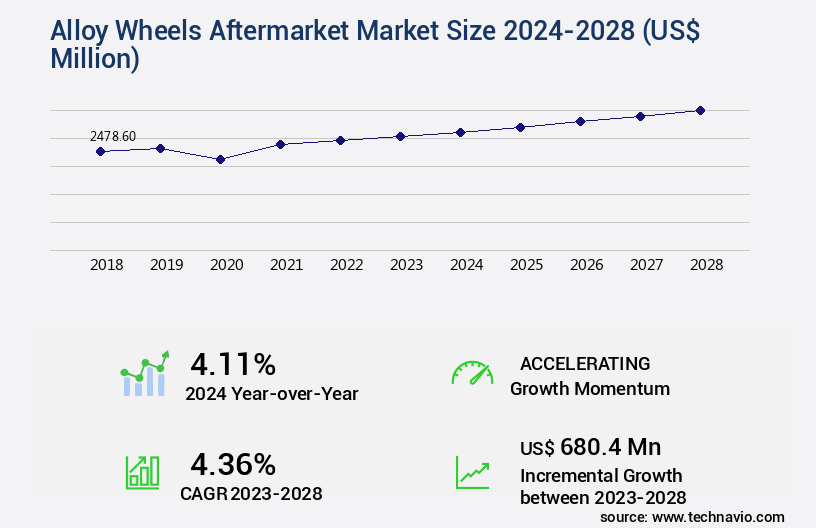

Alloy Wheels Aftermarket Market Size 2024-2028

The alloy wheels aftermarket market size is valued to increase by USD 680.4 million, at a CAGR of 4.36% from 2023 to 2028. Aging vehicle fleet will drive the alloy wheels aftermarket market.

Major Market Trends & Insights

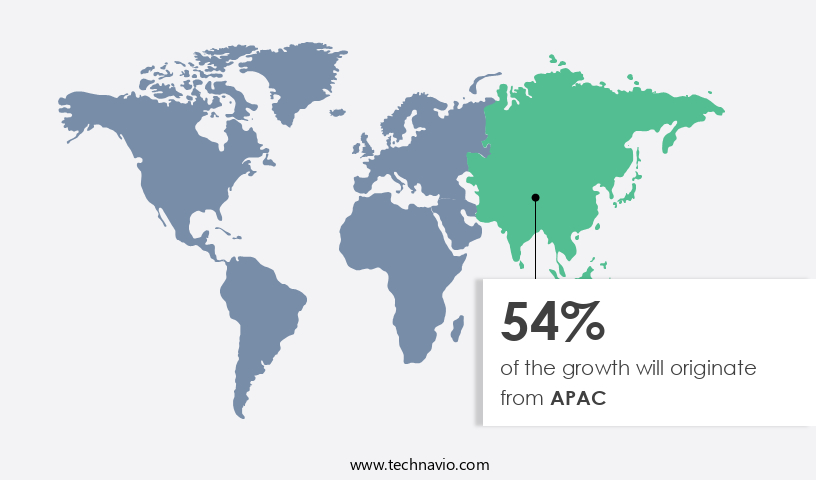

- APAC dominated the market and accounted for a 54% growth during the forecast period.

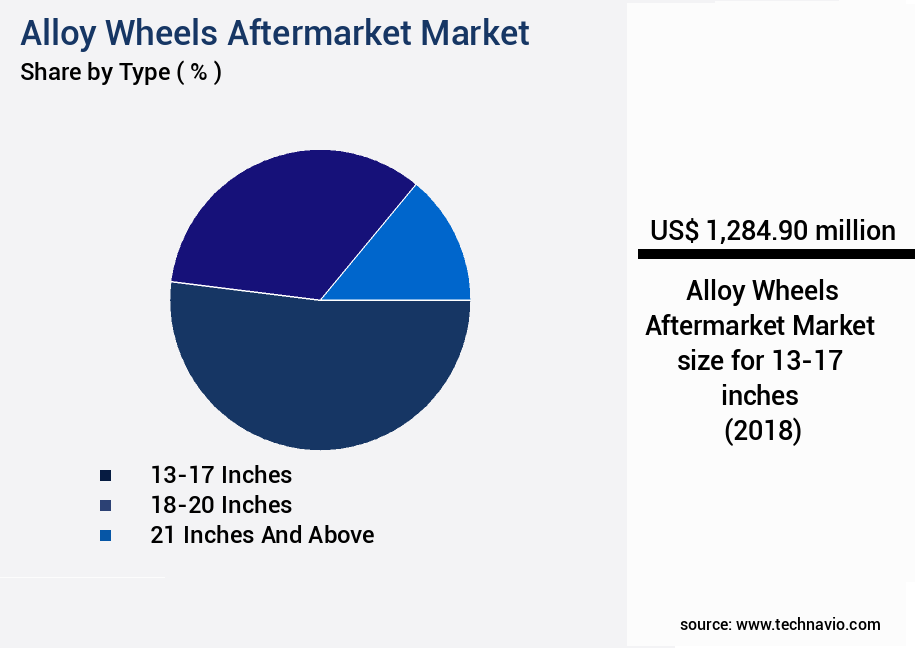

- By Type - 13-17 inches segment was valued at USD 1284.90 million in 2022

- By Vehicle Type - Passenger vehicle segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 42.77 million

