Aircraft Engine MRO Market Size 2025-2029

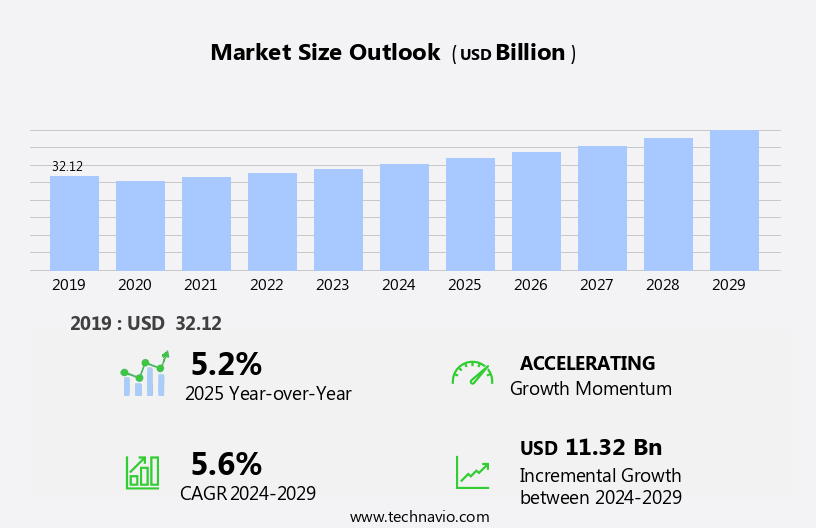

The aircraft engine MRO market size is forecast to increase by USD 11.32 billion at a CAGR of 5.6% between 2024 and 2029.

- The aircraft engine Maintenance, Repair, and Overhaul (MRO) market is experiencing significant growth, driven by increasing investments in MRO facilities and the adoption of advanced technologies such as 3D printing. These trends are transforming the industry, enabling more efficient and cost-effective maintenance solutions. However, the market also faces challenges, including the high cost of new technology and equipment adoption in aircraft engine, and the need for a skilled workforce to operate and maintain these advanced systems. The increasing demand for air travel necessitates a growing workforce to support MRO activities. The aviation industry's continued growth, driven by increasing passenger traffic and aircraft movements, necessitates a corresponding expansion in aircraft maintenance, repair, and overhaul (MRO) activities. These factors are shaping the future of the market, with a focus on innovation, cost savings, and workforce development. The market analysis report provides a comprehensive assessment of these trends and challenges, offering insights into the key drivers and barriers shaping the industry's growth trajectory.

What will be the Size of the Aircraft Engine MRO Market During the Forecast Period?

- Airlines and military forces alike rely on MRO support centers to ensure the optimal performance and safety of their aircraft fleets. Tier-II and tier-III suppliers play a crucial role in providing essential components and services for these MRO activities. The global aircraft fleet is experiencing significant expansion, with both passenger and cargo aircraft in high demand. Next-generation engines, such as the LEAP engine, are revolutionizing the industry with their improved fuel efficiency and reduced emissions.

- Moreover, turbine and piston engines continue to dominate the market, with ongoing advancements in technology driving innovation. Rapid urbanization and emerging countries are contributing to rising air traffic volumes and aircraft utilization. Labor force costs and the availability of skilled technicians remain key challenges for the industry. MRO market dynamics are influenced by various factors, including fleet expansion plans, the adoption of new technologies, and the evolving regulatory landscape. The industry's continued growth and evolution underscore the importance of effective MRO strategies for airlines and military forces alike.

How is this Aircraft Engine MRO Industry segmented and which is the largest segment?

The Aircraft Engine MRO industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

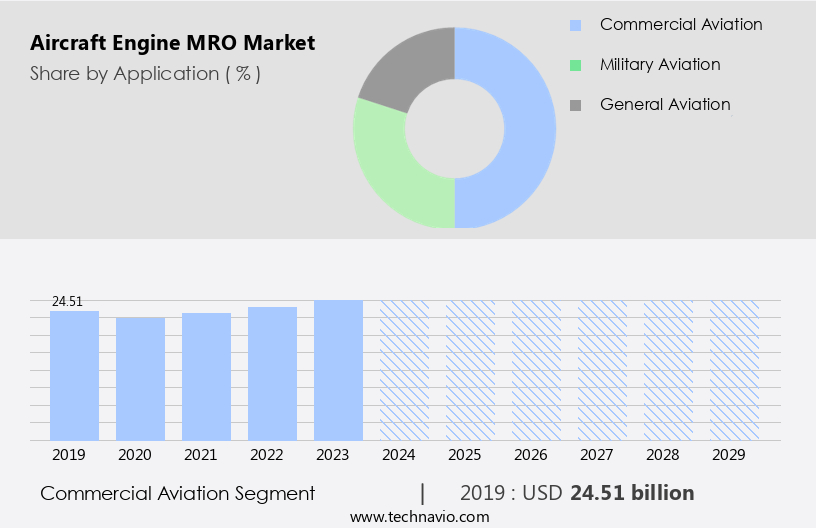

- Commercial aviation

- Military aviation

- General aviation

- Type

- Turbofan and turbojet

- Turboprop

- Geography

- APAC

- China

- India

- South Korea

- Europe

- Germany

- France

- North America

- Canada

- US

- Middle East and Africa

- South America

- Brazil

- APAC

By Application Insights

- The commercial aviation segment is estimated to witness significant growth during the forecast period.

