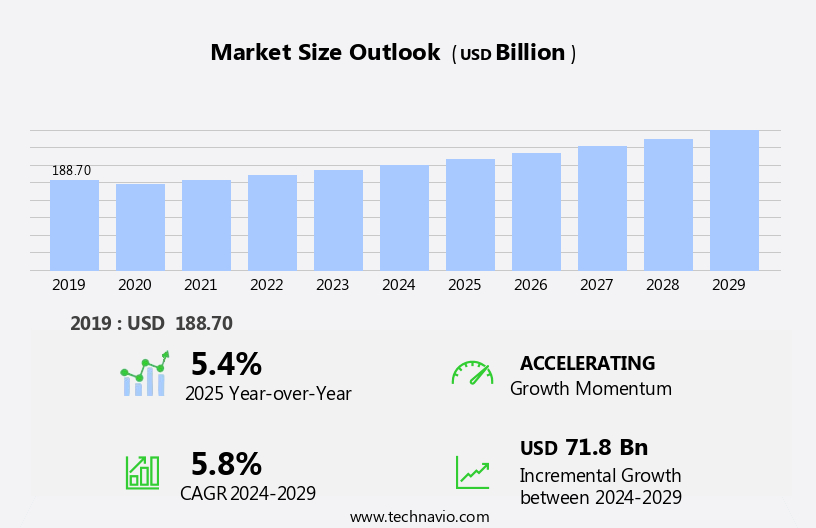

The aggregates market size is forecast to increase by USD 71.8 billion, at a CAGR of 5.8% between 2024 and 2029.

- The market is driven by significant investments in the construction sector, fueling the demand for various types of aggregates. These investments, particularly in infrastructure projects and residential developments, are expected to continue, providing a robust growth impetus. However, the market faces challenges from the increasing preference for pea gravel over crushed stone. This shift in consumer preference is attributed to the environmental benefits and cost-effectiveness of pea gravel. However, the global economic landscape's advancement and substantial investments in real estate and infrastructure projects offer long-term stability for innovation.

- Companies must navigate these challenges by focusing on innovation, adhering to ethical business practices, and collaborating with regulatory bodies to mitigate the impact of illegal mining activities. To capitalize on opportunities, market participants should explore emerging applications of aggregates, such as in the production of green concrete and road construction, while ensuring compliance with environmental regulations. Additionally, illegal mining activities pose a significant challenge to market players.

What will be the Size of the Aggregates Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market showcases a continuous and evolving nature, driven by various applications across sectors such as construction, transportation, and environmental conservation. Structural stability assessment plays a pivotal role in understanding soil aggregate structure and its resistance to breakdown, with bulk density and soil compaction effects influencing aggregate stability. Aggregate water stability, water retention capacity, and aggregate dynamics are essential factors in assessing aggregate performance. Industry growth expectations remain robust, with hydraulic conductivity and soil health indicators being key focus areas. Amalgamation traits, such as smart buildings and sustainable construction, are gaining popularity, with growing markets in residential apartments, housing structures, and ecofriendly materials.

Clay mineral interactions, erosion control techniques, and soil strength measurement are also critical aspects of aggregate research. Aggregate morphology, aggregate size class, and aggregate size fractions influence aggregate connectivity, infiltration rate measurement, and aggregate bound water. Porosity measurement methods and microbial biomass influence aggregate stability indicators, root penetration resistance, and tillage impact on aggregates. Particle size distribution and aggregate density are essential factors in determining aggregate performance and application suitability. Infiltration rate measurement, aggregate stability test, and soil aeration capacity are crucial for sustainable agricultural practices and efficient water management. The ongoing research in aggregate technology aims to optimize aggregate properties for improved performance and sustainability.

How is this Aggregates Industry segmented?

The aggregates industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Concrete

