Ai Governance Tools Market Size and Growth Forecast 2026-2030

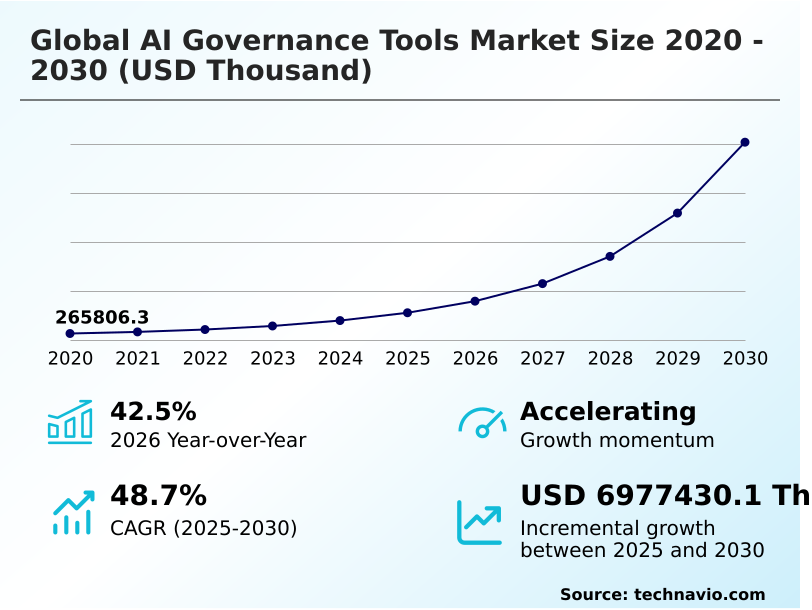

The Ai Governance Tools Market size was valued at USD 1.11 billion in 2025 growing at a CAGR of 48.7% during the forecast period 2026-2030.

