Alkyd Resin Market Size 2024-2028

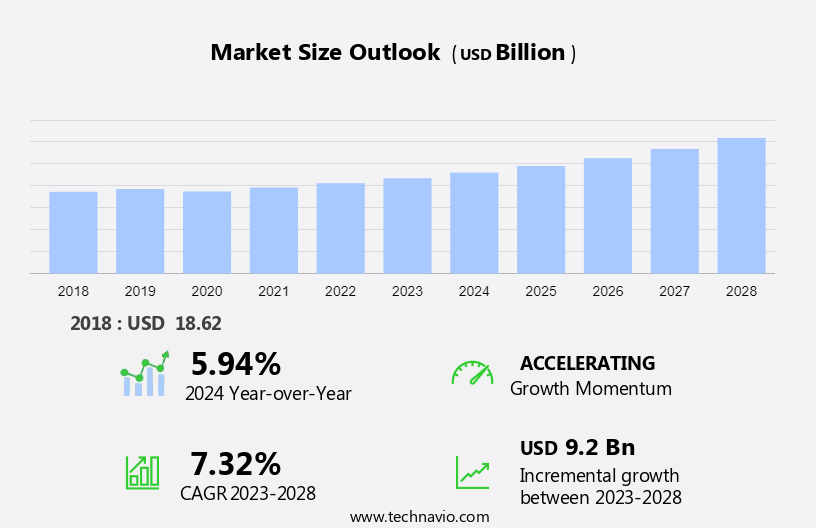

The alkyd resin market size is forecast to increase by USD 9.2 billion at a CAGR of 7.32% between 2023 and 2028.

- The market is experiencing significant growth due to the superior properties of alkyd resins, which include excellent chemical resistance, good adhesion, and a high gloss finish. Another key trend driving market growth is the increasing utilization of alkyd resins in the automotive manufacturing industry, as they are used in the production of automotive coatings. However, the market is also facing challenges, such as the fluctuating prices of crude oil, which is a primary raw material used in the production of alkyd resins. Despite these challenges, the market is expected to continue growing due to the increasing demand for high-performance coatings in various industries, including construction, automotive, and industrial applications.

- Additionally, advancements in technology are leading to the development of more sustainable and eco-friendly alkyd resins, which is another growth opportunity for market participants. Overall, the market is poised for growth, driven by its superior properties and increasing applications in various industries, despite the challenges posed by fluctuating raw material prices.

What will be the Size of the Alkyd Resin Market During the Forecast Period?

- The market encompasses the production and supply of alkyd resins, a type of thermosetting resin derived from the reaction of polybasic acids and polyhydric alcohols, often using fatty acids or triglyceride oils as raw materials. Alkyd resins exhibit desirable properties for coating applications, including brightness, color consistency, thermal stability, and compatibility with various additives and pigments. Market growth is driven by the increasing demand for industrial coatings, particularly in sectors such as automotive, construction, and packaging. Nondrying, semidrying, and drying alkyd resins, as well as acrylated, waterborne, and silicon-modified variants, cater to diverse application requirements. The market size is significant, with continued expansion anticipated due to the ongoing development of high-performance alkyd resins derived from renewable sources, such as palm oleic acid and various vegetable oils including linseed, castor, soybean, and tall oil.

- Molecular weight, unreacted acids, and hydroxyl groups are crucial factors influencing alkyd resin properties and compatibility with other components in coatings formulations. The market's direction is towards sustainable production methods and the use of natural alkyd resins, which offer reduced environmental impact and improved product performance.

