AI Builder Market Size 2025-2029

The AI builder market size is valued to increase USD 15.37 billion, at a CAGR of 34% from 2024 to 2029. Pressing need to democratize AI development amid persistent talent shortage will drive the ai builder market.

Major Market Trends & Insights

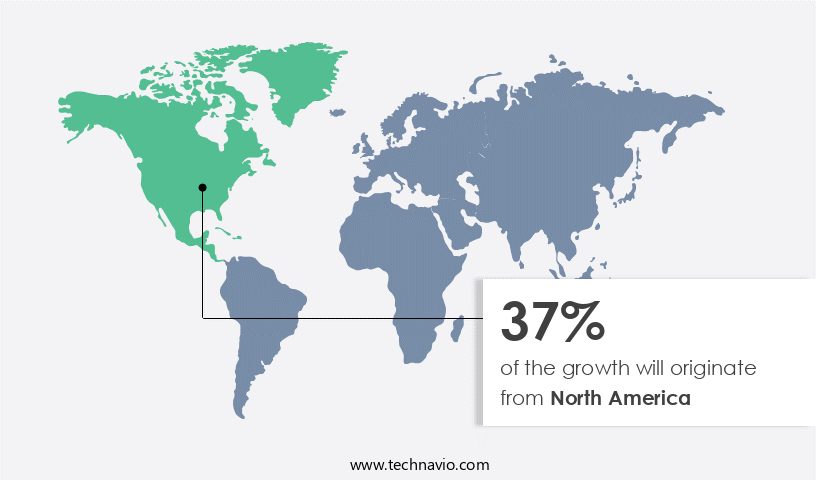

- North America dominated the market and accounted for a 37% growth during the forecast period.

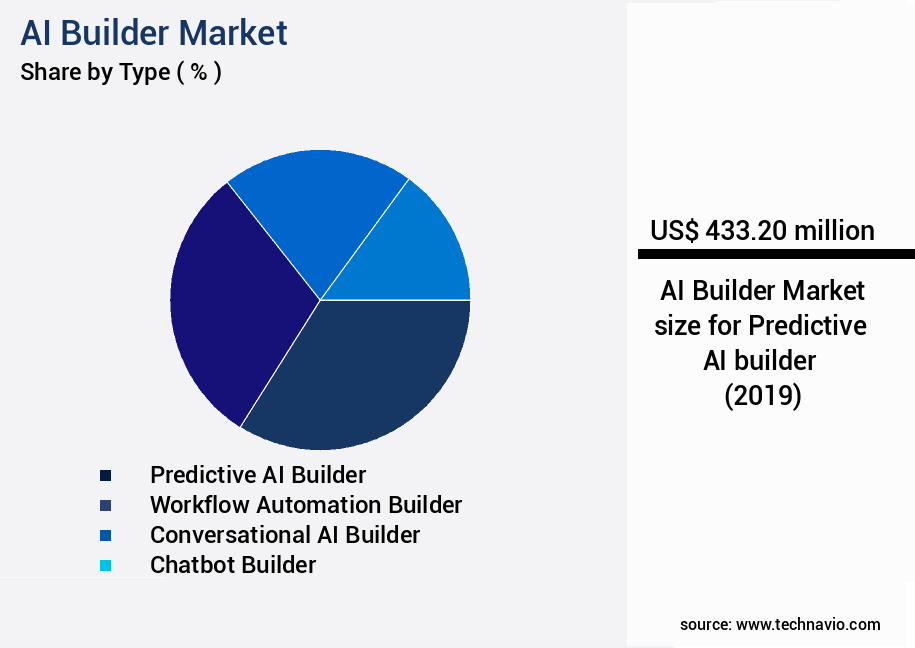

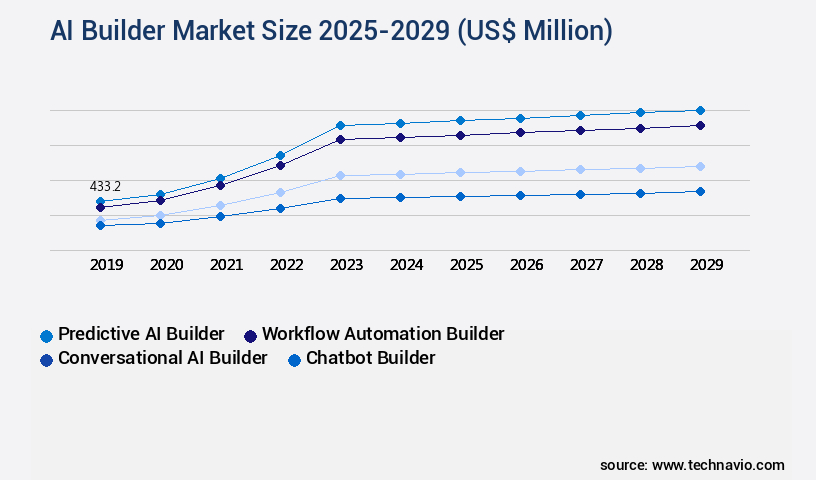

- By Type - Predictive AI builder segment was valued at USD 433.20 billion in 2023