- Market Future Opportunities: USD 680.40 million

- CAGR from 2023 to 2028 : 4.36%

Market Summary

- The Alloy Wheels Aftermarket is witnessing significant growth due to the increasing trend of vehicle customization and the aging vehicle fleet. As vehicles age, the demand for wheel replacements increases, leading to a burgeoning aftermarket. Technological advancements in alloy wheel manufacturing, such as lightweight materials and improved durability, are also driving demand. One real-world business scenario illustrating the importance of the alloy wheels aftermarket is supply chain optimization. A leading automotive parts distributor implemented an advanced inventory management system, which included real-time data analytics and automated reordering. By closely monitoring demand patterns and stock levels for alloy wheels, the distributor was able to reduce stockouts by 15% and improve delivery times, leading to increased customer satisfaction and loyalty.

- Moreover, the rise in OEM fitment of alloy wheels as standard equipment in new vehicles is further fueling market growth. According to recent studies, the number of vehicles with alloy wheels as standard equipment has increased by 25% over the past decade. This trend is expected to continue, as alloy wheels offer improved performance, durability, and aesthetics compared to traditional steel wheels. In conclusion, the Alloy Wheels Aftermarket is experiencing robust growth due to factors such as the aging vehicle fleet, technological advancements, and increasing OEM fitment. Businesses in this sector can benefit from supply chain optimization strategies and the latest manufacturing technologies to stay competitive and meet the evolving demands of consumers.

What will be the Size of the Alloy Wheels Aftermarket Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Alloy Wheels Aftermarket Market Segmented ?

The alloy wheels aftermarket industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- 13-17 inches

- 18-20 inches

- 21 inches and above

- Vehicle Type

- Passenger vehicle

- Commercial vehicle

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Type Insights

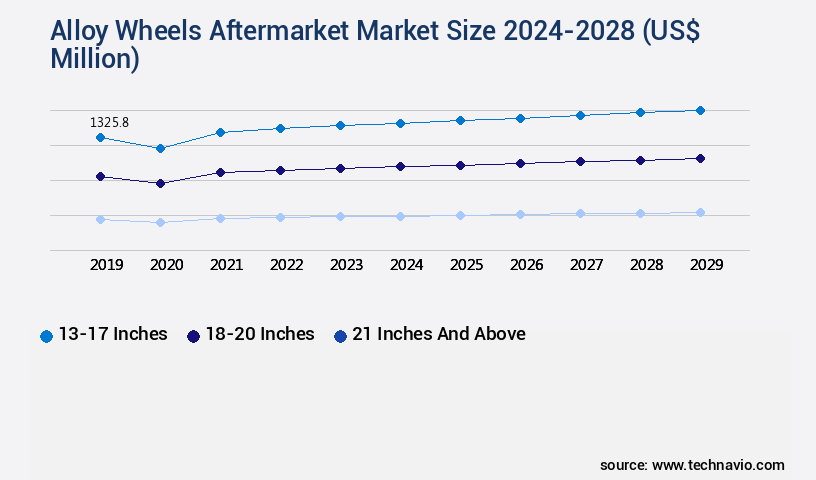

The 13-17 inches segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, driven by consumer preferences for wheel customization and advanced wheel technologies. Structural integrity, impact resistance, and finish customization are key focus areas for manufacturers, with vibration damping and warranty claims also under scrutiny. Distribution channels expand, with retail pricing strategies and profit margins influencing sales performance. Manufacturing automation, design for manufacturing, and wheel styling trends shape the market landscape. Product recalls due to wheel material strength and coating durability issues are mitigated through rigorous testing, including load capacity, heat dissipation, and fatigue life assessment. Quality control metrics such as wheel alignment systems, tire pressure monitoring, and surface finish quality are crucial for customer satisfaction.

The smaller 13-17 inch alloy wheels segment, accounting for a significant market share, offers benefits like faster road coverage, higher sustainability, and lower maintenance due to their smaller surface area and faster rotations. This segment's growth is further fueled by advancements in manufacturing processes, such as casting process optimization and corrosion resistance testing, ensuring machining tolerances and improving overall product lifecycle management.

