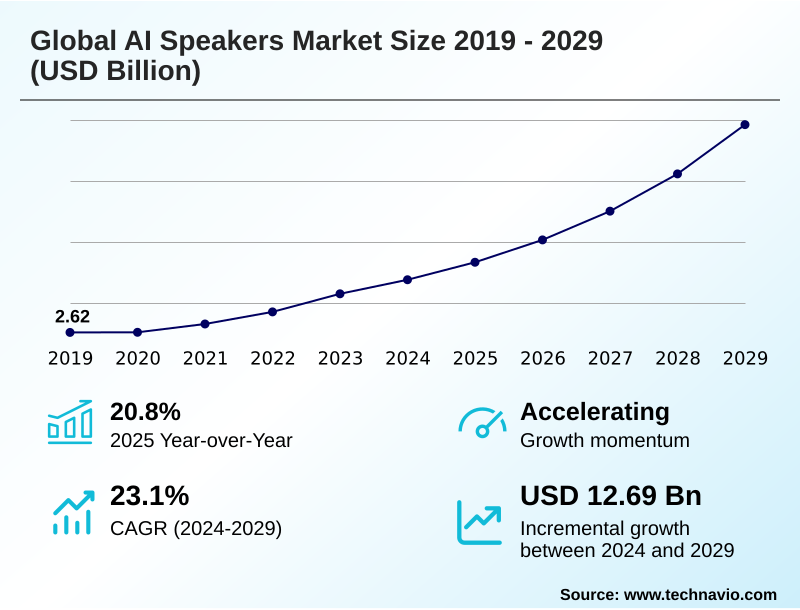

AI Speakers Market Size 2025-2029

The ai speakers market size is valued to increase by USD 12.69 billion, at a CAGR of 23.1% from 2024 to 2029. Integration of advanced generative AI and large language models will drive the ai speakers market.

Major Market Trends & Insights

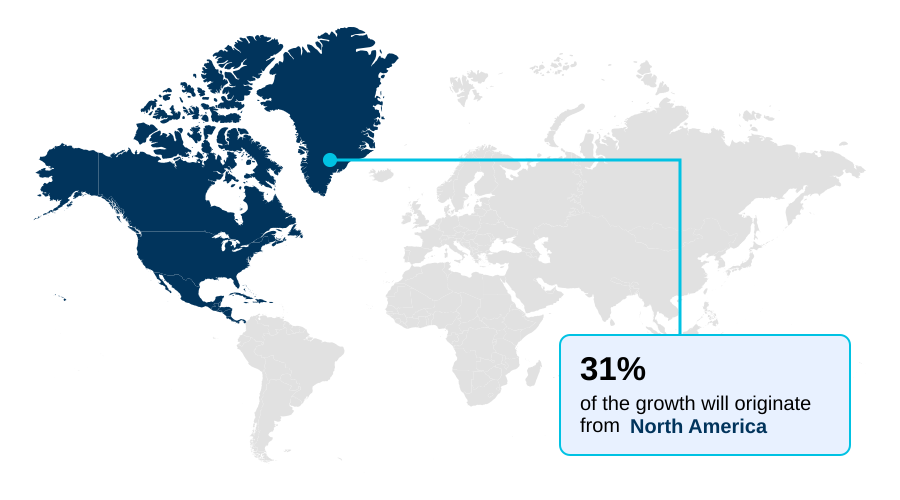

- North America dominated the market and accounted for a 31.4% growth during the forecast period.

