AI Procurement Intelligence Market Size 2025-2029

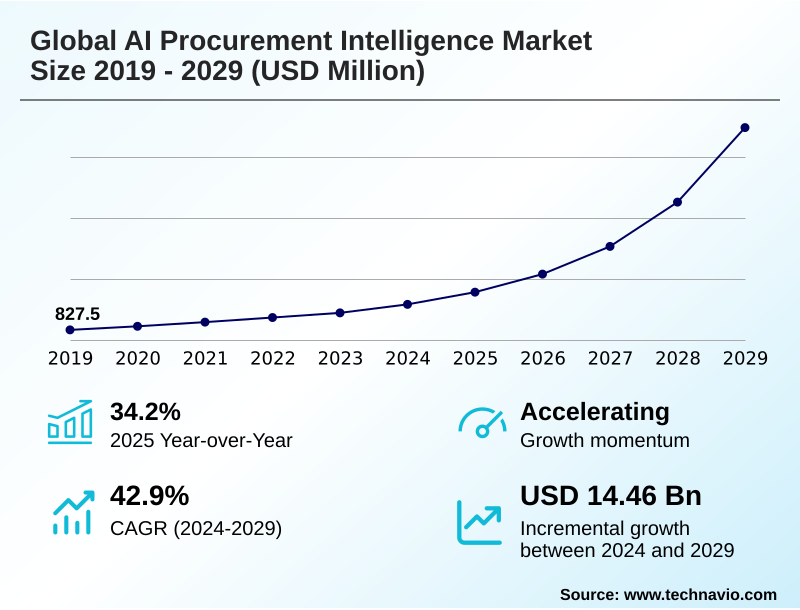

The ai procurement intelligence market size is valued to increase by USD 14.46 billion, at a CAGR of 42.9% from 2024 to 2029. Imperative for cost optimization and efficiency amid global economic volatility will drive the ai procurement intelligence market.

Major Market Trends & Insights

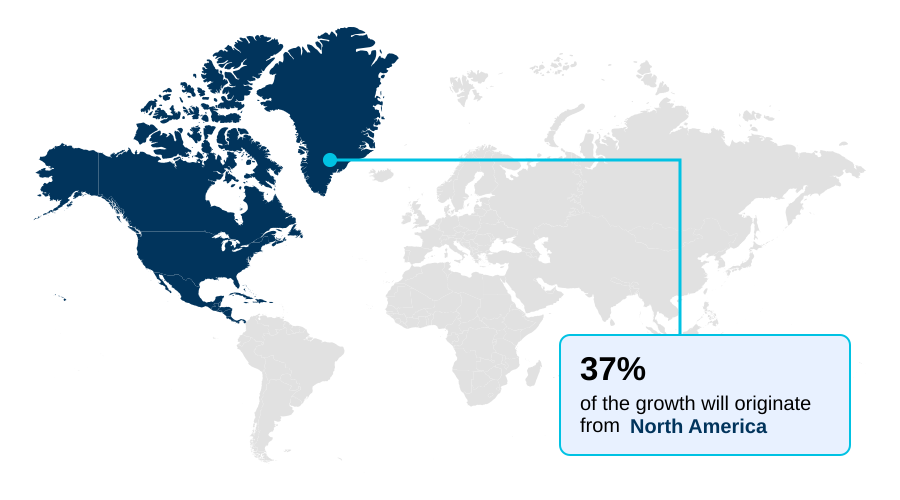

- North America dominated the market and accounted for a 37.3% growth during the forecast period.

