AI Legal Tech Market Size 2026-2030

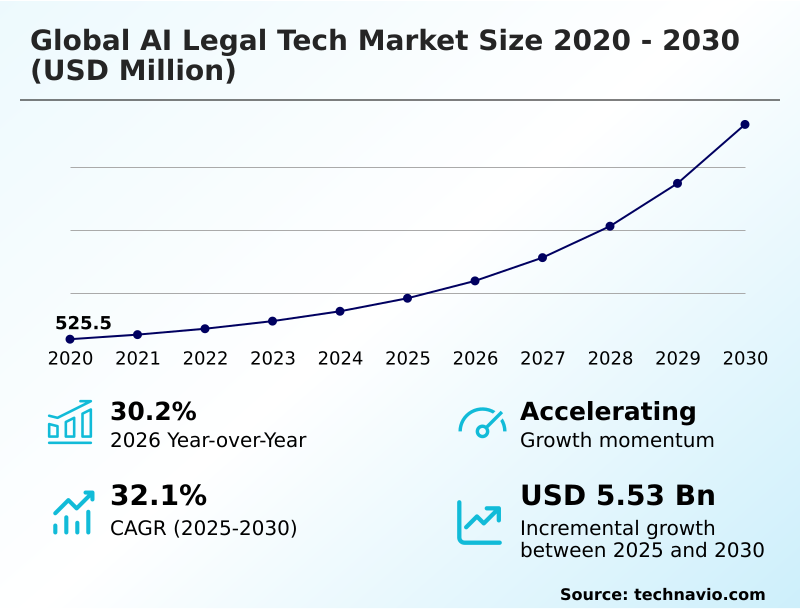

The AI Legal Tech Market size was valued at USD 1.83 billion in 2025, growing at a CAGR of 32.1% during the forecast period 2026-2030.

Major Market Trends & Insights

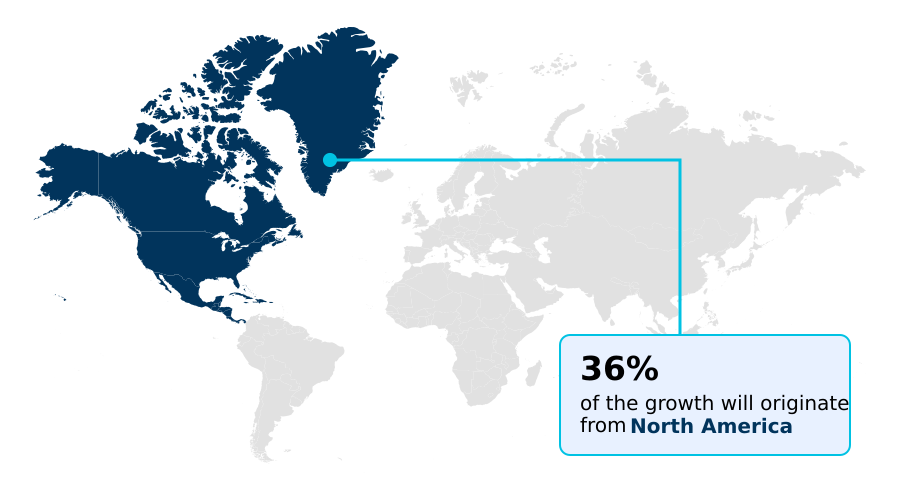

- North America dominated the market and accounted for a 35.5% growth during the forecast period.

- By Component - Solution segment was valued at USD 951.6 million in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 6.83 billion

- Market Future Opportunities 2025-2030: USD 5.53 billion

- CAGR from 2025 to 2030 : 32.1%

Market Summary

- The AI legal tech market is undergoing a profound structural evolution, with adoption rates for integrated solutions increasing by 30.2% year-over-year. This growth is driven by the shift from standalone tools to unified, intelligent ecosystems that embed AI directly into daily legal workflows.

- For instance, a large law firm can leverage AI for e-discovery to review documents, reducing manual labor by over 60% and accelerating case preparation. The primary driver for this adoption is the escalating demand for cost efficiency, compelling firms to automate routine tasks to remain competitive.

- However, this transition is challenged by the persistent issue of data privacy and the need for robust AI governance to prevent model hallucinations and maintain attorney-client privilege. Consequently, the market is characterized by a dual focus on advancing autonomous capabilities while ensuring the technology is secure, traceable, and ethically sound.

What will be the Size of the AI Legal Tech Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI Legal Tech Market Segmented?

