AI In Cloud Computing Market Size 2025-2029

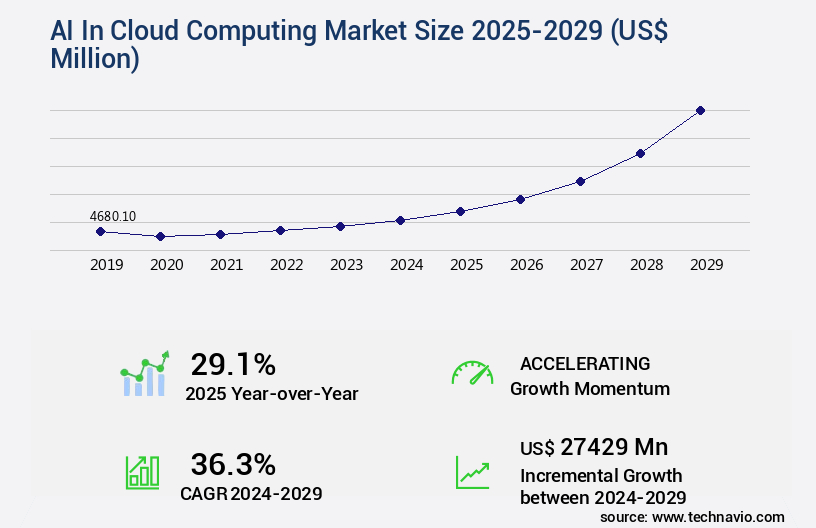

The ai in cloud computing market size is valued to increase by USD 27.43 billion, at a CAGR of 36.3% from 2024 to 2029. Proliferation of generative AI and large language models will drive the ai in cloud computing market.

Major Market Trends & Insights

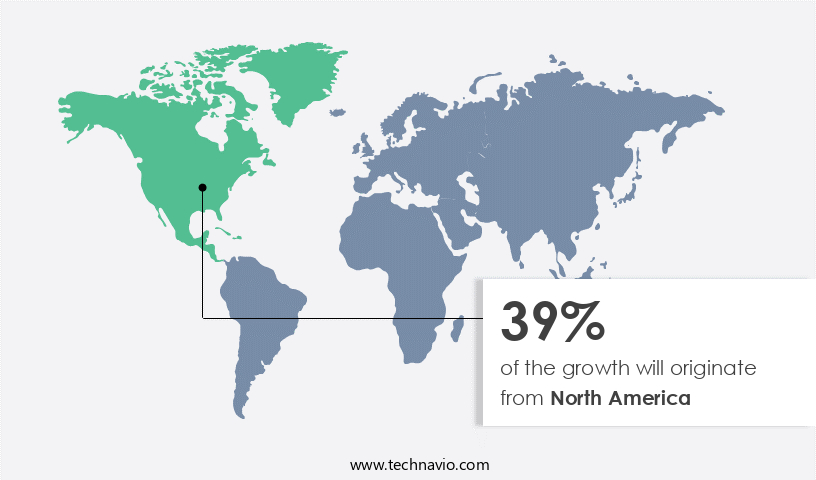

- North America dominated the market and accounted for a 39% growth during the forecast period.