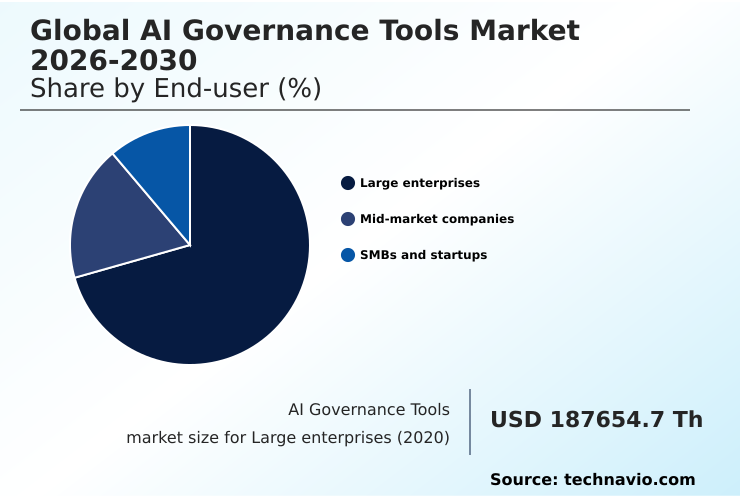

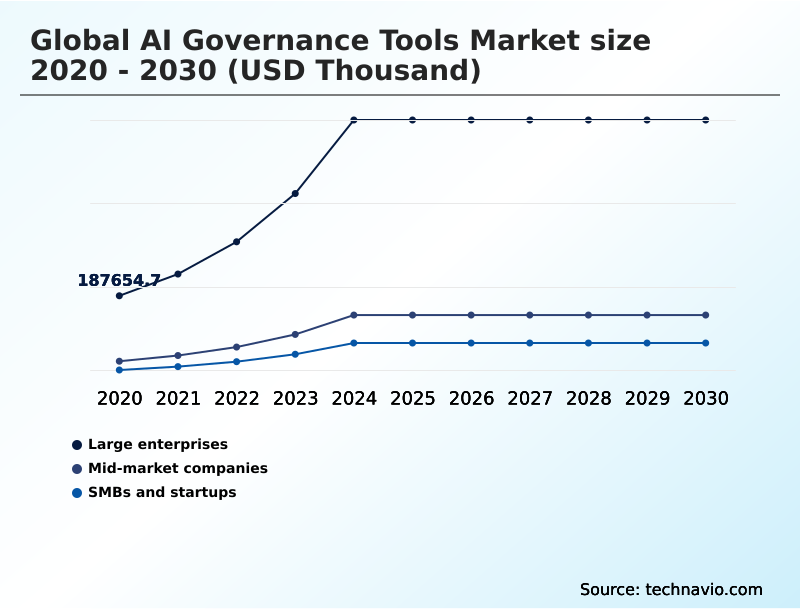

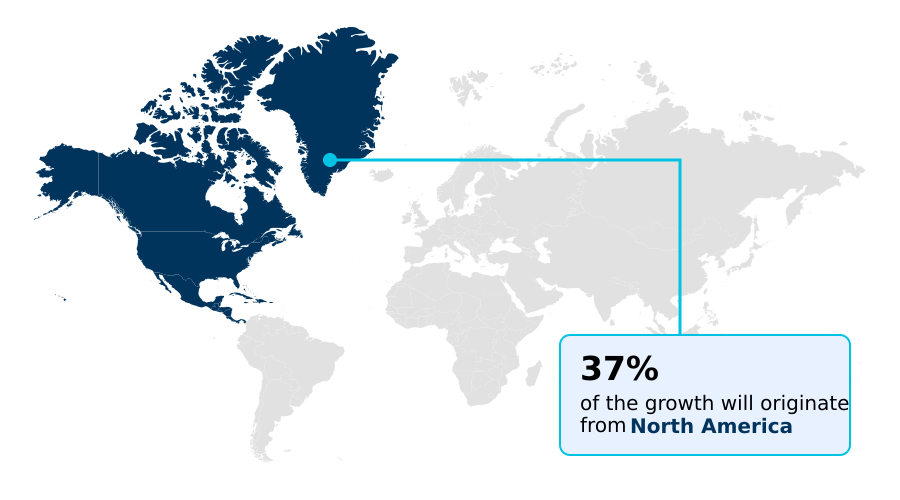

North America accounts for 37.4% of incremental growth during the forecast period. The Large enterprises segment by End-user was valued at USD 561.65 million in 2024, while the Risk and compliance monitoring segment holds the largest revenue share by Type.

The market is projected to grow by from 2020 to 2030, with USD 6.98 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Ai Governance Tools Market Overview

The AI governance tools market is defined by a critical shift from experimental AI to its deployment in core business functions, making formal AI governance frameworks essential for operational resilience. This is particularly evident in North America, which is projected to contribute 37.4% of the market's incremental growth, driven by early and widespread adoption. The focus for enterprises is translating abstract responsible AI principles into enforceable controls using specialized AI risk management tools. A typical scenario involves a financial services firm implementing a comprehensive AI model inventory to catalog hundreds of algorithmic trading models. By deploying a centralized AI governance platform with capabilities for continuous performance monitoring and automated model validation, the firm can address model drift detection in real-time. This provides the necessary AI audit trails to comply with SEC mandates and ensures robust model risk management through explainable AI (XAI) and proactive bias detection and fairness auditing, which have become non-negotiable for maintaining regulatory compliance and public trust.

Drivers, Trends, and Challenges in the Ai Governance Tools Market

The practical application of AI governance is highly sector-specific, requiring tailored solutions. For example, AI governance tools for financial services concentrate on bias detection in credit scoring models and managing model risk with AI governance in high-frequency trading. Concurrently, AI governance tools for healthcare are essential for validating diagnostic models and ensuring patient data privacy.

The debate over open source vs commercial AI governance often revolves around the total cost of implementing AI governance tools, as commercial platforms offer robust support for implementing AI governance in MLOps and provide templates for compliance with the EU AI Act.