The ai legal tech industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Solution

- Services

- Deployment

- On-premises

- Cloud-based

- Technology

- Machine learning

- Deep learning

- Natural language processing

- End-user

- Law firms

- Corporate departments

- Government bodies

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- Australia

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- Israel

- Rest of World (ROW)

- North America

How is the AI Legal Tech Market Segmented by Component?

The solution segment is estimated to witness significant growth during the forecast period.

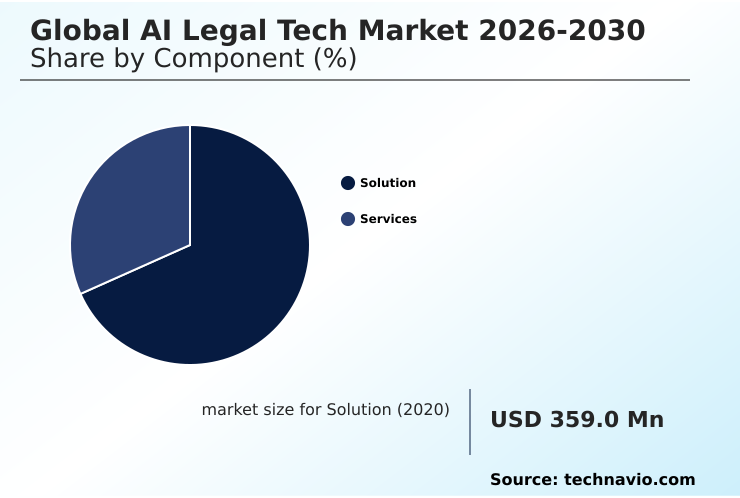

The solution segment of the AI legal tech market, which accounts for 67% of the total revenue, is shifting from standalone applications to integrated platforms featuring agentic AI and legal reasoning.

These systems are not just tools but core infrastructure, with cloud-based deployment enabling a 30% faster rollout of updates compared to on-premises versions.

The adoption of workflow native intelligence and natural language processing is crucial, as it allows for the automation of complex tasks like e-discovery and contract lifecycle management. This integration supports alternative fee arrangements by providing predictable outcomes.

Solutions that incorporate generative AI and legal research automation are seeing higher demand, driven by the need for efficiency and the ability to handle large-scale document automation.

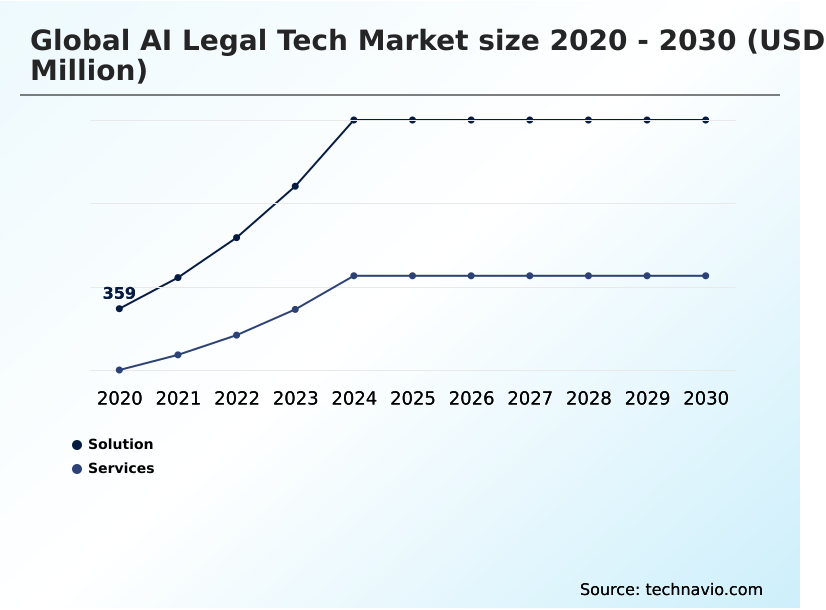

The Solution segment was valued at USD 951.6 million in 2024 and showed a gradual increase during the forecast period.

How demand for the AI Legal Tech market is rising in the leading region?

North America is estimated to contribute 35.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Legal Tech Market demand is rising in North America Request Free Sample

North America leads the AI legal tech market, commanding 35.5% of the incremental growth, driven by a mature legal sector that aggressively pursues digitization to enhance efficiency.

The US accounts for over 80% of the region's market, with law firms leveraging agentic AI for complex litigation and contract lifecycle management.