How is this Alkyd Resin Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

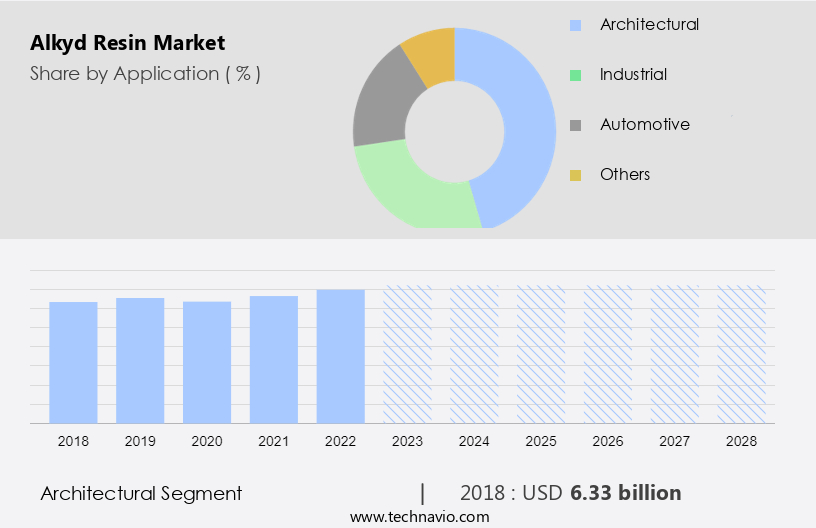

- Application

- Architectural

- Industrial

- Automotive

- Others

- Type

- Fatty acid process

- Glyceride process

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- France

- North America

- US

- Middle East and Africa

- South America

- APAC

By Application Insights

- The architectural segment is estimated to witness significant growth during the forecast period.

Alkyd resins are a type of thermosetting resin widely used in the production of architectural coatings for commercial and residential buildings. These coatings offer protection against moisture, UV radiation, and microbes, and include paints, primers, lacquers, varnishes, and stains. The shift towards low volatile organic compound (VOC) content in coatings, driven by stringent regulations in developed regions like the US, the UK, and Germany, has boosted the demand for alkyd resins. Sustainability is a growing concern for consumers in these markets, leading to increased interest in eco-friendly alkyd resins derived from renewable resources such as vegetable oils, including linseed oil, castor oil, soybean oil, and tall oil.

The polyesterification process, which involves the reaction of polybasic acids and polyhydric alcohols, is commonly used to produce alkyd resins. Other variations include acrylated alkyds, waterborne alkyds, and silicon modified alkyds. These resins offer desirable properties such as brightness, color consistency, thermal stability, and excellent compatibility with various pigments and additives. They exhibit good chemical resistance, gloss retention, durability, and resistance to water, alkali, and brine. The molecular weight and unreacted acids in alkyd resins can be controlled to optimize their performance in different applications.

Get a glance at the market report of share of various segments Request Free Sample

The Architectural segment was valued at USD 6.33 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