Commercial aviation operators prioritize engine maintenance to ensure the optimal performance and safety of their aircraft. Routine inspections, lubrication, and component replacements are crucial for preventing wear and tear. Unscheduled engine issues necessitate MRO (Maintenance, Repair, and Overhaul) services for diagnosis and repair. Overhauls involve comprehensive inspections, repairs, and component replacement to extend engine life. Commercial airlines schedule overhauls based on operating hours or regulatory requirements. Adherence to safety and airworthiness regulations, such as those set by the FAA and EASA, is essential in the highly regulated commercial aviation sector. Newer generation engines require expensive materials and digitized, automated maintenance activities to enhance turnaround time and efficiency. MRO services play a vital role in maintaining the airworthiness and safety of aircraft engines in both commercial aviation and military applications.

Get a glance at the Aircraft Engine MRO Industry report of share of various segments Request Free Sample

The commercial aviation segment was valued at USD 24.51 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

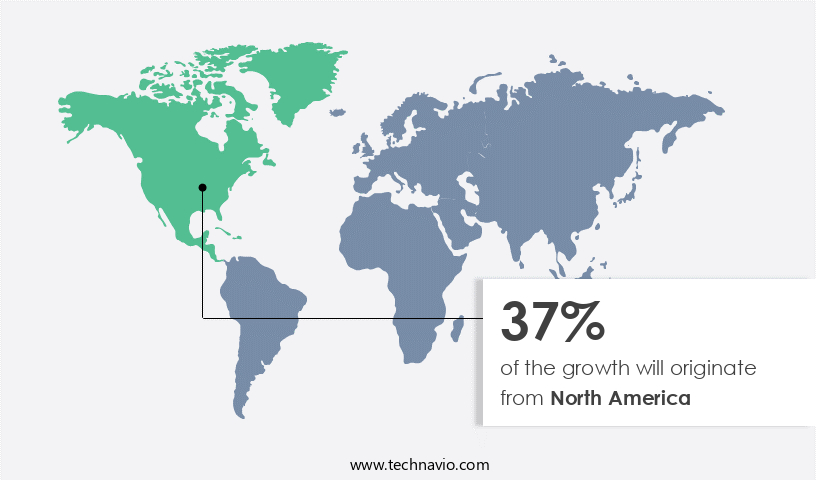

- North America is estimated to contribute 37% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The Asia Pacific (APAC) region is experiencing steady growth in the commercial aviation industry due to increasing passenger traffic driven by low-cost carriers (LCCs), rising living standards, a growing middle class, and tourism expansion. Fleet operators are seeking energy-efficient aircraft to replace aging models, providing opportunities for aircraft and engine manufacturers to compete in the region with attractive pricing strategies. APAC is expected to lead the global aviation industry over the next two decades due to its high growth rates. Additionally, there is a rising demand for advanced technologies, including next-generation engines such as the LEAP engine, from Tier-I, II, and III suppliers to support MRO (Maintenance, Repair, and Overhaul) centers for cargo and passenger aircraft, as well as piston and turbine engines.

Market Dynamics

Our aircraft engine MRO market researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Aircraft Engine MRO Industry?

Increasing investments in MRO facilities is the key driver of the market.

- The global aircraft engine Maintenance, Repair, and Overhaul (MRO) market is experiencing significant growth due to several factors. Aviation industries, including airlines and military forces, are investing heavily in fleet expansion plans, leading to an increase in aircraft movements and subsequent demand for engine maintenance and overhaul activities. This trend is particularly noticeable in emerging countries, where air traffic volumes are surging due to rapid urbanization and expanding middle-class populations. MRO companies are responding to this demand by setting up new facilities in these regions. For instance, Airbus Helicopters recently opened a new MRO facility in Singapore to enhance helicopter maintenance capabilities in the Asia-Pacific region.

