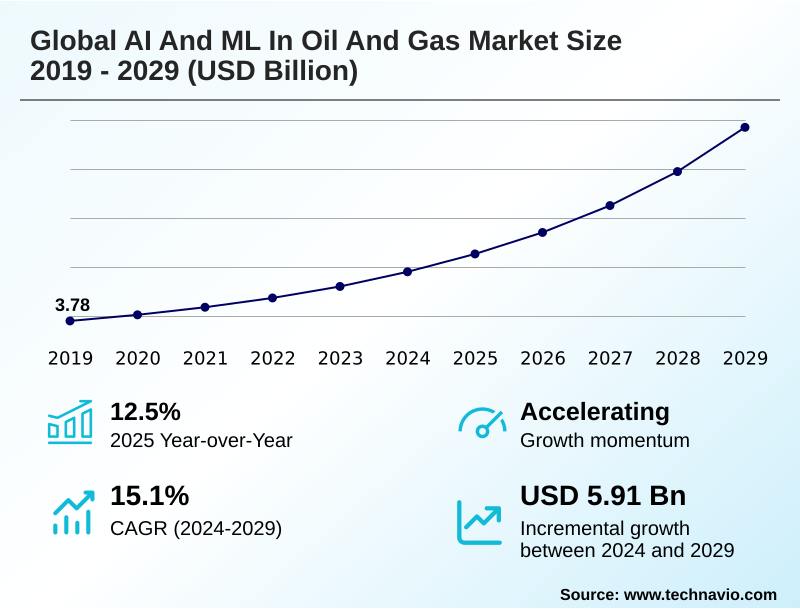

AI And ML In Oil And Gas Market Size 2025-2029

The ai and ml in oil and gas market size is valued to increase by USD 5.91 billion, at a CAGR of 15.1% from 2024 to 2029. Imperative for enhanced operational efficiency and cost reduction will drive the ai and ml in oil and gas market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 29.6% growth during the forecast period.

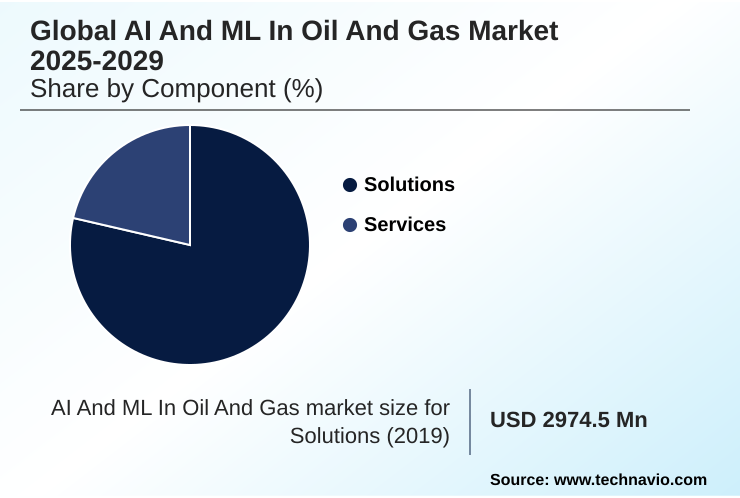

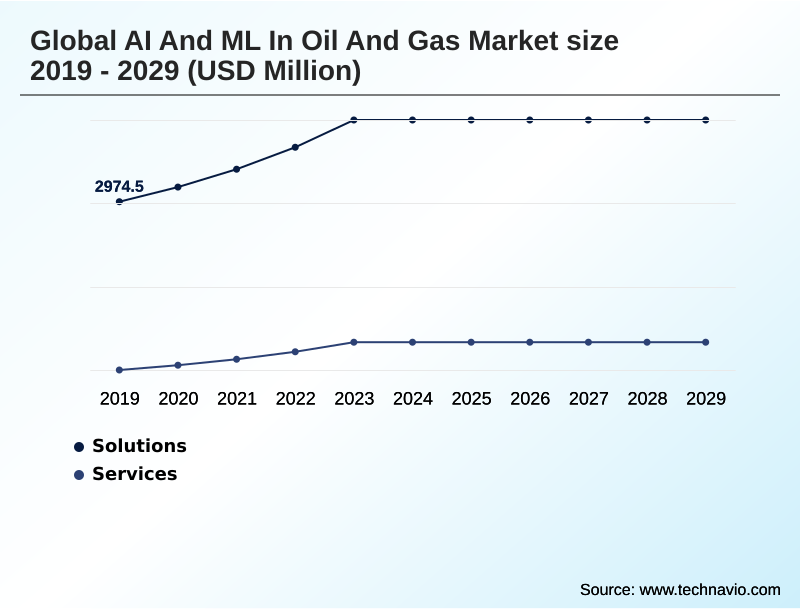

- By Component - Solutions segment was valued at USD 4.03 billion in 2023

- By Application - Predictive maintenance segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 7.92 billion

