AI Audio Processing Software Market Size 2025-2029

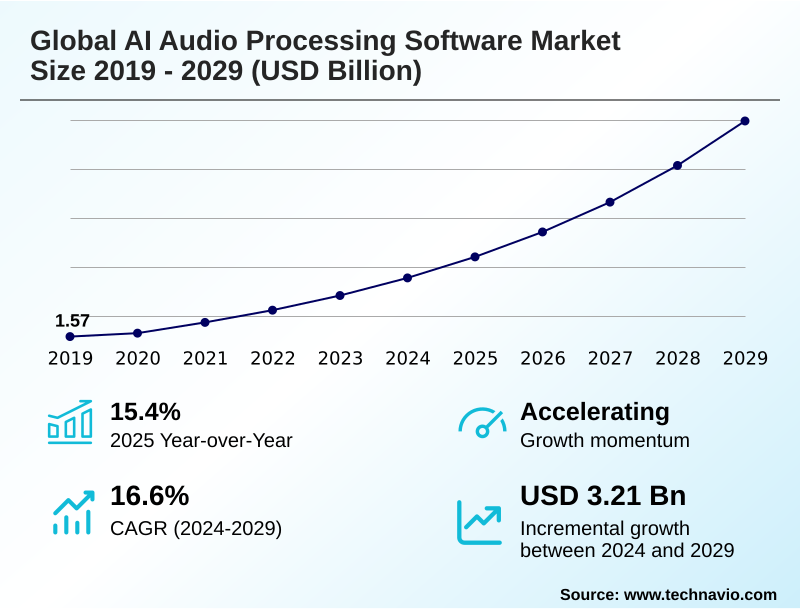

The ai audio processing software market size is valued to increase by USD 3.21 billion, at a CAGR of 16.6% from 2024 to 2029. Exponential growth in enterprise adoption for enhanced customer experience and operational efficiency will drive the ai audio processing software market.

Major Market Trends & Insights

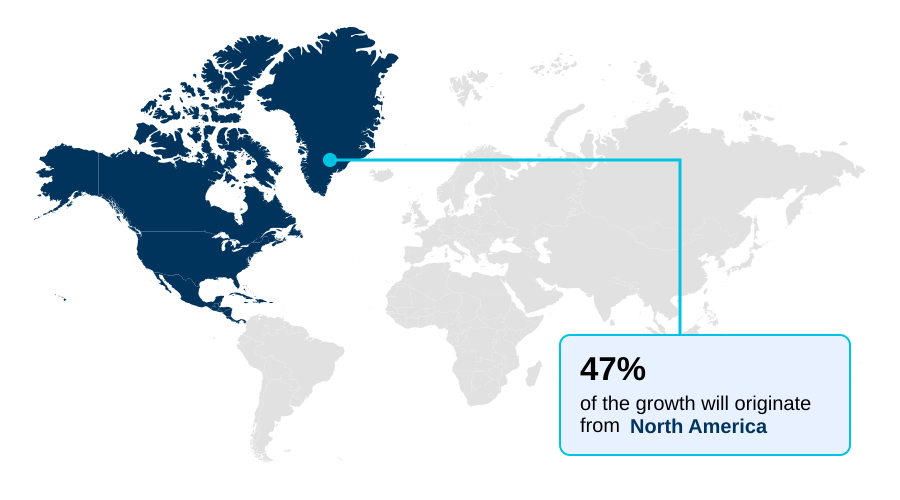

- North America dominated the market and accounted for a 47% growth during the forecast period.