- Similarly, Lockheed Martin Corp. Expanded its MRO services by opening a new facility in Japan, focusing on the maintenance of advanced fighter jets for the Japanese Air Self-Defense Force. Moreover, the increasing adoption of digitization and automation in maintenance activities is reducing turnaround time and improving safety. The commercial aviation segment, which includes narrow-body and wide-body aircraft, is a significant contributor to the market's growth. Military aviation is another major segment, with defense funding driving the demand for engine MRO services. The engine maintenance cost is a critical factor for both commercial and military aviation segments. As a result, engine manufacturers and MRO service providers are partnering to offer long-term contracts and joint ventures to reduce costs and improve efficiency.

What are the market trends shaping the Aircraft Engine MRO Industry?

Growing adoption of 3D printing technology for aircraft engine MRO is the upcoming trend in the market.

- The Aircraft Engine MRO (Maintenance, Repair, and Overhaul) market in the aviation industry is experiencing significant growth due to increasing passenger traffic, aircraft movements, and fleet expansion plans. Both commercial aviation and military aviation segments require extensive engine maintenance, repair, and overhaul activities, driving the demand for engine MRO services. Newer generation engines with expensive material requirements and digitization and automation of maintenance activities are key trends in the market. Airline companies and military forces are forming long-term partnerships and joint ventures with service providers to improve turnaround time, ensure safety, and reduce engine maintenance costs. General aviation, cargo aircraft, and next-generation engines are also contributing to the market growth.

- Moreover, the engine MRO market encompasses a wide range of engines, including turbine engines (Leap 1B engines), piston engines, turboprops, turbofans, turboshafts, fixed-wing aircraft, and rotary-wing aircraft. The market is expected to grow further due to air traffic volumes, aircraft utilization, and workforce supply, despite increasing labor force costs and technical maintenance job demands. Tier-II and Tier-III suppliers play a crucial role in providing component requirements and technical and training services. Air travel continues to be a significant contributor to the global economy, and the aviation industry's ongoing digitization and automation processes are expected to further drive the engine MRO market.

What challenges does Aircraft Engine MRO Industry face during the growth?

Barriers to adoption of new technology and equipment in aircraft MRO is a key challenge affecting the industry growth.

- The Aircraft Engine MRO (Maintenance, Repair, and Overhaul) market in the aviation industry encompasses various segments, including passenger traffic, aircraft movements, and fleet expansion plans of airlines and military forces. Aircraft maintenance, repair, and overhaul activities are essential for ensuring the safety and efficiency of aircraft engines. The commercial aviation segment, which includes passenger airlines, requires frequent engine maintenance due to high aircraft utilization and increasing air traffic volumes. Newer generation engines, such as LEAP 1B engines, have expensive material requirements and complex component needs, necessitating digitization and automation of maintenance activities for faster turnaround times. Service providers, such as S7 Technics at Sheremetyevo airport, offer engine MRO services at maintenance facilities and overhaul facilities.

- Furthermore, these partnerships are crucial for airlines and military forces to ensure their total aircraft fleet remains operational. Military aviation also requires engine maintenance, with a focus on Tier-II and Tier-III suppliers for supplying spare parts. Cargo aircraft and various types of aircraft, including fixed-wing aircraft and rotary-wing aircraft, also require engine MRO services. The military aviation sector faces challenges in adopting new technologies due to high obsolescence rates and the need for long-term partnerships and joint ventures. The civil aviation sector, driven by rapid urbanization and emerging countries, requires continuous investment in engine maintenance and training services at aviation training centers.

