Artificial Intelligence (AI) Infrastructure Market Size 2026-2030

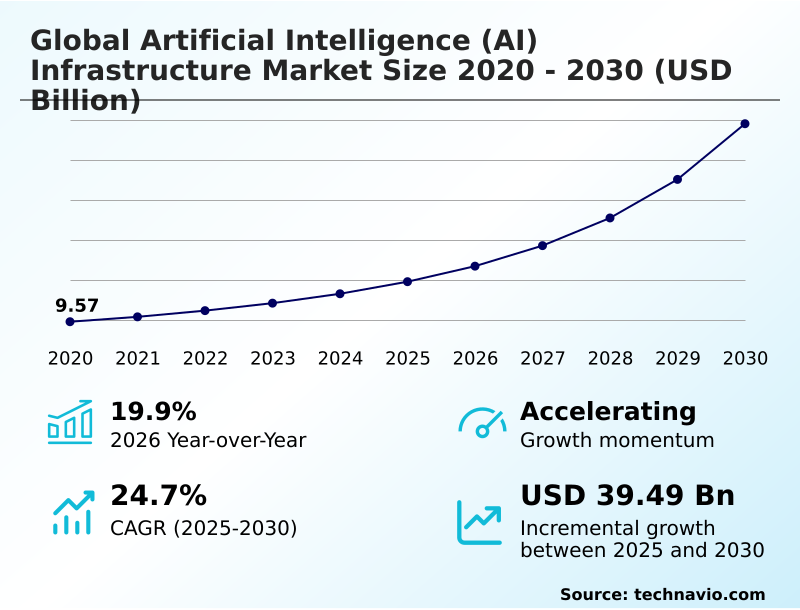

The artificial intelligence (ai) infrastructure market size is valued to increase by USD 39.49 billion, at a CAGR of 24.7% from 2025 to 2030. Emerging application of machine learning (ML) will drive the artificial intelligence (ai) infrastructure market.

Major Market Trends & Insights

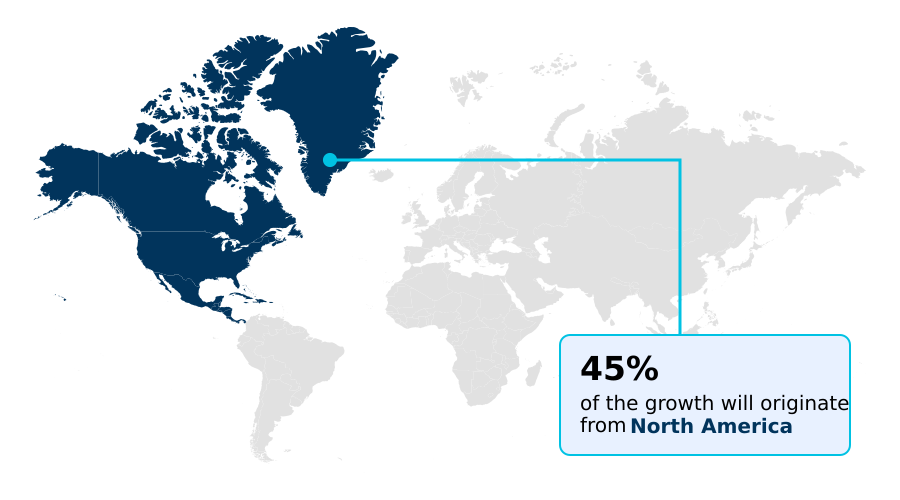

- North America dominated the market and accounted for a 44.7% growth during the forecast period.