In contrast, the APAC market, with a CAGR of 33.1%, is the fastest-growing region, fueled by government-led initiatives to modernize judiciary systems and improve access to justice.

This geographic divergence is shaped by differing regulatory environments and adoption drivers; North America focuses on optimizing established workflows, while APAC prioritizes building digital-first legal infrastructure.

This dynamic requires providers to tailor their sovereign AI and data sovereignty solutions to meet distinct regional needs for data privacy regulations and legal reasoning.

What are the key Drivers, Trends, and Challenges in the AI Legal Tech Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of artificial intelligence within the legal sector is fundamentally reshaping operational paradigms, with a clear focus on enhancing efficiency and accuracy. Firms are increasingly exploring agentic AI for legal research, moving beyond simple keyword searches to sophisticated, context-aware inquiries that can synthesize information from vast legal corpora.

- This is complemented by the growing use of AI legal tech contract analysis, which automates the review of complex agreements, identifies risks, and ensures compliance with internal playbooks. The role of natural language processing in law is central to these advancements, enabling machines to understand the nuance and intent of legal text.

- For example, AI for legal document automation has streamlined the creation of everything from simple motions to complex transactional documents, reducing drafting time by over 50% in some use cases. However, this rapid adoption brings the challenge of AI governance in legal practice to the forefront.

- Ensuring that these autonomous systems are transparent, auditable, and free from bias is a critical concern, demanding robust ethical AI frameworks.

- The development of these technologies is not happening in a vacuum; it is a direct response to the need to manage escalating data volumes and client demands for more predictable, value-based pricing, a stark difference from firms still relying on a 100% manual review process.

What are the key market drivers leading to the rise in the adoption of AI Legal Tech Industry?

- A key market driver is the fundamental shift toward agentic AI and autonomous workflows, which redefines legal process efficiency and enhances professional productivity.

- The primary driver for the AI legal tech market is the intense economic pressure on law firms and corporate legal departments to deliver more value at a lower cost, which has accelerated the shift toward alternative fee arrangements.

- Automating routine tasks such as document review and legal research automation can reduce operational costs by over 30%, a crucial factor in maintaining profitability.

- This economic imperative is fueling the adoption of agentic AI, which can conduct initial case assessments and draft transaction documents, increasing legal operations productivity by up to 40%.

- The deep integration of AI into native software ecosystems removes adoption friction, making advanced predictive litigation analytics and document automation accessible to firms of all sizes. This digital transformation enables a more strategic allocation of human resources.

What are the market trends shaping the AI Legal Tech Industry?

- The market is undergoing a significant transition from reactive, prompt-based assistants toward proactive agentic AI. This evolution facilitates the autonomous execution of complex, multi-step legal workflows without constant human intervention.

- The AI legal tech market is rapidly shifting from reactive chatbots to proactive, agentic AI systems that can execute multi-step workflows with over 90% autonomy. This trend toward autonomous workflows is not just about efficiency; it is a strategic move to free up legal professionals for higher-value advisory work.

- For example, integrated systems are seeing 25% higher adoption rates than standalone tools because they embed legal reasoning and generative AI capabilities directly into existing document management platforms. This workflow-native intelligence minimizes disruption and accelerates the return on investment.

- The focus on retrieval-augmented generation ensures that all AI-generated outputs are linked to citable authority, addressing the critical need for accuracy and reliability in legal practice.

What challenges does the AI Legal Tech Industry face during its growth?

- Regulatory fragmentation and the escalating complexity of compliance across multiple jurisdictions present a primary challenge, hindering streamlined market growth and increasing operational costs.

- A significant challenge hindering the AI legal tech market is the fragmented and evolving regulatory landscape, which can increase compliance overhead for technology providers by up to 20%. Navigating differing data privacy regulations and AI governance mandates across jurisdictions like North America and Europe creates significant development friction.

- Furthermore, the inherent risk of AI model 'hallucination' poses a serious threat to the precision required in legal work, where a single error can have major consequences.

- This technical trust deficit is compounded by data sovereignty concerns, forcing a difficult trade-off between leveraging powerful cloud-based large language models and maintaining attorney-client privilege through less powerful on-premises solutions, where processing latency can be 15% higher.

