AI In Mergers And Acquisitions Market Size 2025-2029

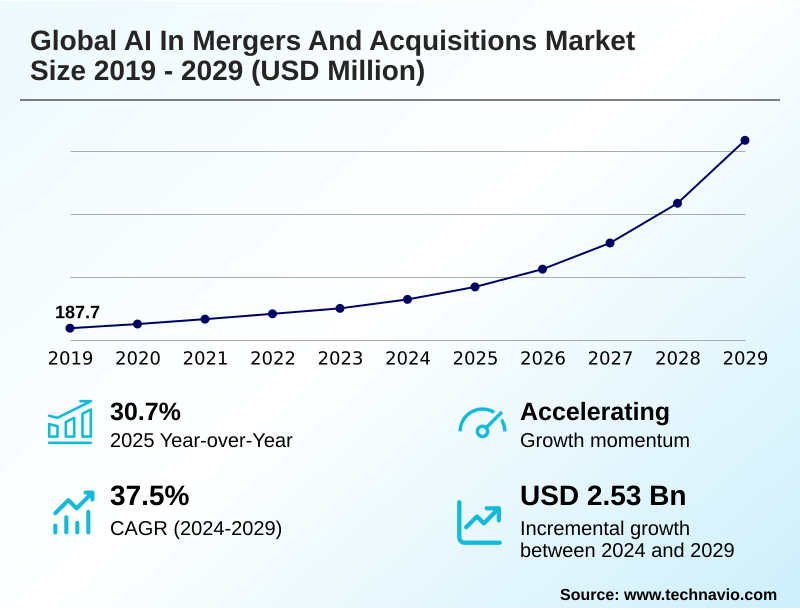

The ai in mergers and acquisitions market size is valued to increase by USD 2.53 billion, at a CAGR of 37.5% from 2024 to 2029. Enhanced due diligence efficiency and accuracy will drive the ai in mergers and acquisitions market.

Major Market Trends & Insights

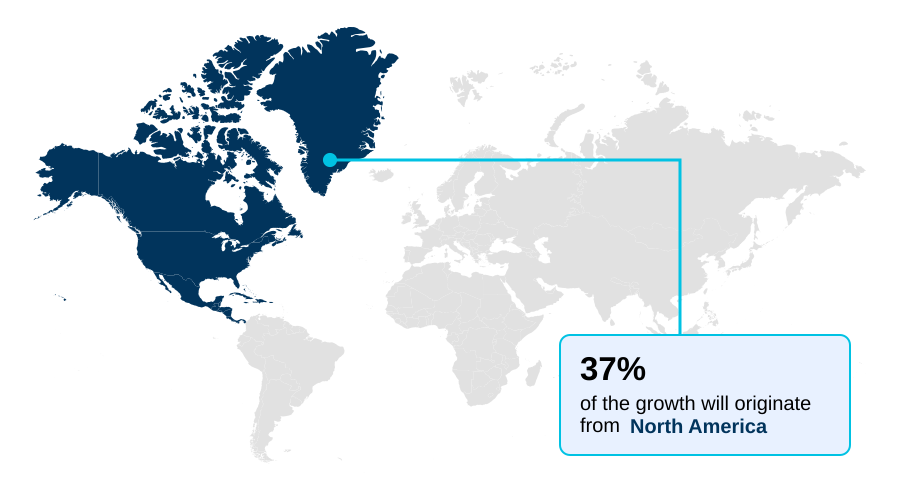

- North America dominated the market and accounted for a 37.3% growth during the forecast period.