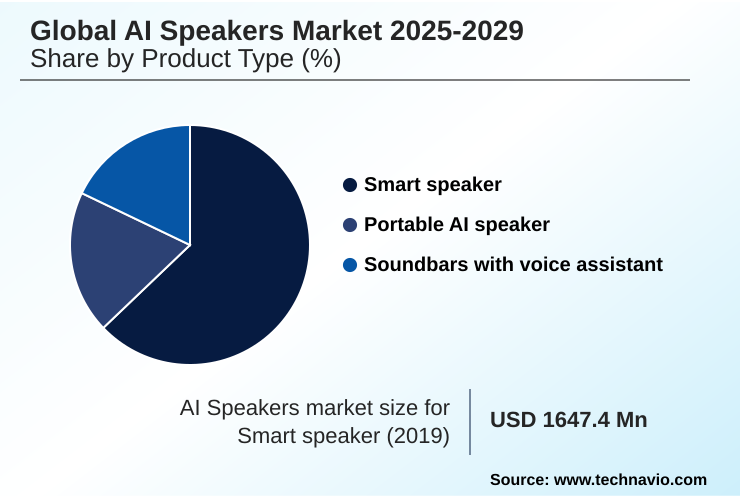

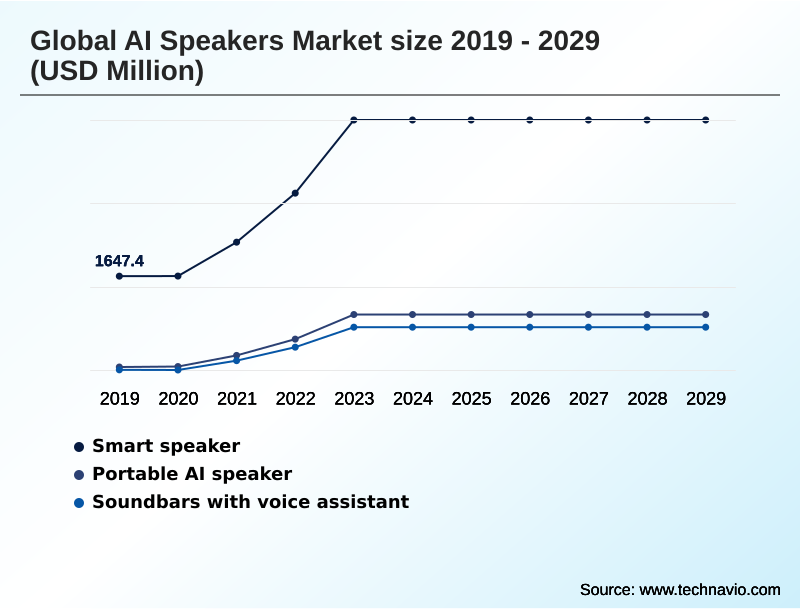

- By Product Type - Smart speaker segment was valued at USD 3.61 billion in 2023

- By Component - Hardware segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 17.00 billion

- Market Future Opportunities: USD 12.69 billion

- CAGR from 2024 to 2029 : 23.1%

Market Summary

- The AI speakers market is transitioning from novelty devices to essential components of the connected home. This evolution is propelled by the integration of sophisticated large language models and a focus on creating a seamless ambient computing ecosystem.

- As these devices become more intelligent, they move beyond simple music playback to serve as a central hub for controlling a diverse range of IoT devices. A key trend is the push for on-device AI processing to address privacy concerns and improve response times.

- However, the market faces challenges related to saturation in developed regions and the need for compelling innovation to spur upgrades. For example, in a commercial setting, a hospitality chain can deploy AI speakers to streamline guest services, from room-service ordering to controlling room ambiance, thereby improving operational efficiency without major infrastructure changes.

- The success of AI speakers hinges on balancing advanced, proactive assistance with robust security and a trustworthy user experience, making them indispensable in both residential and commercial environments.

What will be the Size of the AI Speakers Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Speakers Market Segmented?

The ai speakers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product type

- Smart speaker

- Portable AI speaker

- Soundbars with voice assistant

- Component

- Hardware

- Software

- Services

- Connectivity

- Wi-Fi

- Bluetooth

- Cellular or LTE

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Product Type Insights

The smart speaker segment is estimated to witness significant growth during the forecast period.

The smart speaker segment is evolving from a functional device for music playback into a sophisticated home automation hub.

This transformation is driven by the integration of advanced computational audio technology and on-device AI processing, which ensures a low-latency response for commands.

The adoption of the Matter connectivity standard is critical, allowing these devices to act as a centralized command center for an increasingly interoperable smart home.

This enhancement, which includes functionality as thread border routers, solidifies the device's role in the ambient computing ecosystem.

For instance, integrated smart energy management routines now enable automated cost savings, with some systems demonstrating a 15% reduction in off-peak energy consumption.

This shift toward practical utility, powered by advanced acoustic engineering and seamless ecosystem integration, defines the segment's current trajectory, moving beyond commoditized hardware functions toward delivering tangible value through software-defined features and voice-activated user interface.