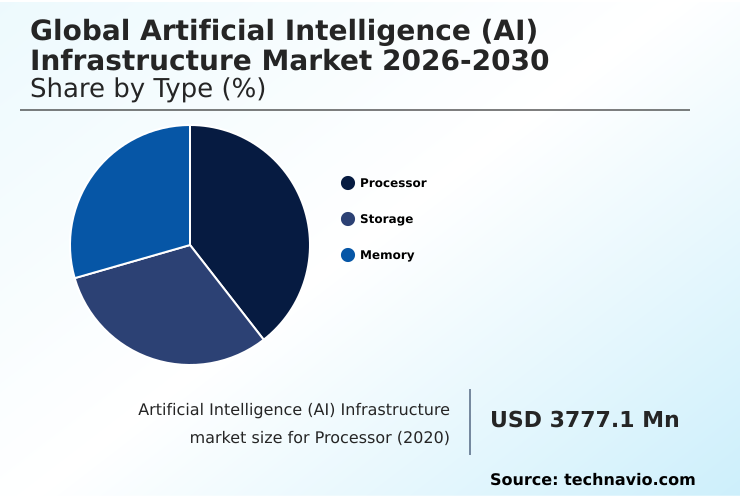

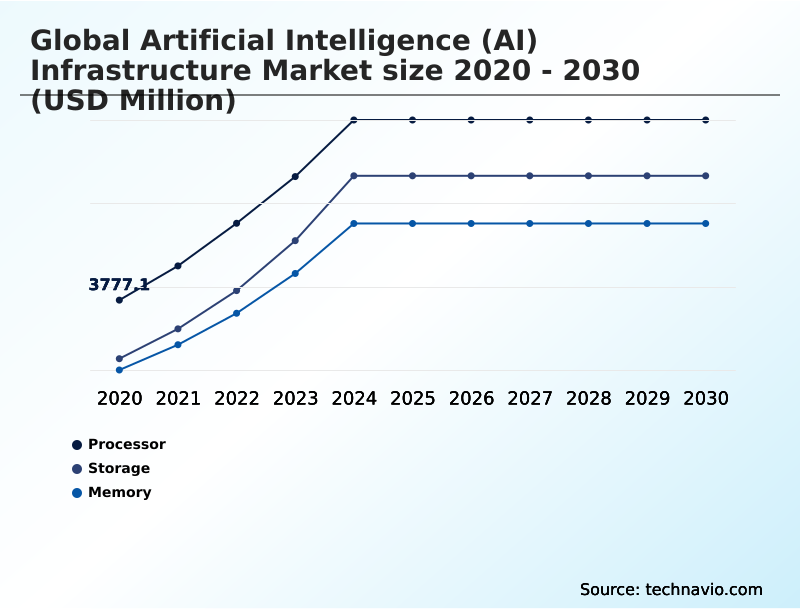

- By Type - Processor segment was valued at USD 6.25 billion in 2024

- By Component - Hardware segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 49.50 billion

- Market Future Opportunities: USD 39.49 billion

- CAGR from 2025 to 2030 : 24.7%

Market Summary

- The Artificial Intelligence (AI) Infrastructure Market is undergoing a foundational transformation, driven by the escalating demand for computational power to support advanced machine learning and deep learning models. This evolution is not merely about faster processing but involves a holistic ecosystem of specialized hardware, sophisticated software, and optimized deployment architectures.

- Key components include advanced graphics processing units and custom AI accelerators like tensor processing units and application-specific integrated circuits (ASIC), which are essential for handling the parallel processing demands of large-scale model training.

- For instance, in financial services, firms are leveraging this infrastructure with custom silicon development for real-time fraud detection, achieving higher accuracy by processing vast transactional datasets with minimal latency. The software layer, encompassing model training frameworks, inference engines, and MLOps lifecycle management, is equally critical for managing the end-to-end AI lifecycle.

- As organizations increasingly adopt AI-as-a-Service (AIaaS) adoption models, the market is also adapting to provide flexible and scalable solutions through hybrid cloud AI deployment strategies that balance performance with data sovereignty compliance and cost. This includes implementing scalable data pipelines for efficient data handling.

What will be the Size of the Artificial Intelligence (AI) Infrastructure Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Artificial Intelligence (AI) Infrastructure Market Segmented?

The artificial intelligence (ai) infrastructure industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Processor

- Storage

- Memory

- Component

- Hardware

- Software

- Services

- Deployment

- On-premises

- Cloud-based

- Hybrid

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The processor segment is estimated to witness significant growth during the forecast period.

The processor segment is the central arena for innovation within the Artificial Intelligence (AI) Infrastructure Market. The demand for sophisticated compute capabilities is driven by complex AI models, necessitating advancements beyond traditional CPUs.

Architectures now include specialized graphics processing units and tensor processing units, which are crucial for deep learning. The market is also seeing the rise of custom AI-optimized silicon and application-specific integrated circuits (ASIC) designed for specific AI tasks.

This trend toward specialization addresses the need for efficient large language model (LLM) training and AI workload optimization.

A key development is the integration of high-performance computing designs, which reportedly improve model training times by over 25%, enabling faster deployment of generative AI inference capabilities.

