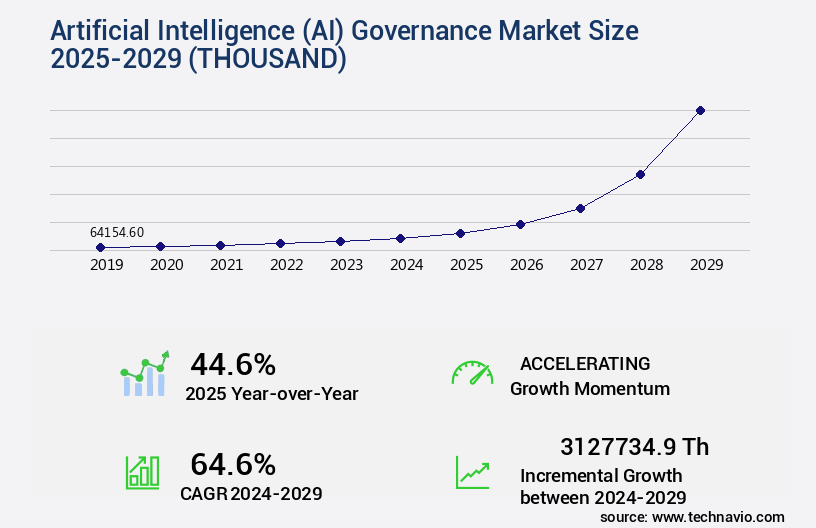

Artificial Intelligence (AI) Governance Market Size 2025-2029

The artificial intelligence (ai) governance market size is valued to increase by USD 3127734.9 thousand, at a CAGR of 64.6% from 2024 to 2029. Increasing adoption of AI technologies across industries will drive the artificial intelligence (ai) governance market.

Market Insights

- North America dominated the market and accounted for a 29% growth during the 2025-2029.