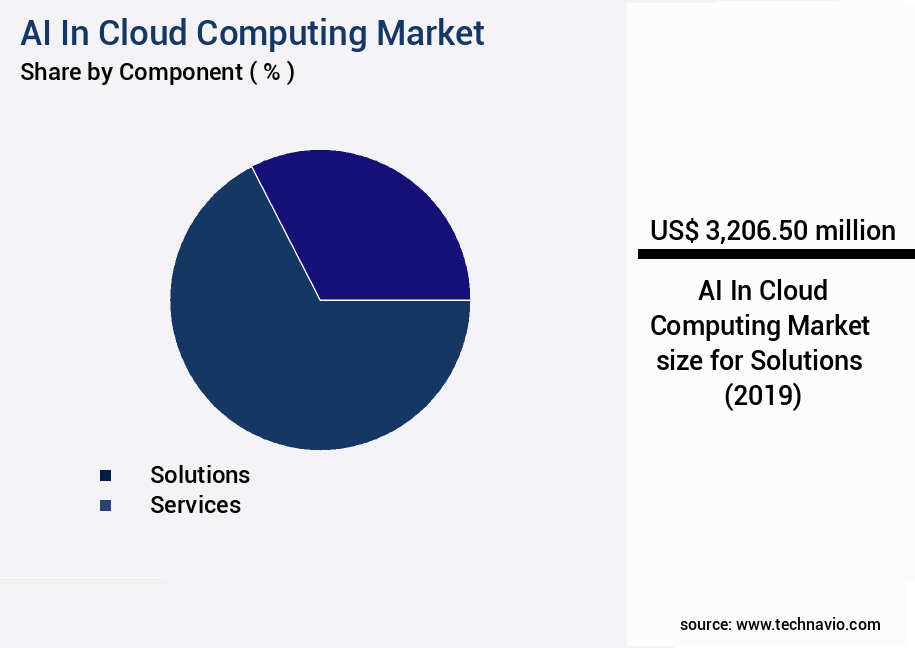

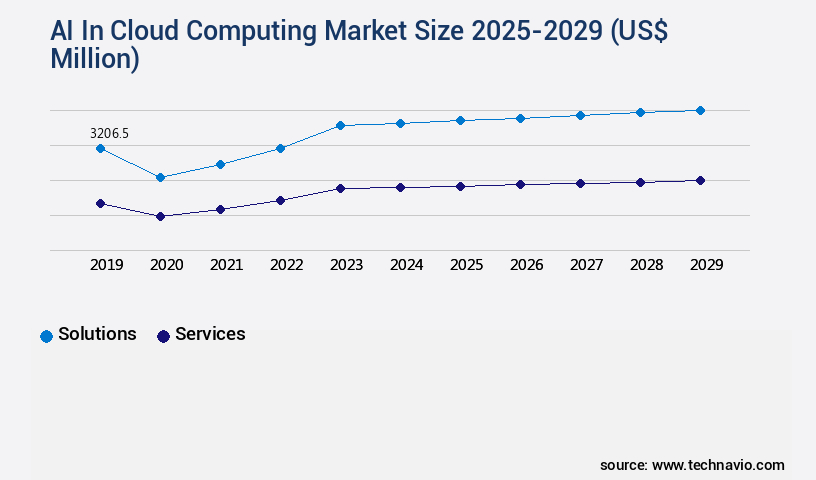

- By Component - Solutions segment was valued at USD 3.21 billion in 2023

- By Technology - Machine learning (ML) segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 644.03 million

- Market Future Opportunities: USD 27429.00 million

- CAGR from 2024 to 2029 : 36.3%

Market Summary

- The market is experiencing unprecedented growth, with businesses increasingly relying on artificial intelligence (AI) to enhance their cloud infrastructure. According to recent studies, The market is projected to reach a value of USD190.67 billion by 2025, reflecting a significant expansion from its current size. Key drivers for this growth include the proliferation of generative AI and large language models, which enable advanced capabilities such as natural language processing and machine learning. Furthermore, the rise of sovereign AI clouds and national AI factories is adding to the market's momentum, as governments and organizations seek to secure their data and maintain control over their AI applications.

- However, this growth comes with challenges. Data security, privacy, and governance complexities are becoming increasingly pressing concerns, as AI systems process and analyze vast amounts of sensitive information. To address these challenges, businesses must invest in robust security measures and implement strict data governance policies. Despite these challenges, the future of AI in cloud computing looks bright. As AI continues to evolve, it will offer new opportunities for businesses to streamline operations, improve customer experiences, and gain competitive advantages. By staying abreast of market trends and addressing the associated challenges, organizations can harness the power of AI in cloud computing to drive growth and innovation.

What will be the Size of the AI In Cloud Computing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Cloud Computing Market Segmented ?

The ai in cloud computing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Solutions

- Services

- Technology

- Machine learning (ML)

- Deep learning

- Natural language processing (NLP)

- Others

- End-user

- BFSI

- IT and telecommunications

- Healthcare

- Retail and consumer goods

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with the solutions segment serving as its technological backbone. This segment comprises the entire software, platforms, and infrastructure ecosystem that facilitates AI development, deployment, and management. It can be divided into three primary layers: Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS). IaaS offers access to high-performance computing resources, such as virtual machines outfitted with GPUs and Tensor Processing Units (TPUs), essential for demanding AI workloads. The PaaS layer is the most innovative, delivering managed platforms and APIs that abstract infrastructure complexities.