The rise of generative AI has made generative AI governance and security paramount, focusing on risks such as data poisoning and requiring an extensive AI audit trail for regulatory reporting. In high-stakes fields, such as with AI governance tools for autonomous vehicles, the emphasis is on best practices for AI model validation and securing AI models from adversarial attacks.

Integrating an AI governance platform with GRC systems is now a standard practice for comprehensive risk oversight and is crucial for AI governance tools for regulatory compliance.

Capabilities like automated monitoring for AI model drift and explainability tools for black box models are now standard features, essential for functions ranging from AI governance tools for supply chain to ensuring fairness in AI hiring tools.

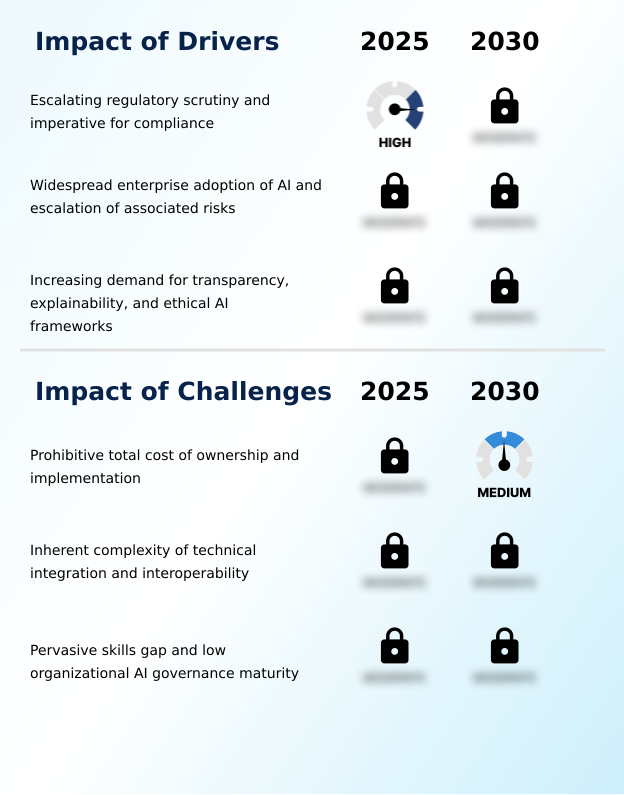

Primary Growth Driver: The primary market driver is the escalating regulatory scrutiny and the corresponding imperative for organizations to achieve and demonstrate compliance with emerging AI-specific legal frameworks.

Escalating regulatory scrutiny, exemplified by frameworks like the EU AI Act and Brazil's LGPD, stands as the foremost market driver, making AI compliance software an operational necessity.

This legal imperative compels organizations to adopt tools capable of automated regulatory reporting and AI impact assessment to mitigate the risk of severe financial penalties.

A second major driver is the widespread enterprise adoption of AI, which introduces a new spectrum of complex operational risks.

As organizations deploy AI at scale, the reliance on AI governance platforms for comprehensive model risk management and data governance for AI becomes essential.

With North America accounting for 37.4% of the market's incremental growth, the demand for sophisticated AI risk management tools to safeguard brand reputation and maintain stakeholder trust is a powerful and enduring catalyst.

Emerging Market Trend: A key market trend is the rise of explainable AI (XAI) and model interpretability as a fundamental governance requirement. This shift reflects growing demands for transparency in automated decision-making from regulators and stakeholders.

A primary market trend is the strategic convergence of AI-specific functions with broader Enterprise Risk Management (ERM) frameworks, signaling a move beyond siloed, standalone tools. The demand for explainable AI (XAI) and robust model interpretability is now a core compliance requirement, driven by regulations such as the EU AI Act that include a right to explanation.

This is compelling investment in advanced explainability and transparency tools. Another key trend is the proliferation of automated solutions for continuous performance monitoring and full model lifecycle management.