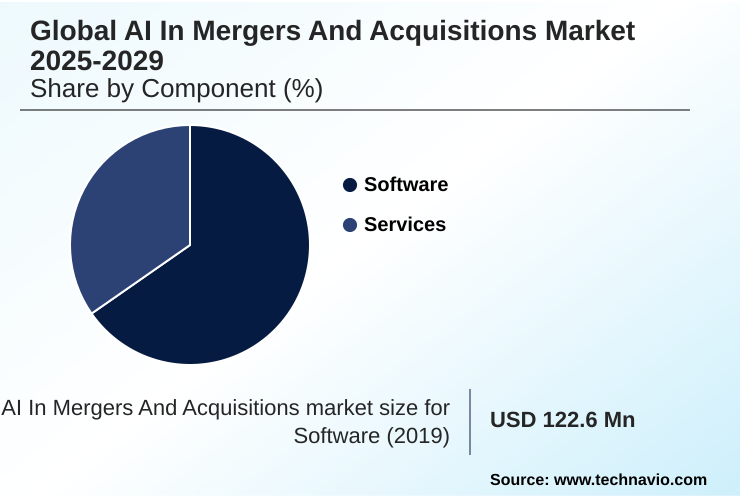

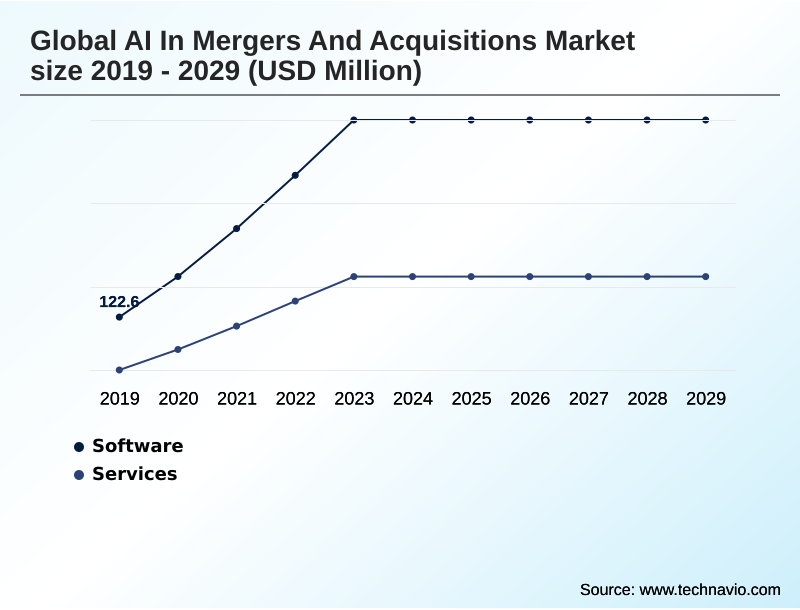

- By Component - Software segment was valued at USD 336.8 million in 2023

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.99 billion

- Market Future Opportunities: USD 2.53 billion

- CAGR from 2024 to 2029 : 37.5%

Market Summary

- The AI in mergers and acquisitions market is undergoing a significant transformation, driven by technologies that enhance every phase of the deal lifecycle. Key market drivers include the need for enhanced due diligence efficiency and improved target identification. The integration of generative AI modeling is a primary trend, enabling firms to automate complex analyses and streamline workflows.

- However, the market faces challenges related to data privacy, the high cost of implementation, and a notable talent gap in specialized expertise. For instance, a financial institution can leverage AI-powered due diligence platforms to analyze thousands of contracts for risk in a fraction of the time, a scenario where AI's speed and accuracy provide a distinct competitive advantage.

- This shift toward data-driven decision-making is reshaping strategic imperatives, pushing firms to adopt advanced analytical tools to stay competitive in a complex dealmaking environment. The technology is not just an ancillary tool but is becoming a core component of corporate strategy.

What will be the Size of the AI In Mergers And Acquisitions Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Mergers And Acquisitions Market Segmented?

The ai in mergers and acquisitions industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Services

- Deployment

- Cloud-based

- On-premises

- End-user

- BFSI

- Healthcare

- Consumer and retail

- Manufacturing

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is the core engine of the AI in mergers and acquisitions market, providing the platforms that enable deal lifecycle automation.

These solutions facilitate a more efficient mergers and acquisitions workflow through AI-driven workflow automation and automated document categorization. An AI-powered market intelligence platform is crucial for data-driven valuation and intellectual property analysis.

Firms are adopting these tools to achieve operational synergy identification and streamline the creation of documents like the confidential information memorandum.

With AI-powered forecasting tools, which an estimated 80% of practitioners expect to use, these platforms are transforming the transaction management solution landscape. The use of an AI-powered VDR is central to this shift, underpinning the entire data monetization strategy.

The Software segment was valued at USD 336.8 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Mergers And Acquisitions Market Demand is Rising in North America Get Free Sample

The geographic landscape of the AI in mergers and acquisitions market is led by North America, where targets accounted for 61% of all global M&A value, making it a key digital transformation catalyst.

Firms in this region aggressively use AI for post-merger integration planning and synergy realization tracking. In Europe, the focus is on regulatory compliance navigation, with companies leveraging AI-powered background checks and AI-driven deal sourcing to navigate complex legal frameworks.