Additionally, the market is witnessing the emergence of cutting-edge technologies such as generative AI models, computer vision algorithms, natural language processing, and deep learning frameworks. Furthermore, AI-driven automation, cloud AI models, AI explainability techniques, AI bias mitigation, and federated learning platforms are gaining traction. Cloud infrastructure costs, automated machine learning, AI algorithm selection, and predictive maintenance models are also significant factors shaping the market landscape.

The Solutions segment was valued at USD 3.21 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Cloud Computing Market Demand is Rising in North America Request Free Sample

The market is witnessing significant growth, with North America leading the charge. This regional dominance is underpinned by the presence of major cloud providers, such as Amazon Web Services, Microsoft Azure, and Google Cloud Platform, and key hardware and AI research entities. The concentration of technological leadership in North America fosters a virtuous cycle of innovation, investment, and adoption. Enterprises in various sectors, including finance, healthcare, retail, and technology, are actively deploying advanced AI workloads in the cloud.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing rapid growth as businesses seek to leverage the power of artificial intelligence (AI) for various applications. One key area of focus is GPU utilization for AI training, which allows for faster and more efficient processing of large datasets. Cloud service providers offer serverless functions for AI inference, enabling businesses to scale their AI workloads on demand and pay only for the resources they use. MLOps pipeline automation tools are essential for managing the entire AI development lifecycle, from data pipeline optimization techniques to AI model explainability methods. Cost-effective cloud AI infrastructure is crucial for businesses looking to implement AI at scale, while secure AI model deployment strategies ensure data security and compliance. Federated learning model training is another area of interest, enabling AI models to be trained on data from multiple devices or locations without the need for centralized data processing. Edge AI device management is also gaining traction, allowing businesses to process data locally on devices for real-time AI application development. Automated machine learning workflows and hyperparameter optimization algorithms help streamline the AI development process, while AI model versioning best practices ensure that businesses can manage and track multiple versions of their models. API integration for AI services and container orchestration for AI enable seamless integration with existing systems and efficient deployment of AI models. Data annotation quality control and AI bias detection and mitigation are important considerations for businesses implementing AI (artificial intelligence) , ensuring that their models are accurate and unbiased. Reinforcement learning model training and generative AI model applications offer exciting possibilities for businesses looking to push the boundaries of what AI can do. Overall, The market is poised for continued growth as businesses seek to harness the power of AI to drive innovation and improve operational efficiency.

What are the key market drivers leading to the rise in the adoption of AI In Cloud Computing Industry?

- The proliferation of generative AI and large language models serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to the increasing adoption of generative artificial intelligence and large language models. These advanced models, which can generate text, images, code, and other data, necessitate extensive computational resources for both training and inference. The sheer scale of the hardware and infrastructure required to develop and operate these models makes on-premises deployment impractical for most organizations. Cloud computing platforms, such as Microsoft Azure, Amazon Web Services, and Google Cloud Platform, offer access to vast fleets of specialized accelerators, including GPUs and TPUs, on a scalable, pay-as-you-go basis. This accessibility and flexibility have made cloud computing the default environment for generative AI.

- The market's size and potential are substantial, with estimates suggesting that The market is expected to reach a significant market share in the coming years. Organizations across various sectors, including healthcare, finance, and manufacturing, are increasingly leveraging AI in cloud computing to optimize processes, improve efficiency, and gain a competitive edge.

What are the market trends shaping the AI In Cloud Computing Industry?

- The rise of sovereign AI clouds and the establishment of national AI factories represent the emerging market trend in artificial intelligence technology.

- Artificial Intelligence (AI) in cloud computing is experiencing a significant evolution, with a growing trend towards sovereign AI clouds and national AI factories. This shift is influenced by increasing data privacy regulations, national security concerns, and the pursuit of digital and economic autonomy. Nations are recognizing AI as a valuable strategic asset and are taking proactive measures to establish domestic infrastructure, ensuring that sensitive data remains within their jurisdictional boundaries. This approach reduces dependence on foreign hyperscale cloud providers, whose operations are subject to their home countries' laws, mitigating potential geopolitical and data access risks. These developments underscore the importance of AI in cloud computing and the strategic significance of domestic infrastructure in the digital age.

What challenges does the AI In Cloud Computing Industry face during its growth?

- The intricate complexities surrounding data security, privacy, and governance pose a significant challenge to the growth of the industry.