- Market Future Opportunities: USD 5.91 billion

- CAGR from 2024 to 2029 : 15.1%

Market Summary

- The AI and ML in oil and gas market is undergoing a fundamental transformation, driven by the strategic imperative to enhance operational efficiency and meet stringent environmental standards. The proliferation of big data from the industrial internet of things (iiot) and the accessibility of cloud computing have created a fertile ground for ai-based reservoir simulation and deep learning models.

- These technologies are moving beyond pilot projects to become core components of digital transformation, with applications in prescriptive maintenance ai and automated drilling optimization. For example, a midstream operator can deploy ai-powered inspection robots that use computer vision for safety to autonomously patrol thousands of miles of pipeline.

- These systems provide real-time pipeline integrity monitoring, detecting minute leaks and enabling a response that is more than 50% faster than traditional methods. This shift from reactive to predictive operations also faces challenges, including data integration complexities and a shortage of talent with hybrid domain and data science skills.

- However, the demonstrated value in reducing costs, enhancing safety through ai for process safety management, and improving esg compliance with ai continues to accelerate adoption across the industry.

What will be the Size of the AI And ML In Oil And Gas Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI And ML In Oil And Gas Market Segmented?

The ai and ml in oil and gas industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Solutions

- Services

- Application

- Predictive maintenance

- Production optimization

- Supply chain and logistics

- Exploration and drilling

- Others

- End-user

- Downstream

- Upstream

- Midstream

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- Middle East and Africa

- Saudi Arabia

- UAE

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The solutions segment is defined by advanced software and platforms enabling data-driven decisions and intelligent automation. This includes comprehensive production optimization platforms that utilize iot sensor data analysis and integrated ecosystems providing ai-powered process control for ml for downstream processes.

Specialized point applications are also critical, offering deep learning models for specific challenges like seismic data interpretation and ai for exploration and production.

These tools leverage high-performance computing for ai to execute complex tasks, improving fault detection in subsurface imaging algorithms by up to 15%. The deployment of ai for hydraulic fracturing and drilling optimization with ai is transforming upstream efficiency.

Solutions focused on generative ai knowledge management and ai in upstream operations are also gaining traction, democratizing access to complex operational insights and enabling cognitive computing for geoscience.

The Solutions segment was valued at USD 4.03 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 29.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI And ML In Oil And Gas Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the global AI and ML in oil and gas market 2025-2029 is diverse, with adoption patterns reflecting regional priorities.

North America leads in applying ai for unconventional resources, focusing on drilling optimization with ai and real-time geosteering ai to drive efficiency in shale plays.

Europe’s mature offshore basins prioritize asset integrity management and machine learning for asset integrity, with digital twin simulation being key to extending asset life.

The APAC region is projected to exhibit the fastest growth, with a dynamic expansion rate nearly 4% higher than in Europe, driven by national oil companies investing heavily in modernizing infrastructure and ai for production optimization.

The Middle East is aggressively deploying large-scale ai for enhanced oil recovery and real-time production monitoring. Deployment of ai for subsea systems is critical in deepwater regions like South America, while ai-driven energy trading models are becoming standard globally.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic implementation of artificial intelligence is redefining operational benchmarks across the energy value chain. Companies are increasingly focused on using ai to reduce drilling time through better subsurface analysis and real-time adjustments. A key application is the predictive maintenance for electric submersible pumps, which forecasts failures and minimizes costly downtime.

- In downstream, ai applications for refinery process control and models for optimizing refinery yield with machine learning are becoming standard for maximizing profitability. Upstream, machine learning for seismic fault interpretation and the use of ai models for subsurface reservoir characterization are accelerating exploration cycles. The rise of generative ai for oil and gas reports is unlocking decades of unstructured data.

- For remote operations, edge ai for remote offshore platforms enables immediate decision-making. In unconventional plays, optimizing hydraulic fracturing with ai and using models to predict parent-child well interference are crucial for maximizing recovery. ESG drivers are pushing the adoption of ai-powered methane leak detection systems.

- The progress in autonomous drilling platform safety protocols and real-time geosteering for horizontal wells showcases the maturity of these technologies. In logistics, supply chain logistics optimization with ml improves efficiency. Other impactful use cases include enhancing oil recovery with ai models, deploying digital twin for offshore asset management, and leveraging ai for optimizing lng plant throughput.

