Industrial AI Software Market Size 2026-2030

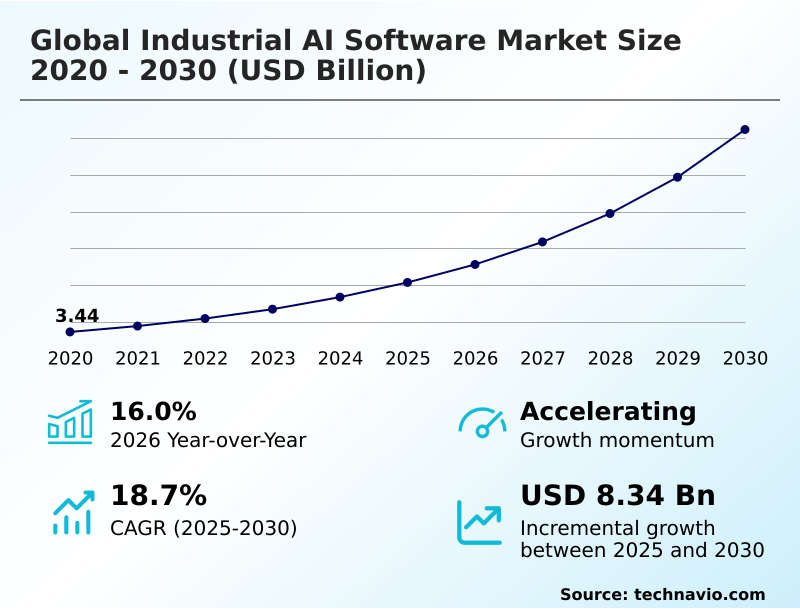

The industrial ai software market size is valued to increase by USD 8.34 billion, at a CAGR of 18.7% from 2025 to 2030. Shift toward industrially trained intelligence and domain specific foundation will drive the industrial ai software market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 33.6% growth during the forecast period.

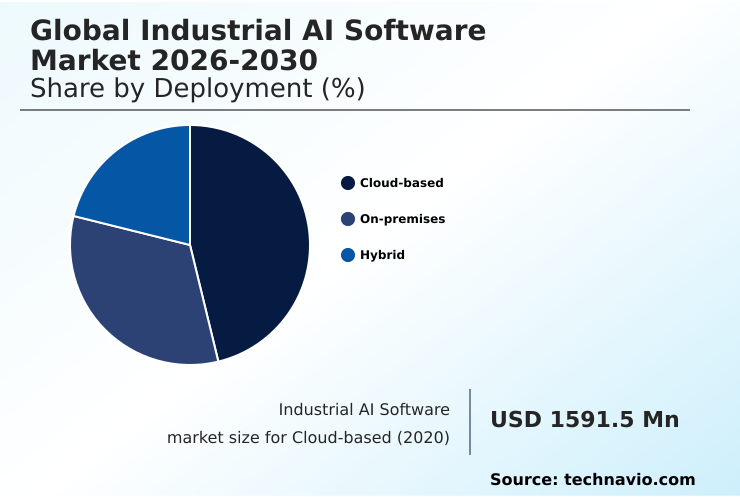

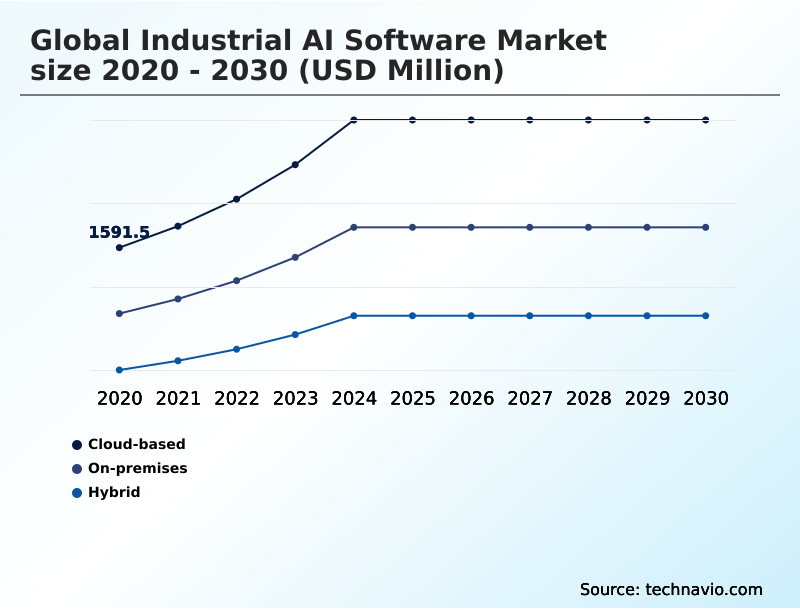

- By Deployment - Cloud-based segment was valued at USD 2.49 billion in 2024

- By Industry Application - Manufacturing segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 11.03 billion

