AI Based 3D Vision System Market Size 2025-2029

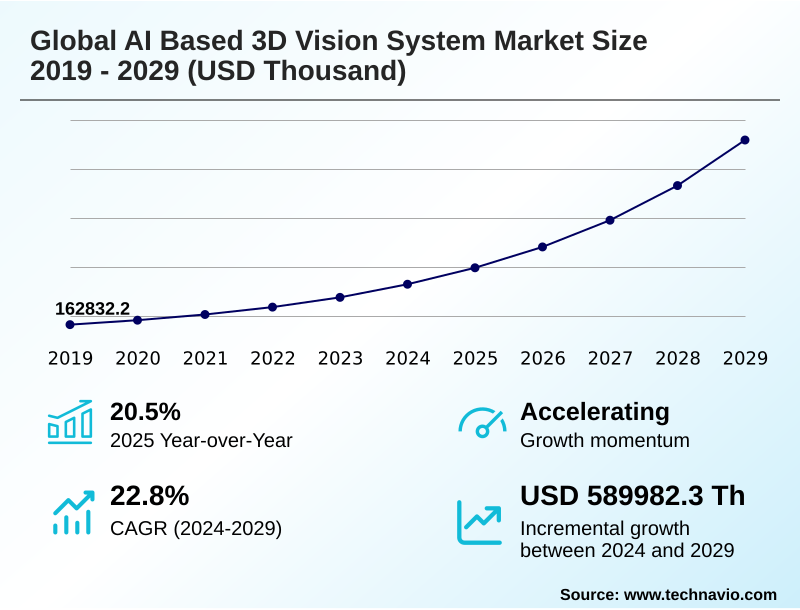

The ai based 3d vision system market size is valued to increase by USD 589.98 million, at a CAGR of 22.8% from 2024 to 2029. Rising imperative for automation and enhanced quality control across industries will drive the ai based 3d vision system market.

Major Market Trends & Insights

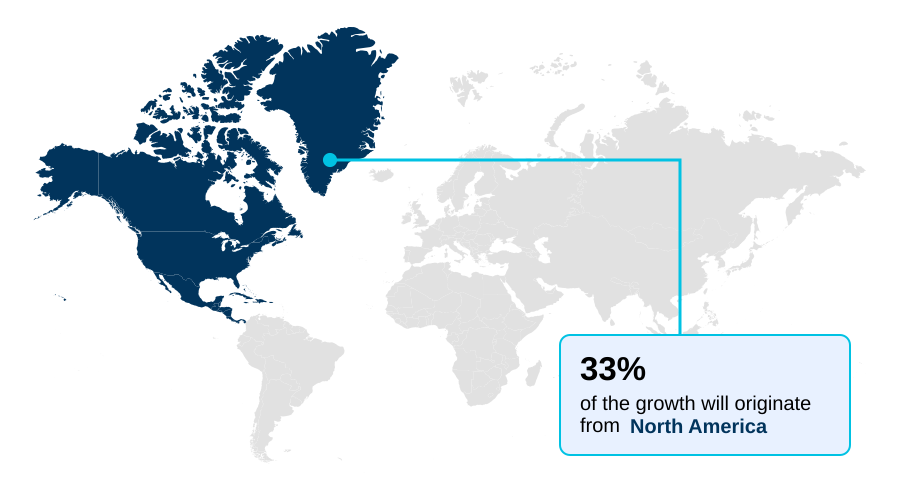

- North America dominated the market and accounted for a 33.1% growth during the forecast period.