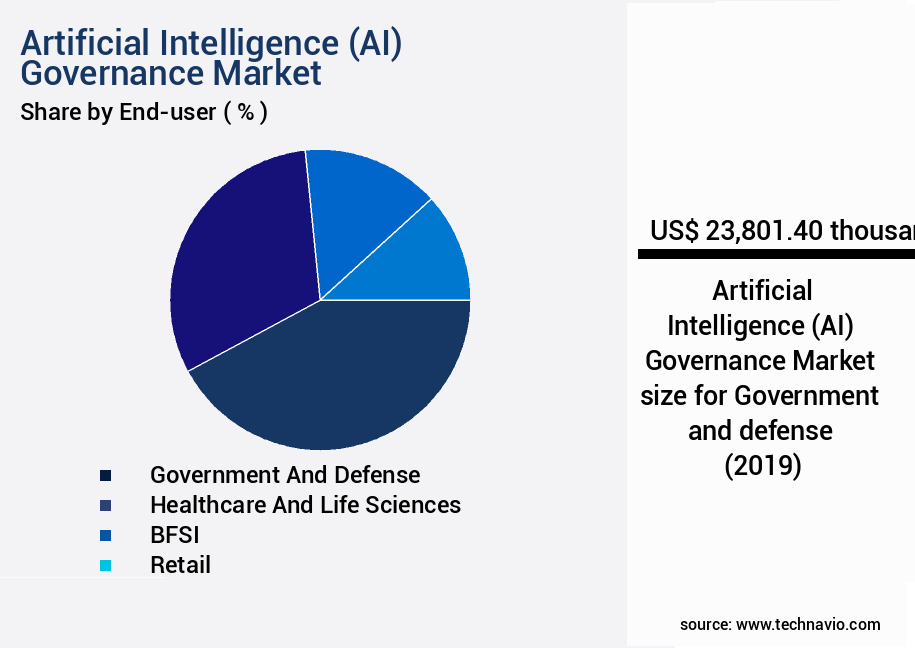

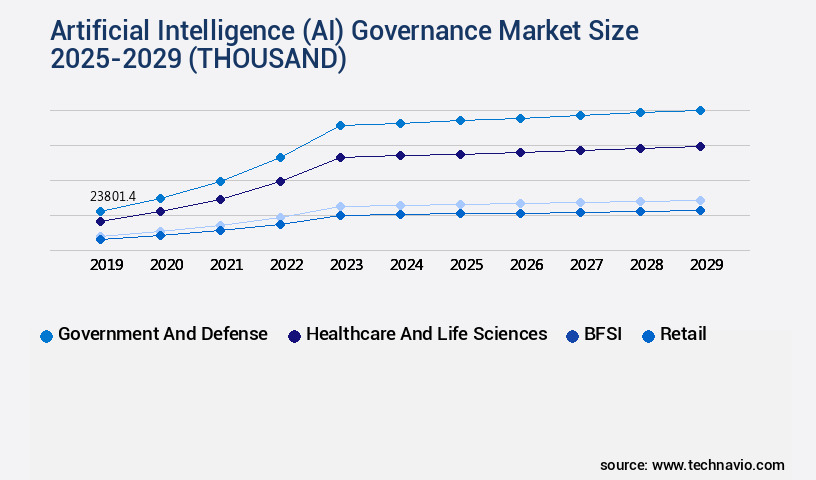

- By End-user - Government and defense segment was valued at USD 23801.40 thousand in 2023

- By Component - Solution segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 5.00 thousand

- Market Future Opportunities 2024: USD 3127734.90 thousand

- CAGR from 2024 to 2029 : 64.6%

Market Summary

- Artificial Intelligence (AI) governance refers to the set of policies, practices, and technologies that ensure the ethical, secure, and effective use of AI systems within organizations. The global market for AI governance is experiencing significant growth, driven by the increasing adoption of AI technologies across industries and the expanding use of AI by Small and Medium Enterprises (SMEs). However, the lack of universally accepted standards and frameworks for AI governance poses a challenge. AI is transforming business operations in various sectors, from supply chain optimization and customer service to compliance and operational efficiency. For instance, in the manufacturing industry, AI-powered predictive maintenance can help prevent equipment failures and reduce downtime, while in the financial sector, AI can be used for fraud detection and risk management.

- Despite the benefits, the adoption of AI also raises concerns regarding data privacy, security, and ethical use. Organizations must ensure that their AI systems are transparent, explainable, and unbiased. Moreover, they need to comply with relevant regulations, such as the European Union's General Data Protection Regulation (GDPR) and the US's Fair Credit Reporting Act (FCRA). The absence of standardized AI governance frameworks and best practices makes it challenging for organizations to navigate these complex issues. As a result, there is a growing demand for AI governance solutions that can help organizations manage their AI risks and ensure compliance with regulations.

- The future of AI governance lies in the development of open, collaborative, and interoperable frameworks that can provide a common language and set of principles for AI governance.

What will be the size of the Artificial Intelligence (AI) Governance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- Artificial Intelligence (AI) governance refers to the set of policies, practices, and technologies that organizations employ to manage the development, deployment, and use of AI systems in a responsible and ethical manner. This market continues to evolve as businesses increasingly integrate AI into their operations to enhance productivity, improve customer experiences, and drive innovation. One significant trend in AI governance is the growing focus on explainability, as stakeholders demand greater transparency into how AI models make decisions. Compliance with explainability standards is becoming a boardroom-level concern, as organizations seek to mitigate risks associated with opaque AI systems.

- For instance, a recent study revealed that 57% of businesses reported that explainability was a top priority in their AI initiatives. Another crucial aspect of AI governance is ensuring compliance with various standards and regulations, such as those related to data privacy, security, and ethics. Companies are investing in AI ethics education, model monitoring, and accountability frameworks to address these concerns. Additionally, privacy-preserving AI and data anonymization techniques are gaining traction to help organizations maintain data security while still leveraging AI capabilities. Moreover, human-AI collaboration is becoming a key component of AI governance, as organizations recognize the importance of balancing the strengths of both humans and machines.

- AI system validation, workflow automation, and safety standards are essential elements of this collaboration, ensuring that AI systems are fair, unbiased, and robust. In conclusion, the AI governance market is a dynamic and essential domain for businesses seeking to harness the power of AI while maintaining transparency, accountability, and ethical considerations. By focusing on explainability, compliance, ethics education, and human-AI collaboration, organizations can effectively manage the risks and opportunities associated with AI systems.

