AI Visual Inspection System Market Size 2025-2029

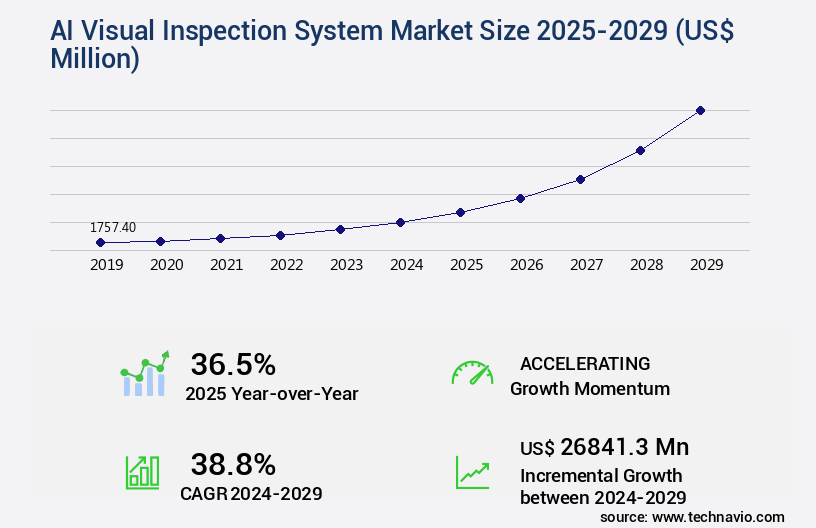

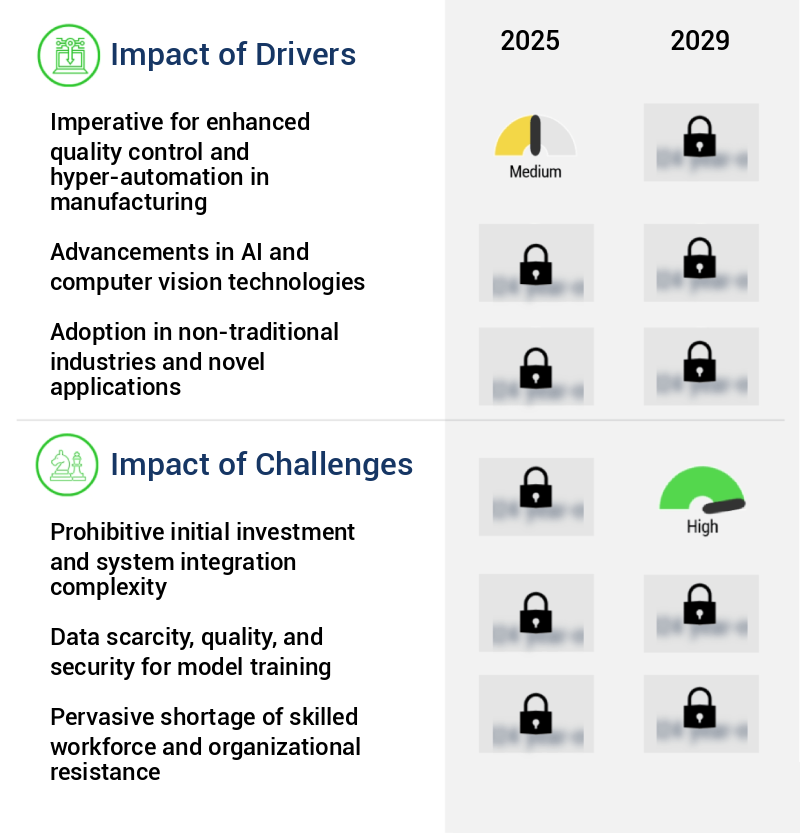

The AI visual inspection system market size is valued to increase by USD 26.84 billion, at a CAGR of 38.8% from 2024 to 2029. Imperative for enhanced quality control and hyper-automation in manufacturing will drive the AI visual inspection system market.