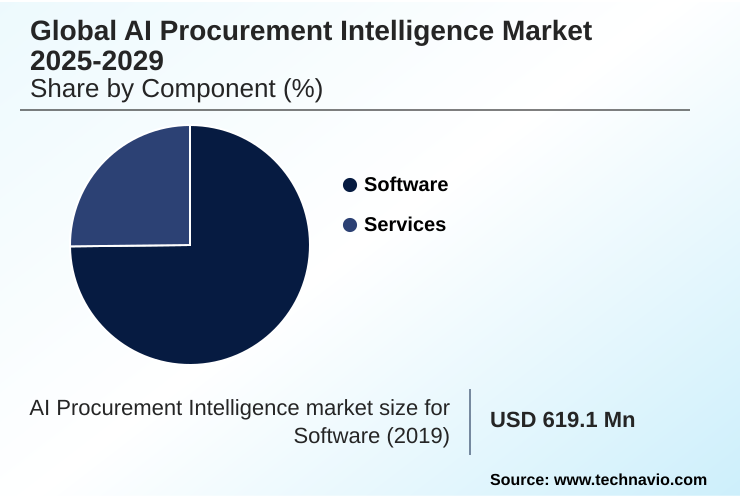

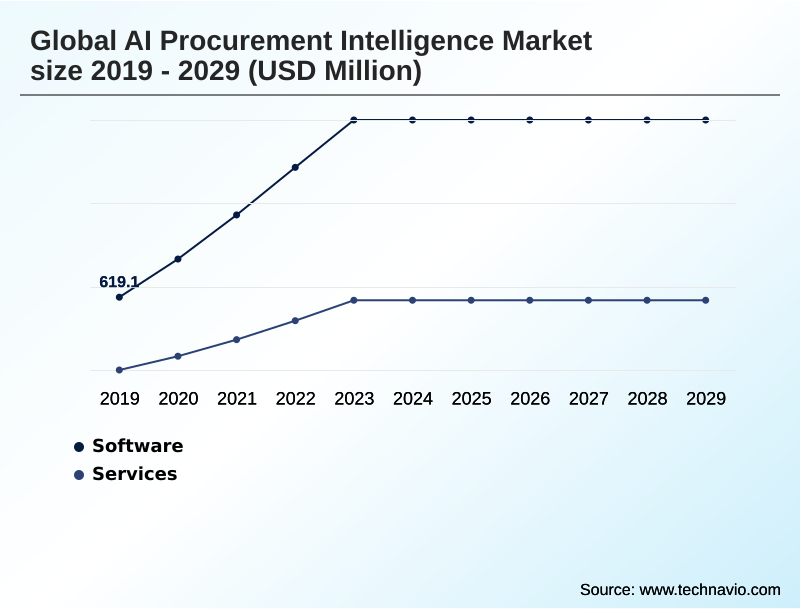

- By Component - Software segment was valued at USD 1.62 billion in 2023

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 16.55 billion

- Market Future Opportunities: USD 14.46 billion

- CAGR from 2024 to 2029 : 42.9%

Market Summary

- The AI procurement intelligence market is fundamentally transforming how organizations manage spend and mitigate supply chain vulnerabilities. This evolution is driven by the strategic need for greater operational efficiency and resilience in a volatile global economy. Advanced platforms leverage AI to move beyond historical analysis, offering predictive insights that empower proactive decision-making.

- Core applications include automated spend analysis, which identifies savings opportunities, and predictive supplier risk management, which ensures continuity. For instance, a global manufacturing firm can use an AI platform to monitor signals of financial distress in a tier-two component supplier.

- Upon receiving a predictive alert, the procurement team preemptively activates a vetted alternative supplier, seamlessly avoiding a production line stoppage that would have otherwise occurred. The integration of generative AI is further democratizing these capabilities, allowing users to query complex datasets using natural language.

- However, the market's potential is tempered by challenges related to data fragmentation and the need for robust change management to foster adoption and trust in AI-driven recommendations.

What will be the Size of the AI Procurement Intelligence Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Procurement Intelligence Market Segmented?

The ai procurement intelligence industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Services

- Deployment

- Cloud-based

- On-premises

- End-user

- Large enterprises

- SMEs

- Government and public sector

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is the core of the AI procurement intelligence market, characterized by cloud-based platforms enabling data-driven decision-making. These solutions focus on hyper-automation and enhanced user experience through intuitive interfaces.