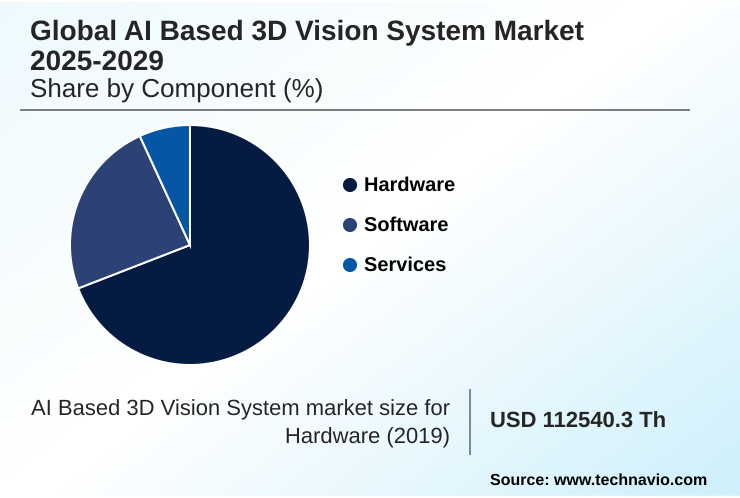

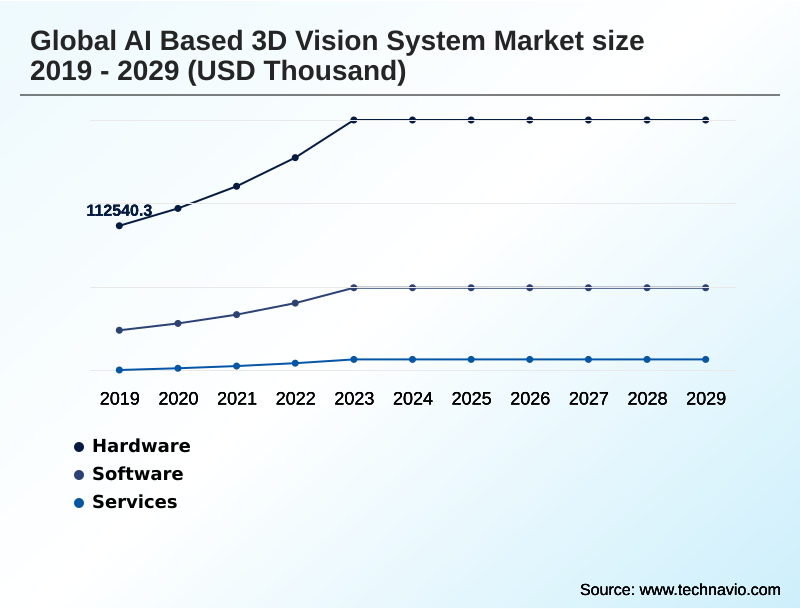

- By Component - Hardware segment was valued at USD 186.84 million in 2023

- By Type - PC based segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 589.98 million

- CAGR from 2024 to 2029 : 22.8%

Market Summary

- The AI based 3D vision system market is defined by the integration of advanced 3d imaging technologies with powerful artificial intelligence to grant machines sophisticated visual perception. This synergy enables systems to move beyond simple 2D analysis, utilizing technologies like stereo vision and structured light scanners to interpret depth and volume for complex tasks.

- Key market drivers include the push for Industry 4.0 automation and superior quality assurance in manufacturing. A key trend is the convergence of AI with edge computing, allowing for real-time processing and decision-making directly on devices.

- For instance, in a smart factory environment, an assembly line robot uses an embedded vision system for real-time robotic guidance, instantly detecting and adjusting for misaligned components, thereby preventing defects without halting production. This capability relies on sophisticated computer vision and deep learning models to perform dimensional measurement and automated inspection with high precision.

- However, challenges such as high implementation costs, the need for skilled personnel, and concerns over data privacy temper the pace of adoption. The market's evolution is geared towards more accessible, powerful, and integrated solutions that address these operational hurdles, expanding applications into sectors like logistics and healthcare.

What will be the Size of the AI Based 3D Vision System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI Based 3D Vision System Market Segmented?