Exclusive Customer Landscape

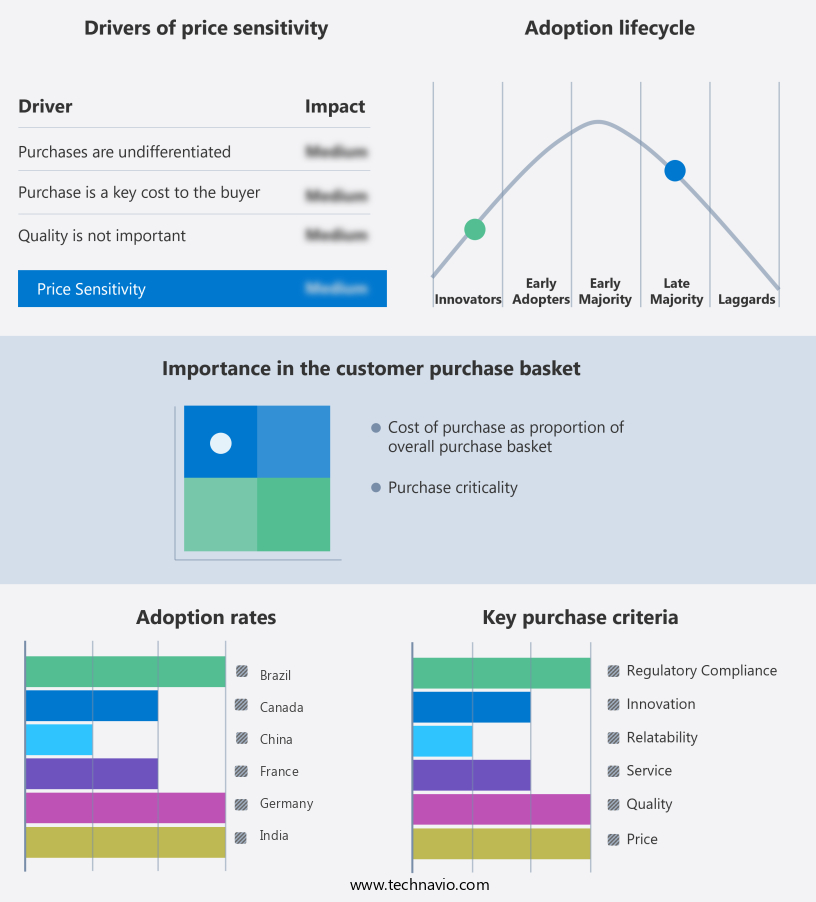

The aircraft engine MRO market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AAR Corp. - The company offers aircraft engine MRO services such as scheduled maintenance, unscheduled repairs, hot section inspections, boroscope inspections, and component overhaul services.

The Aircraft Engine MRO industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A J Walter Aviation Ltd.

- ANA Engine Technics Co. ltd.

- Aviation Technical Services

- AZUL SA

- CFM International

- Delta TechOps

- General Electric Company

- Hindustan Aeronautics Ltd.

- Hong Kong Aircraft Engineering Company Limited.

- IAG Aero Group

- Israel Aerospace Industries Ltd.

- Lufthansa Group

- MTU Aero Engines AG

- Pratt and Whitney

- Rolls Royce Holdings Plc

- Sanad

- SIA Engineering Company

- Singapore Technologies Engineering Ltd.

- Synerjet Corp.

- TAP Maintenance & Engineering

- The Boeing Co.

- Turkish Airlines

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The aircraft engine Maintenance, Repair, and Overhaul (MRO) market plays a crucial role in ensuring the optimal performance and safety of aircraft engines. This sector encompasses a wide range of activities, including maintenance, repair, overhaul, technical training, and component requirements for various types of engines powering fixed-wing and rotary-wing aircraft. Aircraft engine MRO is an essential component of the aviation industry, with its significance extending to both commercial and military sectors. The commercial aviation segment experiences continuous growth due to increasing passenger traffic, fleet expansion plans, and airline companies' efforts to maintain their fleets' operational efficiency.

Meanwhile, military aviation relies on MRO to ensure the readiness of defense forces and their aircraft, with defense funding being a significant factor. The market is witnessing a shift towards digitization and automation as technology advances. Newer generation engines demand expensive material requirements, and MRO service providers are investing in digital tools to streamline maintenance activities, reduce turnaround time, and enhance safety. Safety remains a top priority in the market. Service providers focus on implementing rigorous safety protocols and adhering to industry standards to ensure the engines' reliable operation. Moreover, MRO facilities are expanding their capacity to cater to the growing demand for engine services.

Furthermore, engine MRO services are provided by various types of service providers, including original equipment manufacturers (OEMs), independent repair stations, and MRO support centers. Tier-II and tier-III suppliers also play a vital role in the market by providing components and technical services. The total aircraft fleet continues to grow, driven by the increasing demand for air travel and rapid urbanization in emerging countries. This expansion results in higher air traffic volumes and increased aircraft utilization, leading to a greater need for engine MRO services. Workforce supply and labor force costs are essential considerations for engine MRO providers. Technical maintenance jobs are in high demand, and the industry is continuously evolving to meet the needs of the growing aircraft fleet and the increasing complexity of engines.

In addition, MRO facilities offer various services, including field maintenance, depot maintenance, and overhaul facilities. Engine types include turbine engines (leap 1b engines, for example), piston engines, turboprops, turbofans, and turboshafts, each requiring unique maintenance approaches. Long-term partnerships and joint ventures are common in the engine MRO market, as they enable service providers to share resources, expertise, and costs, ultimately benefiting both parties. Companies such as S7 Technics at Sheremetyevo Airport have established themselves as key players in the market by offering comprehensive engine MRO services and maintaining strong partnerships with various airlines and OEMs. In conclusion, the market is a dynamic and evolving sector that plays a vital role in ensuring the safety, efficiency, and reliability of aircraft engines. With the growing demand for air travel and the increasing complexity of engines, the market is expected to continue its expansion in the coming years.

|

Aircraft Engine MRO Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

199 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.6% |

|

Market growth 2025-2029 |

USD 11.32 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.2 |

|

Key countries |

US, China, Russia, Germany, India, South Korea, Canada, France, UAE, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the Aircraft Engine MRO industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of industry companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -