AI In Real Estate And Construction Market Size 2025-2029

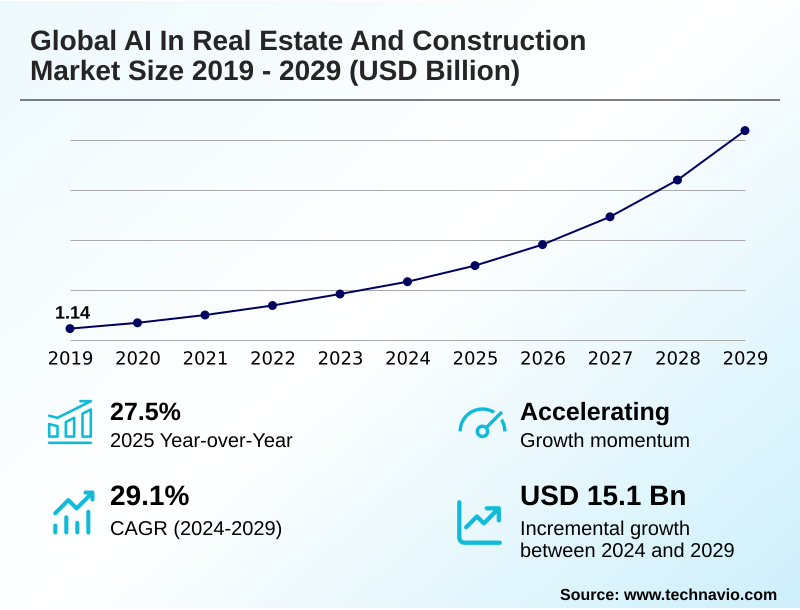

The ai in real estate and construction market size is valued to increase by USD 15.10 billion, at a CAGR of 29.1% from 2024 to 2029. Imperative for enhanced productivity and operational efficiency will drive the ai in real estate and construction market.

Major Market Trends & Insights

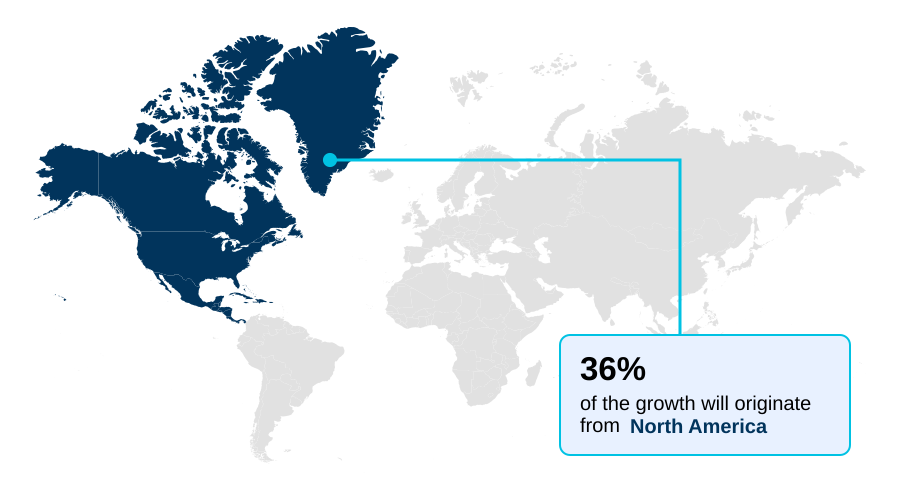

- North America dominated the market and accounted for a 36.1% growth during the forecast period.