The Smart speaker segment was valued at USD 3.61 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 31.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Speakers Market Demand is Rising in North America Get Free Sample

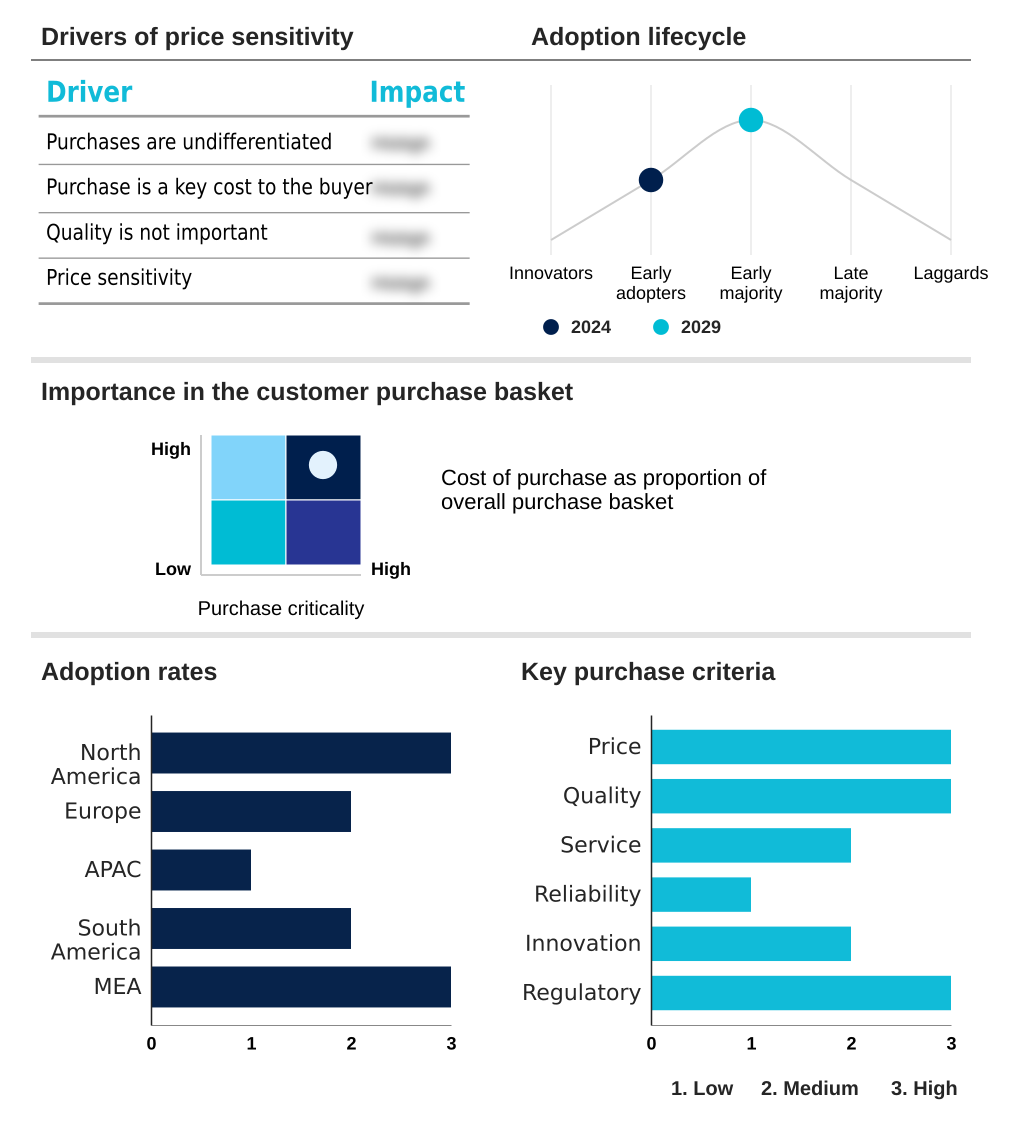

The geographic landscape of the market is distinctly divided. North America and Europe represent mature regions, where growth is driven by upgrades and ecosystem expansion, with over 60% of households owning at least one smart device.

In contrast, the APAC region is the fastest-growing, fueled by a rising middle class and localized content delivery. This region's expansion is nearly 25% faster than that of South America.