- By Deployment - Cloud segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities: USD 15367.10 million

- CAGR from 2024 to 2029 : 34%

Market Summary

- In the realm of business technology, the market has emerged as a significant force, fueled by the pressing need to democratize AI development amidst a persistent talent shortage. This market is characterized by the strategic shift towards sovereign and open-source foundation models, which offer businesses greater flexibility and control over their AI applications. However, this transition is not without challenges. Navigating complex governance, risk, and compliance mandates requires a deep understanding of legal and ethical frameworks. According to recent estimates, the market is projected to reach a value of USD30.3 billion by 2026, growing at a steady pace. A recent study revealed that over 70% of companies implementing AI use predictive analytics, underscoring the market's growing importance.

- This growth is driven by the increasing adoption of AI solutions across industries, from healthcare to finance, and the recognition of their transformative potential. Despite this promising outlook, businesses must address the intricacies of integrating AI builders into their existing tech stacks and ensuring their ethical use. The future direction of the market lies in continued innovation and collaboration. As businesses seek to harness the power of AI to drive growth and improve operational efficiency, the demand for user-friendly, customizable, and secure AI development tools will only increase. This trend is expected to lead to further advancements in the market, making AI development more accessible and effective for businesses of all sizes.

What will be the Size of the AI Builder Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI Builder Market Segmented ?

The ai builder industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Predictive AI builder

- Workflow automation builder

- Conversational AI builder

- Chatbot builder

- Others

- Deployment

- Cloud

- On premises

- End-user

- BFSI

- IT and telecom

- Healthcare

- Retail

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The predictive ai builder segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with the predictive AI builder segment being a significant contributor. These platforms empower organizations to develop predictive models using historical data, democratizing machine learning for business analysts and citizen data scientists. The workflow entails uploading datasets, followed by automated tasks like data cleansing, feature engineering, algorithm selection, hyperparameter tuning, and model evaluation – collectively known as automated machine learning (AutoML). Applications span various industries, including customer churn prediction, sales forecasting, credit risk assessment, demand planning, and predictive maintenance. The market's ongoing activities involve advancements in transfer learning applications, model evaluation metrics, hybrid cloud solutions, reinforcement learning methods, neural network architectures, machine learning models, responsible AI practices, deep learning frameworks, natural language processing, data security measures, and accuracy and precision.

The Predictive AI builder segment was valued at USD 433.20 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Builder Market Demand is Rising in North America Request Free Sample

The market is witnessing significant evolution, with North America leading the charge as the most mature and dominant region. This regional dominance is driven by its status as a technological innovation hub and a favorable business environment. Notable players in North America include Amazon Web Services, Microsoft, and Google, whose cloud platforms serve as the foundation for the AI builder landscape. These companies have fueled market growth through continuous innovation and the integration of advanced AI into accessible, low-code platforms. For example, in late 2023, Microsoft introduced Azure AI Studio, an all-encompassing environment that consolidates tools and simplifies the development of custom copilots and generative AI applications.

The European market is anticipated to experience substantial growth, driven by increasing adoption of AI solutions in various industries and the presence of key players like IBM and SAP. The Asia Pacific region is also expected to witness significant growth due to the rising demand for AI-powered solutions in sectors such as healthcare, finance, and manufacturing.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as businesses seek to improve model accuracy through deep learning techniques. Implementing responsible AI practices is a critical aspect of this development, ensuring that machine learning pipelines are robust and deployment strategies are optimized. Enhancing model explainability is essential to build trust and transparency in AI systems, while leveraging transfer learning applications can streamline development processes. Effective data annotation techniques are crucial for creating high-performing models, and mitigating bias is a key challenge that must be addressed. Developing efficient data preprocessing steps and applying reinforcement learning methods can help improve model performance, while using unsupervised learning tasks for insights can uncover hidden patterns and trends. Cloud-based infrastructure is increasingly being used to deploy models, enabling scalability and flexibility. Building conversational AI chatbots and performing sentiment analysis on social media data are popular applications, while creating knowledge graphs for semantic search and using computer vision for image recognition are other areas of growth. Time series forecasting models and implementing anomaly detection algorithms are essential for predictive maintenance and fraud detection, respectively. Automating model training pipelines using CI/CD practices ensures consistency and speed, while monitoring model performance using evaluation metrics is crucial for continuous improvement. Overall, the market is dynamic and evolving, with a focus on improving model accuracy, implementing responsible AI practices, and leveraging advanced techniques such as deep learning and transfer learning. Companies that can effectively address these challenges and provide innovative solutions will be well-positioned for success.

