AI In Vision Market Size 2025-2029

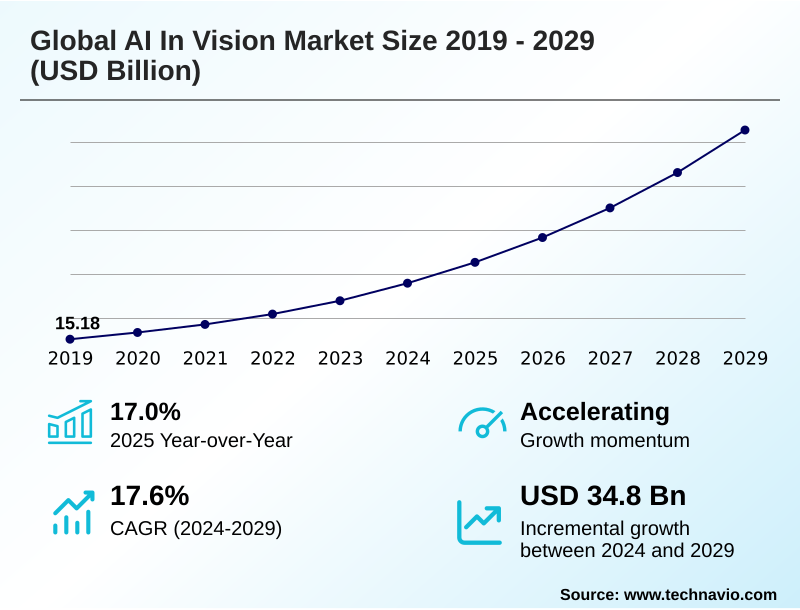

The ai in vision market size is valued to increase by USD 34.80 billion, at a CAGR of 17.6% from 2024 to 2029. Increasing demand for automation and Industry 4.0 integration will drive the ai in vision market.

Major Market Trends & Insights

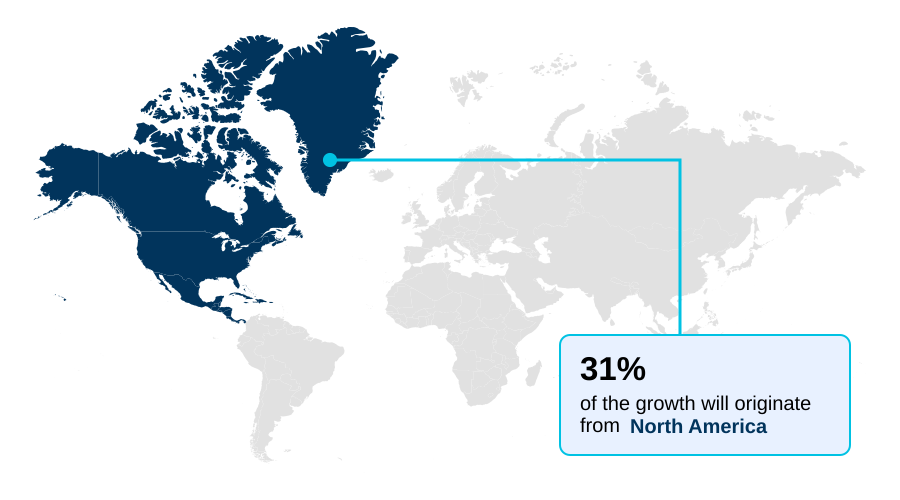

- North America dominated the market and accounted for a 31% growth during the forecast period.