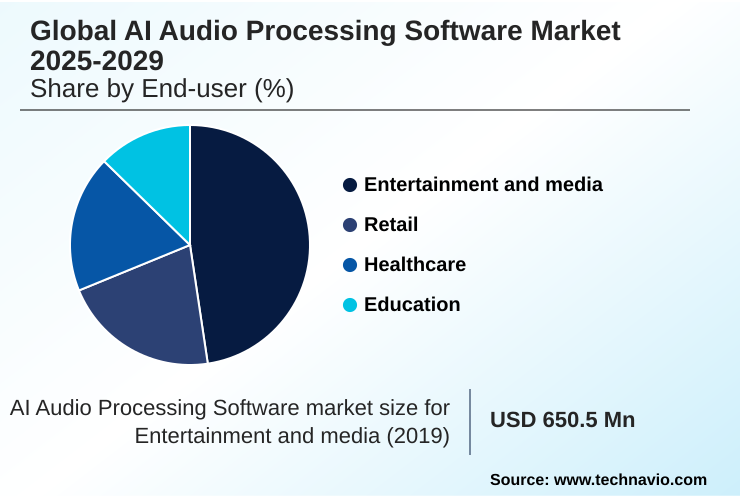

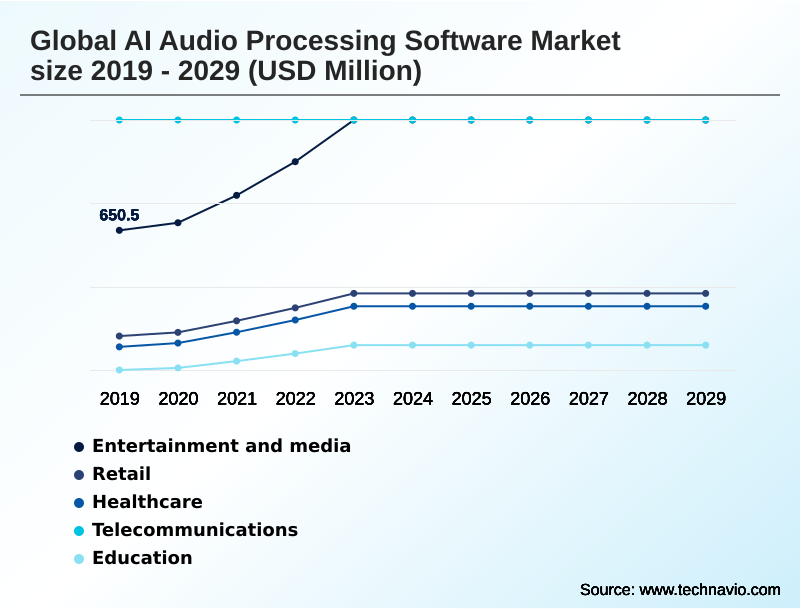

- By End-user - Entertainment and media segment was valued at USD 1.03 billion in 2023

- By Deployment - Cloud segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 4.41 billion

- Market Future Opportunities: USD 3.21 billion

- CAGR from 2024 to 2029 : 16.6%

Market Summary

- The AI audio processing software market is defined by technologies that analyze, interpret, and generate audio signals using advanced machine learning. Beyond simple signal processing, these platforms incorporate contextual audio understanding and predictive capabilities. Core functionalities like automatic speech recognition (ASR), real-time transcription, and natural language understanding are foundational.

- The market's expansion is driven by the integration of voice-activated interfaces into consumer and enterprise applications. A significant driver is the evolution of generative audio models, which enable hyper-realistic voice synthesis and voice cloning for digital content creation.

- In a practical business scenario, a financial services firm uses voice biometrics for secure authentication, while concurrently employing sentiment analysis from voice during customer calls to gauge satisfaction and ensure regulatory compliance, flagging interactions for review using keyword spotting. This reliance on low-latency audio processing and conversational AI platforms highlights the technology's role in improving both security and operational efficiency.

- However, the industry grapples with challenges related to algorithmic bias in voice recognition and the need for robust AI governance frameworks to address the risks of deepfake audio and ensure privacy-preserving AI. The move towards on-device processing using neural processing units (NPUs) is a key trend addressing these data security concerns.

What will be the Size of the AI Audio Processing Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI Audio Processing Software Market Segmented?

The ai audio processing software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Entertainment and media

- Retail

- Healthcare

- Telecommunication

- Education

- Deployment

- Cloud

- On premises

- Application

- Media production

- Customer service

- Communication tools

- Advertising and content

- Assistive technologies

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By End-user Insights

The entertainment and media segment is estimated to witness significant growth during the forecast period.