The ai based 3d vision system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Software

- Services

- Type

- PC based

- Smart camera based

- Others

- Application

- Quality assurance and inspection

- Positioning and guidance

- Measurement

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- Israel

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment, encompassing high-resolution cameras, graphic processing units, and specialized sensor fusion technologies, forms the essential physical foundation for the market.

Continuous innovation in hardware is a primary engine of market expansion, with advancements in time-of-flight sensors and structured light scanners making 3d imaging technologies more accessible.

A pivotal trend is the integration of AI with edge computing, which allows for real-time processing of point clouds directly on devices. This powerful combination is critical for applications demanding instantaneous decision-making, such as robotic guidance in manufacturing.

By localizing data processing, these systems can reduce data transmission needs by over 90%, enhancing both speed and cybersecurity for critical infrastructure. This supports complex tasks like dimensional measurement and quality assurance.

The Hardware segment was valued at USD 186.84 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Based 3D Vision System Market Demand is Rising in North America Request Free Sample

The geographic landscape of the AI based 3D vision system market is shaped by regional industrial strengths and strategic technology investments.

North America leads, contributing over 33% of the market's incremental growth, driven by its advanced manufacturing and logistics sectors' demand for robotic automation solutions and process automation. The region is a hub for innovation in neural networks and software platforms.

APAC is the largest market, characterized by government-led smart manufacturing initiatives and a massive electronics production base, fostering rapid adoption of automated inspection and quality control systems.

In Europe, the focus on Industry 4.0 principles fuels demand for systems that improve operational efficiency; implementations can reduce production line downtime by up to 20%.

Both regions heavily leverage vision intelligence platforms and machine learning algorithms to maintain a competitive edge through enhanced visual perception and predictive maintenance.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of AI based 3D vision systems is reshaping industrial operations, with a strong focus on specialized applications. The use of deep learning for automated inspection is becoming a standard in high-precision manufacturing, where machine vision systems for defect detection can identify microscopic flaws that are invisible to the human eye.

- In the logistics sector, the adoption of AI based 3D vision for logistics is crucial for enabling computer vision for warehouse automation, allowing robots to perform complex bin-picking tasks with high accuracy.

- The trend towards ai vision systems with edge computing addresses latency issues, which is critical for ai for real time robotic guidance on fast-moving production lines and in ai vision in autonomous vehicle navigation. The development of generative AI for 3d model generation is further expanding capabilities, allowing for rapid digital twin creation.

- As industries advance, the demand for ai powered predictive analytics in manufacturing grows, leveraging data from vision systems to prevent equipment failure. Applications are also expanding into healthcare with ai algorithms for 3d medical imaging and ai based vision for surgical navigation.

- However, challenges persist, including the complexity of integrating ai vision with legacy equipment and ensuring data security in cloud based vision systems. The industry is also tackling the need for a skilled workforce for AI vision deployment, addressing everything from the nuances of ai vision for driver monitoring systems to the detailed cost analysis of AI 3d vision systems.

- The use of time of flight sensors for robotics and structured light scanning for quality control is becoming more widespread, even in areas like ai vision for food and beverage processing, where solutions that are more than twice as efficient as manual methods are being deployed.

What are the key market drivers leading to the rise in the adoption of AI Based 3D Vision System Industry?