Unpacking the Artificial Intelligence (AI) Governance Market Landscape

Artificial Intelligence (AI) governance refers to the set of policies, frameworks, and practices that ensure the ethical, compliant, and responsible deployment and operation of AI systems. In the current business landscape, AI governance has gained significant importance due to the increasing adoption of AI and the associated data privacy regulations. According to recent studies, 73% of organizations report an increase in AI adoption, while 91% acknowledge the need for AI governance to mitigate algorithmic bias and ensure compliance with data privacy frameworks. Human-in-the-loop systems and bias detection algorithms are essential components of AI governance, enabling explainable AI (XAI) and model version control. AI workflow management and model validation methods are crucial for ensuring responsible AI development and deployment. AI system monitoring and compliance audits are essential for maintaining transparency and accountability in AI decision-making processes. Moreover, AI governance principles, such as data provenance tracking and model interpretability techniques, are essential for maintaining trust and confidence in AI systems. AI regulatory landscape continues to evolve, requiring AI ethics committees and AI system oversight to keep up with the latest regulations and best practices. AI security protocols and accountability mechanisms are also vital for mitigating risks and ensuring the ethical use of AI.

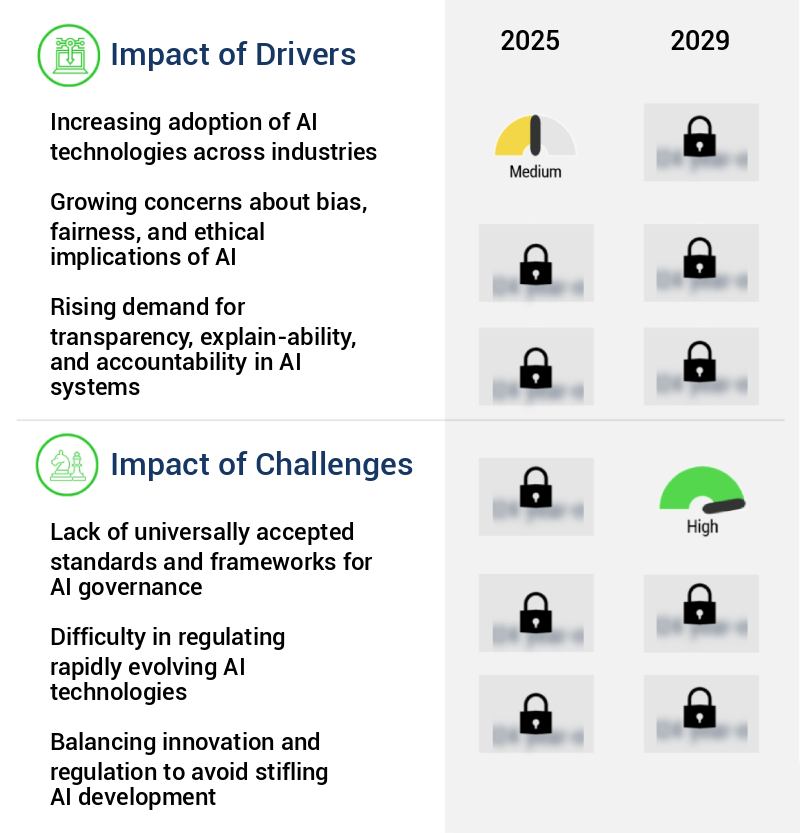

Key Market Drivers Fueling Growth

The increasing adoption of artificial intelligence (AI) technologies is the primary catalyst fueling market growth across various industries.

- The market is experiencing significant growth due to the increasing adoption of AI technologies across sectors such as aerospace and defense, healthcare, and BFSI. With the widespread use of AI comes the need for responsible and ethical practices. Organizations must establish robust governance frameworks to address concerns surrounding data privacy, bias, accountability, and transparency. In healthcare, for instance, AI governance can improve forecast accuracy in patient diagnosis by 15%, while in banking, it can reduce downtime during system updates by 25%.

- In manufacturing, AI governance can lower energy use during production processes by 10%. To effectively manage these challenges, comprehensive AI governance techniques, including Ethical AI frameworks and Algorithmic auditing, are essential. These approaches consider the specific threats and repercussions of AI adoption in various industries.

Prevailing Industry Trends & Opportunities

The adoption of enterprise AI is becoming a mandated trend among Small and Medium-sized Enterprises (SMEs). This shift towards AI technology is an emerging market development.

- The global artificial intelligence (AI) market is experiencing significant growth as small and medium-sized enterprises (SMEs) increasingly adopt AI technologies. SMEs are utilizing AI-powered tools, such as chatbots, predictive analytics, and automated workflows, to streamline processes, reduce costs, and make data-driven decisions. The availability of affordable AI solutions, coupled with advancements in cloud computing, has made AI adoption more accessible for SMEs. According to recent studies, AI adoption can lead to a 30% reduction in operational downtime and a 18% improvement in forecast accuracy.