The entertainment and media industry leverages AI audio processing to automate workflows and enable new creative expressions. Technologies like automatic speech recognition (ASR) and real-time transcription accelerate captioning, while AI-powered noise suppression and audio restoration algorithms enhance post-production quality.

The rise of generative audio models is particularly transformative, enabling hyper-realistic voice synthesis for automated audiobook narration and AI-driven dubbing for global content distribution. This digital content creation is supported by procedural audio generation for dynamic soundscapes in gaming.

This focus on contextual audio understanding has led to workflow accelerations of over 40% in subtitling and localization tasks.

The use of on-device AI workloads and voice user interface (VUI) design is also becoming crucial for interactive media experiences that require low-latency audio processing. These creator economy tools are redefining content lifecycles.

The Entertainment and media segment was valued at USD 1.03 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 47% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Audio Processing Software Market Demand is Rising in North America Request Free Sample

The geographic landscape is led by North America, where a high concentration of technology firms drives innovation in AI-powered noise suppression and conversational AI platforms.

Enterprise adoption for contact center automation is a primary driver, with deployments showing up to a 15% improvement in first-call resolution rates.

In APAC, the market is characterized by mobile-first adoption, with on-device processing being critical for accessibility technology enhancement in diverse linguistic environments.

Europe's market is uniquely shaped by stringent AI governance frameworks, promoting demand for privacy-preserving AI and transparent audio watermarking solutions.

Key technologies like voice synthesis and speech recognition are being adapted for regional languages, with multilingual speech models becoming a competitive differentiator.

The growth in South America is fueled by the fintech sector's use of voice biometrics, where adoption has contributed to a 20% reduction in specific types of account takeover fraud.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The market's long-tail opportunities are found in specialized, high-value applications. A key debate centers on cloud vs on-device audio processing, with the latter being critical for low-latency speech recognition for automotive systems. In healthcare, AI for ambient clinical documentation is revolutionizing physician workflows, while vocal biomarker for neurological disease screening offers non-invasive diagnostic potential.

- The entertainment sector is being transformed by generative AI for video game dialogue and hyper-realistic synthetic voice for audiobooks, alongside automated audio mastering for musicians and AI music generation from text prompts. Real-time voice cloning for dubbing is making global content more accessible.

- For enterprise and security, voice biometrics for financial fraud detection and sentiment analysis in customer service calls are delivering measurable ROI. For instance, contact centers using sentiment analysis report agent performance improvements nearly double that of those relying only on call duration metrics.

- Other critical use cases include neural noise cancellation for collaboration tools, speaker diarization in multi-participant calls, and AI-powered audio restoration for archives. The technology also underpins on-device AI for smart home assistants, AI-based audio watermarking for security, and text-to-speech for personalized marketing.

- Even industrial settings benefit from AI audio for predictive industrial maintenance, while assistive devices utilize context-aware hearing aid sound adjustment, and surveillance applications use AI audio analysis for public safety surveillance.

What are the key market drivers leading to the rise in the adoption of AI Audio Processing Software Industry?