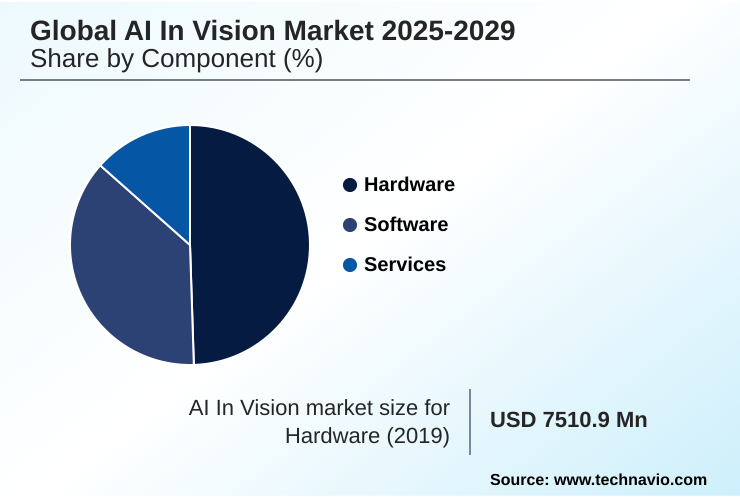

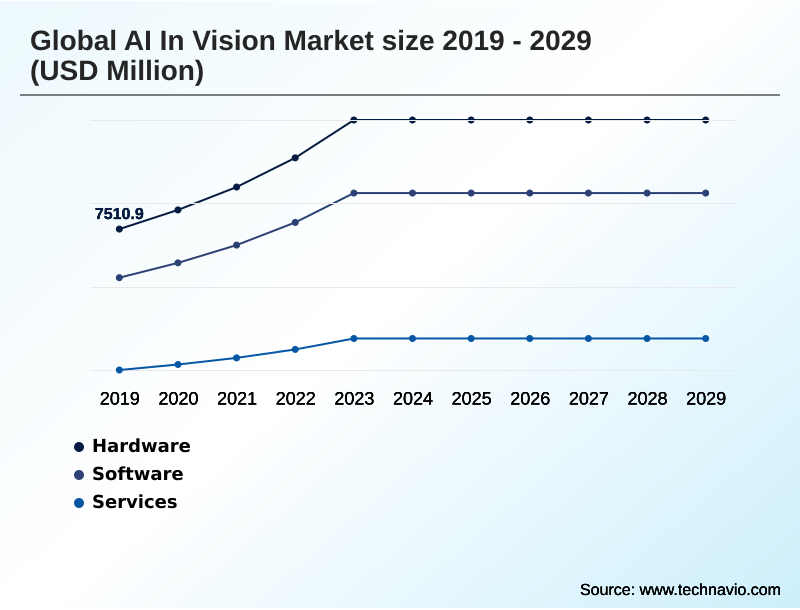

- By Component - Hardware segment was valued at USD 11.75 billion in 2023

- By Technology - Computer vision segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 47.54 billion

- Market Future Opportunities: USD 34.80 billion

- CAGR from 2024 to 2029 : 17.6%

Market Summary

- The AI in vision market is a transformative force enabling industries to derive actionable intelligence from visual data. At its core, the market is driven by the demand for automation in sectors like manufacturing, where automated quality control systems use deep learning models to identify microscopic defects with near-perfect accuracy, enhancing product quality and reducing waste.

- The synergistic evolution of sophisticated computer vision algorithms, from convolutional neural networks to advanced vision transformers, and powerful, specialized hardware like graphics processing units and neural processing units, underpins this expansion. This enables a broad spectrum of applications, from advanced driver-assistance systems enhancing vehicle safety to AI in medical imaging analysis that aids in early disease detection.

- However, the industry grapples with significant challenges, including the high cost of implementation, the need for vast, unbiased datasets, and navigating complex ethical and data privacy regulations. The rise of generative AI and on-device AI processing are key trends shaping the future, promising to lower barriers to entry and enable more responsive, secure, and context-aware applications across the board.

What will be the Size of the AI In Vision Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Vision Market Segmented?

The ai in vision industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Software

- Services

- Technology

- Computer vision

- Virtual reality

- Augmented reality

- Mixed reality

- End-user

- Manufacturing

- Healthcare and life sciences

- Automotive

- Retail and e-commerce

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment is the bedrock of the AI in vision market, comprising the specialized silicon that powers intensive machine learning tasks.