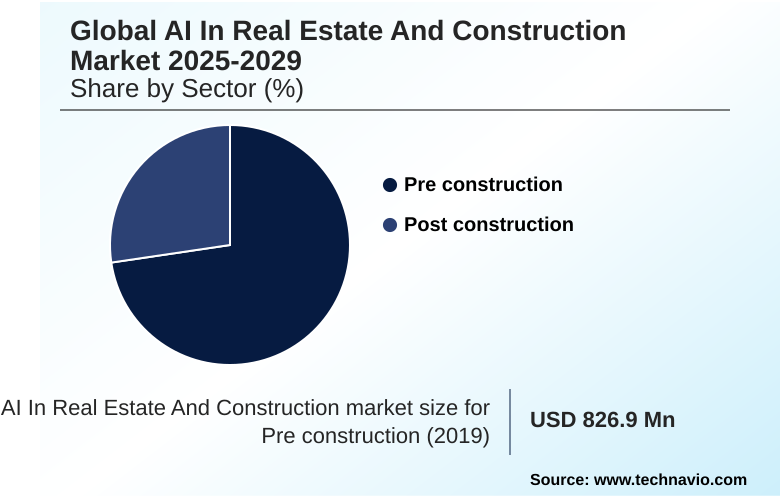

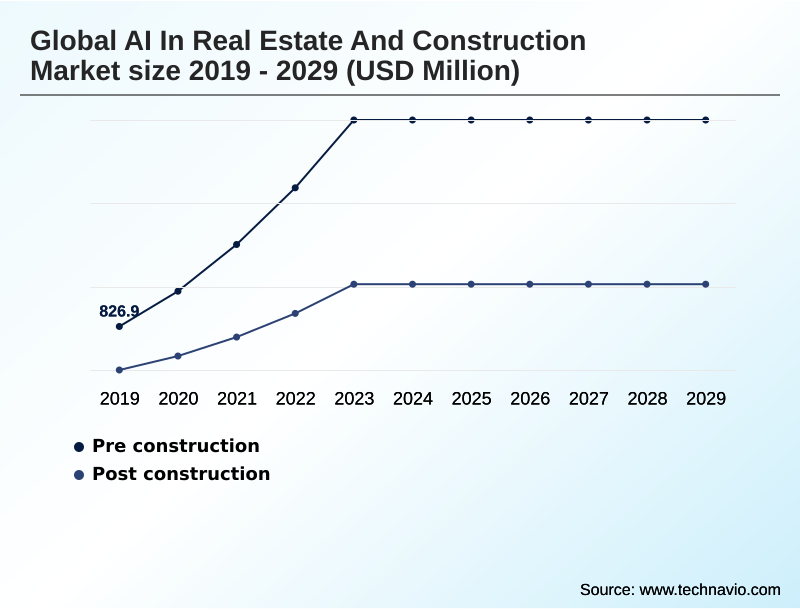

- By Sector - Pre construction segment was valued at USD 3.27 billion in 2023

- By Organization Size - Large enterprises segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 19.80 billion

- Market Future Opportunities: USD 15.10 billion

- CAGR from 2024 to 2029 : 29.1%

Market Summary

- The AI in real estate and construction market is defined by the deployment of intelligent technologies to address long-standing industry inefficiencies. This shift is driven by the need for enhanced productivity, the proliferation of data from sources like building information modeling (BIM), and increasing pressure for ESG compliance.

- Key trends include the rise of generative design, where algorithms create optimized architectural plans, and the adoption of digital twin ecosystems for lifecycle asset management. AI-native platforms are central to this transformation, offering tools for predictive analytics and construction site automation.

- For example, a major contractor can leverage an AI-driven project management platform using predictive maintenance algorithms to analyze real-time sensor data from heavy equipment, forecasting potential failures and scheduling maintenance during planned downtime. This proactive approach, which relies on point cloud data analysis and machine learning, minimizes costly on-site breakdowns and project delays.

- However, challenges such as unstructured data extraction and the need for significant upfront investment without immediate ROI persist, tempering the pace of widespread adoption of technologies like AI-powered robotics.

What will be the Size of the AI In Real Estate And Construction Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Real Estate And Construction Market Segmented?

The ai in real estate and construction industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Sector

- Pre construction

- Post construction

- Organization size

- Large enterprises

- SMEs

- Technology

- ML and DL

- NLP

- Generative AI

- Computer vision

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Sector Insights

The pre construction segment is estimated to witness significant growth during the forecast period.

The global AI in real estate and construction market 2025-2029 is segmented by sector, organization size, technology, and geography. The pre-construction phase, a critical segment, is being reshaped by AI-powered robotics.

Here, generative design and construction sequencing simulation are paramount, allowing firms to explore thousands of optimized architectural plans.

This proactive risk mitigation is enhanced by predictive cost estimation and automated quantity takeoffs, where machine learning models analyze historical data to forecast expenses with high accuracy.

For instance, AI-driven cost models have shown to improve bidding accuracy by over 15%.

This data-driven decision making helps in construction logistics planning and resource allocation modeling, transforming how projects are conceived and de-risked before any physical work begins, ensuring greater budget certainty and competitive-edge in capital project planning.