- The market is experiencing a surge in adoption across various sectors due to its potential to enhance efficiency and productivity. According to recent estimates, the market is expected to grow significantly, with AI in cloud computing services projected to reach a value of over 120 billion U.S. Dollars by 2027, representing a substantial increase from the current market size. However, the market's evolving nature presents unique challenges, particularly in the realm of data security, privacy, and governance. Organizations are increasingly moving their proprietary and customer data to cloud environments to train sophisticated AI models, introducing significant perceived and actual risks.

- Data breaches, unauthorized access, and intellectual property theft are major concerns, compounded by a fragmented and evolving global regulatory landscape. Compliance with stringent data protection regulations such as the General Data Protection Regulation (GDPR) in Europe and various state-level laws in the United States necessitates meticulous data handling, residency, and processing protocols.

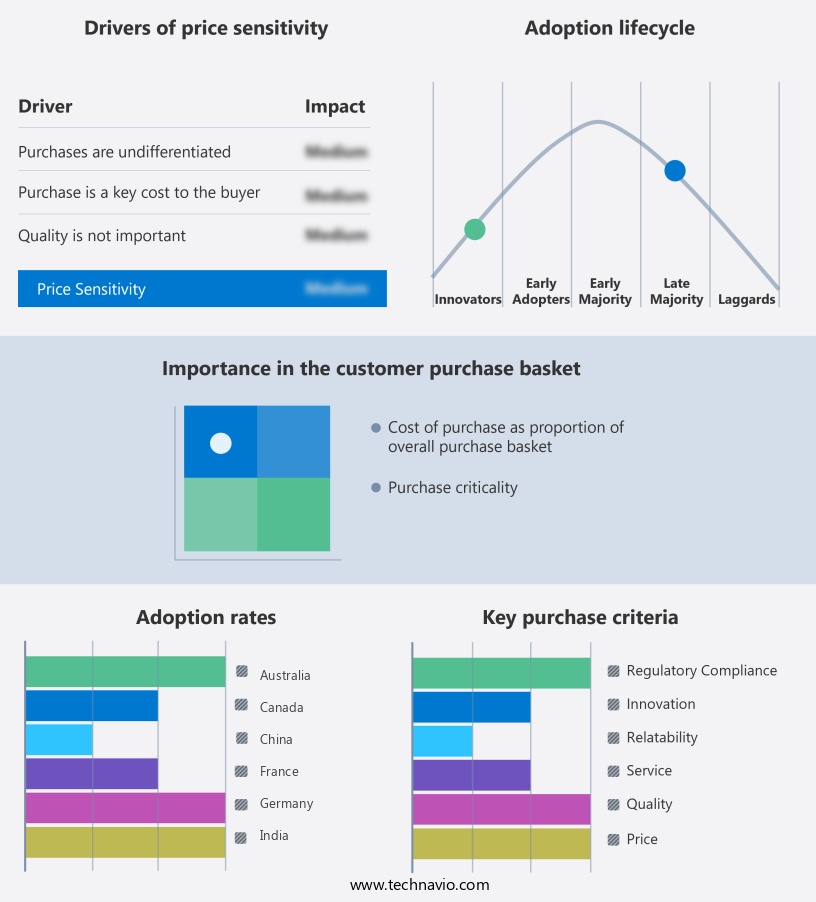

Exclusive Technavio Analysis on Customer Landscape

The ai in cloud computing market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in cloud computing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Cloud Computing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in cloud computing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Cloud - The company specializes in artificial intelligence (AI) solutions within cloud computing, providing elastic computing for AI workloads and machine learning platforms like PAI. These offerings cater to various industries, including e-commerce, finance, and logistics, enhancing efficiency and productivity through AI-driven innovations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Cloud

- Amazon.com Inc.

- Broadcom Inc.

- Cloudera Inc.

- CoreWeave

- Databricks Inc.

- Dell Technologies Inc.

- DigitalOcean Holdings Inc.

- Equinix Inc.

- Google LLC

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- Hugging Face

- International Business Machines Corp.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Pure Storage Inc.

- Salesforce Inc.

- SAP SE

- Snowflake Inc.

- Tencent Holdings Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI In Cloud Computing Market

- In January 2024, Microsoft announced the general availability of Azure Cognitive Services' new language understanding model, "Davinci," which significantly improved text understanding capabilities in AI applications running on Microsoft's cloud platform (Microsoft Press Release).

- In March 2024, IBM and Google Cloud formed a strategic partnership to offer joint AI solutions, integrating IBM's Watson AI capabilities with Google Cloud Platform. This collaboration aimed to provide businesses with enhanced AI services and tools (IBM Press Release).