With the APAC region projected for a 51.5% CAGR, the need for scalable AI model monitoring tools to govern vast and diverse model ecosystems is becoming a critical operational necessity, reflecting a market-wide pivot to automated, real-time oversight.

Key Industry Challenge: A key market challenge is the prohibitive total cost of ownership, which includes not only high software fees but also the extensive expenses of complex technical integration and implementation.

A significant market restraint is the high total cost of ownership, which includes not only steep licensing fees but also the resource-intensive process of technical integration. The inherent complexity of integrating AI governance tools with heterogeneous IT and MLOps ecosystems often requires specialized engineering expertise, which deters many potential adopters.

Another critical challenge is the pervasive skills gap; a global shortage of professionals with the multidisciplinary expertise required for effective machine learning governance persists. This widespread lack of organizational AI governance maturity, particularly among smaller companies, limits the addressable market largely to well-resourced enterprises.

These factors make it difficult for many organizations to justify the substantial investment in a comprehensive AI governance framework, thereby impeding broader market penetration.

Explore Full Market Dynamics Analysis Request Free Sample

Ai Governance Tools Market Segmentation

The ai governance tools industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

End-user Segment Analysis

The large enterprises segment is estimated to witness significant growth during the forecast period.

Large enterprises represent the most mature and dominant end-user segment, driven by the operational necessity of managing complex, large-scale artificial intelligence deployments across multiple jurisdictions.

For these organizations, adopting robust AI risk management tools is a fundamental component of enterprise risk management, not an optional enhancement.

Their procurement decisions prioritize highly scalable, secure platforms that offer comprehensive model risk management and can generate immutable AI audit trails for regulatory reporting.

Given their global footprint, these firms require enterprise AI governance solutions that seamlessly integrate into existing GRC frameworks to enforce AI policy management consistently.

The significant budgets allocated to technology and risk mitigation enable investment in premium, full-featured AI compliance software suites that provide capabilities like bias detection and fairness auditing, solidifying their position as the primary revenue contributor.

The Large enterprises segment was valued at USD 561.65 million in 2024 and showed a gradual increase during the forecast period.

Ai Governance Tools Market by Region: North America Leads with 37.4% Growth Share

North America is estimated to contribute 37.4% to the growth of the global market during the forecast period.

The geographic landscape is led by North America, accounting for 37.4% of incremental growth, where a mature market and a proactive regulatory environment compel the use of advanced AI governance platforms.

Europe, contributing 25.85%, sees its growth catalyzed by the EU AI Act, which mandates stringent regulatory compliance frameworks and detailed AI impact assessments.

In APAC, which accounts for 22.88% of growth, the focus is on enabling cross-border digital trade through harmonized standards that promote tools for federated learning governance and privacy-enhancing technologies (PETs).

While regions like South America and the Middle East and Africa are nascent, their growth is accelerating due to data privacy laws like Brazil's LGPD, which require explainability and transparency tools.

This regional diversity necessitates hybrid cloud AI governance solutions adaptable to varied legal and operational contexts.