A key trend is the integration of advanced machine learning algorithms and natural language processing to deliver deeper insights. A spend analytics platform can automate spend classification with over 95% accuracy, enabling better sourcing optimization and category management.

Functionalities such as purchase requisition automation and intelligent contract abstraction are becoming standard.

This evolution toward highly intelligent, interconnected systems transforms the procurement function, moving it from a tactical role to a strategic one by leveraging sophisticated supplier data management and invoice data extraction to provide a comprehensive view of enterprise expenditures.

The Software segment was valued at USD 1.62 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Procurement Intelligence Market Demand is Rising in North America Get Free Sample

The geographic landscape of the AI procurement intelligence market is characterized by varied maturity and growth dynamics.

North America stands as the dominant region, accounting for approximately 37% of the market's incremental growth, driven by a high concentration of technology adopters and a corporate culture focused on efficiency.

In this region, AI for direct procurement and AI for indirect procurement are well-established segments. Europe is a close second, with adoption propelled by stringent regulatory requirements.

In contrast, the APAC region is the fastest-growing market, where AI is critical for managing complex manufacturing supply chains and sourcing event automation.

South America and the Middle East and Africa are emerging regions where AI in public sector procurement is gaining traction to improve transparency and efficiency in government spending, with AI-powered demand forecasting and automated invoice processing becoming key investment areas.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises are increasingly focused on comparing AI procurement intelligence platforms to identify solutions that align with strategic objectives beyond simple cost-cutting. The benefits of predictive analytics in sourcing are clear, enabling organizations to anticipate market shifts and secure resources proactively.

- A critical use case is leveraging AI for ESG supply chain compliance, where platforms automate the monitoring of supplier ethics and sustainability metrics, a task that is unmanageable at scale through manual methods. Another significant trend is the impact of AI on tail spend management, where AI-powered negotiation and automation tools can capture value in previously unmanaged categories.

- Organizations that have mastered automating procure-to-pay with AI report processing efficiencies more than double those of their peers still reliant on manual workflows. Key AI-driven supplier risk mitigation strategies include continuous monitoring and predictive alerts, which are essential for business continuity.

- As teams consider the best practices for AI procurement implementation, the emphasis is on integrating AI with existing ERP systems to create a unified data ecosystem. Measuring ROI of AI in procurement involves tracking not just direct savings but also improvements in compliance and risk posture.

- Using AI for supplier discovery and vetting accelerates onboarding, while AI-powered contract lifecycle management benefits include enhanced compliance and obligation tracking. AI tools for strategic sourcing decisions empower category managers to build resilient, cost-effective supply networks.

- Ultimately, the successful deployment of these technologies hinges on addressing the challenges of AI adoption in procurement, including data quality and change management, and understanding the ethical considerations of AI in sourcing to ensure fairness and transparency.

What are the key market drivers leading to the rise in the adoption of AI Procurement Intelligence Industry?