What are the key market drivers leading to the rise in the adoption of AI Builder Industry?

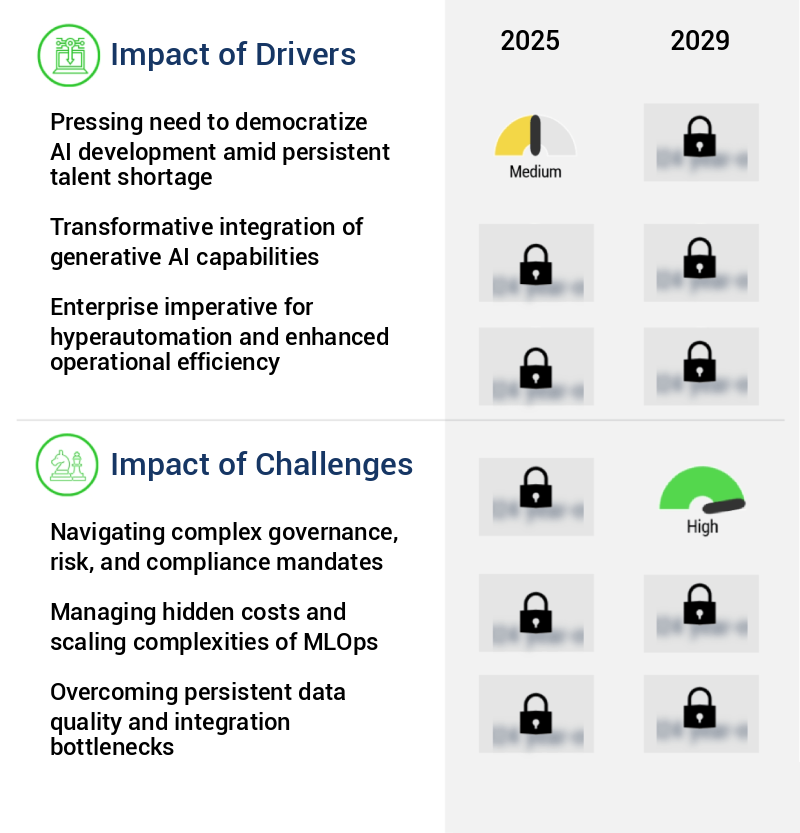

- The persistent talent shortage necessitates the urgent democratization of AI development, driving significant market growth.

- The market is experiencing a surge in demand due to the substantial gap between enterprise requirements for artificial intelligence (AI) solutions and the limited pool of highly specialized talent. The fields of data science and machine learning engineering necessitate profound expertise in statistics, programming, and intricate algorithms, resulting in a small workforce. This talent shortage acts as a significant barrier, hindering innovation and making AI projects financially burdensome for numerous organizations. AI builder platforms counteract this fundamental issue by democratizing access to sophisticated AI capabilities.

- Through user-friendly graphical user interfaces, automated machine learning (AutoML) features, and low-code or no-code settings, these platforms enable a new breed of creators - the citizen data scientists. This democratization of AI development is crucial for fostering innovation and driving growth in various sectors, including healthcare, finance, and manufacturing.

What are the market trends shaping the AI Builder Industry?

- The strategic shift toward sovereign and open-source foundation models is an emerging trend in the market. Open-source and sovereign models are increasingly preferred by organizations.

- The market is undergoing a transformative shift, with enterprises and governments moving away from proprietary, closed-source foundation models towards open-source and sovereign alternatives. This trend, driven by the need for greater control, transparency, cost-efficiency, and customization, has led to a surge in the development and adoption of powerful open-source large language models (LLMs). The release of Meta's Llama 2 for commercial use in July 2023 marked a significant milestone, offering a high-performance, freely available foundation for numerous new applications.