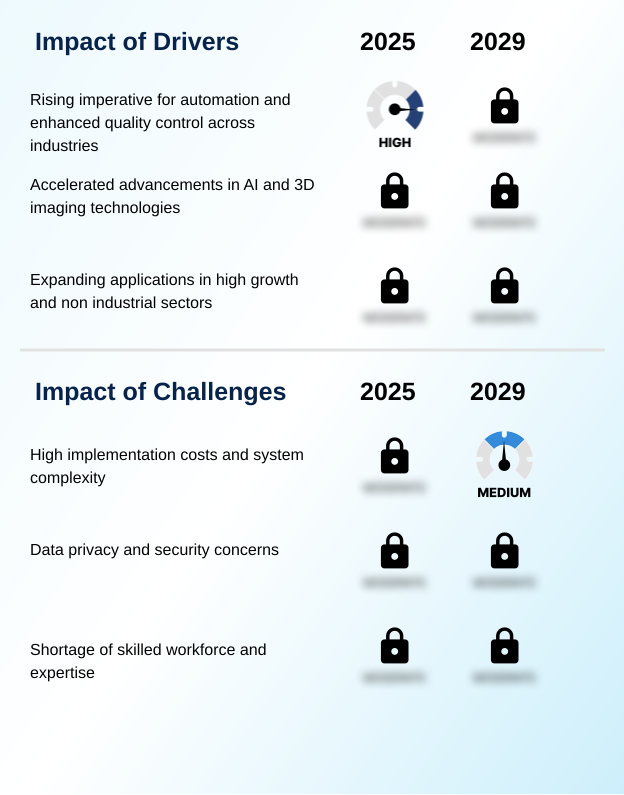

- The rising imperative for enhanced quality control and widespread automation across industries serves as the primary driver for market growth.

- Market growth is fundamentally driven by the industrial imperative for higher efficiency and quality.

- The integration of robotic guidance systems powered by 3d imaging technologies and neural networks is automating complex tasks, leading to scrap rate reductions of up to 15% in high-volume manufacturing.

- Accelerated advancements in AI and 3D imaging are making real-time processing more accessible, allowing for immediate quality assurance checks on production lines.

- In the logistics sector, the use of AI-powered robotic bin picking and sorting is improving order fulfillment accuracy to over 99.9%.

- The expansion into non-industrial sectors like healthcare is also significant, with medical imaging and surgical navigation benefiting from the precision offered by these technologies, enabling better patient outcomes. These drivers reflect a broad-based demand for enhanced visual perception across industries.

What are the market trends shaping the AI Based 3D Vision System Industry?

- The proliferation of deep learning is revolutionizing automated quality control and inspection processes. This represents a significant upcoming trend, driving superior performance and cognitive capabilities in the market.

- Market trends are defined by the convergence of intelligent software and powerful hardware, expanding the scope of automated tasks. The proliferation of deep learning is enabling superior object recognition and defect detection, with adoption rates in logistics projected to more than double as firms replace manual processes.

- This is driven by advanced vision AI platform solutions and the use of large language models to simplify system interaction. A significant trend is the shift toward edge computing, where new system-on-chips (SoCs) enable real-time processing and contextual decision-making directly on devices like autonomous mobile robots.

- This approach enhances data privacy and supports applications in surgical navigation and augmented reality, where latency is critical. These advancements in computer vision and machine learning algorithms are making systems more intuitive and powerful.

What challenges does the AI Based 3D Vision System Industry face during its growth?

- High implementation costs combined with inherent system complexity present a key challenge that affects the industry's growth trajectory.

- Despite strong drivers, market adoption faces significant hurdles related to cost, complexity, and security. The total cost of ownership for an AI vision system can be three to five times the initial hardware price due to expenses for software platforms, system integration, and specialized expertise. This financial barrier is particularly challenging for small and medium-sized enterprises.

- Furthermore, profound data privacy and cybersecurity concerns arise from the collection of detailed visual data, including biometric information, which can be targets for industrial espionage. Navigating complex regulatory landscapes adds another layer of difficulty.

- The shortage of a skilled workforce with expertise in computer vision, robotics, and machine learning leads to intense competition for talent, with acquisition costs increasing by over 20% in some regions.

Exclusive Technavio Analysis on Customer Landscape

The ai based 3d vision system market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai based 3d vision system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Based 3D Vision System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai based 3d vision system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Cutting-edge robotic automation solutions are delivered through proprietary 4D vision technology and specialized robotic vision software, enabling ultra-fast, precise, and reliable vision-guided tasks for complex operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- Apera AI

- AVEVA Group Plc

- Avnet Inc.

- Chooch Intelligence Technologies Co.