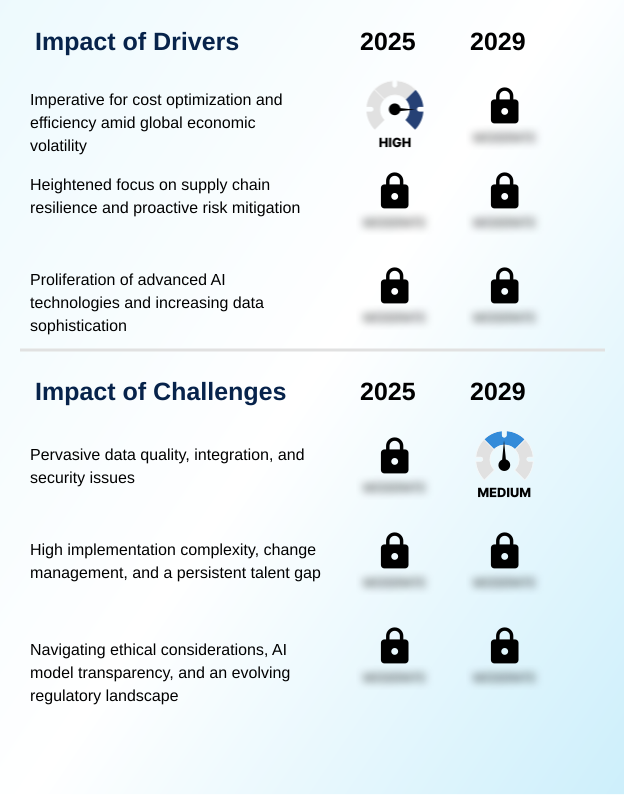

- The imperative for cost optimization and enhanced efficiency, driven by global economic volatility, is a key driver for the market.

- Market growth is fueled by powerful drivers, chief among them the imperative for supply chain resilience. AI-powered platforms provide predictive risk alerts that enable companies to mitigate disruptions 40% faster than traditional methods.

- The need for enhanced spend visibility is another critical driver, with solutions that use prescriptive analytics to uncover savings opportunities and reduce maverick spend by up to 20%.

- This digital procurement transformation is also propelled by the pressure for cost savings, where AI-driven supplier consolidation strategies deliver significant economies of scale. Furthermore, the ability of AI to provide real-time market intelligence empowers procurement teams with superior negotiating leverage.

- These tools enhance supplier performance management and supplier risk scoring, allowing for a more strategic and data-driven approach to managing the supply base.

What are the market trends shaping the AI Procurement Intelligence Industry?

- The proliferation of generative AI and hyper-automation in predictive sourcing is a significant upcoming trend. This evolution is reshaping procurement from a reactive process into a proactive, strategic function.

- Key trends are reshaping the market, led by the integration of generative AI and hyper-automation. The rise of the generative AI assistant and the AI copilot for procurement is making sophisticated analytics accessible through conversational interfaces, with some platforms reducing query times by over 70%.

- This is driving a move toward autonomous procurement, especially for tail spend automation, where AI-powered negotiation can secure an average of 5-8% more savings than manual processes. Another dominant trend is the focus on ethical sourcing, compelling organizations to adopt AI for monitoring supplier compliance.

- This emphasis on predictive sourcing and strategic sourcing, supported by technologies that enable guided buying, is creating more resilient and responsible supply chains. Hyper-automation is accelerating this transformation by connecting disparate systems into a seamless workflow.

What challenges does the AI Procurement Intelligence Industry face during its growth?

- Pervasive data quality, integration, and security issues represent a key challenge affecting the industry's growth trajectory.

- Despite its potential, the market faces significant challenges, primarily centered on data integrity and implementation complexity. The lack of data enrichment and poor data quality can lead to analytical errors in over 25% of AI-driven insights, undermining user trust.

- The 'black box' nature of some models creates a need for explainable AI (XAI) to ensure transparency in decisions related to contract analytics and procure-to-pay optimization. Integrating AI with legacy systems using robotic process automation often proves more complex than anticipated, with implementations lacking proper change management facing a 40% lower adoption rate.

- Furthermore, ensuring ESG compliance monitoring requires deep supplier tier mapping and robust contract lifecycle management, a capability many organizations struggle to support. These challenges hinder the full realization of benefits from technologies like cognitive procurement.