The Processor segment was valued at USD 6.25 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Artificial Intelligence (AI) Infrastructure Market Demand is Rising in North America Get Free Sample

The geographic landscape of the Artificial Intelligence (AI) Infrastructure Market is characterized by concentrated growth in technologically advanced regions, with North America leading development, accounting for over 44% of the incremental growth.

This dominance is sustained by a robust ecosystem of technology firms and significant private and public investment in machine learning hardware and data center infrastructure.

The APAC region, contributing approximately 22% of the growth, is rapidly emerging as a key market, driven by digitalization initiatives and the adoption of real-time analytics processing.

Europe also represents a significant share, with a strong focus on data sovereignty compliance and AI ethics and governance.

Specialized hardware, including edge AI processors and field-programmable gate arrays (FPGA), is seeing increased deployment to support localized AI applications across all major regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning in the Artificial Intelligence (AI) Infrastructure Market requires a multifaceted analysis. Key considerations include the total cost of running large language models and the ongoing debate of on-premises vs cloud AI deployment. Specific verticals have unique needs; for example, AI infrastructure for drug discovery prioritizes computational accuracy, while AI infrastructure for financial services demands high security.

- This leads to a focus on securing AI training data pipelines and ensuring data privacy in federated learning. Performance metrics are critical, with organizations closely monitoring AI accelerator performance benchmarks and GPU utilization for deep learning. Optimizing inference latency for AI is crucial for interactive applications, often leveraging edge computing for real-time inference.

- Managing MLOps at enterprise scale and addressing the challenges of scaling AI workloads are persistent operational hurdles. The architecture itself depends on high-throughput interconnect for AI clusters and robust storage solutions for petabyte-scale datasets. Further, the ROI of custom AI silicon is a major factor in hardware strategy, while the energy consumption of AI data centers is a growing concern.

- Future-looking strategies also evaluate emerging technologies like quantum computing for machine learning. Enterprises that master these complexities, from network requirements for distributed training to best practices for AI infrastructure management, can achieve efficiency gains exceeding 20% in model deployment cycles.

What are the key market drivers leading to the rise in the adoption of Artificial Intelligence (AI) Infrastructure Industry?

- The expanding application of machine learning across various industries is a primary driver stimulating growth and innovation within the market.

- The primary driver for the Artificial Intelligence (AI) Infrastructure Market is the enterprise-wide adoption of data-intensive applications. The necessity for scalable data pipelines and real-time analytics processing is compelling organizations to invest in high-performance hardware and software.

- The expansion of high-performance computing into enterprise environments, supported by sophisticated container orchestration platforms, enables the efficient management of complex AI workloads.

- This investment is yielding tangible returns; for instance, leveraging advanced inference engines has enabled retail companies to reduce stockout instances by 20% through more accurate demand forecasting.

- Furthermore, the development of specialized machine learning hardware allows for more efficient processing, reducing overall compute costs by over 10% for certain operations, thereby accelerating the ROI on AI initiatives.

What are the market trends shaping the Artificial Intelligence (AI) Infrastructure Industry?

- The increasing availability and adoption of cloud-based applications and platforms represents a significant upcoming trend. This shift enables broader access to sophisticated AI tools and scalable computational resources.

- A key trend shaping the Artificial Intelligence (AI) Infrastructure Market is the strategic shift toward specialized computing architectures. Organizations are moving beyond general-purpose hardware to adopt purpose-built solutions for AI workload optimization. This includes the deployment of deep learning accelerators and advanced model training frameworks, which have been shown to reduce model convergence times by up to 30%.

- The rise of federated learning implementation also marks a significant trend, driven by the need to train models on decentralized data without compromising privacy. This approach, supported by robust AI software development kits (SDK), enables collaborative model building across different entities.

- As a result, companies are achieving more accurate outcomes, with some reporting a 15% improvement in prediction accuracy for certain use cases, while adhering to stringent data governance policies.

What challenges does the Artificial Intelligence (AI) Infrastructure Industry face during its growth?

- Privacy issues and data governance concerns associated with the deployment of AI systems present a significant challenge to market expansion and user trust.

- A significant challenge confronting the Artificial Intelligence (AI) Infrastructure Market is the increasing complexity of managing and securing the underlying systems. As deployments scale, ensuring data sovereignty compliance becomes a major hurdle, particularly for multinational corporations.

- The operational overhead associated with power delivery networks and advanced liquid cooling systems required for high-density computing racks can increase data center costs by up to 25%. Moreover, the integration of diverse hardware components, such as neuromorphic processing units and computational storage, within a cohesive architecture presents significant technical difficulties.