Customer Landscape Analysis for the Ai Governance Tools Market

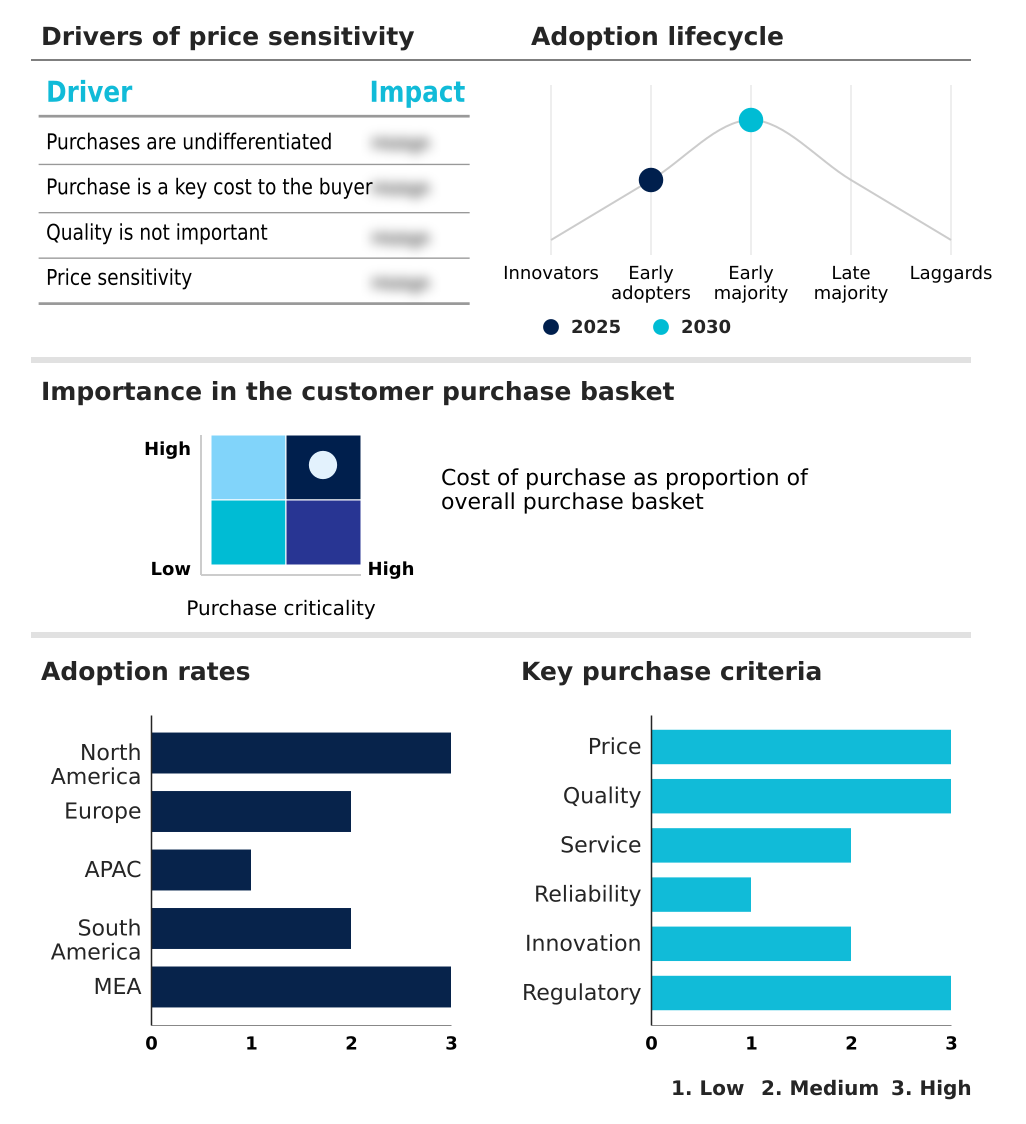

The ai governance tools market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai governance tools market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Ai Governance Tools Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the ai governance tools market industry.

Alteryx Inc. - The portfolio integrates analytics, process automation, and AI governance, offering a unified platform for end-to-end data intelligence and operational control in enterprise environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alteryx Inc.

- Amazon Web Services Inc.

- ARTHUR

- BigID Inc.

- Collibra

- Credo AI

- Dataiku Inc.

- DataRobot Inc.

- Fair Isaac Corp.

- Fiddler AI

- Google LLC

- H2O.ai Inc.

- IBM Corp.

- Informatica Inc.

- Microsoft Corp.

- Monitaur Inc.

- OneTrust LLC

- SAS Institute Inc.

- Seldon Technologies

- Trust Arc Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Ai Governance Tools Market

- In January 2025, Microsoft Corp. announced significant innovations for its Purview platform, enhancing data security and governance with features like Data Loss Prevention policies to safely accelerate AI transformation.