The Pre construction segment was valued at USD 3.27 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Real Estate And Construction Market Demand is Rising in North America Get Free Sample

The geographic landscape of the AI in real estate and construction market is characterized by varied adoption rates and regional priorities.

North America leads, accounting for over 36% of incremental growth, driven by high labor costs and a mature technology ecosystem focused on predictive analytics. Europe emphasizes sustainability, using AI for ESG compliance reporting and to meet stringent green building standards.

The APAC region is the fastest-growing, with massive smart city initiatives and government mandates fueling the deployment of AI-powered robotics and smart building management. For instance, AI-driven progress tracking has improved schedule adherence by 25% on large infrastructure projects.

This global expansion highlights a shift towards AI-native platforms and construction site automation, with applications like automated valuation models becoming standard in developed real estate markets and reality capture technologies being deployed worldwide to create digital twins.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic evaluation of AI's role in the built environment increasingly centers on specific use cases and measurable outcomes. Stakeholders are assessing the impact of AI on construction project timelines, where automated progress tracking using drone imagery provides real-time visibility that is significantly more accurate than manual reporting.

- In the design phase, the focus is on comparing generative design software for architectural planning, which can produce thousands of optimized iterations. Concurrently, the benefits of digital twins in facility management are becoming clear, especially when integrated with AI-powered predictive maintenance for heavy equipment, which reduces costly downtime.

- On-site, computer vision for construction safety monitoring is a critical application, while the role of robotics in automating construction tasks addresses labor shortages. For investors, the ROI of AI in real estate asset management is paramount, with tools for AI-driven real estate investment analysis becoming indispensable.

- Firms are leveraging natural language processing for contract analysis to mitigate legal risks and using AI to optimize building energy consumption. The future of autonomous construction vehicles and how AI improves construction supply chain logistics are key topics, alongside AI applications for property valuation accuracy.

- Addressing the challenges of AI implementation in construction remains crucial for maximizing these benefits across the asset lifecycle. The move towards automating ESG reporting with AI platforms further underscores the technology's transformative potential.

What are the key market drivers leading to the rise in the adoption of AI In Real Estate And Construction Industry?

- The imperative for enhanced productivity and operational efficiency across the real estate and construction sectors serves as a primary driver for market growth.

- Market growth is primarily driven by the urgent need for operational efficiency and the increasing availability of high-quality data.

- The imperative to overcome stagnant productivity fuels the adoption of AI-driven project management tools, which use predictive cost estimation and resource allocation modeling to improve outcomes. Firms utilizing these systems report up to a 20% improvement in budget adherence.

- The proliferation of data from building information modeling (BIM), IoT sensors, and drone survey data analytics creates the necessary foundation for sophisticated machine learning. Furthermore, mounting pressure for enhanced ESG compliance reporting and site safety compliance is a significant catalyst.

- AI-powered computer vision for on-site safety monitoring and energy consumption optimization systems help firms meet regulatory demands while also reducing operational costs by over 15%.

What are the market trends shaping the AI In Real Estate And Construction Industry?

- A defining market trend is the rapid ascendancy of generative artificial intelligence and hyper-automation. This marks a significant evolutionary leap from predictive AI to creative and synthetic AI capabilities.

- Key market trends are centered on the rapid advancement from predictive to synthetic AI capabilities, fundamentally altering project design and management. The rise of generative design and construction sequencing simulation allows firms to explore thousands of optimized project plans, accelerating conceptual phases by over 45%.

- This is complemented by a strategic shift towards integrated digital twin ecosystems, which serve as a single source of truth for asset lifecycle management. These platforms leverage AI for real-time progress tracking and proactive risk mitigation. Simultaneously, the proliferation of AI-powered robotics and construction site automation is addressing labor shortages and enhancing safety.

- Robotic systems for tasks like welding and bricklaying have shown a 3x improvement in speed over manual methods, reshaping on-site operations and driving operational efficiency gains.

What challenges does the AI In Real Estate And Construction Industry face during its growth?

- Pervasive issues related to data fragmentation and poor data quality present a key challenge affecting industry growth.

- Significant challenges hinder widespread AI adoption, primarily revolving around data, cost, and culture. The industry's notoriously fragmented data landscape, filled with unstructured formats, creates a major hurdle; data scientists report spending over 70% of their time on data cleansing rather than model development. This issue of unstructured data extraction complicates the use of predictive analytics.