While graphics processing units remain essential for training large models, the primary growth catalyst is the proliferation of hardware for inference at the network periphery. This shift toward edge computing is crucial for applications demanding real-time responsiveness.

The development of systems on a chip that integrate dedicated neural processing units is accelerating this trend, enabling powerful on-device AI capabilities.

These custom application specific integrated circuits enable complex on-device AI processing, reducing response delays in driver monitoring systems and AR/VR with AI vision by over 60%.

This localized processing is essential for edge AI for low latency in safety-critical systems, AI for surgical robotics, and privacy-sensitive applications like facial recognition used in AI for public safety.

The Hardware segment was valued at USD 11.75 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 31% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Vision Market Demand is Rising in North America Get Free Sample

North America leads the AI in vision market, accounting for over 31% of incremental growth, driven by R&D in autonomous navigation systems and widespread adoption in healthcare and defense.

The region is a hub for spatial data analytics and digital twin technology.

In contrast, APAC is the fastest-growing market, propelled by smart city traffic management initiatives and a massive manufacturing base in China utilizing automated optical inspection for AI for supply chain optimization.

Europe’s market is distinguished by its strong industrial focus, with Germany’s Industry 4.0 strategy leveraging object detection and image classification for factory automation, improving production efficiency by 20%.

Applications like in-cabin monitoring in the automotive sector and image segmentation in medical diagnostics are key growth areas across mature regions, while emerging economies leverage the technology for AI in retail inventory management and even AI in sports analytics.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises evaluating the adoption of advanced visual intelligence must weigh the cost of implementing AI vision systems against the significant operational returns. The ROI of autonomous retail stores, for instance, is increasingly clear, with some early adopters reporting a twofold increase in checkout efficiency.

- A key architectural decision is the choice between edge AI vs cloud AI for video analytics; while cloud offers vast computational power, the need for real-time response is driving a definitive shift toward the edge, effectively reducing latency with edge AI vision in critical applications.

- Technologically, the evolution is rapid, and it is important to understand how vision transformers improve object detection over older architectures. The use of generative AI for synthetic training data is becoming a standard practice to mitigate the challenges of AI model bias in vision and reduce data acquisition costs.

- This is particularly relevant given the tightening regulatory landscape, where the impact of the EU AI act on vision market is forcing a greater focus on governance and transparency, especially concerning the ethical implications of facial recognition AI.

- From using AI vision for predictive maintenance in factories to deploying 3D digital twin for industrial inspection and computer vision in precision agriculture drones, the applications are expanding.

- Advances in on-device AI vision, powered by the role of NPUs in edge AI vision, are enabling new use cases in AI vision in autonomous driving safety and enhancing multimodal AI for customer experience.

What are the key market drivers leading to the rise in the adoption of AI In Vision Industry?