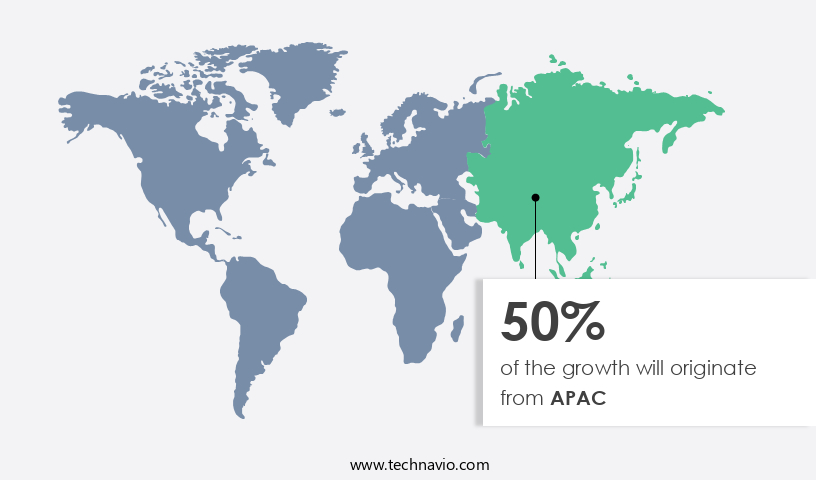

- APAC is estimated to contribute 50% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market is driven by rapid industrialization and infrastructure development in the Asia Pacific (APAC) region, particularly in countries like China, Malaysia, Indonesia, Vietnam, Japan, South Korea, and India. The construction industry's growth in these countries, including projects such as the Three Gorges Dam in China and the Navi Mumbai International Airport in India, will significantly increase the demand for alkyd resins due to their extensive use in industrial coatings. Alkyd resins are organic polyesters produced through the polyesterification of polybasic acids and polyhydric alcohols, often using fatty acids or triglyceride oils as raw materials. They offer desirable properties such as brightness, color consistency, thermal stability, and resistance to water, brine, and acids.

Natural alkyd resins derived from renewable resources like palm oleic acid, linseed oil, castor oil, soybean oil, and tall oil are gaining popularity due to their eco-friendly nature. The market segments include nondrying alkyd, semidrying alkyd, drying alkyd, acrylated alkyd, waterborne alkyd, silicon modified alkyd, and polyol-based alkyd resins. Alkyd resins exhibit excellent compatibility with various solvents and exhibit high solids compositions, making them ideal for surface coatings applications. The market's growth is further fueled by the increasing demand for high-performance coatings with superior chemical resistance, gloss retention, durability, and flexibility.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Alkyd Resin Industry?

Superior properties of alkyd resins are the key driver of the market.

- Alkyd resins are thermoplastic organic polyesters derived from the reaction of polyhydric alcohols and polybasic acids or their anhydrides. These resins are widely utilized in the production of protective coatings due to their excellent weathering properties. Alkyd resins are a significant component in the synthesis of synthetic paints, valued for their versatility and cost-effectiveness. A key feature of alkyd resins is their compatibility with various coating polymers, such as vinyl resins. Vinyl resins, which contain hydroxyl groups, can be blended with alkyd resins to enhance desirable application properties, such as adhesion. This combination is frequently employed in the manufacture of marine top-coat paints.

- Alkyd resins offer various types, including nondrying, semidrying, and drying alkyds, as well as acrylated, waterborne, silicon modified, and polyol-based alkyds. Their molecular weight, compatibility with vegetable oils like linseed, castor, soybean, and tall oil, and resistance to acid, water, and alkali are essential factors that contribute to their extensive use in industrial coatings. The market is driven by the demand for surface coatings with superior brightness, color consistency, thermal stability, and chemical resistance. The industry also focuses on enhancing the properties of alkyd resins through processes like esterification, polymerization, and etherification, leading to improved gloss retention, durability, and flexibility.

What are the market trends shaping the Alkyd Resin Industry?

Growing product utilization in automotive manufacturing is the upcoming market trend.

- The market is experiencing growth due to the increasing demand in the automotive industry. Alkyd resins, which are thermoplastic organic polyesters derived through polycondensation of polyhydric alcohols and polybasic acids, are widely used in coatings applications. Their desirable properties, including brightness, color consistency, thermal stability, and compatibility with various vegetable oils such as linseed, castor, soybean, tall oil, and triglyceride oils, make them ideal for industrial coatings. The automotive sector's expansion, driven by the moderate growth rate and the promotion of electric vehicles by governments, is leading to an increased demand for these resins. These resins offer superior properties for automotive coatings, such as good initial gloss, strength, and excellent gloss retention, even in harsh climatic conditions.

- These factors are expected to fuel the growth of the market during the forecast period. These resins come in various forms, including nondrying alkyd, semidrying alkyd, drying alkyd, acrylated alkyd, waterborne alkyd, silicon modified alkyd, and polyol-based alkyd resins. These resins undergo polymerization processes such as esterification, polymer structure modification, and monoglyceride formation to create the final product. These resins exhibit excellent chemical resistance, gloss retention, durability, and flexibility, making them suitable for various applications beyond the automotive industry. Additionally, the use of renewable resources like vegetable oils and fatty acids in the production of these resins aligns with the growing trend towards eco-friendly manufacturing processes.