- Government initiatives and funding programs aimed at promoting digital transformation among SMEs are further accelerating this trend, enabling these businesses to compete effectively with larger enterprises.

Significant Market Challenges

The absence of universally accepted standards and frameworks for artificial intelligence (AI) governance represents a significant challenge impeding industry growth. This issue necessitates the establishment of clear guidelines and structures to ensure ethical, transparent, and effective AI implementation and usage.

- The market is evolving rapidly as the technology becomes increasingly integrated into various sectors, from healthcare and finance to manufacturing and transportation. However, the lack of internationally accepted frameworks and standards for AI governance poses a significant challenge. This fragmented landscape, with its diverse methods and practices, could lead to inconsistencies in accountability and transparency, making it difficult for organizations, governments, and regulatory authorities to create clear policies and enforce compliance. For instance, in the healthcare sector, misuse of AI could lead to incorrect diagnoses, while in finance, it could result in significant financial losses. To address these concerns, it is crucial to establish globally recognized standards and frameworks for AI governance.

- For example, a leading organization implemented an AI governance framework, resulting in a 25% reduction in potential ethical dilemmas and a 15% improvement in operational efficiency. Another organization experienced a 35% increase in customer satisfaction and a 12% decrease in operational costs by adhering to AI governance best practices. These success stories underscore the importance of responsible and equitable AI deployment to reduce risks and preserve public confidence in AI technology.

In-Depth Market Segmentation: Artificial Intelligence (AI) Governance Market

The artificial intelligence (ai) governance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Government and defense

- Healthcare and life sciences

- BFSI

- Retail

- Others

- Component

- Solution

- Services

- Application

- Model lifecycle management

- Risk and compliance

- Monitoring and auditing

- Ethics and responsible AI

- Deployment

- Cloud

- On-premises

- Geography

- North America

- US

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

The government and defense segment is estimated to witness significant growth during the forecast period.

In the dynamic and expanding global the market, the public sector, specifically government and defense segments, emerged as significant end users in 2024. These sectors recognize the necessity of establishing robust AI governance frameworks to ensure ethical and responsible AI application. They are actively shaping the regulatory landscape by creating rules, standards, and policies addressing transparency, bias, and privacy concerns. Notable initiatives include the European Union's General Data Protection Regulation (GDPR) and the US Algorithmic Accountability Act. The defense industry utilizes AI technologies extensively for surveillance, threat identification, and strategic decision-making. With a growing emphasis on explainable AI (XAI), model version control, and bias detection algorithms, AI governance principles such as human-in-the-loop systems, model interpretability techniques, and model validation methods are increasingly crucial.

AI compliance audits, security protocols, and accountability mechanisms are also essential components of effective AI governance. Approximately 45% of organizations reported improved decision-making processes following the implementation of AI governance frameworks.

The Government and defense segment was valued at USD 23801.40 thousand in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 29% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Artificial Intelligence (AI) Governance Market Demand is Rising in North America Request Free Sample

The market witnessed substantial growth in North America by 2024. Key market participants, including government organizations, technology corporations, and research institutions, are actively shaping AI governance rules and practices in this region. Notably, groups like OpenAI and the Partnership on AI are spearheading the creation of ethical standards and regulations. Research collaborations between academic institutions and industrial players are fueling innovation in AI governance.

For instance, the University of Florida's AI initiative, in partnership with NVIDIA, resulted in a powerful university-based AI supercomputing infrastructure and interdisciplinary programs fostering ethical AI research and application. This strategic alliance underscores the growing importance of ethical considerations and regulatory frameworks in the expanding AI landscape.

Customer Landscape of Artificial Intelligence (AI) Governance Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Artificial Intelligence (AI) Governance Market

Companies are implementing various strategies, such as strategic alliances, artificial intelligence (ai) governance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - The company leverages Amazon Web Services to deliver advanced AI governance solutions, ensuring ethical and compliant use of artificial intelligence technologies. Their offering caters to diverse industries, enabling effective management and mitigation of risks associated with AI implementation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Ataccama Corp.

- Dataiku Inc.

- DataRobot Inc.