- In February 2025, IBM Corp. formed a strategic partnership with telecommunications group Etisalat to deploy enterprise-grade agentic AI solutions tailored for governance and regulatory compliance within the telecom sector.

- In March 2025, Microsoft Corp. launched its new AI Governance Toolkit for Azure OpenAI service users, providing a comprehensive suite of tools for responsible AI deployment, including integrated audit trails and risk management frameworks.

- In April 2025, Brazil's National Data Protection Authority (ANPD) published binding technical regulations under the LGPD, mandating the use of AI governance tools for algorithmic impact assessments and model explainability.

Research Analyst Overview: Ai Governance Tools Market

The market is fundamentally transitioning from reactive, post-deployment auditing to proactive, lifecycle-embedded control systems. The introduction of regulations such as the EU AI Act has elevated AI policy management to a boardroom-level concern, directly influencing product strategy and market access decisions. Organizations are now mandated to demonstrate compliance through detailed AI audit trails and automated regulatory reporting.

The significant share of the risk and compliance monitoring segment, which accounts for a substantial portion of the market, underscores this compliance-driven reality. At the operational level, this mandates the integration of bias detection and fairness auditing and explainability and transparency tools directly into MLOps pipelines.

A key technical focus is on model drift detection, where continuous performance monitoring is essential. Consequently, boardroom budget allocations increasingly weigh the upfront cost of deploying comprehensive AI governance platforms against the severe financial and reputational risks of non-compliance, making robust model risk management a cornerstone of modern corporate strategy.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ai Governance Tools Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 48.7% |

| Market growth 2026-2030 | USD 6977430.1 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 42.5% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, UAE, Israel, Saudi Arabia, South Africa and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Ai Governance Tools Market: Key Questions Answered in This Report

-

What is the expected growth of the Ai Governance Tools Market between 2026 and 2030?

-

The Ai Governance Tools Market is expected to grow by USD 6.98 billion during 2026-2030, registering a CAGR of 48.7%. Year-over-year growth in 2026 is estimated at 42.5%%. This acceleration is shaped by escalating regulatory scrutiny and imperative for compliance, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Large enterprises, Mid-market companies, and SMBs and startups), Type (Risk and compliance monitoring, Model lifecycle management, Bias detection and fairness auditing, and Explainability and transparency tools), Deployment (Cloud-native SaaS, Hybrid or multi-cloud, and On-premises integration) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Large enterprises segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 37.4% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, UK, Germany, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, UAE, Israel, Saudi Arabia, South Africa and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is escalating regulatory scrutiny and imperative for compliance, which is accelerating investment and industry demand. The main challenge is prohibitive total cost of ownership and implementation, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Ai Governance Tools Market?

-

Key vendors include Alteryx Inc., Amazon Web Services Inc., ARTHUR, BigID Inc., Collibra, Credo AI, Dataiku Inc., DataRobot Inc., Fair Isaac Corp., Fiddler AI, Google LLC, H2O.ai Inc., IBM Corp., Informatica Inc., Microsoft Corp., Monitaur Inc., OneTrust LLC, SAS Institute Inc., Seldon Technologies and Trust Arc Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Ai Governance Tools Market Research Insights

Market dynamics are shaped by the critical need for machine learning governance as organizations scale AI from isolated projects to enterprise-wide systems. The growing adoption of generative AI governance for large language models amplifies this demand. A significant portion of this is driven by compliance with frameworks like the EU AI Act, which mandates stringent AI risk and compliance oversight.

For instance, a healthcare provider using a diagnostic algorithm must deploy AI fairness metrics and AI transparency solutions to prove non-discriminatory outcomes, a process managed through a comprehensive enterprise AI governance platform. This contrasts with the large enterprise segment, which leads adoption, and the SMB segment, where the focus is on more accessible cloud AI governance tools.

The market is evolving beyond simple monitoring to holistic AI value alignment, ensuring that automated systems operate safely and ethically.

We can help! Our analysts can customize this ai governance tools market research report to meet your requirements.

RIA -

RIA -