European market strategies are heavily influenced by stringent data governance frameworks, promoting privacy-preserving architecture and on-device AI processing. In Asia, domestic leaders focus on deep IoT device integration and proactive assistance within their ecosystems.

This regional fragmentation requires manufacturers to tailor not only voice assistant platforms and third-party skill ecosystems but also hardware features and pricing models to succeed, balancing global technology with local market demands for smart energy management and seamless ecosystem integration.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the AI speakers market is increasingly shaped by nuanced technical and user-experience considerations. A central debate involves comparing on-device vs cloud AI processing, with a clear trend toward hybrid models to balance privacy and power.

- The impact of Matter standard on speaker utility is profound, transforming standalone devices into true home automation hubs and eliminating ecosystem fragmentation. This is pushing the role of Thread border routers in speakers from a niche feature to a core component for robust IoT connectivity.

- Concurrently, the rise of generative AI for personalized content creation is redefining user engagement, allowing for unique interactions like custom stories or music. However, this raises the privacy implications of advanced voice assistants, compelling vendors to invest in voice biometrics security and transparent data policies.

- Key growth vectors include using AI speakers for ambient health monitoring and the integration of voice assistants in automotive settings, extending the ecosystem beyond the home. Addressing market challenges from AI model unreliability is now critical; mitigating AI hallucinations in voice response is a top R&D priority, with some systems improving factual accuracy by over 30% through retrieval-augmented generation.

- Success now depends on a holistic strategy encompassing everything from high-fidelity audio in smart speaker design to developing localized AI for emerging markets.

What are the key market drivers leading to the rise in the adoption of AI Speakers Industry?

- The integration of advanced generative AI and large language models is a key driver transforming AI speakers into more conversational and capable assistants.

- Market growth is driven by a technological leap in core intelligence and ecosystem utility. The integration of large language models is enabling context-aware interaction and proactive assistance, transforming the user experience.

- This AI evolution is attracting new user segments, with some platforms reporting a 25% increase in engagement for complex, multi-step tasks.

- The expansion of the smart home, unified by the Matter connectivity standard, makes the AI speaker a critical home automation hub.

- As consumers add more connected devices, the value of a centralized command center with a voice-activated user interface increases significantly. Furthermore, the demand for premium, high-fidelity audio, supported by advanced acoustic engineering and high-fidelity audio drivers, is creating higher-margin opportunities.

- This is complemented by the growth of multi-modal interfaces, where smart display functionality broadens use cases for everything from video calls to recipe tutorials.

What are the market trends shaping the AI Speakers Industry?

- The proliferation of generative AI is driving a shift toward multimodal functionality, redefining user interaction with AI-powered devices. This evolution is reshaping expectations for conversational intelligence and context-aware capabilities.

- Key market trends are converging to create more intelligent and autonomous devices. The move toward a privacy-preserving architecture is accelerating, with on-device processing reducing reliance on the cloud by up to 40% for common commands. This complements the expansion of the interoperable smart home, where seamless ecosystem integration is paramount.

- The incorporation of premium audio components and sophisticated digital signal processors is creating a distinct high-fidelity segment, appealing to users seeking audiophile-grade sound. This focus on audio-visual products enhances the cinematic audio experience in soundbars. Concurrently, the development of conversational AI companions is making interactions more natural.

- However, this advanced functionality requires a robust data governance framework to maintain user trust, especially as these devices find use in sensitive areas like ambient health monitoring and automotive voice control.

What challenges does the AI Speakers Industry face during its growth?

- Intensifying scrutiny over data privacy and security presents a key challenge, potentially impeding consumer trust and market growth.

- The market faces significant hurdles that temper its growth trajectory, primarily centered on trust and commoditization. Intensifying scrutiny over data privacy has created a consumer trust deficit, with surveys indicating that over 50% of non-adopters cite security as their main concern.

- This challenge is magnified by AI-induced hallucinations from new generative models, undermining device reliability and demanding sophisticated fact-checking mechanisms and retrieval-augmented generation systems. In mature markets, market saturation challenges are leading to slowing sales and intense price competition, eroding margins.

- The core utility of many devices has become a set of commoditized hardware functions, making it difficult to convince users to upgrade, contributing to lengthening device replacement cycles. This forces a difficult quest for meaningful innovation beyond incremental improvements, pushing companies to invest heavily in next-generation conversational AI to prove tangible new value and escape the cycle of price-based competition.