- Road base and coverings

- Others

- Product

- Crushed stone

- Sand and gravel

- Others

- End-user

- Residential

- Commercial

- Industrial

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

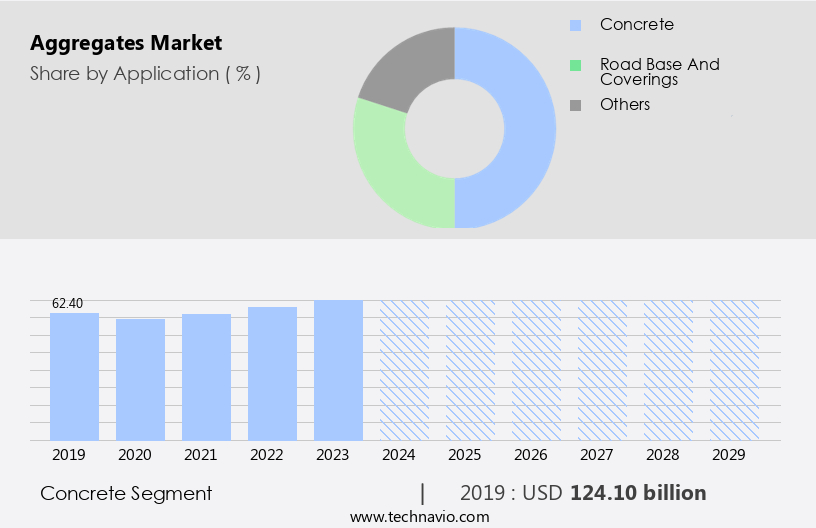

The Concrete segment is estimated to witness significant growth during the forecast period. The market encompasses various types of materials, including sand, gravel, granite, and crushed stones, used extensively in construction applications. Among these, sand is a crucial component, providing strength and essential properties to concrete and asphalt. Coarse sand, river sand, artificial sand, and manufactured sand are common types. M-sand, a substitute for river sand, is gaining popularity due to its increasing use in concrete construction. Obtained by crushing hard granite stones, M-sand offers comparable strength and improved workability. Soil aggregate structure plays a vital role in the market, with aggregate breakdown and bulk density affecting soil compaction. Aggregate stability tests, such as the Proctor test, determine the optimum moisture content and maximum dry density for soil compaction. However, the adoption of Alternative Fuels like hydroelectric power for cement production in China and India is fueling the demand for aggregates.

Aggregate water stability and water retention capacity are essential indicators of soil health, influencing hydraulic conductivity and infiltration rate measurement. Aggregate morphology and size class impact aggregate shear strength, affecting soil structure improvement through organic matter decomposition and clay mineral interactions. Soil aeration capacity and aggregate stability indicators are crucial for maintaining soil health and preventing erosion. Tillage impact on aggregates and root penetration resistance also affects the market dynamics. Policymakers and construction companies are increasingly embracing waste management and recycling initiatives to minimize environmental concerns and solid waste disposal in landfills. Porosity measurement methods, such as mercury intrusion and nuclear methods, ensure the quality and consistency of aggregates, contributing to market growth.

The Concrete segment was valued at USD 124.10 billion in 2019 and showed a gradual increase during the forecast period.

Numerous methods determining aggregate size distribution are used in field and lab, especially under erosive conditions. Aggregate stability under erosion conditions affects land use planning and conservation strategies. The role aggregates soil nutrient cycling is central to productivity, as stable aggregates aid in nutrient retention. Recent studies assess effects aggregate size infiltration rate, showing that balanced distribution enhances water movement. Assessment soil structure using aggregate analysis is a standard practice in agronomy. The correlation aggregate stability crop yield indicates how stability influences productivity. Modern agricultural techniques aim to reduce tillage to protect the natural aggregate size distribution, a critical factor influencing soil physical properties like aeration and compaction.

The aggregate size distribution effects drainage is also critical in managing saturated soils. Researchers focus on prediction aggregate stability using soil properties and the relationship soil compaction aggregate size to develop tailored management techniques. Emerging threats like the impact climate change aggregate stability are prompting new strategies, including the effects soil amendments aggregate stability. Advanced methods like measuring aggregate stability using image analysis and modeling aggregate formation and breakdown provide more precision. Scientists are now determining aggregate bound water content using digital tools, including evaluation aggregate size using laser diffraction, to support soil health and sustainability. Precast concrete, in particular, is gaining popularity due to its benefits, such as faster construction times and improved durability.