- Furthermore, computer vision for ppe compliance monitoring and anomaly detection in scada systems using ai enhance safety and security. This holistic adoption, including using ai for carbon capture modeling and ai-driven demand forecasting for petroleum products, has led to a twofold improvement in project completion timelines compared to legacy methods.

What are the key market drivers leading to the rise in the adoption of AI And ML In Oil And Gas Industry?

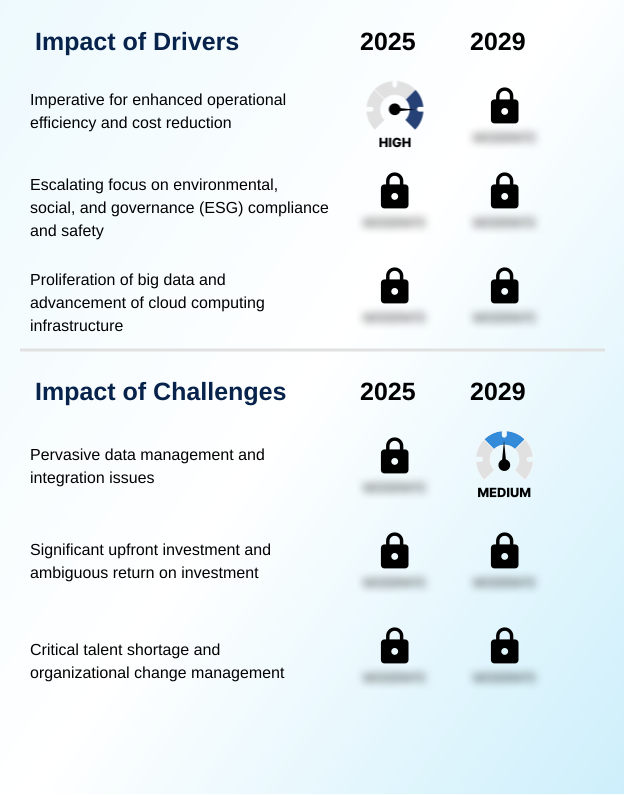

- The imperative to enhance operational efficiency and reduce costs across the value chain remains a primary driver for market adoption.

- Market growth is propelled by the imperative for enhanced efficiency and cost reduction. The application of AI in upstream operations and machine learning in midstream logistics delivers tangible returns, with some companies reporting operational efficiency gains of up to 15%.

- A second major driver is the escalating focus on ESG compliance. AI for emissions tracking and tools for methane emissions detection are no longer optional, enabling operators to achieve a 20% reduction in reported fugitive emissions.

- Finally, the proliferation of big data, coupled with advanced cloud computing and a robust industrial internet of things (iiot), provides the necessary foundation.

- This synergy allows for the effective use of ai for petrochemical plants and real-time geosteering systems, turning vast datasets into actionable intelligence.

What are the market trends shaping the AI And ML In Oil And Gas Industry?

- The emergence of generative AI and large language models is a key market trend, driving new capabilities in knowledge management and data synthesis.

- The market is shaped by three transformative trends. The emergence of the generative AI in energy sector and large language models is unlocking unstructured data, improving knowledge retrieval speeds by over 50% for applications like ai-based reservoir simulation.

- Second, a move toward hyper-automation and intelligent automation in oilfield is creating self-optimizing assets, with autonomous drilling systems and ai for process safety management reducing manual interventions. Finally, the proliferation of edge AI for remote assets and edge computing in energy is critical for real-time decision-making where connectivity is limited.

- This enables immediate responses in machine learning for asset integrity, with anomaly detection algorithms reducing threat identification times by up to 90%, thereby enhancing both safety and operational uptime with ai for production optimization.

What challenges does the AI And ML In Oil And Gas Industry face during its growth?

- Pervasive data management and integration issues present a significant challenge to the effective deployment and scaling of AI initiatives.

- Despite significant opportunities, the market faces key challenges. Pervasive data management issues, including data silos and poor quality, remain a primary obstacle, with data integration often consuming over 60% of an AI project's timeline. Second, the significant upfront investment for computer vision in oil and gas and other advanced tools is coupled with ambiguous ROI, causing many initiatives to stall.

- It's estimated that up to 40% of pilot projects fail to scale due to an unclear business case. Finally, a critical talent shortage of professionals skilled in both domain expertise and data science, alongside organizational resistance to change, hampers the effective adoption of even the most sophisticated wellbore stability analysis and drilling hazard prediction models.