Exclusive Technavio Analysis on Customer Landscape

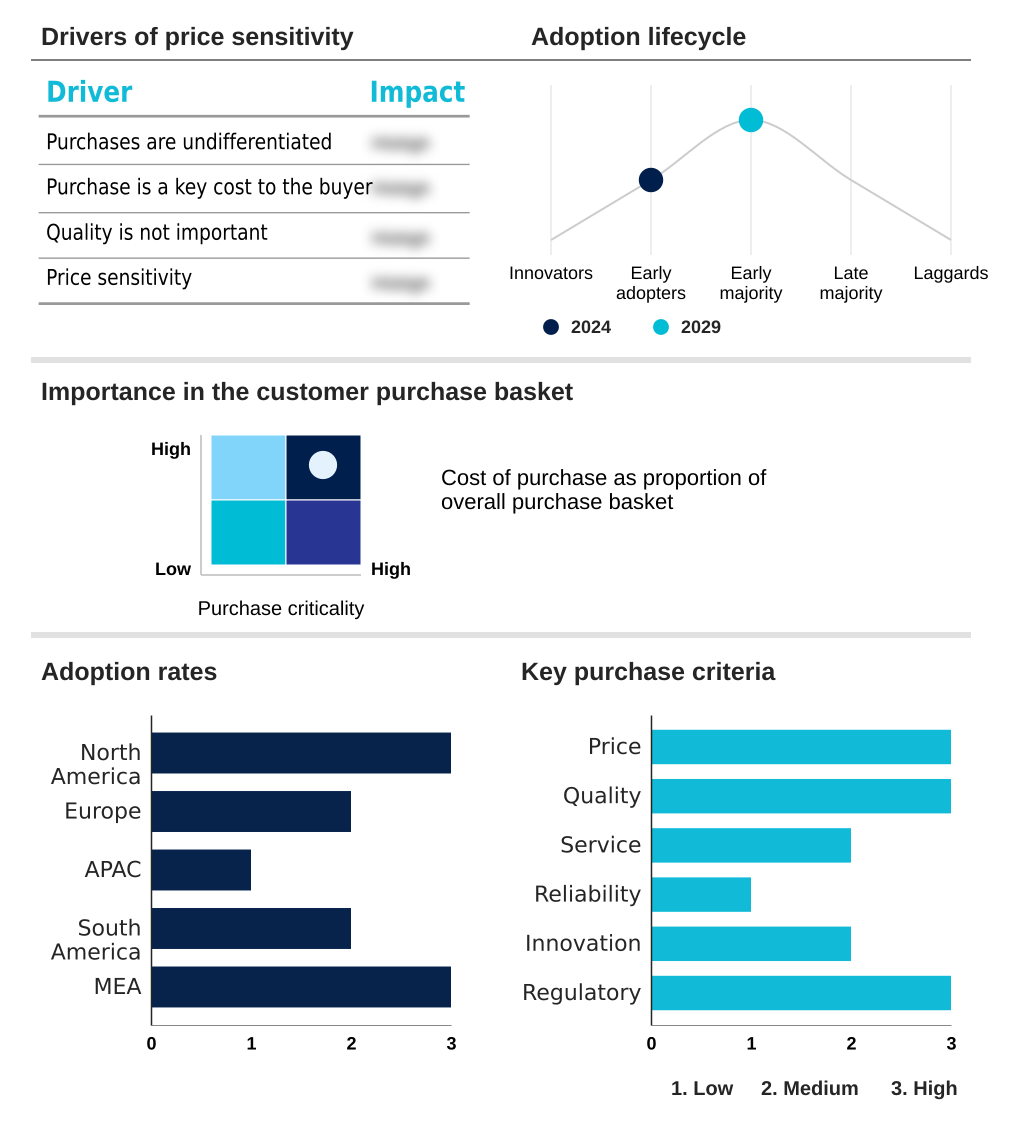

The ai procurement intelligence market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai procurement intelligence market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Procurement Intelligence Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai procurement intelligence market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arkestro Inc - Key offerings leverage community intelligence and aggregated spend data to deliver prescriptive insights, improving spend classification and enterprise fraud detection.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arkestro Inc

- Basware Corp.

- Coupa Software Inc.

- EcoVadis

- GEP

- Globality Inc

- Icertis Inc.

- Ivalua Inc.

- JAGGAER LLC

- Keelvar

- Microsoft Corp.

- Oracle Corp.