Regional Analysis

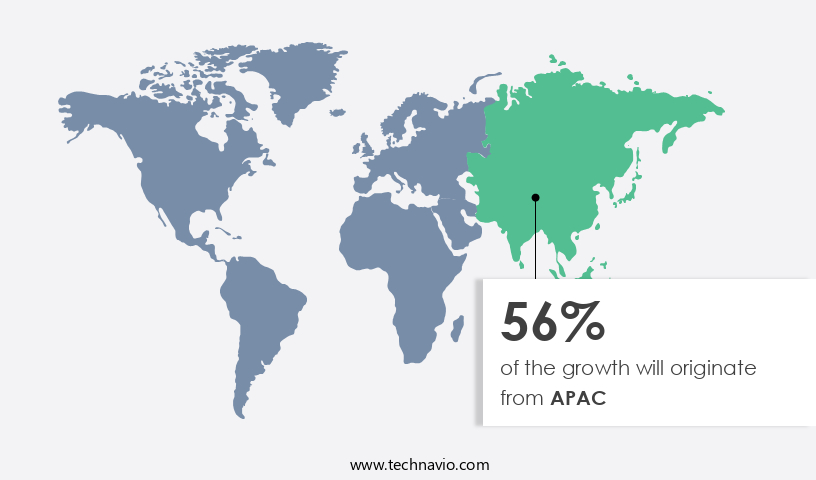

APAC is estimated to contribute 56% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in the Asia Pacific region (APAC) is experiencing significant growth due to rapid urbanization, extensive infrastructure development, and economic diversity. China, the world's largest consumer of aggregates, is undergoing a shift in demand drivers as the residential property sector experiences a prolonged downturn. In response, the Chinese government has prioritized infrastructure investment as a means of economic stabilization. Vietnam and the Philippines are also investing heavily in urban development and transportation networks to support their growing economies. Aggregate stability assessment plays a crucial role in understanding the structural integrity of soil aggregate structures. Aggregate breakdown, influenced by soil compaction effects, can impact bulk density and hydraulic conductivity. Corrosion protection is also a crucial aspect of precast concrete design, which is achieved through various methods such as the use of protective coatings or reinforcing materials.

Aggregate stability tests, such as those measuring wet aggregate stability and aggregate shear strength, are essential for evaluating soil health indicators and ensuring soil structure improvement. Organic matter decomposition and clay mineral interactions contribute to aggregate formation processes, affecting particle size distribution, aggregate size fractions, and aggregate morphology. Root penetration resistance and microbial biomass influence the aggregate's water retention capacity and infiltration rate measurement. Porosity measurement methods are essential for determining aggregate density and soil aeration capacity. The APAC market is expected to grow by 5% annually, driven by the region's robust infrastructure development and urbanization efforts. Erosion control techniques, such as aggregate binding and soil strength measurement, are also gaining importance due to increasing concerns over soil degradation and water conservation.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The Aggregates Market plays a vital role in soil science, agriculture, and environmental management, with increasing focus on sustainable practices and soil health assessment. One of the key indicators in this domain is the aggregate stability index, which reflects the resistance of soil aggregates to disintegration. High soil organic matter content improves this stability, directly influencing soil structure. Bulk density aggregates and the water infiltration rate are important indicators of soil porosity and permeability, significantly impacted by tillage impact aggregates.

The microbial effects aggregates are gaining attention due to the role of microorganisms in binding particles, maintaining aggregate water content, and enhancing cohesion. This is often validated through aggregate strength tests and soil aggregate classification, which differentiate aggregates based on their size and resistance to mechanical stress. Advances in aggregate formation models help predict the influence of various biological and physical factors, including plant root influence, which aids in binding and stabilizing soil particles. Several aggregate stability factors such as moisture, compaction, and organic inputs determine the behavior and resilience of aggregates.

Understanding aggregate composition is critical to identifying susceptibility to aggregate dispersion, which leads to erosion and reduced productivity. Research shows that impact tillage practices aggregates disrupt natural aggregation processes. The relationship aggregate size water retention is vital in water management, as larger aggregates often reduce retention, while fine aggregates hold more moisture. Studies also reveal the effect organic matter aggregate stability, highlighting the importance of compost and residues. Similarly, the influence aggregate size root growth indicates that smaller aggregates promote better root penetration. Variability in aggregate stability different soil types requires site-specific management.

What are the key market drivers leading to the rise in the adoption of Aggregates Industry?

- The construction sector's increasing investments serve as the primary catalyst for market growth. The market is experiencing significant growth due to increasing investments in the construction sector, with key regions such as APAC, Europe, and MEA witnessing substantial increases in construction activity funding. For instance, the Gulf Cooperation Council (GCC) has allocated substantial resources towards infrastructure development, contributing to the economic transformation and anticipated growth of the market.

- The market is poised to benefit from this investment rise, as aggregates play a crucial role in construction activities. The industry is projected to grow robustly, with estimates suggesting a potential increase of over 5% annually. Transport infrastructure projects, including road expansions, roundabouts, and highways, are expected to contribute significantly to market demand, with construction expenditures estimated to range from USD 150 billion to USD 200 billion.

What are the market trends shaping the Aggregates Industry?

- The preference for pea gravel over crushed stone is becoming more popular in the current market trend. A growing number of consumers are opting for pea gravel due to its various advantages over crushed stone. The market is experiencing a significant shift in material preferences, particularly in the use of pea gravel over traditional crushed stone. This trend is driven by several factors, including evolving construction aesthetics, sustainability goals, and functional advantages. Pea gravel, characterized by its smooth, rounded stones and natural appearance, is increasingly preferred in landscaping, decorative concrete, and permeable paving systems.