Exclusive Technavio Analysis on Customer Landscape

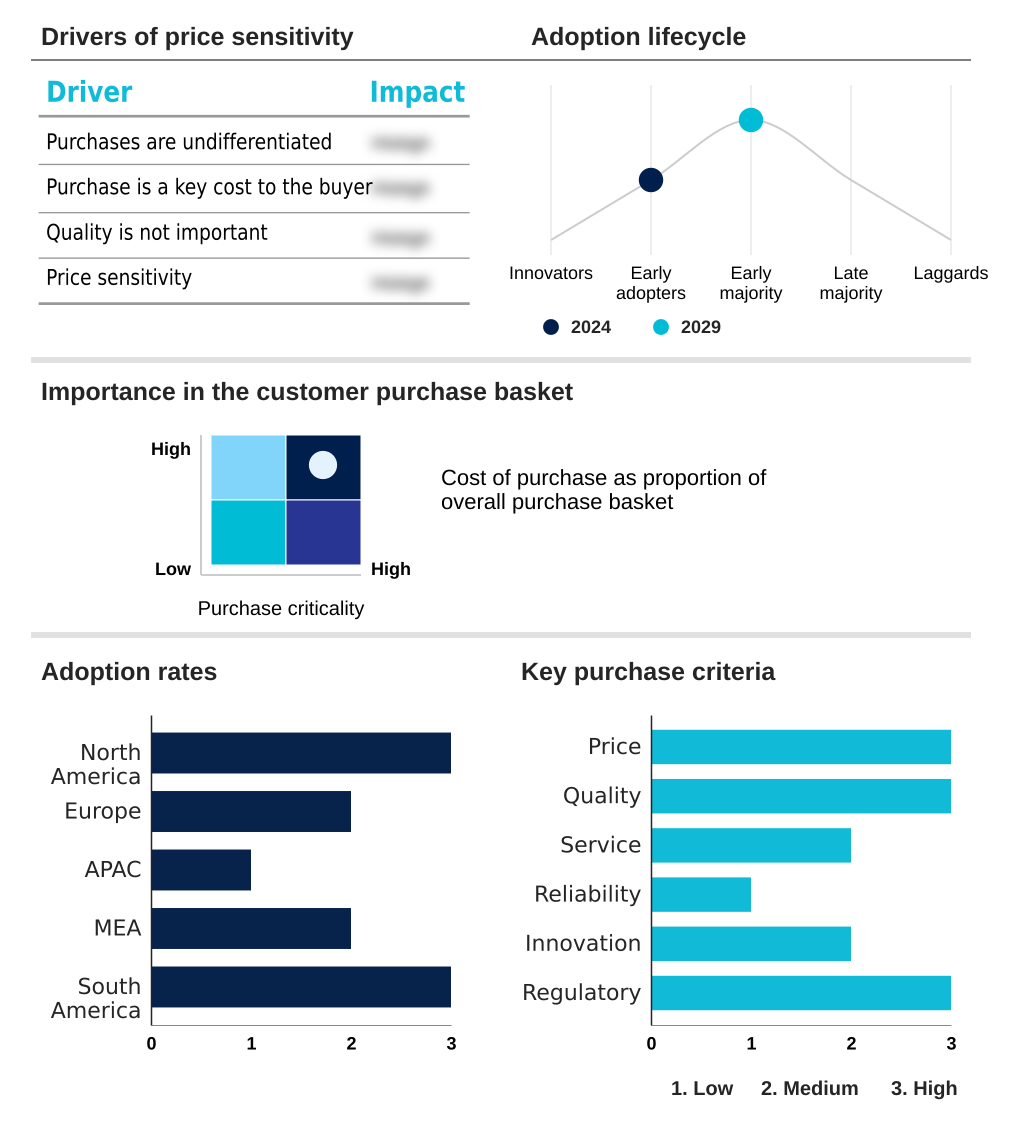

The ai and ml in oil and gas market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai and ml in oil and gas market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI And ML In Oil And Gas Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai and ml in oil and gas market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Enables real-time process optimization and emissions reduction through AI and ML platforms, driving efficiency in industrial automation and energy management.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Accenture PLC

- Baker Hughes Co.

- Beyond Limits

- BP Plc

- C3.ai Inc.

- Exxon Mobil Corp.

- Google LLC

- Halliburton Co.

- IBM Corp.

- Microsoft Corp.

- Oracle Corp.

- Saudi Arabian Oil Co.

- Schlumberger Ltd.

- SensorUp Inc.

- Shell plc

- Siemens AG

- SparkCognition Inc.