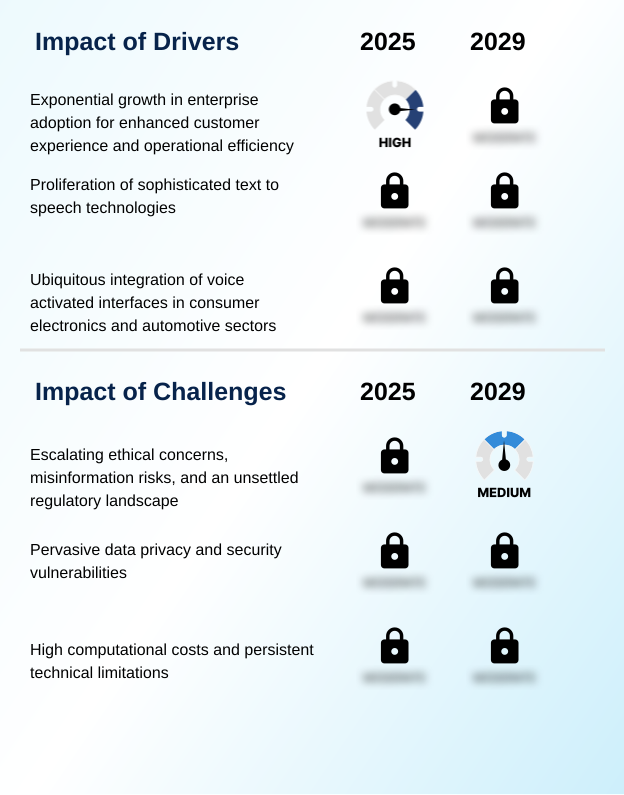

- A key market driver is the exponential growth in enterprise adoption, as businesses leverage AI audio processing software to enhance customer experiences and improve operational efficiency.

- A primary driver is escalating enterprise adoption for operational efficiency, particularly in contact center automation.

- Deploying speech-to-text (STT) and sentiment analysis from voice allows businesses to analyze 100% of customer interactions, compared to the 2-3% typical with manual reviews, uncovering critical insights.

- The proliferation of voice-activated interfaces in consumer electronics and automotive sectors is another major force, demanding sophisticated natural language understanding and robust noise cancellation technologies. This ubiquitous integration makes voice user interface (VUI) design a competitive necessity.

- Furthermore, the rapid advancements in large language models (LLMs) have fundamentally expanded the capabilities of text-to-speech (TTS) systems, making them suitable for brand marketing and intelligent meeting summaries, which have been shown to reduce post-meeting administrative work by up to 60%.

- These deep learning architectures are unlocking new value from audio data.

What are the market trends shaping the AI Audio Processing Software Industry?

- The market is experiencing a significant trend driven by proliferating demand for generative AI. This technology is being leveraged for hyper-realistic voice synthesis and scalable content creation.

- A transformative trend is the rapid commercialization of generative audio models for creating hyper-realistic voice synthesis. This capability, powered by transformer-based audio models, is disrupting media by enabling AI-driven dubbing and automated content creation, reducing production timelines by over 50% in certain localization workflows.

- Another key trend is the shift toward on-device processing, driven by consumer demand for privacy and low-latency interaction. This edge computing for audio is enabling more secure voice biometrics and is a core component of in-car intelligent assistants, where response time is critical. This migration is supported by hardware advancements allowing complex on-device AI workloads.

- The focus on contextual audio understanding is also growing, with systems moving beyond simple commands to holistic acoustic scene classification, improving user experience in smart devices by an estimated 40% in noisy environments.

What challenges does the AI Audio Processing Software Industry face during its growth?

- A key challenge affecting industry growth involves escalating ethical concerns, the risks of misinformation, and navigating an unsettled regulatory landscape.

- The market faces significant challenges from the high computational resource requirements needed to train state-of-the-art models, where training costs can be over 70% of a project's initial budget. This creates a high barrier to entry. Another major restraint involves ethical AI development and the risks posed by deepfake audio.

- The potential for misuse in creating misinformation has led to intense regulatory scrutiny, with proposed AI governance frameworks threatening to impose heavy compliance burdens. Data privacy is also a critical concern; navigating regulations requires significant investment in privacy-preserving AI architectures and transparent data minimization principles.

- Technical limitations also persist, including algorithmic bias in voice recognition for non-native speakers, which can see error rates increase by more than 25% compared to standard dialects, hindering global inclusivity and market penetration of audio deepfake detection systems.