- Market Future Opportunities: USD 8.34 billion

- CAGR from 2025 to 2030 : 18.7%

Market Summary

- The industrial AI software market is undergoing a structural transformation, moving from localized pilot programs to the widespread deployment of autonomous and perception-driven architectures. This expansion is driven by the escalating demand for high-fidelity predictive maintenance, real-time supply chain optimization, and the integration of physical AI.

- As organizations strive for higher operational efficiency, the role of software-defined automation has become paramount. For instance, a manufacturer facing supply chain volatility can utilize predictive analytics to model multiple what-if scenarios, identifying potential bottlenecks before they materialize and optimizing raw material usage in real-time. This capability is vital for maintaining profitability amid sudden shifts in trade policy.

- The challenge of integrating these advanced tools with legacy systems persists, but the convergence of hardware-aware software optimization and sovereign data infrastructure ensures that industrial AI remains a resilient pillar of the modern production economy.

What will be the Size of the Industrial AI Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Industrial AI Software Market Segmented?

The industrial ai software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Industry application

- Manufacturing

- Energy and utilities

- Healthcare and pharmaceuticals

- Chemicals and materials

- Others

- Technology

- Machine learning

- Computer vision

- Natural language processing

- Robotic process automation

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The cloud-based segment is pivotal for the industrial AI software market, offering scalability and facilitating cross-regional collaboration through advanced cognitive computing tools.

This model supports the massive processing power needed for training complex neural networks and managing petabytes of sensor data, enabling rapid deployment of software updates without local IT intervention.

This approach is instrumental in industrial data operations (DataOps), aggregating data from multiple global sites to provide a unified view of operational efficiency and supply chain resilience.

As data sovereignty concerns are met with regionalized data centers, reliance on cloud-based deployment deepens.

The integration of a unified runtime adapter can streamline device management, improving execution performance for high-performance computing in distributed environments, showcasing how AI for operational efficiency is realized through software-defined automation, MLOps, and agentic AI systems.

The Cloud-based segment was valued at USD 2.49 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 33.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Industrial AI Software Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dynamic, with APAC accounting for 33.6% of the market's incremental growth, fueled by government-led modernization initiatives. This region shows strong adoption of computer vision for quality inspection and high-speed robotics control.

North America leverages its technology pioneers for full-scale enterprise deployments, while Europe focuses on data sovereignty and decarbonization, driving demand for explainable AI (XAI) and hybrid cloud orchestration.

South America is adopting cloud-native AI solutions to leapfrog legacy infrastructure, particularly in mining and agriculture.

Across these regions, the focus is on AI for supply chain resilience and industrial data analytics platforms, leading to an estimated 15% reduction in energy consumption in optimized facilities.

This global activity highlights the varied adoption of physical AI interaction and smart factory technology stacks.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global industrial AI software market 2026-2030 is marked by a focus on tangible outcomes, with organizations actively exploring how to use AI to reduce unplanned downtime and seeking the best AI software for manufacturing process optimization. The benefits of digital twins in production are becoming increasingly clear, allowing for comprehensive virtual testing that de-risks capital-intensive projects.

- In practice, computer vision for automated quality inspection is setting new benchmarks for precision, while the question of how AI improves supply chain visibility is being answered through real-time tracking and predictive logistics.

- Advanced firms are implementing federated learning in industry to train models without compromising data privacy, showcasing the critical role of edge computing in industrial AI for low-latency decision-making. AI copilots for industrial workforce training are bridging skill gaps, while predictive maintenance for heavy machinery remains a cornerstone application.

- Furthermore, generative design for lightweighting components and AI-driven energy consumption monitoring are addressing sustainability mandates. Securing industrial control systems with AI is a top priority, as is using natural language processing for maintenance logs to unlock unstructured data. Robotic process automation in supply chains is streamlining workflows, while managing data sovereignty in cloud AI has become a key strategic consideration.

- The challenges of integrating AI with legacy systems are being met with new middleware, and AI software for asset performance management is crucial for maximizing asset lifecycles. Companies optimizing chemical synthesis with machine learning are reporting efficiency gains that are nearly double those of traditional methods.