Exclusive Technavio Analysis on Customer Landscape

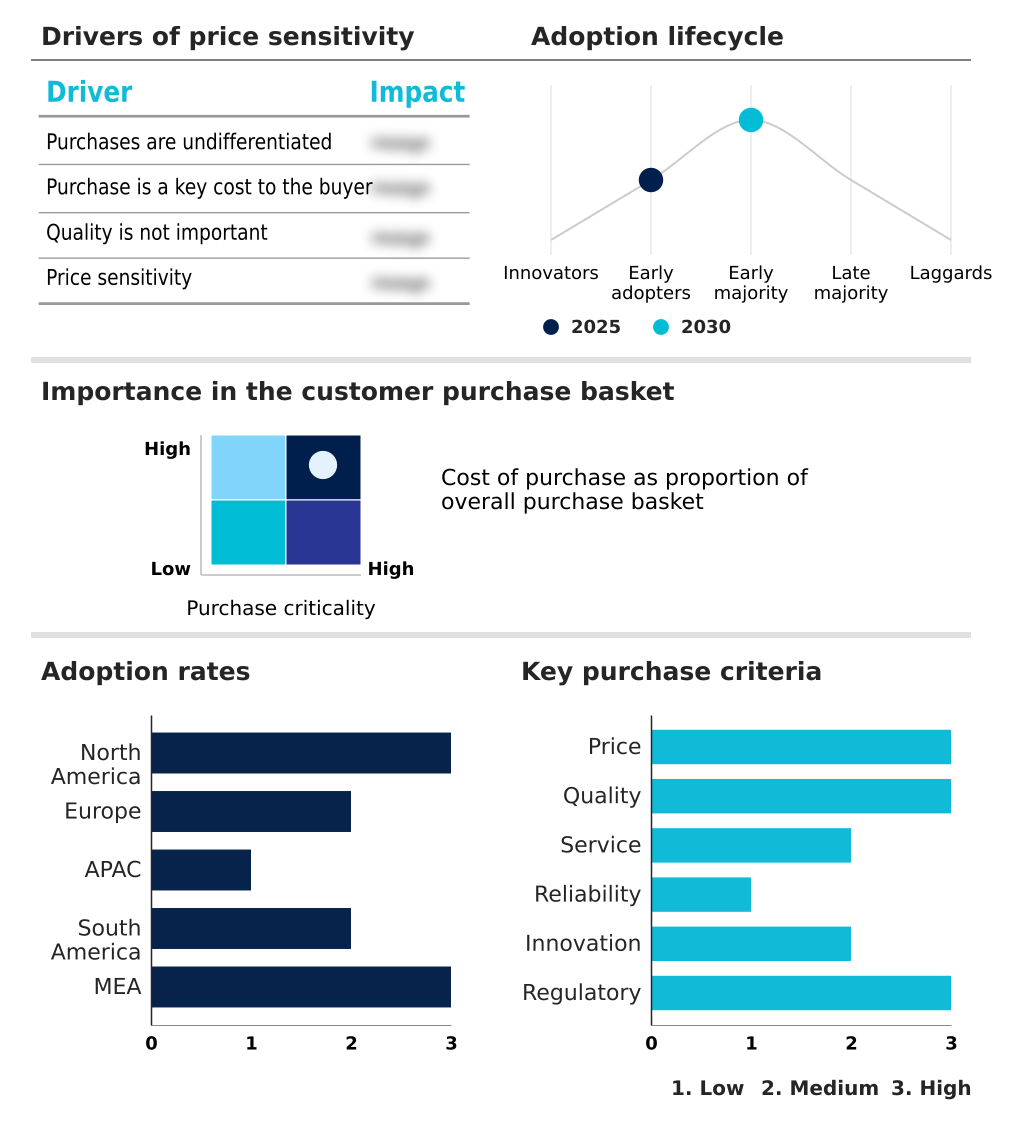

The ai legal tech market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai legal tech market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Legal Tech Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai legal tech market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - Vendors provide model inference optimization tools, enabling optimized deployment and acceleration of deep learning inference workloads on diverse hardware architectures, including CPUs, GPUs, and NPUs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Alibaba Group Holding Ltd.

- Amazon Web Services Inc.

- Axelera AI

- Cerebras Systems Inc.

- Gcore

- Google LLC

- Graphcore Ltd.

- Groq Inc.

- Hugging Face Inc.

- IBM Corp.

- Intel Corp.

- Microsoft Corp.

- Modular Inc.

- NVIDIA Corp.

- Qualcomm Inc.