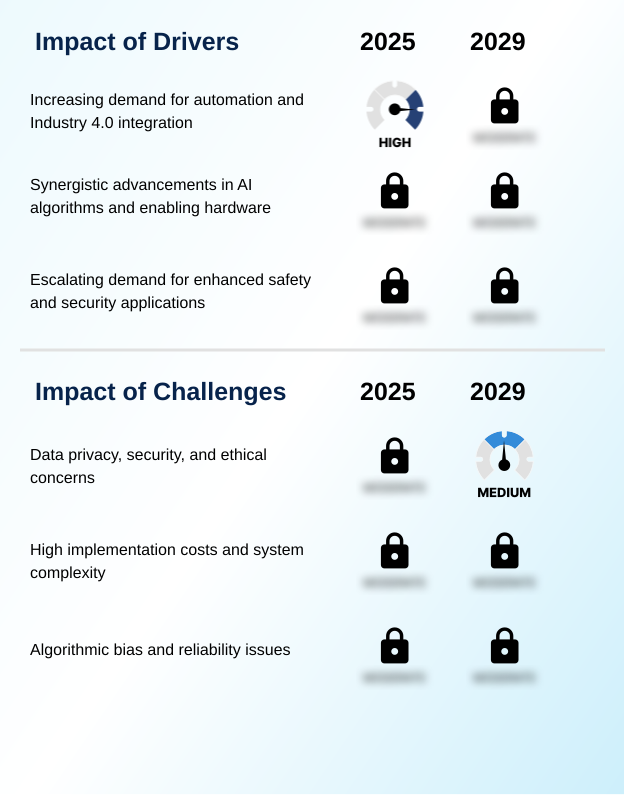

- The increasing demand for automation and deeper integration with Industry 4.0 initiatives serves as a key driver for the market.

- The pursuit of automation and operational efficiency through AI for industrial automation is a primary market driver.

- In smart factories, automated quality control systems powered by deep learning models identify defects with superhuman accuracy, with some deployments reducing error rates by over 95%.

- Vision-guided robotics are transforming manufacturing floors, enabling precise vision-guided robotic assembly and AI in logistics automation. The synergy between innovative computer vision algorithms for tasks like activity recognition and specialized hardware underpins this growth.

- The escalating demand for safety is another significant force, fueling the adoption of advanced driver-assistance systems and AI for predictive maintenance solutions.

- These systems use real-time object detection and analysis to prevent accidents and equipment failures, improving AI in quality control and operational uptime by more than 25%.

What are the market trends shaping the AI In Vision Industry?

- A significant market trend is the proliferation of generative AI within vision applications, expanding capabilities from data analysis to content creation.

- A key trend is the rapid integration of generative AI, which enables the creation of new visual content and addresses data scarcity through synthetic data generation for AI. Models like vision transformers and multimodal foundation models are moving the market beyond simple analysis to active creation.

- This has led to advancements in generative video and 3d scene reconstruction, revolutionizing generative AI in media creation. Multimodal AI applications and vision language models are enabling more intuitive human-robot interaction, where systems can understand visual and verbal commands contextually. This trend reduces model development time for AI-driven diagnostic tools by up to 40%.

- The ability to create realistic simulations, such as a 3d digital twin for industrial inspection, allows for virtual system validation, reducing latency with edge AI vision during physical deployment.

What challenges does the AI In Vision Industry face during its growth?

- Data privacy, security, and ethical concerns represent a key challenge affecting the industry's growth trajectory.

- Significant challenges surround data privacy in AI vision, security, and the need for ethical AI deployment. The use of biometric identification in public spaces has sparked intense regulatory scrutiny, with error rate disparities in some legacy systems exceeding 30% across demographic groups. This issue of algorithmic bias, often rooted in non-representative training data, remains a fundamental hurdle.

- The complexity and cost of implementation, including the labor-intensive process of data annotation and the capital for high-performance computing, constrain wider adoption. The 'black box' nature of many convolutional neural networks makes it difficult to audit for fairness, a critical requirement for applications like AI in medical imaging analysis or AI-powered video analytics.

- Even with advanced techniques like foveated rendering and eye tracking improving efficiency, ensuring model reliability across diverse, real-world conditions for applications from frictionless checkout solutions to computer vision for smart agriculture and scene segmentation remains a persistent concern.