- The substantial upfront investment required for AI-native platforms and autonomous construction equipment, coupled with an often ambiguous immediate ROI, deters many firms, especially SMEs. A profound cultural inertia and a critical shortage of skilled talent, with salary demands for AI specialists increasing by nearly 25% in recent years, further constrain the market.

- Overcoming these barriers is essential for unlocking the full potential of technologies like natural language processing and computer vision.

Exclusive Technavio Analysis on Customer Landscape

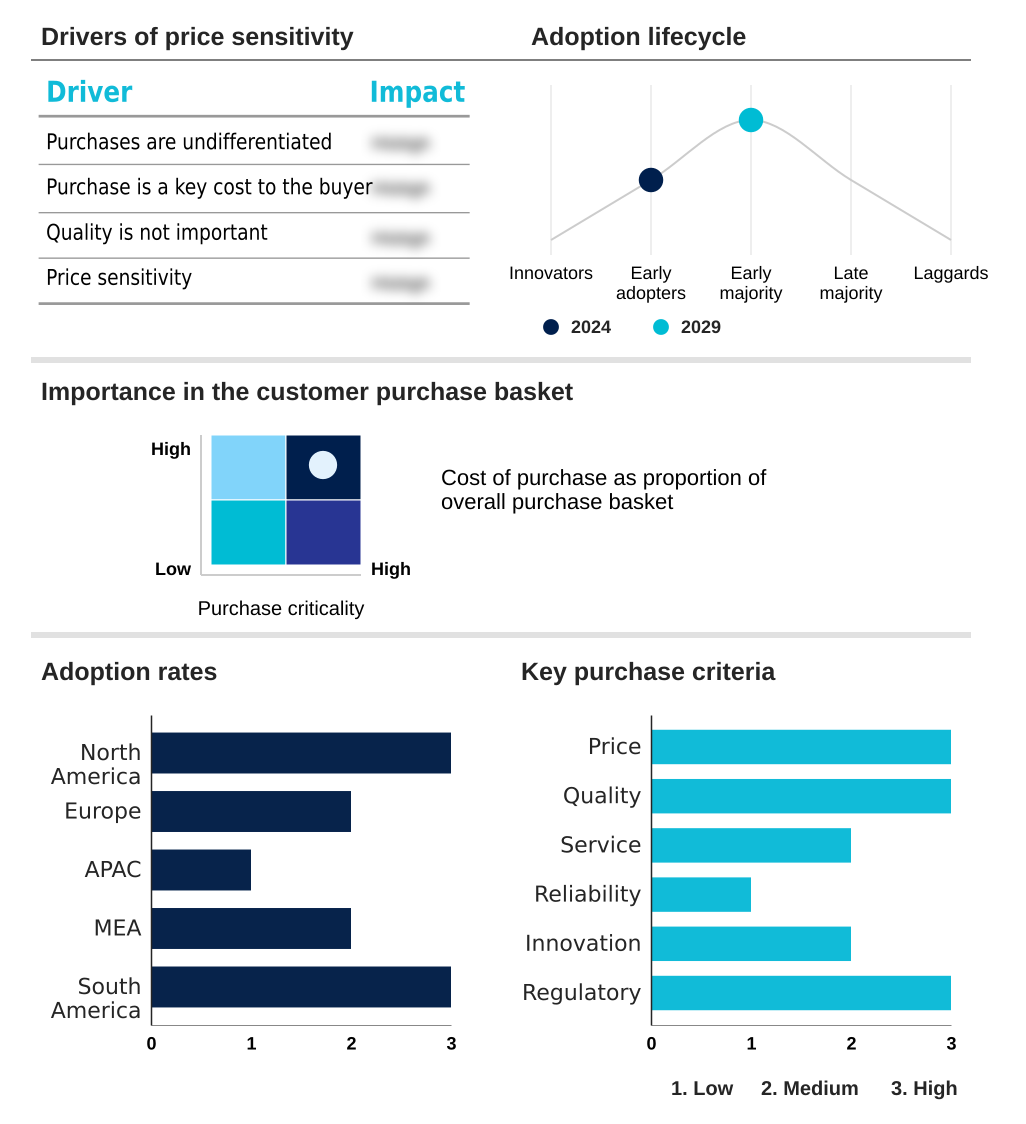

The ai in real estate and construction market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in real estate and construction market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Real Estate And Construction Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in real estate and construction market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acciona SA - Key offerings focus on integrated platforms that embed AI for predictive analytics, risk mitigation, and automated workflow intelligence across the entire asset lifecycle.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acciona SA

- AECOM

- AirWorks Solutions Inc.