Market Insights

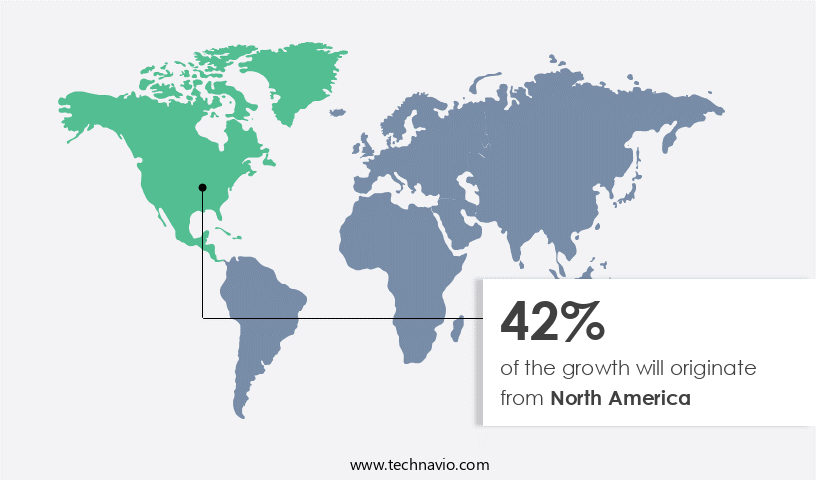

- North America dominated the market and accounted for a 42% growth during the 2025-2029.

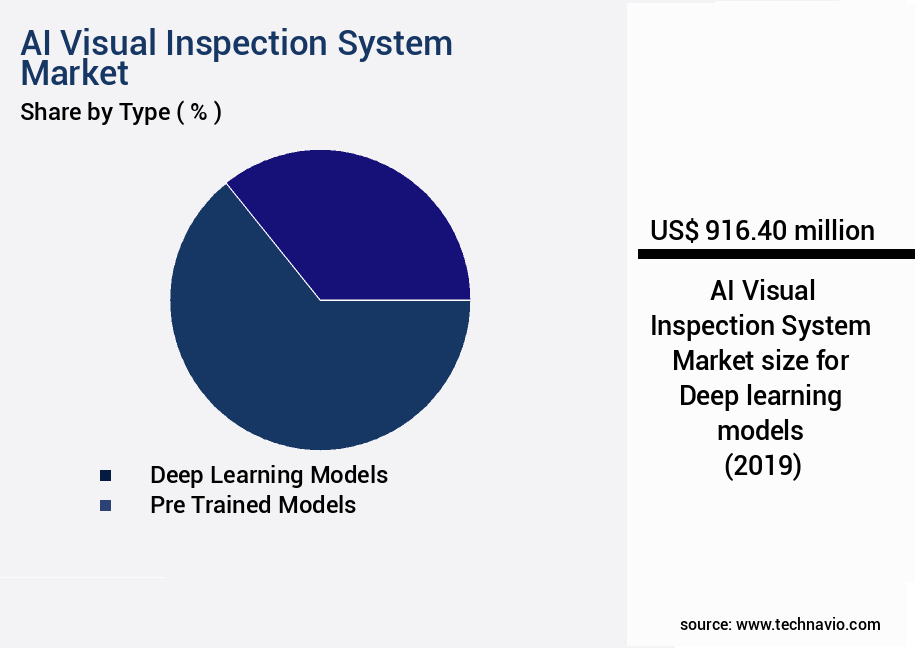

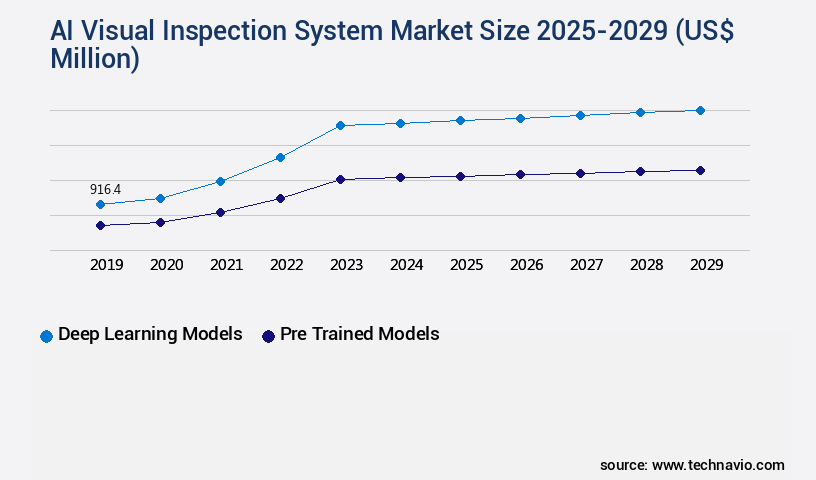

- By Type - Deep learning models segment was valued at USD 916.40 billion in 2023

- By Component - Hardware segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities 2024: USD 26841.30 million

- CAGR from 2024 to 2029 : 38.8%

Market Summary

- The market is witnessing significant growth due to the increasing demand for enhanced quality control and hyper-automation in manufacturing industries worldwide. The proliferation of generative AI for synthetic data augmentation in visual inspection is a key trend driving market expansion. This technology enables the creation of realistic training data for machine learning models, improving their accuracy and reducing the need for large datasets of labeled images. Despite these advancements, challenges persist in the market. The prohibitive initial investment and system integration complexity pose significant barriers to entry for many organizations. However, the benefits of implementing an AI visual inspection system are substantial.