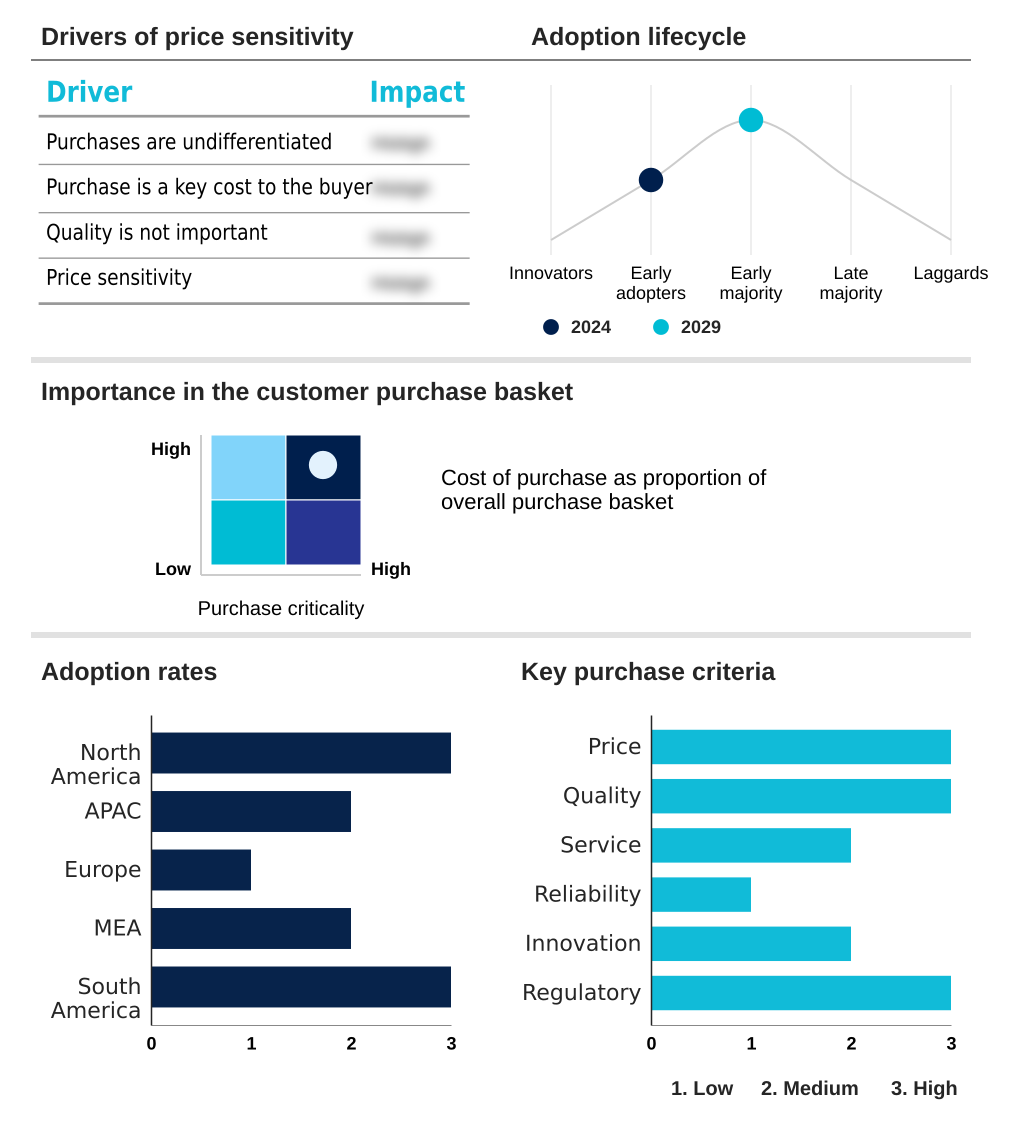

Exclusive Technavio Analysis on Customer Landscape

The ai in vision market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in vision market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Vision Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in vision market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Key offerings enable image analysis, facial recognition, and autonomous logistics through comprehensive cloud-based services, supporting enterprise-grade computer vision applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Apptronik Inc.

- Cipia Vision Ltd.

- Clarifai Inc.

- Google LLC

- Hawk Eye Innovations Ltd.

- Imagga Technologies Ltd.

- Intel Corp.

- Magic Leap Inc.

- Matterport Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- NVIDIA Corp.

- Opencv.ai

- Qualcomm Inc.