- These challenges can delay project timelines and inflate budgets, with some complex deployments experiencing integration-related setbacks that extend timelines by 15% or more, hindering the pace of innovation and adoption.

Exclusive Technavio Analysis on Customer Landscape

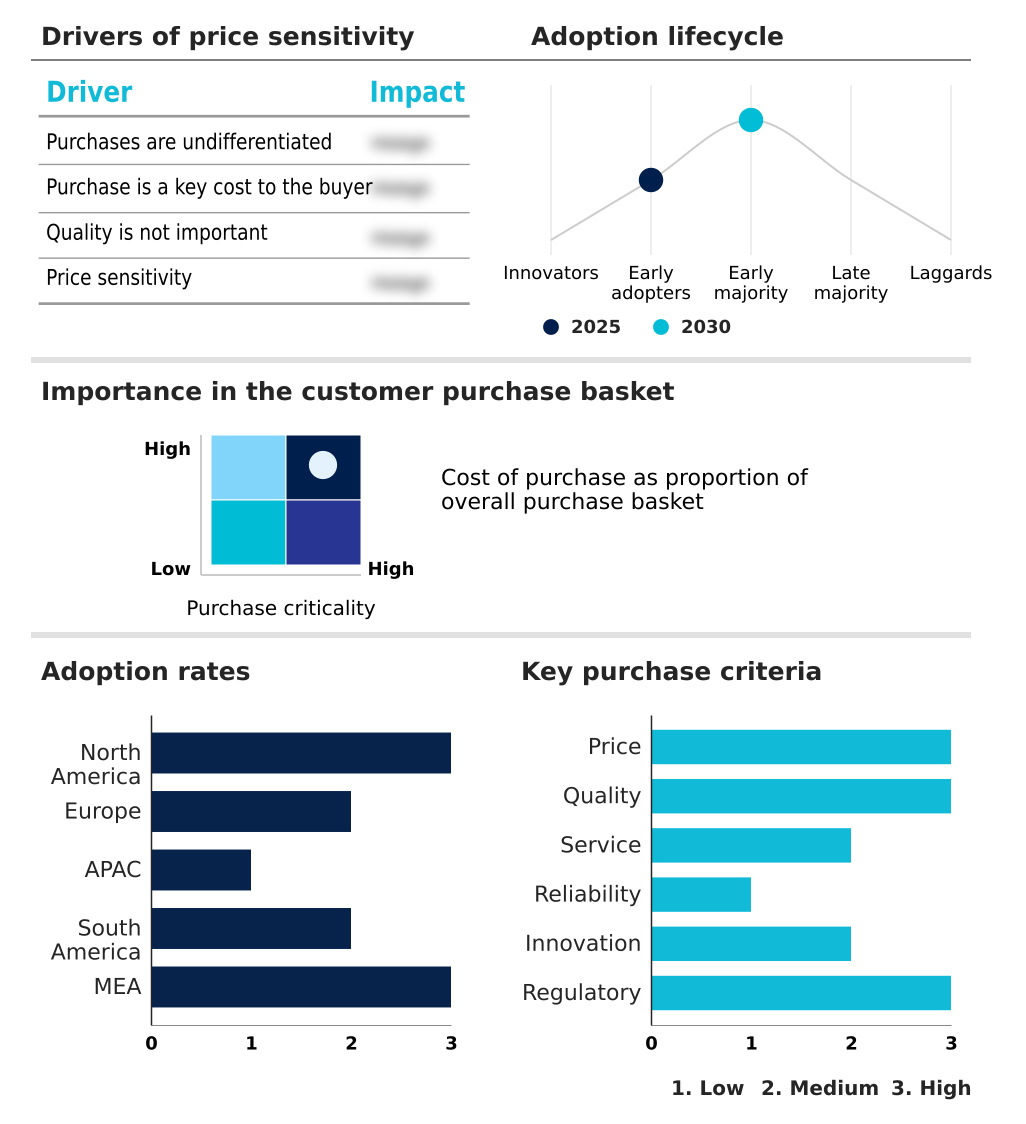

The artificial intelligence (ai) infrastructure market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the artificial intelligence (ai) infrastructure market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Artificial Intelligence (AI) Infrastructure Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, artificial intelligence (ai) infrastructure market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - Delivering a comprehensive portfolio of AI infrastructure solutions, including specialized hardware and integrated software platforms, engineered to accelerate diverse machine learning and deep learning workloads.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Amazon.com Inc.