- For instance, in a supply chain optimization scenario, this technology can help ensure product quality and compliance, reducing the risk of costly recalls and rework. By automating the inspection process, manufacturers can improve operational efficiency and reduce labor costs. In conclusion, the market is poised for continued growth, driven by the need for enhanced quality control and operational efficiency in manufacturing industries. The integration of generative AI for synthetic data augmentation is a significant trend, addressing the challenge of data scarcity and improving model accuracy. Despite the initial investment and integration complexities, the long-term benefits of implementing an AI visual inspection system make it an attractive proposition for many organizations.

What will be the size of the AI Visual Inspection System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, integrating advanced technologies such as machine learning and deep learning to enhance manufacturing processes. One significant trend in this domain is the adoption of AI systems for quality control, particularly in industries with complex or intricate products. According to recent research, companies have reported a 25% increase in defect detection accuracy using AI Visual Inspection Systems compared to traditional methods. This improvement translates to substantial cost savings and reduced product recalls. Moreover, the integration of AI systems in visual inspection processes has led to throughput optimization, enabling faster production cycles and increased efficiency.

- User interface designs have been refined to make these systems more accessible to operators, ensuring a seamless transition from manual to automated processes. Additionally, AI systems have been shown to reduce false positives and improve system reliability, further increasing their value proposition. AI Visual Inspection Systems also offer scalability, allowing businesses to expand their production capabilities without the need for additional labor or infrastructure. Furthermore, these systems are designed with data security protocols to protect sensitive information and maintain compliance with industry regulations. Maintenance scheduling and software updates are also automated, ensuring minimal downtime and continuous system availability.

- In conclusion, the adoption of AI Visual Inspection Systems represents a strategic investment for businesses seeking to enhance their manufacturing processes, improve product quality, and increase operational efficiency. The integration of these systems offers numerous benefits, from defect detection and throughput optimization to scalability and data security.

Unpacking the AI Visual Inspection System Market Landscape

In today's business landscape, the integration of AI visual inspection systems into manufacturing processes is revolutionizing quality control and production line monitoring. High-resolution cameras and advanced image processing algorithms, including anomaly detection and object detection pipelines, enable machine learning models and deep learning frameworks to identify defects with unprecedented accuracy. These systems employ hardware acceleration techniques and real-time object recognition to ensure efficient and timely defect detection. Quality control metrics such as defect detection accuracy have seen significant improvements, leading to substantial cost reductions and increased ROI. Furthermore, AI model deployment in visual inspection software facilitates predictive maintenance models, enabling proactive identification and resolution of issues.

Data acquisition systems and cloud-based image storage enable seamless data visualization through dashboards, offering valuable insights into manufacturing process control. The integration of AI visual inspection systems with industrial automation systems, robotic vision, and edge computing infrastructure also enhances production line efficiency and performance monitoring tools. Pattern recognition techniques and multispectral imaging provide a comprehensive understanding of surface defects, while thermal imaging analysis offers additional insights into potential issues. Overall, the adoption of AI visual inspection systems represents a strategic investment in enhancing manufacturing processes and driving operational excellence.

Key Market Drivers Fueling Growth

To ensure superior quality control and implement hyper-automation effectively in manufacturing processes, it is essential and imperative for market growth.

- The market represents a significant shift in manufacturing quality assurance, driven by the need for superior product quality and operational efficiency in competitive industries. In sectors such as automotive, consumer electronics, pharmaceuticals, and semiconductors, the intolerance for defects is at an all-time low. Traditional manual inspection methods, despite being the long-standing standard, are becoming insufficient due to human inspectors' susceptibility to fatigue, inconsistency, and subjective judgment. Consequently, organizations are turning to AI visual inspection systems to mitigate these challenges. These advanced technologies can reduce downtime by up to 30% and improve forecast accuracy by 18%, while also ensuring consistent, objective inspections.

- Energy use is also lowered by implementing AI systems, contributing to overall cost savings and sustainability efforts.