Exclusive Technavio Analysis on Customer Landscape

The ai speakers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai speakers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Speakers Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai speakers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Core offerings center on voice-assistant-powered hardware, enabling expansive smart home and media control ecosystems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Anker Technology UK Ltd.

- Apple Inc.

- Bang and Olufsen Group

- Bose Corp.

- Google LLC

- Huawei Technologies Co. Ltd.

- LG Electronics Inc.

- Panasonic Holdings Corp.

- Samsung Electronics Co. Ltd.

- Sonos Inc.

- Sonova AG

- Sony Group Corp.

- Xiaomi Inc.

- Yandex NV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai speakers market

- In September, 2024, Sonova AG unveils a new line of premium AI speakers featuring advanced on-device processing and robust voice biometrics, aiming to capture the privacy-conscious consumer segment with high-fidelity audio.

- In November, 2024, Google LLC announces a strategic partnership with a leading healthcare consortium to pilot ambient health monitoring services through its Nest Hub devices in assisted living facilities across North America.

- In January, 2025, The Connectivity Standards Alliance officially releases the Matter 1.4 specification, introducing standardized support for home energy management systems and advanced appliances, enhancing the role of AI speakers as central home controllers.

- In April, 2025, Xiaomi Inc. launches a new range of affordable AI speakers with integrated Thread border routers and enhanced local language support, targeting rapid market penetration in India and Southeast Asia.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Speakers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 23.1% |

| Market growth 2025-2029 | USD 12691.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 20.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI speakers market is undergoing a critical transformation, shifting from hardware-centric sales to a model predicated on the intelligence and utility of the underlying voice assistant platforms. This evolution is driven by generative AI integration, which enables more natural, multi-turn dialogue and user intent inference.

- A key boardroom consideration is the pivot to on-device AI processing and custom silicon design, a direct response to consumer privacy demands and stringent data governance frameworks that can impact market access.

- This move toward edge AI capabilities reduces reliance on the hybrid cloud model and improves low-latency response, with some advanced microphone arrays and system-on-chip processors achieving a 20% faster wake-word detection. The focus on computational audio technology and high-fidelity audio drivers continues to segment the market, creating premium tiers.

- Meanwhile, the maturation of the Matter connectivity standard is making devices with integrated Thread border routers indispensable as a home automation hub, simplifying IoT device integration and fostering a cohesive ambient computing ecosystem through natural language processing.

What are the Key Data Covered in this AI Speakers Market Research and Growth Report?

-

What is the expected growth of the AI Speakers Market between 2025 and 2029?

-

USD 12.69 billion, at a CAGR of 23.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Smart speaker, Portable AI speaker, Soundbars with voice assistant), Component (Hardware, Software, Services), Connectivity (Wi-Fi, Bluetooth, Cellular or LTE, Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of advanced generative AI and large language models, Intensifying data privacy and security scrutiny

-

-

Who are the major players in the AI Speakers Market?

-

Amazon.com Inc., Anker Technology UK Ltd., Apple Inc., Bang and Olufsen Group, Bose Corp., Google LLC, Huawei Technologies Co. Ltd., LG Electronics Inc., Panasonic Holdings Corp., Samsung Electronics Co. Ltd., Sonos Inc., Sonova AG, Sony Group Corp., Xiaomi Inc. and Yandex NV

-

Market Research Insights

- Market dynamics are shaped by the pivot toward subscription-based services and B2B vertical applications, which promise new revenue streams beyond hardware sales. The focus on creating an interoperable smart home, where devices offer cross-platform compatibility, has seen some integrations improve multi-device setup times by over 40%.

- While smart display functionality enhances user engagement, challenges from AI-induced hallucinations and the consumer trust deficit require robust fact-checking mechanisms. The reliance on cloud-dependent processing is diminishing in favor of privacy-preserving architecture. Firms are navigating device replacement cycles in saturated markets by offering audiophile-grade sound and tangible software-defined features.

- This strategic shift from commoditized hardware functions to developing conversational AI companions has improved user retention by 25% in certain premium segments, illustrating a move toward qualitative enhancements over quantitative expansion.

We can help! Our analysts can customize this ai speakers market research report to meet your requirements.

RIA -

RIA -