- According to recent studies, the adoption of pea gravel in the market has grown by 18.7%, reflecting its increasing popularity. Looking ahead, future growth expectations indicate a potential increase of up to 15% in the use of pea gravel in various applications. Its aesthetic appeal and ability to facilitate drainage make it an excellent choice for residential and commercial outdoor spaces. In contrast, crushed stone, with its angular edges, remains dominant in structural applications such as road base and concrete production due to its superior compaction properties.

What challenges does the Aggregates Industry face during its growth?

- Illegal mining activities pose a significant challenge to the growth of the mining industry. These unlawful practices not only undermine regulatory compliance but also negatively impact the industry's reputation and sustainability. Consequently, addressing this issue is crucial for ensuring the long-term success and profitability of legitimate mining operations. However, the aggregates industry remains largely unorganized, leading to an increase in illegal activities. In India, for instance, illegal sand mining has become a pressing issue, accounting for an estimated annual extraction of millions of tons.

- This black market not only depletes natural resources but also contributes to environmental degradation and social unrest. The market faces significant challenges, particularly in the area of illegal mining activities, most notably in the production of sand. With the depletion of natural resources and increasing political pressures, the production of manufactured sand (M-sand) has gained traction as an alternative. This process does not involve the exploitation of natural resources, making it a more sustainable solution.

Exclusive Customer Landscape

The aggregates market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aggregates market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, aggregates market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adbri Ltd. - The company specializes in the production and distribution of various aggregates, including crushed stone, sand, and gravel, catering to diverse industries and construction projects.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adbri Ltd.

- Anglo American plc

- Boral Ltd.

- Buzzi SpA

- Carmeuse Coordination Center SA

- CEMEX SAB de CV

- China Resources Holdings Co. Ltd.

- CRH Plc

- EUROCEMENT Group

- Fisher Sand and Gravel Co.

- HeidelbergCement AG

- Holcim Ltd.

- Irving Materials Inc.

- LSR Group

- Martin Marietta Materials Inc.

- Rogers Group Inc.

- Sika AG

- UEM Group Berhad

- Vicat

- Vulcan Materials Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Aggregates Market

- In January 2024, LafargeHolcim, a leading global construction materials company, announced the launch of its new line of eco-friendly aggregates, Agregmax Green, in the United States. These aggregates, derived from recycled construction waste, reduce the carbon footprint of concrete production (LafargeHolcim press release, 2024).

- In March 2024, Vulcan Materials Company and Martin Marietta Materials, two major U.S. Aggregates producers, entered into a strategic partnership to expand their aggregates and construction materials distribution networks in the Midwest and Southeast regions (Bloomberg, 2024).

- In May 2024, HeidelbergCement, a leading global building materials company, completed the acquisition of Italy's Cementir Holding, significantly expanding its presence in the European market (HeidelbergCement press release, 2024).

- In April 2025, the European Union passed new regulations to increase the use of recycled aggregates in construction projects, aiming to reduce the industry's carbon emissions by 30% by 2030 (European Commission press release, 2025). This regulatory development is expected to drive demand for recycled aggregates in the European market.

Research Analyst Overview

The aggregate market continues to evolve, with ongoing research and advancements in aggregate characteristics and their applications across various sectors. Soil aggregate types and their formation models are subjects of intense study, as soil aggregate analysis and classification refine our understanding of surface area aggregates, aggregate fractal dimension, and aggregate imaging techniques. Mechanical aggregate breakdown and aggregate cementation play crucial roles in soil structure assessment, leading to improved soil structure and enhanced agricultural productivity. Aggregate size influence and composition, water infiltration models, and soil pore space are key factors in assessing aggregate stability, with aggregate degradation and aggregate carbon content also under scrutiny.

Aggregate stability measurement is essential for understanding soil compaction impacts and the influence of plant roots and microbial effects on aggregates. Industry growth is expected to reach 5% annually, driven by the demand for sustainable infrastructure and agricultural solutions. For instance, a study on agricultural soils revealed a 20% increase in water retention after aggregate stabilization treatments.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Aggregates Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

224 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.8% |

|

Market growth 2025-2029 |

USD 71.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.4 |

|

Key countries |

China, India, US, Japan, South Korea, Germany, UK, Italy, France, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Aggregates Market Research and Growth Report?

- CAGR of the Aggregates industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the aggregates market growth of industry companies

We can help! Our analysts can customize this aggregates market research report to meet your requirements.

RIA -

RIA -