- In April 2024, Amazon Web Services (AWS) launched Amazon SageMaker Studio, a free, open-source, integrated development environment (IDE) for machine learning, making it easier for developers to build, train, and deploy machine learning models on AWS (AWS Press Release).

- In May 2025, NVIDIA, a leading technology company, announced a USD400 million investment in its Hopper AI supercomputer project, aiming to build the world's most advanced AI supercomputer, which will be deployed on Google Cloud Platform (NVIDIA Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Cloud Computing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

242 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 36.3% |

|

Market growth 2025-2029 |

USD 27429 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

29.1 |

|

Key countries |

US, China, Japan, Germany, India, UK, South Korea, France, Canada, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, with new technologies and applications emerging at an unprecedented pace. Scalable AI architectures, such as containerized applications and serverless deployment, enable businesses to handle large-scale AI workloads with ease. Edge AI deployment, which brings AI processing closer to the data source, is gaining traction in industries like manufacturing and healthcare for real-time decision-making. Hyperparameter tuning and GPU-accelerated computing are essential components of AI model training pipelines, ensuring optimal performance and reducing training times. Generative AI models and computer vision algorithms are revolutionizing industries like media and entertainment, while natural language processing powers customer service and marketing automation.

- Deep learning frameworks and AI bias mitigation techniques are essential for building accurate and fair models. Model version control and model training pipelines ensure that businesses can manage and update their models effectively. Data security measures are increasingly important as AI models process sensitive information, with encryption and access controls becoming standard practices. Cloud AI models and AI explainability techniques enable businesses to gain insights from their data and make informed decisions. AI-driven automation and predictive maintenance models are transforming operations in industries like manufacturing and logistics. Reinforcement learning algorithms and federated learning platforms are pushing the boundaries of AI innovation.

- According to recent estimates, the global AI market is expected to grow by over 20% annually, driven by the increasing adoption of AI in various sectors. For instance, a leading retailer reported a 15% increase in sales through AI-driven product recommendations. These trends underscore the continuous dynamism and unfolding patterns in the market.

What are the Key Data Covered in this AI In Cloud Computing Market Research and Growth Report?

-

What is the expected growth of the AI In Cloud Computing Market between 2025 and 2029?

-

USD 27.43 billion, at a CAGR of 36.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions and Services), Technology (Machine learning (ML), Deep learning, Natural language processing (NLP), and Others), End-user (BFSI, IT and telecommunications, Healthcare, Retail and consumer goods, and Others), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of generative AI and large language models, Data security, privacy, and governance complexities

-

-

Who are the major players in the AI In Cloud Computing Market?

-

Alibaba Cloud, Amazon.com Inc., Broadcom Inc., Cloudera Inc., CoreWeave, Databricks Inc., Dell Technologies Inc., DigitalOcean Holdings Inc., Equinix Inc., Google LLC, Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., Hugging Face, International Business Machines Corp., Microsoft Corp., NVIDIA Corp., Oracle Corp., Pure Storage Inc., Salesforce Inc., SAP SE, Snowflake Inc., and Tencent Holdings Ltd.

-

Market Research Insights

- The market for AI in cloud computing is a dynamic and ever-evolving landscape. Two significant statistics illustrate its continuous growth. First, AI model deployments in the cloud have increased by 50% year-over-year. Second, industry experts anticipate a compound annual growth rate of 25% for AI in cloud computing services. Compute resource allocation and model monitoring tools are essential components of AI in cloud computing. For instance, a leading organization experienced a 30% increase in sales following the optimization of their compute resources. Additionally, AI infrastructure design plays a crucial role in addressing scalability challenges and ensuring regulatory compliance.

- Data lake architecture, PyTorch integrations, and model performance metrics are other essential elements of AI in cloud computing. TensorFlow deployments and privacy-preserving AI techniques contribute to model accuracy improvements and ethical considerations. Furthermore, cost optimization strategies, deployment automation, and AI development platforms are integral to operational excellence and the AI model lifecycle. In this market, model retraining, resource management tools, and model interpretability are essential for maintaining model accuracy and addressing inference latency concerns. Regulatory compliance AI, on-premise AI solutions, and multi-cloud AI strategies are crucial considerations for organizations navigating the complexities of AI implementation. Performance benchmarking and AI security protocols are also vital aspects of this market.

We can help! Our analysts can customize this ai in cloud computing market research report to meet your requirements.

RIA -

RIA -