Exclusive Technavio Analysis on Customer Landscape

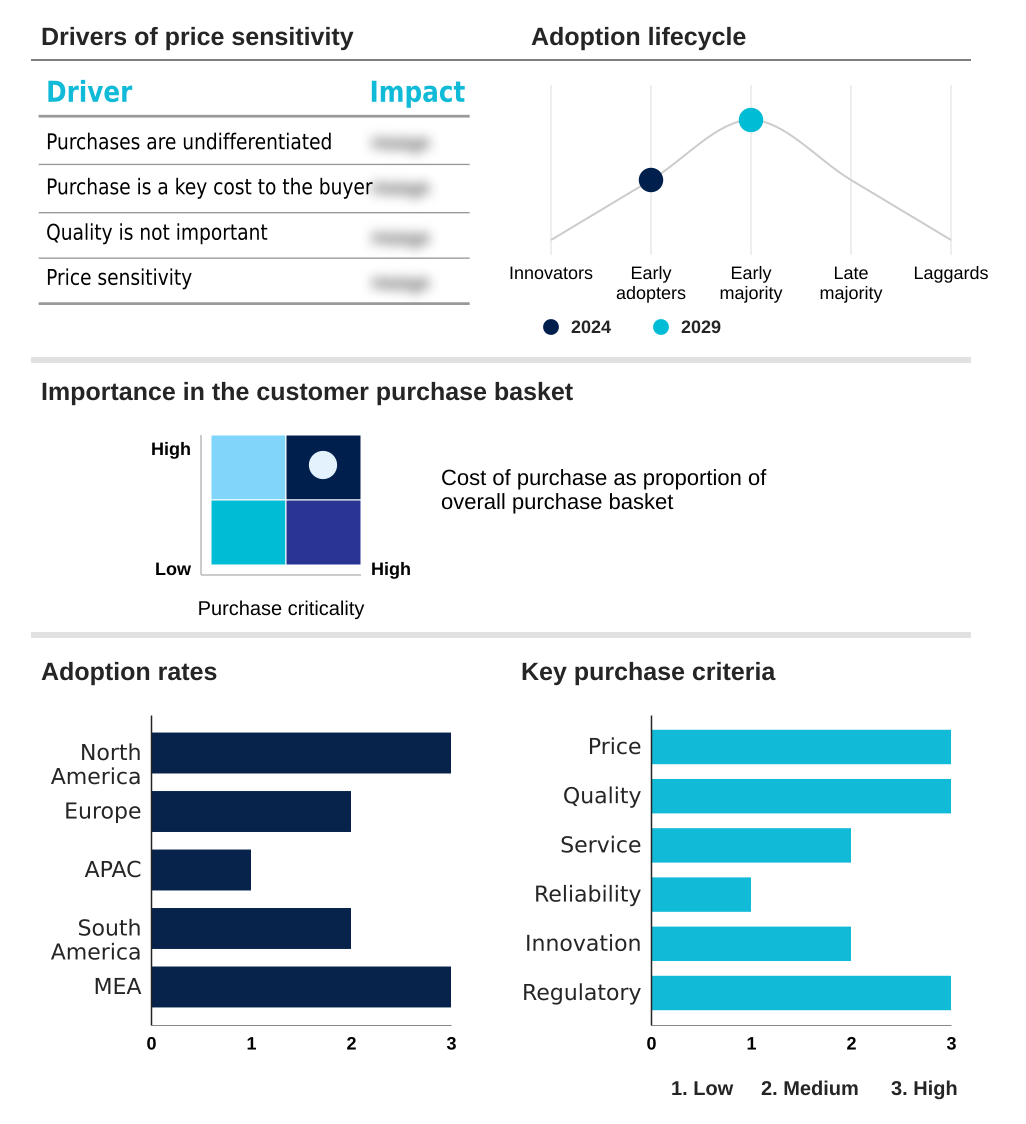

The ai audio processing software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai audio processing software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Audio Processing Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai audio processing software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Offerings include enterprise-grade speech-to-text, text-to-speech synthesis, and advanced call analytics, enabling data-driven insights for contact center operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- Apple Inc.

- AssemblyAI

- Deepgram Inc.

- DOLBY LABORATORIES INC.

- Google Cloud

- iFLYTEK Co. Ltd.

- IBM Corp.

- Krisp Technologies Inc.

- LOVO Inc

- LumenVox GmbH

- Microsoft Corp.

- Resemble AI

- Sensory Inc.

- SoundHound AI Inc.