The APAC region is also a high-growth area, where AI facilitates cross-border transaction analysis and sentiment analysis to overcome cultural and language barriers. Across all regions, IT systems integration is a critical application.

The adoption of operational excellence tools and AI for portfolio management is becoming a global standard, with firms using AI-enhanced document structuring to improve efficiency, underscoring a worldwide shift in dealmaking strategy.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The AI in mergers and acquisitions market is experiencing accelerated adoption, with a notable year-over-year growth rate exceeding 30%. This expansion is fueled by the strategic need to enhance corporate finance decisions. The role of AI in private equity deal sourcing is becoming particularly prominent, as firms seek a competitive advantage.

- There is a growing reliance on using generative AI for due diligence reporting, which significantly streamlines the analysis phase. A key application is leveraging AI for cultural integration analysis, which helps mitigate post-deal risks. Furthermore, AI platforms for post-merger synergy tracking are critical for ensuring value creation.

- Firms are increasingly using predictive analytics for off-market deal sourcing, uncovering opportunities that traditional methods miss. The impact of AI on deal negotiation strategy is substantial, as data-driven insights provide stronger bargaining positions. A core technical application involves natural language processing for contract review, which is more accurate than manual methods.

- The use of AI tools for intellectual property valuation is transforming how technology assets are assessed. Within M&A, automating compliance checks with AI is now standard practice, as is the use of AI for supply chain synergy modeling. AI applications in cross-border M&A are essential for navigating diverse legal systems.

- The adoption of machine learning for predicting deal success provides a quantitative basis for strategic choices. Organizations also utilize an AI-driven platform for target screening and for identifying revenue enhancement synergies, which automates KYC and AML in M&A. This is complemented by generative AI for creating deal marketing materials and real-time market intelligence using AI.

- The implementation of AI models for dynamic company valuation is another critical development shaping the industry.

What are the key market drivers leading to the rise in the adoption of AI In Mergers And Acquisitions Industry?

- Enhanced efficiency and accuracy in due diligence processes stand out as a key driver for market growth.

- The primary market driver is the significant efficiency gained through AI-powered due diligence, which can accelerate transaction timelines by up to 50%. Technologies like natural language processing are used for automated contract review, providing actionable risk insights with high precision.

- Deal sourcing automation, powered by algorithmic target screening and private market intelligence, is another key driver, allowing firms to uncover off-market opportunities. Predictive valuation models are delivering more accurate and defensible valuations.

- AI-powered advisory services are leveraging these tools to enhance deal marketing automation and real-time deal monitoring. To ensure security, robust data room security protocols are essential.

- The focus on AI model explainability is also growing, as dealmakers require transparency behind the analytical outputs that inform their high-stakes decisions.

What are the market trends shaping the AI In Mergers And Acquisitions Industry?

- The ascendancy of generative AI in mergers and acquisitions processes is a dominant market trend. This technology is increasingly being integrated across the entire deal lifecycle, from sourcing to post-merger integration.

- A dominant trend is the integration of generative AI modeling and AI-native platform intelligence across the deal lifecycle. This strategic acquisition driver is pushing firms toward data-driven dealmaking, where predictive deal sourcing identifies potential acquisition targets that conventional methods miss.

- Adoption rates are climbing, with 80% of practitioners expecting to use these technologies for tasks like dynamic valuation modeling and AI-driven strategic simulation. In Europe, approximately 42% of firms are now leveraging AI, with a focus on cross-border transaction analysis and legal tech integration. The technology also supports cultural alignment analysis, which is critical for post-merger success.

- The ability to generate proprietary deal flow using AI-powered market intelligence is creating a distinct competitive advantage for early adopters.

What challenges does the AI In Mergers And Acquisitions Industry face during its growth?

- Significant concerns regarding data privacy and security present a key challenge affecting industry growth.

- Significant challenges hinder widespread adoption, led by data security and compliance risk assessment. The total cost of ownership for AI solutions can be three to five times the initial software cost, creating a high barrier to entry.

- There is also a critical need for AI talent upskilling, as the demand for specialists with M&A domain expertise has increased by over 60%. Establishing effective AI governance frameworks and ensuring algorithmic bias mitigation require significant investment. For due diligence, virtual data room analytics must be complemented by human-in-the-loop oversight.