- Finally, reinforcement learning for real-time control and agentic AI for autonomous warehouse operations represent the frontier of industrial automation.

What are the key market drivers leading to the rise in the adoption of Industrial AI Software Industry?

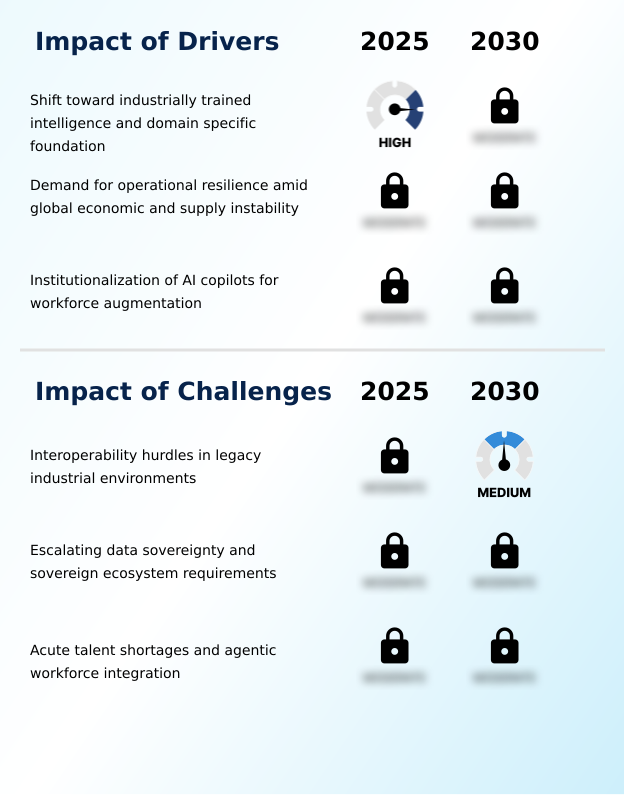

- A key market driver is the strategic shift toward industrially trained intelligence and domain-specific foundational models designed for complex operational environments.

- Market growth is fueled by the strategic transition toward industrially trained intelligence and domain-specific foundational models, moving beyond generic platforms. This allows for precise, context-aware recommendations that a standard large language model cannot offer.

- Another significant driver is the need for operational resilience amid global instability, where Overall Equipment Effectiveness (OEE) and asset performance management (APM) platforms with predictive analytics improve supply chain forecast accuracy by over 25%.

- The institutionalization of AI copilots for workforce augmentation addresses labor shortages by enabling junior employees to perform at expert levels, accelerating onboarding by as much as 50%.

- These drivers underscore the move toward an orchestrated system of human expertise and digital workers, transforming the shop floor into an intelligent, adaptive ecosystem through advanced automation in manufacturing and AI-powered drug discovery.

What are the market trends shaping the Industrial AI Software Industry?

- The convergence of the industrial metaverse with real-time digital twins is an emerging market trend. This integration creates immersive virtual environments for advanced operational management and testing.

- Key trends are reshaping industrial operations, led by the convergence of the industrial metaverse with high-fidelity, real-time digital twins. This approach, leveraging physics-informed neural networks and closed-loop optimization, allows companies to simulate facility upgrades, reducing physical prototyping costs by up to 40%.

- Concurrently, a shift toward AI-driven energy management and sustainability compels manufacturers to adopt AI for energy management, with some plants lowering their carbon footprint by 15% through predictive consumption models. The rise of sovereign industrial clouds, driven by data privacy regulations, is creating demand for hybrid solutions that orchestrate workloads across edge devices and private data centers.

- This trend supports federated learning, enabling collaborative model training without sharing raw data, a crucial aspect of industrial AI deployment models and agentic process automation.

What challenges does the Industrial AI Software Industry face during its growth?

- A key challenge affecting industry growth is the presence of interoperability hurdles within legacy industrial environments, which complicates modern data integration.

- The market faces significant challenges, primarily the lack of interoperability within legacy industrial environments. The integration of modern IT/OT convergence strategies with older programmable logic controllers (PLC) and supervisory control and data acquisition (SCADA) systems is complex, with the absence of standardized protocols inflating project timelines by over 60%.

- Escalating data sovereignty and sovereign ecosystem requirements complicate the business models of multinational providers, who must now create costly region-specific deployments to comply with varied legal frameworks. Furthermore, an acute shortage of specialized talent proficient in data monetization and agentic systems hinders adoption.

- This talent deficit results in a 20% lower ROI on AI investments compared to initiatives with properly skilled teams, impacting the deployment of industrial AI for logistics and semiconductor fabrication AI.