- Speechmatics

- Verbit.ai

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai audio processing software market

- In September, 2024, a leading European luxury automaker announced a strategic partnership with a conversational AI specialist to deploy a next-generation, proactive in-car assistant across its entire 2026 model lineup, focusing on hyper-personalized driver experiences.

- In November, 2024, a major enterprise software corporation acquired a prominent generative voice AI startup for over USD 2 billion, aiming to integrate its real-time voice cloning and synthesis technology into its collaboration and content creation suites.

- In February, 2025, a consortium of APAC-based technology firms and research institutions launched a new initiative to build foundation models for Southeast Asian languages, releasing an open-source multilingual speech model to accelerate regional AI audio application development.

- In April, 2025, a prominent semiconductor company unveiled a new chipset with a dedicated NPU optimized for on-device multimodal AI, enabling real-time audio translation and ambient sound analysis on next-generation laptops and edge devices with a 40% improvement in power efficiency.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Audio Processing Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16.6% |

| Market growth 2025-2029 | USD 3209.1 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 15.4% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI audio processing software market is driven by the enterprise need to convert unstructured audio into actionable data. Core technologies include automatic speech recognition (ASR) for real-time transcription and natural language understanding for interpreting intent. The rise of generative audio models is enabling voice synthesis and voice cloning, while on-device processing via neural processing units (NPUs) addresses privacy concerns.

- Computational sound scene analysis and ambient intelligence are moving beyond simple keyword spotting to holistic environmental understanding, using techniques like speaker diarization and acoustic event detection. In practice, applications range from ambient clinical intelligence in healthcare to voice-directed warehousing. For example, communication platforms integrating AI-powered noise suppression have reported a 30% reduction in user-reported audio distractions.

- Security is a major vertical, employing voice biometrics and voiceprint analysis for authentication and audio watermarking to combat deepfake audio. Key functionalities like text-to-speech (TTS), speech-to-text (STT), and low-latency audio processing are crucial for voice-activated interfaces. The evolution of conversational AI platforms is supported by large language models (LLMs) and TinyML for audio.

- Creative fields utilize procedural audio generation and audio restoration algorithms, while consumer tech leverages spatial audio processing and vocal biomarker analysis.

What are the Key Data Covered in this AI Audio Processing Software Market Research and Growth Report?

-

What is the expected growth of the AI Audio Processing Software Market between 2025 and 2029?

-

USD 3.21 billion, at a CAGR of 16.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Entertainment and media, Retail, Healthcare, Telecommunications, Education), Deployment (Cloud, On premises), Application (Media production, Customer service, Communication tools, Advertising and content, Assistive technologies) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Exponential growth in enterprise adoption for enhanced customer experience and operational efficiency, Escalating ethical concerns, misinformation risks, and an unsettled regulatory landscape

-

-

Who are the major players in the AI Audio Processing Software Market?

-

Amazon Web Services Inc., Apple Inc., AssemblyAI, Deepgram Inc., DOLBY LABORATORIES INC., Google Cloud, iFLYTEK Co. Ltd., IBM Corp., Krisp Technologies Inc., LOVO Inc, LumenVox GmbH, Microsoft Corp., Resemble AI, Sensory Inc., SoundHound AI Inc., Speechmatics and Verbit.ai

-

Market Research Insights

- Market dynamics are shaped by the convergence of deep learning architectures and enterprise demand for efficiency. The adoption of contact center automation has shown to reduce average handling times by up to 30%, a direct result of effective real-time agent assist technologies.

- Meanwhile, the creator economy tools landscape is being reshaped by hyper-realistic voice synthesis, enabling content producers to achieve studio-quality audio without traditional overhead. The integration into in-car intelligent assistants has improved command recognition accuracy in noisy environments by over 25%. These advancements, coupled with a focus on ethical AI development and AI governance frameworks, are critical for market acceptance.

- Firms leveraging these capabilities are achieving significant operational gains, with accessibility technology enhancement also emerging as a key value proposition. This is all balanced by the high computational resource requirements needed for such advanced systems.

We can help! Our analysts can customize this ai audio processing software market research report to meet your requirements.

RIA -

RIA -