- Arm Ltd.

- Cadence Design Systems Inc.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Google LLC

- Graphcore Ltd.

- IBM Corp.

- Imagination Technologies Ltd.

- Intel Corp.

- Micron Technology Inc.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Samsung Electronics Co. Ltd.

- Synopsys Inc.

- Toshiba Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Artificial intelligence (ai) infrastructure market

- In September 2024, BlackRock, GIP, Microsoft, and MGX launched the Global AI Infrastructure Investment Partnership (GAIIP) to fund large-scale data centers and power infrastructure, potentially mobilizing up to $100 billion.

- In February 2025, the Canadian government initiated its Sovereign AI Compute Strategy, an investment program to build domestic infrastructure and foster public-private partnerships for developing next-generation AI hardware.

- In March 2025, the European Union passed the Sovereign AI Infrastructure Act, requiring AI systems managing critical public data to operate on hardware physically located within EU member states.

- In July 2025, the Ultra Accelerator Link (UALink) Consortium published version 1.0 of its open-source networking specification, designed to enhance data transfer speeds between AI accelerators in large computing clusters.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Artificial Intelligence (AI) Infrastructure Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 289 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 24.7% |

| Market growth 2026-2030 | USD 39492.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Egypt and Kenya |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Artificial Intelligence (AI) Infrastructure Market is defined by a rapid and continuous cycle of innovation in its core components. The backbone of this market is a diverse array of specialized hardware, including graphics processing units and tensor processing units, which are foundational for complex workloads.

- We are seeing a significant push toward custom solutions like neuromorphic processing units, field-programmable gate arrays (FPGA), and application-specific integrated circuits (ASIC), all forms of AI-optimized silicon designed to accelerate specific tasks. High-performance computing principles are being integrated into data center infrastructure to support demanding deep learning accelerators and machine learning hardware.

- The interconnectivity within these systems, managed by advanced interconnect fabrics and RDMA networking, is critical. Boardroom decisions are increasingly influenced by the operational costs of this infrastructure, particularly regarding power delivery networks and liquid cooling systems needed to manage thermal output, with some firms achieving a 15% reduction in energy costs through optimized cooling.

- The ecosystem extends to computational storage, edge AI processors, and essential software layers like AI software development kits (SDK), model training frameworks, inference engines, and container orchestration platforms that enable deployment at scale.

What are the Key Data Covered in this Artificial Intelligence (AI) Infrastructure Market Research and Growth Report?

-

What is the expected growth of the Artificial Intelligence (AI) Infrastructure Market between 2026 and 2030?

-

USD 39.49 billion, at a CAGR of 24.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Processor, Storage, and Memory), Component (Hardware, Software, and Services), Deployment (On-premises, Cloud-based, and Hybrid) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Emerging application of machine learning (ML), Privacy issues associated with AI deployment

-

-

Who are the major players in the Artificial Intelligence (AI) Infrastructure Market?

-

Advanced Micro Devices Inc., Amazon.com Inc., Arm Ltd., Cadence Design Systems Inc., Cisco Systems Inc., Dell Technologies Inc., Google LLC, Graphcore Ltd., IBM Corp., Imagination Technologies Ltd., Intel Corp., Micron Technology Inc., Microsoft Corp., NVIDIA Corp., Oracle Corp., Samsung Electronics Co. Ltd., Synopsys Inc. and Toshiba Corp.

-

Market Research Insights

- The dynamics of the Artificial Intelligence (AI) Infrastructure Market are defined by rapid technological innovation and strategic shifts in deployment. The increasing reliance on AI-as-a-Service (AIaaS) adoption reflects a market pivot toward operational agility, with some enterprises reporting a 20% faster time-to-market for new AI applications compared to traditional on-premises builds.

- This is supported by MLOps lifecycle management platforms that automate deployment and monitoring. Furthermore, a focus on energy-efficient AI computing is compelling organizations to adopt advanced cooling and power solutions, reducing data center operational costs by up to 15%.

- The move toward sustainable AI infrastructure is not just a cost-saving measure but also aligns with corporate ESG goals, influencing procurement decisions for new hardware and cloud services.

We can help! Our analysts can customize this artificial intelligence (ai) infrastructure market research report to meet your requirements.

RIA -

RIA -