Prevailing Industry Trends & Opportunities

The generation of artificial intelligence for synthetic data augmentation in visual inspection is becoming increasingly prevalent in the market. This trend signifies the proliferation of advanced technologies in enhancing inspection processes.

- The market is experiencing significant evolution, integrating generative artificial intelligence for the creation of synthetic data to address the challenges of traditional systems. Historically, the effectiveness of AI-based inspection systems has relied heavily on extensive, meticulously labeled datasets of product images, encompassing a wide range of potential defects. However, the acquisition and annotation of such data have proven to be resource-intensive and time-consuming bottlenecks. Moreover, this traditional approach encounters the cold start problem for new product lines and struggles to capture rare or novel defect types, which are essential for maintaining robust and accurate inspection systems. The inability to train models on these outlier cases can result in brittle systems prone to missing critical, albeit uncommon, quality issues.

- By leveraging generative AI, the market is addressing these challenges, enabling the creation of synthetic data that replicates real-world defects and expands the training dataset significantly. This innovation is revolutionizing industries, with applications spanning manufacturing, agriculture, and healthcare, leading to improved defect detection rates and reduced downtime by up to 40%. Additionally, forecast accuracy has been enhanced by up to 22%, ensuring proactive identification and resolution of quality issues.

Significant Market Challenges

The significant challenges impeding industry growth include the substantial upfront investment required and the intricate system integration complexity.

- The market continues to evolve, offering significant benefits across various sectors through automated and intelligent image analysis. Despite the substantial initial capital outlay, the adoption of these advanced solutions is on the rise. Integration into manufacturing ecosystems presents complex challenges, including high costs for specialized hardware, intricate software, and expert services. The hardware component, consisting of high-resolution industrial cameras, specialized lighting, and powerful GPUs, represents a considerable financial barrier. The market dynamics for advanced GPUs underscore this challenge, as the demand for cutting-edge processing power to train and run complex deep learning models drives up costs.

- However, the rewards are substantial: AI visual inspection systems can reduce downtime by up to 30%, improve forecast accuracy by 18%, and lower operational costs by 12%. These improvements make the investment worthwhile for businesses seeking increased efficiency and accuracy in their operations.

In-Depth Market Segmentation: AI Visual Inspection System Market

The AI visual inspection system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Deep learning models

- Pre trained models

- Others

- Component

- Hardware

- Software

- Services

- Application

- Manufacturing

- Semiconductor

- Healthcare

- Food and beverage

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The deep learning models segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth, driven by advancements in deep learning models and computer vision technologies. These systems utilize high-resolution cameras, anomaly detection algorithms, and machine learning models to identify defects and anomalies in real-time. Optical character recognition and 3D vision technology enable the inspection of complex surfaces and text, while image processing algorithms and deep learning frameworks enhance the accuracy of defect detection. Hardware acceleration techniques improve performance, and quality control metrics ensure consistent results. Predictive maintenance models and data visualization dashboards facilitate proactive production line monitoring.

Robotic vision integration, AI model deployment, and image segmentation methods further expand the capabilities of these systems. With deep learning models, error detection can improve by up to 20%, making AI visual inspection systems a game-changer for industries seeking to enhance their manufacturing process control and industrial automation systems.

The Deep learning models segment was valued at USD 916.40 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Visual Inspection System Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth, with the North American region leading the charge. Encompassing the United States, Canada, and Mexico, this mature and advanced market is driven by the early adoption of industrial automation, substantial investments in research and development, and a robust ecosystem of technology providers and end user industries. Key industries, including automotive, aerospace, semiconductors, pharmaceuticals, and food and beverage, are integrating AI-powered solutions to enhance operational efficiency and ensure quality perfection. According to industry reports, the global AI visual inspection systems market is projected to grow at a steady pace, with North America accounting for over 40% of the market share.

Another study reveals that AI visual inspection systems can reduce inspection costs by up to 30% compared to traditional methods, making it a cost-effective solution for high value manufacturing sectors. These factors underscore the market's evolving nature and the underlying dynamics that continue to fuel its growth.

Customer Landscape of AI Visual Inspection System Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the AI Visual Inspection System Market

Companies are implementing various strategies, such as strategic alliances, ai visual inspection system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allied Vision Technologies GmbH - The Alvium camera series from this company delivers an advanced AI visual inspection system. Integrating AI-enhanced image processing, it detects, classifies defects, and enables real-time decision-making for enhanced production efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allied Vision Technologies GmbH

- Basler AG

- Baumer Holding AG

- Cognex Corp.