- Key technical challenges include implementing robust data validation techniques and anomaly detection algorithms for automated risk assessment. Furthermore, managing financial crime intelligence with tools for AI-based KYC verification, automated AML screening, and real-time risk screening adds another layer of complexity.

Exclusive Technavio Analysis on Customer Landscape

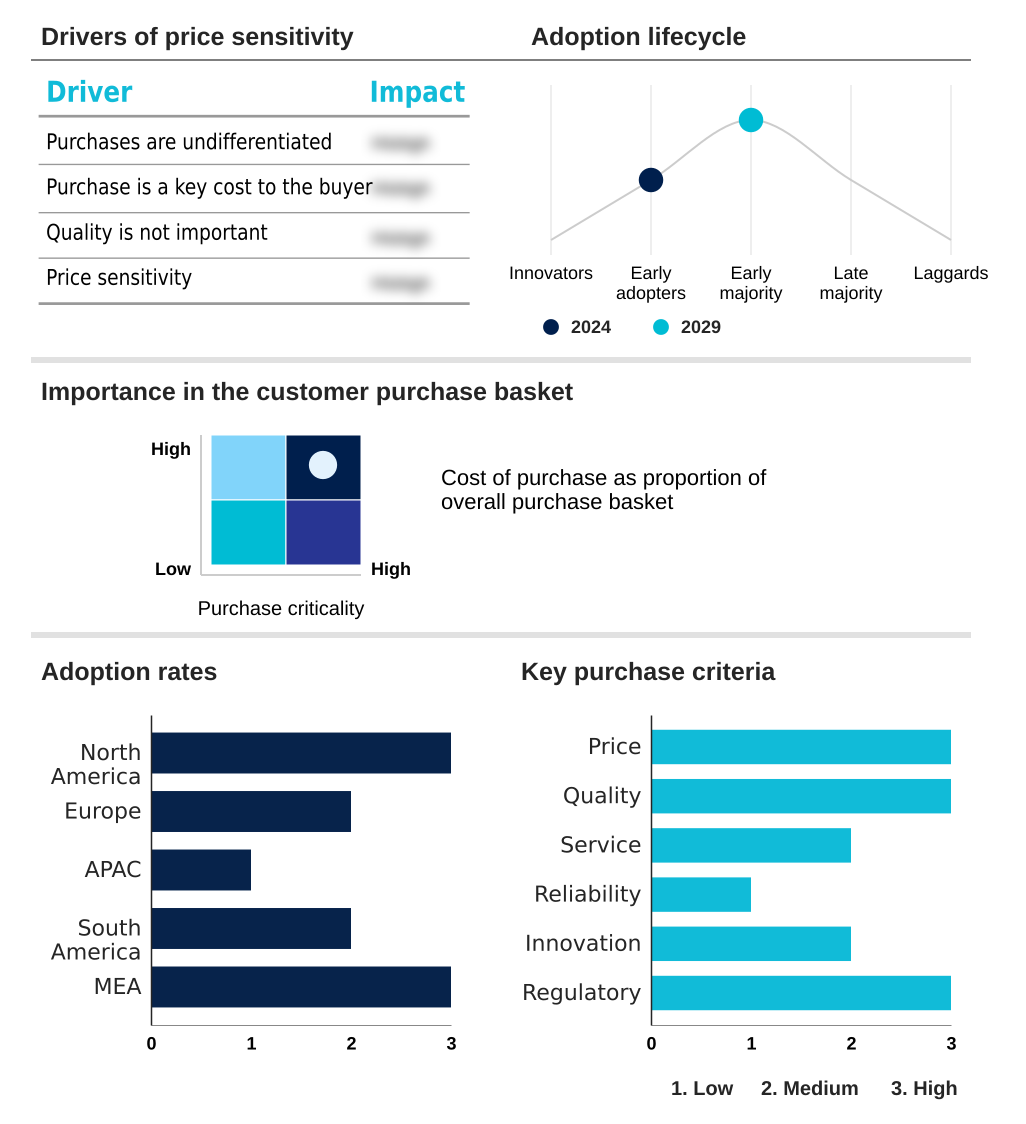

The ai in mergers and acquisitions market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in mergers and acquisitions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Mergers And Acquisitions Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in mergers and acquisitions market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ansarada Group Ltd. - Offerings include AI-powered virtual data rooms and advanced workflow tools, which streamline due diligence and end-to-end M&A execution for enhanced transactional efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ansarada Group Ltd.

- Apollo Asset Management Inc.