What challenges does the Alkyd Resin Industry face during its growth?

Fluctuating crude oil prices is a key challenge affecting the industry growth.

- Alkyd resins, a type of thermoplastic organic polyesters, are derived from the reaction of polyols and polybasic acids or their anhydrides. Polyols are organic compounds with multiple hydroxyl groups, while polybasic acids contain multiple carboxylic acid groups. These raw materials are often sourced from crude oil and triglyceride oils, such as linseed, castor, soybean, tall oil, and palm oleic acid. Price volatility in crude oil, a primary feedstock, significantly impacts alkyd resin production costs.

- This price increase can potentially affect the affordability of these resins for various coating applications. These resins are widely used in industrial coatings due to their desirable properties, including brightness, color consistency, thermal stability, and compatibility with vegetable oils. The market offers various types, including nondrying, semidrying, drying, acrylated, waterborne, silicon modified, and polyol-based alkyds. These resins exhibit excellent chemical resistance, gloss retention, durability, and flexibility, making them suitable for various surface coatings applications. The market is influenced by factors such as molecular weight, unreacted acids, hydroxyl groups, and compatibility with other additives. The production process involves polyesterification, esterification, stepwise polymerization, etherification, and saponification.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allnex GMBH

- Arakawa Chemical Industries Co. Ltd.

- Arkema Group

- BASF SE

- Bayer AG

- Evonik Industries AG

- Matapel Chemicals

- MEGARA RESINS SA

- Mitsui Chemicals Inc

- OPC Polymers

- Polynt Spa

- PPG Industries Inc.

- Solvay SA

- Synpol Products Pvt. Ltd.

- Synthomer Plc

- Synthopol Chemie Dr. rer. pol. Koch GmbH and Co. KG

- Wacker Chemie AG

- Akzo Nobel NV

- Uniform Synthetics Pvt. Ltd.

- Worlee Chemie GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Alkyd resins, a class of thermoplastic organic polyesters, are widely used in various coating applications due to their desirable properties. These resins are produced through a process called polycondensation, which involves the reaction of polyhydric alcohols and polybasic acids. The resulting product is a complex mixture of esters, acids, and unreacted hydroxyl groups. The production of these resins begins with the selection of raw materials, primarily fatty acids and triglyceride oils. These materials undergo a process called esterification, where they react with glycerol or other polyols to form monoglycerides. Subsequently, the monoglycerides undergo polyesterification, a stepwise polymerization process, to form the alkyd resin.

Moreover, the molecular weight and compatibility of these resins can be manipulated by adjusting the reaction conditions and raw material selection. For instance, the use of different fatty acids, such as palm oleic acid, can affect the final product's properties. Natural alkyd resins derived from vegetable oils, including linseed oil, castor oil, soybean oil, and tall oil, are gaining popularity due to their renewable nature. These resins exhibit excellent properties for coating applications. They offer high brightness and color consistency, making them suitable for use in surface coatings. Thermal stability is another crucial property, ensuring that the coating maintains its integrity under various temperature conditions.

Furthermore, they can be categorized based on their drying behavior. Nondrying alkyds do not require solvents for application, while semidrying alkyds require shorter drying times than traditional drying alkyds. Acrylated alkyds and waterborne alkyds are other types that offer advantages such as improved chemical resistance, flexibility, and impact resistance. Silicon-modified alkyds are a newer development in the market. These resins exhibit enhanced properties, such as improved water resistance, alkali resistance, and brine resistance. Eco-labeling and solvent reduction are essential trends in the industry, leading to the development of high solids compositions and the use of renewable resources. The market is driven by the growing demand for industrial coatings.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

176 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.32% |

|

Market growth 2024-2028 |

USD 9.2 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.94 |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Alkyd Resin Market Research and Growth Report?

- CAGR of the Alkyd Resin industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the alkyd resin market growth of industry companies

We can help! Our analysts can customize this alkyd resin market research report to meet your requirements.

RIA -

RIA -