- SenseTime Group Inc.

- Trigo Vision Ltd.

- viso.ai

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in vision market

- In September, 2024, NVIDIA Corp. announced a strategic partnership with a leading automotive OEM to co-develop a centralized computing platform for Level 4 autonomous driving, leveraging its next-generation processors to fuse data from over 20 high-resolution cameras.

- In November, 2024, Clarifai Inc. secured $150 million in Series D funding to expand its full-stack generative AI platform, focusing on the creation of high-fidelity synthetic data to train vision models for rare industrial and medical scenarios.

- In February, 2025, the US Department of Commerce, following the lead of the EU's AI Act, published a new framework proposing stringent testing and transparency requirements for facial recognition technologies used in critical infrastructure and public safety applications.

- In April, 2025, Qualcomm Inc. launched its new robotics chipset featuring a dedicated low-power neural processing unit capable of performing complex on-device visual-language tasks, reducing energy consumption for battery-powered drones and robots by 40%.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Vision Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 17.6% |

| Market growth 2025-2029 | USD 34802.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 17.0% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in vision market is defined by a rapid and continuous cycle of innovation, fundamentally altering how industries interact with the physical world.

- Boardroom decisions are increasingly influenced by the strategic shift toward edge computing, which necessitates capital investment in specialized systems on a chip and neural processing units but offers significant long-term ROI through reduced data transmission costs and enhanced data privacy.

- The technological core of the market revolves around the evolution of deep learning models, including convolutional neural networks and vision transformers, which power a vast array of functions from basic image classification and object detection to complex scene segmentation and activity recognition. Applications such as automated quality control, advanced driver-assistance systems, and in-cabin monitoring are becoming standard.

- This technology is powered by hardware like graphics processing units for training and application specific integrated circuits for deployment. Deployments of vision-guided robotics have shown to increase production throughput by over 25% in certain manufacturing settings. The expansion into generative AI, generative video, and multimodal perception is creating new frontiers, enabling more sophisticated natural user interfaces and spatial computing experiences.

What are the Key Data Covered in this AI In Vision Market Research and Growth Report?

-

What is the expected growth of the AI In Vision Market between 2025 and 2029?

-

USD 34.80 billion, at a CAGR of 17.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, Services), Technology (Computer vision, Virtual reality, Augmented reality, Mixed reality), End-user (Manufacturing, Healthcare and life sciences, Automotive, Retail and e-commerce, Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for automation and Industry 4.0 integration, Data privacy, security, and ethical concerns

-

-

Who are the major players in the AI In Vision Market?

-

Amazon.com Inc., Apptronik Inc., Cipia Vision Ltd., Clarifai Inc., Google LLC, Hawk Eye Innovations Ltd., Imagga Technologies Ltd., Intel Corp., Magic Leap Inc., Matterport Inc., Meta Platforms Inc., Microsoft Corp., NVIDIA Corp., Opencv.ai, Qualcomm Inc., SenseTime Group Inc., Trigo Vision Ltd. and viso.ai

-

Market Research Insights

- Market dynamics are increasingly shaped by the migration from cloud-based processing to on-device AI processing, a shift that addresses the critical need for low-latency decision-making. In applications such as autonomous navigation systems and vision-guided robotic assembly, this transition has reduced response times by over 60%, a crucial factor for safety and operational fluidity.

- Concurrently, AI-powered video analytics is being deployed for smart city traffic management, optimizing traffic flow and decreasing congestion by up to 25% in pilot programs. In the commercial sector, AI in retail inventory management has enabled businesses to cut stockout incidents by nearly a third, directly enhancing customer satisfaction and sales.

- These advancements, built on trends like multimodal AI applications and synthetic data generation for AI, highlight a clear business case driven by measurable efficiency gains and enhanced safety protocols.

We can help! Our analysts can customize this ai in vision market research report to meet your requirements.

RIA -

RIA -