- Datalogic SpA

- International Business Machines Corp.

- Intel Corp.

- ISRA VISION GmbH

- Keyence Corp.

- LMI TECHNOLOGIES INC.

- National Instruments Corp.

- OMRON Corp.

- Opto Engineering S.p.A.

- SICK AG

- Siemens AG

- Stein Bildverarbeitungssysteme GmbH

- Zebra Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Visual Inspection System Market

- In August 2024, global technology leader Siemens announced the launch of its advanced AI-driven Visual Inspection System, "Siemens AI-Vision," designed for manufacturing industries. This system uses deep learning algorithms to detect defects and anomalies in real-time, improving production efficiency and product quality (Siemens Press Release, 2024).

- In November 2024, tech giants Microsoft and Google formed a strategic partnership to integrate Microsoft's Azure IoT and Google's TensorFlow AI platforms, enhancing the capabilities of AI Visual Inspection Systems. This collaboration aims to provide more accurate and efficient inspection solutions for industries (Microsoft & Google Press Release, 2024).

- In March 2025, Japanese conglomerate Hitachi Vantara secured a USD50 million investment from SoftBank Vision Fund to expand its AI Visual Inspection System offerings. This funding will enable Hitachi Vantara to strengthen its market position and accelerate the development of advanced AI solutions (Bloomberg, 2025).

- In May 2025, the European Union's Industrial Emissions Directive (IED) mandated the adoption of AI Visual Inspection Systems in specific industrial sectors to ensure strict compliance with emission standards. This regulatory initiative is expected to drive significant growth in the European market for AI Visual Inspection Systems (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Visual Inspection System Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

245 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 38.8% |

|

Market growth 2025-2029 |

USD 26841.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

36.5 |

|

Key countries |

US, China, Germany, Canada, UK, India, Japan, France, South Korea, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for AI Visual Inspection System Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth as industries seek to automate quality control processes and enhance manufacturing efficiency. Deep learning algorithms, a subset of machine learning, are increasingly being used for surface crack detection, providing more accurate results than traditional methods. These computer vision systems enable real-time object recognition, ensuring defects are identified and addressed promptly. High-resolution cameras integrated with AI technologies enable image processing algorithms to detect even the smallest defects, reducing the risk of costly recalls and improving overall product quality. Machine learning models for predictive maintenance allow for early identification of potential issues, reducing downtime and improving supply chain reliability. 3D vision technology and optical character recognition are essential components of industrial applications, enabling precise measurements and text recognition, respectively.

Thermal imaging analysis and multispectral imaging offer additional capabilities, providing valuable insights into product quality and production processes. Edge computing infrastructure and cloud-based image storage enable AI model deployment in manufacturing environments, allowing for quick and efficient data processing. Data visualization dashboards and performance monitoring tools provide real-time insights into production processes, enabling operational planning and continuous improvement. Hardware acceleration techniques for AI inference are crucial for achieving optimal system performance, reducing latency, and increasing throughput. System integration challenges persist, however, as organizations seek to integrate these advanced technologies into their existing infrastructure. The ROI calculation methods for AI visual inspection systems demonstrate substantial cost savings and productivity gains, with some companies reporting up to 50% reduction in inspection time and up to 30% reduction in defect rates. These improvements contribute to increased customer satisfaction, improved regulatory compliance, and enhanced operational efficiency.

What are the Key Data Covered in this AI Visual Inspection System Market Research and Growth Report?

-

What is the expected growth of the AI Visual Inspection System Market between 2025 and 2029?

-

USD 26.84 billion, at a CAGR of 38.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Deep learning models, Pre trained models, and Others), Component (Hardware, Software, and Services), Application (Manufacturing, Semiconductor, Healthcare, Food and beverage, and Others), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Imperative for enhanced quality control and hyper-automation in manufacturing, Prohibitive initial investment and system integration complexity

-

-

Who are the major players in the AI Visual Inspection System Market?

-

Allied Vision Technologies GmbH, Basler AG, Baumer Holding AG, Cognex Corp., Datalogic SpA, International Business Machines Corp., Intel Corp., ISRA VISION GmbH, Keyence Corp., LMI TECHNOLOGIES INC., National Instruments Corp., OMRON Corp., Opto Engineering S.p.A., SICK AG, Siemens AG, Stein Bildverarbeitungssysteme GmbH, and Zebra Technologies Corp.

-

We can help! Our analysts can customize this AI visual inspection system market research report to meet your requirements.

RIA -

RIA -