- TechnipFMC plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai and ml in oil and gas market

- In September, 2024, Halliburton Co. announced a strategic partnership with a leading cloud provider to integrate advanced generative AI into its DS365.ai platform, aiming to accelerate subsurface decision analysis and well planning for clients.

- In November, 2024, Baker Hughes Co. launched a new suite of edge AI solutions designed for real-time monitoring and autonomous control of subsea production systems, enhancing safety and efficiency in deepwater operations.

- In February, 2025, a consortium of venture capital firms invested a significant sum into SparkCognition Inc. to scale its AI-powered predictive maintenance and asset performance management solutions, specifically targeting the downstream refining sector.

- In April, 2025, a new industry-wide initiative led by major operators like Shell plc and BP Plc was launched to standardize data formats for AI-driven emissions monitoring, aiming to improve ESG reporting accuracy and interoperability across the sector.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI And ML In Oil And Gas Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 279 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.1% |

| Market growth 2025-2029 | USD 5912.6 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 12.5% |

| Key countries | US, Canada, Russia, Germany, UK, France, China, India, Japan, South Korea, Australia, Saudi Arabia, UAE, Brazil and Argentina |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global AI and ML in oil and gas market 2025-2029 is defined by the pervasive integration of intelligent technologies across operations. Core applications include ai-powered process control and production optimization platforms, which are now standard for maximizing yields.

- In the upstream sector, seismic data interpretation and reservoir characterization ml are being revolutionized by subsurface imaging algorithms and deep learning models, enabling more accurate subsurface decision analysis. This is complemented by predictive drilling analytics and the deployment of autonomous drilling systems, which leverage real-time geosteering ai and wellbore stability analysis to mitigate drilling hazard prediction.

- Asset integrity management is a critical focus, with prescriptive maintenance ai and iot sensor data analysis driving reliability. Midstream operations benefit from pipeline integrity monitoring, while downstream sees advances in refinery optimization ai. A key trend is the use of natural language processing for reports and generative ai knowledge management.

- Technologically, the market relies on edge ai for remote assets, digital twin simulation, and high-performance computing for ai supported by data mesh architecture. Enhanced oil recovery modeling, carbon capture utilization storage ai, and methane emissions detection are key for sustainability.

- Other innovations include smart ship operations, automated drilling optimization, real-time production monitoring, ai-driven demand forecasting, and ai-powered inspection robots, with anomaly detection algorithms improving safety. This strategic shift has enabled firms to achieve a 30% reduction in data processing time, directly influencing boardroom decisions on capital allocation and ESG compliance.

What are the Key Data Covered in this AI And ML In Oil And Gas Market Research and Growth Report?

-

What is the expected growth of the AI And ML In Oil And Gas Market between 2025 and 2029?

-

USD 5.91 billion, at a CAGR of 15.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions, and Services), Application (Predictive maintenance, Production optimization, Supply chain and logistics, Exploration and drilling, and Others), End-user (Downstream, Upstream, and Midstream) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Imperative for enhanced operational efficiency and cost reduction, Pervasive data management and integration issues

-

-

Who are the major players in the AI And ML In Oil And Gas Market?

-

ABB Ltd., Accenture PLC, Baker Hughes Co., Beyond Limits, BP Plc, C3.ai Inc., Exxon Mobil Corp., Google LLC, Halliburton Co., IBM Corp., Microsoft Corp., Oracle Corp., Saudi Arabian Oil Co., Schlumberger Ltd., SensorUp Inc., Shell plc, Siemens AG, SparkCognition Inc. and TechnipFMC plc

-

Market Research Insights

- The AI and ML in oil and gas market is characterized by a rapid shift toward intelligent automation in oilfield operations. The adoption of digital oilfield technologies and ai for exploration and production is accelerating project timelines by over 20%.

- In parallel, ml for downstream processes, including ai for petrochemical plants and autonomous refinery operations, is cutting energy waste by 15%, while machine learning in midstream enhances smart pipeline management. The deployment of ai-powered predictive maintenance and ai in asset performance management reduces unplanned downtime significantly.

- A focus on esg compliance with ai is driving investments in ai for emissions tracking and ai for carbon capture projects. The use of generative ai in energy sector and cognitive computing for geoscience is revolutionizing knowledge management.

- Technologies such as real-time drilling optimization, ai for enhanced oil recovery, and machine learning for well completion are central to maximizing asset value. The market also sees growth in specialized areas like ai for unconventional resources, ai applications in lng plants, and ai for subsea systems.

We can help! Our analysts can customize this ai and ml in oil and gas market research report to meet your requirements.

RIA -

RIA -