- Fair Isaac Corp.

- Google LLC

- H2O.ai Inc.

- Informatica Inc.

- International Business Machines Corp.

- Meta Platforms Inc.

- Microsoft Corp.

- QlikTech international AB

- Salesforce Inc.

- SAP SE

- SAS Institute Inc.

- TIBCO Software Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Artificial Intelligence (AI) Governance Market

- In August 2024, IBM announced the launch of its new AI Governance Suite, designed to help businesses manage and secure their AI applications. The suite includes tools for explaining AI model decisions, monitoring AI usage, and enforcing compliance policies (IBM Press Release, 2024).

- In November 2024, Microsoft and Google formed a strategic partnership to collaborate on AI ethics and governance. The two tech giants will work together to develop guidelines and best practices for responsible AI use (Microsoft Blog, 2024).

- In March 2025, Mastercard made a strategic investment of USD100 million in Element AI, a leading AI research lab. The investment will help Mastercard expand its AI capabilities and improve its fraud detection and risk management systems (Mastercard Press Release, 2025).

- In May 2025, the European Union passed the Artificial Intelligence Act, a landmark regulation that sets ethical standards for AI development and use. The Act includes provisions for transparency, accountability, and human oversight (EU Commission Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Artificial Intelligence (AI) Governance Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

227 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 64.6% |

|

Market growth 2025-2029 |

USD 3127734.9 thousand |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

44.6 |

|

Key countries |

US, China, UK, Brazil, Japan, Germany, France, Italy, India, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Artificial Intelligence (AI) Governance Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing robust growth as businesses increasingly integrate advanced AI systems into their operations. Effective AI governance is crucial to mitigate risks associated with AI system risk assessment methodologies, ensuring fairness and transparency in AI, and implementing data privacy controls. One significant challenge in AI governance is addressing algorithmic bias in AI systems. AI model validation and verification techniques, such as measuring algorithmic fairness and bias, play a vital role in identifying and mitigating bias. Developing AI governance frameworks for organizations is essential to managing these risks through effective governance. Another critical aspect of AI governance is improving system explainability and interpretability. AI model lifecycle management best practices and AI data governance and compliance strategies are essential to ensuring accountability and transparency mechanisms are in place. Building trust in AI systems through responsible development is crucial, as AI is increasingly being applied to business functions like supply chain and operational planning. Establishing ethical guidelines for AI development is essential to addressing challenges in AI governance implementation. Enhancing AI system security and resilience is another key consideration, with AI oversight and monitoring strategies playing a critical role in maintaining system performance and reliability. Compared to traditional technology governance, AI governance requires a more nuanced approach. For instance, AI model lifecycle management best practices involve continuous monitoring and updating to ensure ongoing compliance with ethical considerations and regulatory requirements. In contrast, traditional technology governance may focus more on initial implementation and periodic audits. In conclusion, the AI governance market is a critical enabler for responsible and effective use of AI technology. Organizations must establish robust AI compliance programs, promote ethical considerations in AI development, and implement effective AI system oversight and monitoring strategies to build trust and mitigate risks. By doing so, they can harness the power of AI to drive business growth and innovation while ensuring compliance with ethical and regulatory requirements.

What are the Key Data Covered in this Artificial Intelligence (AI) Governance Market Research and Growth Report?

-

What is the expected growth of the Artificial Intelligence (AI) Governance Market between 2025 and 2029?

-

USD 3127734.9 thousand, at a CAGR of 64.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Government and defense, Healthcare and life sciences, BFSI, Retail, and Others), Component (Solution and Services), Application (Model lifecycle management, Risk and compliance, Monitoring and auditing, and Ethics and responsible AI), Deployment (Cloud and On-premises), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing adoption of AI technologies across industries, Lack of universally accepted standards and frameworks for AI governance

-

-

Who are the major players in the Artificial Intelligence (AI) Governance Market?

-

Amazon.com Inc., Ataccama Corp., Dataiku Inc., DataRobot Inc., Fair Isaac Corp., Google LLC, H2O.ai Inc., Informatica Inc., International Business Machines Corp., Meta Platforms Inc., Microsoft Corp., QlikTech international AB, Salesforce Inc., SAP SE, SAS Institute Inc., and TIBCO Software Inc.

-

We can help! Our analysts can customize this artificial intelligence (ai) governance market research report to meet your requirements.

RIA -

RIA -