- Pactum AI Inc

- SAP SE

- Scoutbee

- Sievo

- TealBook

- Zycus Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai procurement intelligence market

- In September, 2024, Oracle Corp. announces the acquisition of a specialized AI firm focused on ESG supply chain compliance, with plans to integrate its technology into the Oracle Fusion Cloud SCM suite to enhance responsible sourcing capabilities.

- In November, 2024, Coupa Software Inc. launches an autonomous negotiation module for tail spend, utilizing generative AI to conduct parallel negotiations with suppliers, projecting an efficiency gain in sourcing cycles by up to 30% for targeted categories.

- In February, 2025, GEP partners with a premier climate data analytics provider to embed real-time carbon footprint tracking and reporting directly into its GEP SMART procurement platform, addressing growing client demand for sustainability metrics.

- In April, 2025, SAP SE unveils an advanced compliance automation feature for its Ariba platform, specifically engineered to help European enterprises meet stringent supply chain due diligence regulations by using AI to continuously monitor sub-tier supplier risk.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Procurement Intelligence Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 283 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 42.9% |

| Market growth 2025-2029 | USD 14464.1 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 34.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, China, Japan, India, Australia, South Korea, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI procurement intelligence market is undergoing a strategic transformation, moving beyond tactical automation to become a core engine for enterprise value. This shift is driven by advancements in machine learning algorithms and natural language processing, which enable sophisticated spend classification, predictive sourcing, and cognitive procurement.

- Platforms now offer robust supplier performance management and supplier risk scoring, which are crucial for building resilient supply chains. The integration of robotic process automation for tasks like automated invoice processing within a broader procure-to-pay optimization strategy is standard.

- Boardroom decisions are increasingly influenced by AI-driven insights, particularly for ESG compliance, where AI tools for strategic sourcing and category management help align purchasing with corporate sustainability goals. Effective spend visibility, achieved through data enrichment and prescriptive analytics, has enabled leading firms to reduce maverick spend by over 15%.

- The evolution includes guided buying experiences, ai-powered negotiation for tail spend automation, and enhanced supplier relationship management, with a focus on comprehensive contract analytics and efficient supplier discovery to drive competitive advantage.

What are the Key Data Covered in this AI Procurement Intelligence Market Research and Growth Report?

-

What is the expected growth of the AI Procurement Intelligence Market between 2025 and 2029?

-

USD 14.46 billion, at a CAGR of 42.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Services), Deployment (Cloud-based, On-premises), End-user (Large enterprises, SMEs, Government and public sector) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Imperative for cost optimization and efficiency amid global economic volatility, Pervasive data quality, integration, and security issues

-

-

Who are the major players in the AI Procurement Intelligence Market?

-

Arkestro Inc, Basware Corp., Coupa Software Inc., EcoVadis, GEP, Globality Inc, Icertis Inc., Ivalua Inc., JAGGAER LLC, Keelvar, Microsoft Corp., Oracle Corp., Pactum AI Inc, SAP SE, Scoutbee, Sievo, TealBook and Zycus Inc.

-

Market Research Insights

- The AI procurement intelligence market is defined by a dynamic interplay of technological innovation and pressing business imperatives. A strategic shift from pure cost reduction to a balanced focus on supply chain resilience is compelling organizations to adopt predictive analytics, with platforms demonstrating up to a 40% faster identification of potential disruptions.

- The accessibility of generative AI is democratizing data analysis, enabling procurement teams to achieve an 80% reduction in time spent on routine data queries. This digital procurement transformation is not uniform; while large enterprises were early adopters, cloud-based models have lowered entry barriers, leading to a 25% increase in adoption among mid-sized firms over the past two years.

- This evolution highlights a move toward more agile, data-centric procurement functions capable of navigating economic uncertainty and leveraging real-time market intelligence.

We can help! Our analysts can customize this ai procurement intelligence market research report to meet your requirements.

RIA -

RIA -