Exclusive Technavio Analysis on Customer Landscape

The industrial ai software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial ai software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Industrial AI Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, industrial ai software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Delivers industrial AI software integrating advanced analytics and machine learning to optimize processes, enable predictive maintenance, and drive operational efficiency in complex industrial settings.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Acerta Analytics Solutions Inc.

- Augury Inc.

- AVEVA Group Ltd.

- C3.ai Inc.

- Emerson Electric Co.

- GE Vernova Inc.

- Hitachi Ltd.

- Honeywell International Inc.

- IBM Corp.

- IFS

- Oracle Corp.

- PTC Inc.

- Quartic.ai Inc.

- Rockwell Automation Inc.

- SAP SE

- Schneider Electric SE

- Siemens AG

- Uptake Technologies Inc.

- Wizata S.A.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial ai software market

- In May 2025, Oracle announced that NVIDIA AI Enterprise, a cloud-native software suite for data science and production-ready AI, became accessible on Oracle Cloud Infrastructure to support enterprise-scale industrial modeling.

- In April 2025, UiPath Inc. launched its Platform for agentic automation, unifying AI agents, software robots, and human interaction into a scalable platform to execute complex business processes autonomously.

- In March 2025, Oracle Corp. expanded its portfolio by integrating new agent-driven capabilities designed to automate investigations and surface contextual insights for complex compliance and operational tasks.

- In January 2025, Siemens AG launched its Digital Twin Composer software on the Xcelerator Marketplace, a platform designed to power the industrial metaverse at scale by fusing real-world engineering data with immersive 3D scenes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial AI Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 314 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.7% |

| Market growth 2026-2030 | USD 8339.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 16.0% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The industrial AI software market is shifting from probabilistic models to deterministic, software-defined automation architectures. This transition prioritizes repeatability and traceability, especially in mission-critical sectors. Key advancements in predictive maintenance algorithms and autonomous process control are enabling a new class of agentic AI systems.

- The integration of computer vision quality inspection and digital twin simulation is becoming standard, powered by the industrial internet of things (IIoT). The rise of sovereign cloud infrastructure is a critical trend influencing boardroom decisions on IT investment and compliance strategy, as companies balance performance with data governance.

- This focus on secure, high-performance platforms is enabling firms to achieve a 30% reduction in new product design cycles through generative design software and reinforcement learning models.

- The market's evolution is defined by a push toward human-in-the-loop oversight, edge computing gateways, and federated learning architecture to create resilient, intelligent manufacturing ecosystems that leverage high-fidelity predictive analytics, natural language processing (NLP), and robotic process automation (RPA) for comprehensive optimization.

What are the Key Data Covered in this Industrial AI Software Market Research and Growth Report?

-

What is the expected growth of the Industrial AI Software Market between 2026 and 2030?

-

USD 8.34 billion, at a CAGR of 18.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, On-premises, and Hybrid), Industry Application (Manufacturing, Energy and utilities, Healthcare and pharmaceuticals, Chemicals and materials, and Others), Technology (Machine learning, Computer vision, Natural language processing, and Robotic process automation) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Shift toward industrially trained intelligence and domain specific foundation, Interoperability hurdles in legacy industrial environments

-

-

Who are the major players in the Industrial AI Software Market?

-

ABB Ltd., Acerta Analytics Solutions Inc., Augury Inc., AVEVA Group Ltd., C3.ai Inc., Emerson Electric Co., GE Vernova Inc., Hitachi Ltd., Honeywell International Inc., IBM Corp., IFS, Oracle Corp., PTC Inc., Quartic.ai Inc., Rockwell Automation Inc., SAP SE, Schneider Electric SE, Siemens AG, Uptake Technologies Inc. and Wizata S.A.

-

Market Research Insights

- Market dynamics are defined by a push for operational resilience and the institutionalization of AI to augment the industrial workforce. The adoption of AI for predictive asset health and intelligent virtual assistants is accelerating, with firms reporting that predictive analytics improve supply chain forecast accuracy by over 25%.

- This shift toward AI-driven sustainability solutions and AI in chemical process optimization allows businesses to manage risks and resource allocation in real-time. The ability to act on detected changes provides a significant competitive advantage.

- As decision-making shifts toward agility, implementing AI-powered quality control and autonomous industrial workflows is critical, enabling junior employees to perform at expert levels and reducing onboarding time by as much as 50%, securing long-term viability in volatile conditions.

We can help! Our analysts can customize this industrial ai software market research report to meet your requirements.

RIA -

RIA -