- Autodesk Inc.

- Bentley Systems Inc.

- Buildots Ltd

- Dusty Robotics

- Elise A.I. Technologies Corp.

- Kwant

- Laing O Rourke

- Larsen and Toubro Ltd.

- Magicbricks Realty Services Limited.

- Matterport Inc.

- Obayashi Corp.

- Procore Technologies Inc.

- Shimizu Corp.

- Skanska AB

- Trimble Inc.

- Vinci

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in real estate and construction market

- In September 2024, Arcol launched its AI-native building design and documentation platform, incorporating generative AI at its core to automate repetitive design tasks and offer intelligent suggestions for architects.

- In November 2024, Buildots, an AI construction management company, announced a significant expansion of its operations in the United States, deploying its computer vision platform to provide fully digitized progress tracking on American construction sites.

- In January 2025, Trimble Inc. introduced new AI-powered tools for its Construction One platform, designed to automatically analyze site data from reality capture technologies to track and validate work progress, enhancing project oversight.

- In April 2025, BrainBox AI announced a strategic agreement with Trane Technologies to integrate its predictive and self-adapting artificial intelligence with Trane's commercial HVAC systems, aiming to embed autonomous AI for energy optimization in buildings.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Real Estate And Construction Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 29.1% |

| Market growth 2025-2029 | USD 15101.0 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 27.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in real estate and construction market is transitioning from niche applications to foundational technology, fundamentally re-engineering industry workflows. This evolution is defined by the integration of technologies like generative design, predictive analytics, and computer vision into cohesive, AI-native platforms.

- The development of digital twin ecosystems, powered by building information modeling and reality capture technologies, represents a critical boardroom-level strategic shift toward whole-lifecycle asset management. These dynamic virtual replicas enable sophisticated construction sequencing simulation and predictive maintenance algorithms, moving firms from reactive problem-solving to proactive optimization.

- For instance, the deployment of AI-powered robotics and autonomous construction equipment, guided by point cloud data analysis, is addressing chronic labor shortages. Implementations of on-site safety monitoring through computer vision have demonstrated a 40% reduction in protocol violations.

- The adoption of tools for unstructured data extraction and lease abstraction via natural language processing is automating back-office functions, solidifying AI's role as an indispensable tool for risk mitigation and operational excellence in both smart building management and construction site automation.

What are the Key Data Covered in this AI In Real Estate And Construction Market Research and Growth Report?

-

What is the expected growth of the AI In Real Estate And Construction Market between 2025 and 2029?

-

USD 15.10 billion, at a CAGR of 29.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Sector (Pre construction, and Post construction), Organization Size (Large enterprises, and SMEs), Technology (ML and DL, NLP, Generative AI, and Computer vision) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Imperative for enhanced productivity and operational efficiency, Pervasive issues of data fragmentation and quality

-

-

Who are the major players in the AI In Real Estate And Construction Market?

-

Acciona SA, AECOM, AirWorks Solutions Inc., Autodesk Inc., Bentley Systems Inc., Buildots Ltd, Dusty Robotics, Elise A.I. Technologies Corp., Kwant, Laing O Rourke, Larsen and Toubro Ltd., Magicbricks Realty Services Limited., Matterport Inc., Obayashi Corp., Procore Technologies Inc., Shimizu Corp., Skanska AB, Trimble Inc. and Vinci

-

Market Research Insights

- Market dynamics are shaped by the strategic adoption of AI to achieve measurable operational efficiency gains. The focus is on leveraging technologies for proactive risk mitigation and data-driven decision making, moving beyond reactive problem-solving. Implementations of automated defect detection systems have been shown to reduce rework costs by up to 30%, a critical factor in an industry with tight margins.

- Furthermore, intelligent building management platforms utilizing energy consumption optimization algorithms can lower utility expenses by as much as 18%. This tangible ROI fuels the demand for solutions that provide workforce productivity analytics and enhance site safety compliance.

- The ability to harness AI for subcontractor performance tracking and change order risk analysis is becoming a key competitive differentiator for firms aiming for superior project outcomes and improved profitability.

We can help! Our analysts can customize this ai in real estate and construction market research report to meet your requirements.

RIA -

RIA -