- This shift represents a strategic pivot that is redefining the AI landscape and expanding its reach across various sectors. The open-source movement in AI is expected to gain momentum, with more organizations embracing this approach to harness the potential of advanced language models and unlock new possibilities.

What challenges does the AI Builder Industry face during its growth?

- Navigating the intricate governance, risk, and compliance mandates is a significant challenge that can impact industry growth. Professionals must ensure adherence to these regulations to maintain business success and avoid potential penalties.

- The market is undergoing significant evolution, expanding its reach across various sectors. These platforms, which enable citizen data scientists to develop AI models without extensive technical expertise, have democratized AI development. However, they also introduce challenges, particularly in the realm of governance, risk, and compliance (GRC). With decentralized model creation, there is a risk of ungoverned or shadow AI models proliferating within organizations, leading to vulnerabilities concerning data privacy, security, and algorithmic bias. The crux of the issue lies in implementing centralized oversight without hindering the innovation and agility these builders aim to foster. Organizations must ensure that non-expert-built models adhere to ethical guidelines, transparency, and fairness.

- According to recent studies, the global AI market is projected to reach a value of USD309.6 billion by 2026, growing at a substantial pace. Another report suggests that the global AI in healthcare market is expected to grow at a compound annual growth rate (CAGR) of 41.5% between 2020 and 2027. These figures underscore the importance of addressing GRC challenges in the market.

Exclusive Technavio Analysis on Customer Landscape

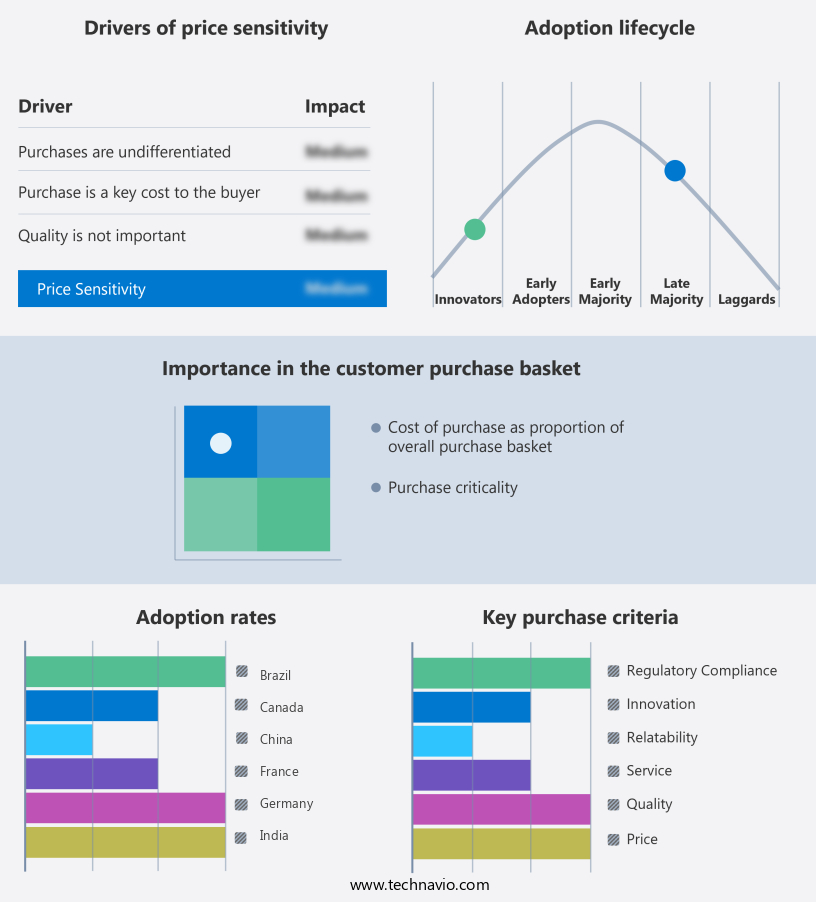

The ai builder market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai builder market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Builder Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai builder market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - This company specializes in artificial intelligence solutions, providing custom model development, generative AI consulting, and platform integration services for enterprise-wide transformation. Their expertise enables businesses to innovate and adapt through advanced AI technologies.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- Adobe Inc.

- Akkio Inc.

- Alibaba Cloud

- Altair Engineering Inc.

- Amazon Web Services Inc.

- Baidu Inc.

- C3.ai Inc.

- Dataiku Inc.

- DataRobot Inc.

- Google LLC

- H2O.ai Inc.