- Recogni

- Scaleway SAS

- Tenstorrent Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Application Software industry, the widespread adoption of cloud-native platforms and SaaS delivery models has been pivotal, creating the necessary infrastructure for scalable, cloud-based AI legal tech solutions and enabling vendors to offer sophisticated capabilities through a subscription model, which enhances accessibility for smaller firms.

- The increasing focus on data privacy regulations and security within the broader software market has directly impacted AI legal tech development, compelling providers to prioritize AI governance and data sovereignty, leading to innovations in sovereign AI and on-premises deployments to ensure compliance and protect attorney-client privilege.

- A major trend in enterprise software is the embedding of intelligent automation and analytics directly into existing workflows, such as ERP and CRM systems. This has accelerated the demand for workflow-native intelligence in the legal field, where AI is integrated seamlessly into document management and communication tools.

- The maturation of business process automation and robotic process automation (RPA) technologies has set a precedent for the adoption of more advanced autonomous systems. This has paved the way for the acceptance of agentic AI and autonomous workflows in the legal sector, shifting the focus from simple task automation to complex legal reasoning and multi-step workflow execution.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Legal Tech Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 311 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 32.1% |

| Market growth 2026-2030 | USD 5530.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 30.2% |

| Key countries | US, Canada, Mexico, UK, Germany, France, The Netherlands, Sweden, Italy, China, Japan, Australia, India, Singapore, Indonesia, Brazil, Argentina, Colombia, UAE, Saudi Arabia, Israel, South Africa and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI legal tech market ecosystem is a complex network where technology providers, legal professionals, and regulatory bodies converge. Law firms and corporate legal departments represent the largest end-user segments, accounting for over 70% of the market, driven by the need to automate high-volume tasks and mitigate risk.

- Foundational model providers and cloud infrastructure giants like AWS and Google form the base of the supply chain, offering the core computing power for model inference optimization. Solution providers build upon this foundation, creating specialized applications for e-discovery and contract lifecycle management.

- Notably, on-premises deployment still holds a significant 59.5% market share, underscoring the paramount importance of data sovereignty and attorney-client privilege. This dynamic ecosystem is further shaped by regulatory bodies that are establishing AI governance frameworks, influencing the development of explainable AI and ethical AI frameworks to ensure accountability and trust.

What are the Key Data Covered in this AI Legal Tech Market Research and Growth Report?

-

What is the expected growth of the AI Legal Tech Market between 2026 and 2030?

-

The AI Legal Tech Market is expected to grow by USD 5.53 billion during 2026-2030, registering a CAGR of 32.1%. Year-over-year growth in 2026 is estimated at 30.2%%. This acceleration is shaped by shift toward agentic ai and autonomous workflows , which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solution, and Services), Deployment (On-premises, and Cloud-based), Technology (Machine learning, Deep learning, and Natural language processing), End-user (Law firms, Corporate departments, Government bodies, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Solution segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 35.5% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, UK, Germany, France, The Netherlands, Sweden, Italy, China, Japan, Australia, India, Singapore, Indonesia, Brazil, Argentina, Colombia, UAE, Saudi Arabia, Israel, South Africa and Nigeria, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is shift toward agentic ai and autonomous workflows , which is accelerating investment and industry demand. The main challenge is regulatory fragmentation and compliance complexity , creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the AI Legal Tech Market?

-

Key vendors include Advanced Micro Devices Inc., Alibaba Group Holding Ltd., Amazon Web Services Inc., Axelera AI, Cerebras Systems Inc., Gcore, Google LLC, Graphcore Ltd., Groq Inc., Hugging Face Inc., IBM Corp., Intel Corp., Microsoft Corp., Modular Inc., NVIDIA Corp., Qualcomm Inc., Recogni, Scaleway SAS and Tenstorrent Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the AI legal tech market, where North America accounts for over 35% of the incremental growth, is defined by a race to deliver autonomous, agentic systems. Key players like LexisNexis and Ironclad are pushing the envelope beyond simple automation. LexisNexis's global launch of its Protege AI assistant introduced sophisticated, citable workflows for disputes and case strategy.

- Similarly, Ironclad's suite of contract intelligence agents aims to transform static documents into actionable business assets. These developments reflect a market-wide pivot from passive systems of record to dynamic systems of action. This transition is a direct response to enterprise demand for tools that can handle multi-step legal reasoning with minimal human oversight.

- However, vendors face the persistent challenge of ensuring model reliability and mitigating the risks of AI hallucination, which requires significant investment in traceability and explainability features.

We can help! Our analysts can customize this ai legal tech market research report to meet your requirements.

RIA -

RIA -