- Avantis AI Inc.

- Biteno GmbH

- ComplyAdvantage

- datasite LLC

- Dealsuite

- Digital Insight Technologies Ltd.

- Drooms GmbH

- Grata Inc.

- Inven.ai

- LexisNexis Legal and Professional

- PitchBook Data Inc.

- S and P Global Inc.

- Signzy Technologies and Services Inc.

- Slipstream Technologies Ltd.

- Sourcescrub

- ZoomInfo Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in mergers and acquisitions market

- In June 2024, OpenAI acquired Rockset, a real-time analytics database company, to enhance its retrieval infrastructure for processing vast amounts of data for its models.

- In May 2024, ComplyAdvantage announced a partnership with Greenlite AI to introduce AI agents to the alert management and remediation process, aiming to enhance the efficiency of financial crime compliance.

- In April 2024, IBM completed its acquisition of HashiCorp for USD 6.4 billion to deepen its AI-powered cloud automation capabilities.

- In March 2024, Microsoft made a strategic deal to hire most of the staff from Inflection AI and license its models, integrating the talent and technology to enhance its product offerings.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Mergers And Acquisitions Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 37.5% |

| Market growth 2025-2029 | USD 2531.1 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 30.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, China, Japan, India, Australia, South Korea, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in mergers and acquisitions market is defined by a strategic shift towards data-centric decision-making. The adoption of AI-powered due diligence and generative AI modeling is becoming standard practice, enabling firms to achieve a 40% improvement in risk detection accuracy. The use of natural language processing for automated contract review is central to this efficiency gain.

- Deal sourcing automation and algorithmic target screening allow for more proactive strategies, supported by predictive valuation models and data-driven valuation techniques. In the post-deal phase, AI supports post-merger integration planning, real-time synergy tracking, and cultural alignment analysis. An AI-powered VDR with virtual data room analytics and automated document categorization streamlines the entire process.

- Key applications include intellectual property analysis, AI-powered market intelligence, and predictive deal sourcing. For compliance, tools for compliance risk assessment, automated risk assessment, AI-based KYC verification, automated AML screening, financial crime intelligence, and ai-driven financial crime management are crucial. The adoption of AI-driven workflow automation and an AI-native platform intelligence is reshaping workflows.

- Other applications include dynamic valuation modeling, operational synergy identification, IT systems integration, AI-powered background checks, and regulatory compliance navigation, making AI an indispensable asset in modern corporate finance.

What are the Key Data Covered in this AI In Mergers And Acquisitions Market Research and Growth Report?

-

What is the expected growth of the AI In Mergers And Acquisitions Market between 2025 and 2029?

-

USD 2.53 billion, at a CAGR of 37.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), Deployment (Cloud-based, and On-premises), End-user (BFSI, Healthcare, Consumer and retail, Manufacturing, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Enhanced due diligence efficiency and accuracy, Data privacy and security concerns

-

-

Who are the major players in the AI In Mergers And Acquisitions Market?

-

Ansarada Group Ltd., Apollo Asset Management Inc., Avantis AI Inc., Biteno GmbH, ComplyAdvantage, datasite LLC, Dealsuite, Digital Insight Technologies Ltd., Drooms GmbH, Grata Inc., Inven.ai, LexisNexis Legal and Professional, PitchBook Data Inc., S and P Global Inc., Signzy Technologies and Services Inc., Slipstream Technologies Ltd., Sourcescrub and ZoomInfo Technologies Inc.

-

Market Research Insights

- The market is shaped by the need for comprehensive deal lifecycle automation, redefining the traditional mergers and acquisitions workflow. A key strategic acquisition driver is the pursuit of proprietary deal flow generation, supported by AI-powered advisory services and forecasting tools. This data-driven dealmaking approach relies on secure data room security protocols and effective data monetization strategy.

- As a digital transformation catalyst, AI is central to legal tech integration and the automated onboarding process. Firms leverage these tools for operational excellence and advanced AI for portfolio management. The market's evolution is also marked by a focus on AI model explainability and robust algorithmic bias mitigation.

- Enhanced data validation techniques and anomaly detection algorithms are critical, requiring human-in-the-loop oversight and strong AI governance frameworks to manage risks. These dynamics are compelling a focus on AI talent upskilling to manage this technological shift.

We can help! Our analysts can customize this ai in mergers and acquisitions market research report to meet your requirements.

RIA -

RIA -