- Cognex Corp.

- Google LLC

- Intel Corp.

- IBM Corp.

- Landing AI

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Qualcomm Inc.

- Robovision BV

- Skyhaus BV

- STMicroelectronics NV

- Symphony Innovation LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai based 3d vision system market

- In August 2024, Zebra Technologies Corp. revealed a major upgrade to its Aurora machine vision software, introducing a new suite of AI tools to address complex visual inspection challenges with sophisticated deep learning models.

- In December 2024, Zivid announced the availability of its Zivid 2+ R-series cameras, specifically engineered to improve robot cycle times in logistics applications, including for historically difficult transparent and shiny objects.

- In January 2025, Zebra Technologies announced the acquisition of Photoneo, a move designed to strengthen its 3D machine vision capabilities and expand its portfolio for industrial automation in manufacturing and logistics.

- In February 2025, Fabrica Machinale Srl's Roboticom division showcased its SandRob system, a robotic solution for surface finishing that utilizes an AI-driven vision system and advanced learning algorithms to recognize surface defects and optimize processes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Based 3D Vision System Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 22.8% |

| Market growth 2025-2029 | USD 589982.3 thousand |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 20.5% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, Brazil, Argentina, Colombia, UAE, Saudi Arabia, Israel, South Africa and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a significant transformation driven by the fusion of 3d imaging technologies with sophisticated AI. The core of this evolution lies in the enhanced visual perception and scene comprehension these systems provide for industrial automation.

- The deployment of deep learning models and neural networks enables unprecedented levels of precision in defect detection and robotic guidance, moving far beyond traditional machine vision capabilities. A critical development fueling this adoption is the dramatic reduction in complexity and time required for system training; the training duration for complex AI models has been reduced from weeks to mere hours.

- This acceleration is making advanced automated inspection and dimensional measurement accessible to a broader range of applications. Technologies such as stereo vision and time of flight sensors, processed by powerful graphic processing units, are foundational.

- The market is now focused on optimizing system integration and overcoming challenges related to high initial costs and cybersecurity to unlock the full potential of real-time processing and spatial awareness in manufacturing and beyond.

What are the Key Data Covered in this AI Based 3D Vision System Market Research and Growth Report?

-

What is the expected growth of the AI Based 3D Vision System Market between 2025 and 2029?

-

USD 589.98 million, at a CAGR of 22.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, Services), Type (PC based, Smart camera based, Others), Application (Quality assurance and inspection, Positioning and guidance, Measurement) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising imperative for automation and enhanced quality control across industries, High implementation costs and system complexity

-

-

Who are the major players in the AI Based 3D Vision System Market?

-

Amazon Web Services Inc., Apera AI, AVEVA Group Plc, Avnet Inc., Chooch Intelligence Technologies Co., Cognex Corp., Google LLC, Intel Corp., IBM Corp., Landing AI, Microsoft Corp., NVIDIA Corp., Oracle Corp., Qualcomm Inc., Robovision BV, Skyhaus BV, STMicroelectronics NV and Symphony Innovation LLC

-

Market Research Insights

- The market is characterized by a dynamic interplay of advanced hardware and intelligent software, driving significant efficiency gains across industries. The adoption of AI-enabled vision systems in warehouse operations has surged, with projections indicating usage will more than double as companies replace traditional scanning methods.

- This shift is enabled by robust robotic automation solutions and sophisticated vision AI assistant platforms that deliver contextual decision-making. These systems leverage multi-camera edge AI and advanced vision intelligence platforms to achieve operational excellence. For instance, manufacturers are reporting defect detection accuracy rates exceeding 99.5%, a substantial improvement over manual inspection.

- This precision minimizes waste and enhances product quality, underscoring the technology's transformative impact on process automation and quality control, leading to a strong return on investment.

We can help! Our analysts can customize this ai based 3d vision system market research report to meet your requirements.

RIA -

RIA -