- International Business Machines Corp.

- Levity AI GmbH

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Tencent Holdings Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Builder Market

- In January 2024, Microsoft announced the general availability of Microsoft Power Apps AI Builder, enabling users without AI expertise to create custom AI models using a low-code platform (Microsoft Press Release). In March 2024, IBM and Google Cloud formed a partnership to integrate IBM Watson's AI capabilities into Google Cloud's AI Platform, enhancing Google's offerings and expanding IBM's reach (IBM Press Release). In April 2025, Amazon Web Services (AWS) secured a significant investment of USD2.5 billion in its AI and machine learning division, strengthening its position in the competitive AI market (Reuters). In May 2025, Apple announced the launch of Core ML 3, a major update to its machine learning framework, enabling developers to create custom machine learning models using Swift and improving model performance (Apple Developer).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Builder Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

246 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 34% |

|

Market growth 2025-2029 |

USD 15367.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

32.0 |

|

Key countries |

US, China, Germany, Japan, UK, Canada, France, India, South Korea, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, with new applications emerging across various sectors. Transfer learning applications, for instance, have gained significant traction due to their ability to leverage pre-trained models for specific tasks, resulting in faster development times and improved accuracy. Model evaluation metrics play a crucial role in assessing model performance, ensuring that unsupervised learning tasks deliver optimal results. Moreover, model versioning systems enable organizations to manage and track multiple model iterations, while ethical AI considerations remain a top priority as the industry matures. Hyperparameter optimization and API integration methods streamline development processes, making AI solutions more accessible.

- Hybrid cloud solutions and reinforcement learning methods are driving innovation in the market, with neural network architectures and deep learning frameworks powering advanced machine learning models. Responsible AI practices and privacy-preserving techniques are essential for maintaining trust and security. Automation workflows and interpretable machine learning are transforming industries, while on-premise deployment and model explainability techniques cater to organizations with unique data security requirements. Continuous deployment, model training pipelines, and data annotation techniques ensure ongoing improvement and adaptation. Computer vision algorithms and natural language processing are revolutionizing industries, with data preprocessing steps and feature engineering processes critical to achieving accurate and precise outcomes.

- Data security measures and model deployment strategies are essential components of successful AI implementations. According to recent industry reports, the AI market is expected to grow by over 20% annually, underscoring its transformative potential. For instance, a leading retailer reported a 15% increase in sales by implementing AI-powered pricing strategies. The continuous unfolding of market activities and evolving patterns underscore the importance of staying informed and adaptive.

What are the Key Data Covered in this AI Builder Market Research and Growth Report?

-

What is the expected growth of the AI Builder Market between 2025 and 2029?

-

USD 15.37 billion, at a CAGR of 34%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Predictive AI builder, Workflow automation builder, Conversational AI builder, Chatbot builder, and Others), Deployment (Cloud and On premises), End-user (BFSI, IT and telecom, Healthcare, Retail, and Others), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Pressing need to democratize AI development amid persistent talent shortage, Navigating complex governance, risk, and compliance mandates

-

-

Who are the major players in the AI Builder Market?

-

Accenture PLC, Adobe Inc., Akkio Inc., Alibaba Cloud, Altair Engineering Inc., Amazon Web Services Inc., Baidu Inc., C3.ai Inc., Dataiku Inc., DataRobot Inc., Google LLC, H2O.ai Inc., International Business Machines Corp., Levity AI GmbH, Microsoft Corp., NVIDIA Corp., Oracle Corp., Salesforce Inc., SAP SE, and Tencent Holdings Ltd.

-

Market Research Insights

- The market for AI builders continues to evolve, encompassing a range of applications including recommendation systems, relationship extraction, predictive maintenance, report generation, document classification, sentiment analysis, text summarization, model retraining, entity recognition, customer segmentation, image segmentation, time series forecasting, conversational AI, knowledge graph creation, model monitoring, model debugging, natural language generation, video analysis, prompt engineering, chatbot development, dashboard creation, fraud detection, model performance tuning, image recognition, anomaly detection, object detection, and semantic search. According to recent reports, the market for AI builders is anticipated to grow by over 20% annually, driven by increasing demand for automated business processes and advanced analytics.

- For instance, a leading retailer reported a 15% increase in sales after implementing an AI-powered recommendation system. This growth is expected to continue as businesses seek to leverage AI to gain insights from their data and improve operational efficiency.

We can help! Our analysts can customize this ai builder market research report to meet your requirements.

RIA -

RIA -