The 13-17 inches segment was valued at USD 1284.90 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 54% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Alloy Wheels Aftermarket Market Demand is Rising in APAC Request Free Sample

The market in the Asia Pacific (APAC) region is experiencing robust growth, driven by the expanding automotive industry and the increasing demand for passenger and commercial vehicles. With improving socio-economic conditions in countries like China and India, consumers in the region have greater access to financing services, leading to a surge in automobile sales. The commercial vehicles sector, fueled by the burgeoning e-commerce logistics, construction, and mining industries, is a significant contributor to this growth. As a result, the demand for aftermarket components, including alloy wheels, is anticipated to increase substantially.

In fact, the sales of alloy wheels in APAC are projected to grow at an impressive pace, surpassing those in Europe and North America. The cost-effective manufacturing and the availability of a large consumer base make APAC an attractive market for alloy wheel manufacturers and suppliers.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global alloy wheel market continues to evolve as advancements in design, manufacturing, and distribution shape both performance and consumer demand. A key area of innovation is the effect of wheel design on vehicle handling, where aerodynamics and geometry significantly influence driving stability. Manufacturers are also focusing on the impact of manufacturing process on wheel strength, ensuring durability while maintaining lightweight structures. Assessments such as evaluation of alloy wheel fatigue life and assessment of surface coating corrosion resistance are becoming critical to extend product lifecycle and improve long-term reliability.

Ongoing optimization efforts target both performance and efficiency. The analysis of wheel alignment impact on tire wear and optimization of wheel design for aerodynamic performance directly connect to cost savings and enhanced vehicle safety. Equally important is the importance of wheel material selection on safety, where advanced alloys are being adopted for resilience and performance. On the operational side, strategies for enhancing wheel manufacturing efficiency and measures for improving alloy wheel quality control are helping manufacturers deliver consistent products while controlling costs.

The market also reflects broader business dynamics, such as the impact of supply chain management on wheel availability and the role of inventory management in minimizing stockouts, both crucial for aftermarket demand. Additionally, methods for improving customer service in aftermarket wheel sales and techniques for optimizing retail pricing for alloy wheels highlight the consumer-centric evolution of the sector. With trends shaped by assessment of consumer preference for alloy wheel styles and strengthened by digital marketing efforts, wheel brands are actively expanding visibility. Meanwhile, technical advances in relationship between wheel weight and fuel efficiency, methods for improving wheel balancing accuracy, and techniques for reducing wheel vibration continue to reinforce the link between engineering precision and end-user satisfaction.

What are the key market drivers leading to the rise in the adoption of Alloy Wheels Aftermarket Industry?

- The aging vehicle fleet serves as the primary catalyst for market growth.

- The global alloy wheels aftermarket is witnessing significant growth due to the increasing preference for alloy wheels over steel wheels in both passenger vehicles and commercial vehicles. With the average age of vehicles continuing to rise in regions like North America and Europe, the demand for alloy wheel replacements is on the rise. The durability and strength of alloy wheels, coupled with their lower weight, make them an attractive option for vehicle owners. Moreover, the availability of alloy wheels in various designs has fueled the interest of automotive enthusiasts, leading to increased demand.

What are the market trends shaping the Alloy Wheels Aftermarket Industry?

- Technological advancements are becoming the prevailing market trend. Or: The market trend is shifting towards technological advancements.

- Carbon fiber alloy wheels, known for their strength and lightweight properties, have expanded their applications beyond motorsport and aerospace industries. These wheels offer significant advantages over aluminum alloy wheels, particularly in terms of durability and performance. While aluminum alloy wheels can deform under light impact, carbon fiber alloy wheels maintain their integrity. Moreover, carbon fiber alloy wheels provide superior performance even when their weight is reduced by half compared to aluminum alloy wheels. This weight reduction results in improved fuel efficiency and faster vehicle acceleration.

- Their adoption can lead to substantial cost savings through reduced downtime and enhanced product performance. For instance, in the automotive industry, carbon fiber alloy wheels can decrease vehicle weight, resulting in a 10% improvement in fuel efficiency. Similarly, in the wind energy sector, carbon fiber alloy blades can increase wind turbine efficiency by up to 15%. By integrating carbon fiber alloy wheels into their offerings, businesses can cater to the growing demand for lightweight, durable, and high-performance components.

What challenges does the Alloy Wheels Aftermarket Industry face during its growth?

- The rise in OEM fitment demand poses a significant challenge to the industry's growth trajectory.

- Alloy wheels have gained significant traction in the automotive industry, with Original Equipment Manufacturers (OEMs) increasingly incorporating them into their vehicles. This trend is noticeable even in lower-variant models, posing a challenge to aftermarket alloy wheel suppliers. In mature markets like the US and Europe, where alloy wheels are commonplace in all vehicle variants, expansion opportunities for aftermarket suppliers are limited. The shift towards alloy wheels is primarily driven by demographic changes and evolving consumer preferences.

Exclusive Technavio Analysis on Customer Landscape

The alloy wheels aftermarket market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the alloy wheels aftermarket market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Alloy Wheels Aftermarket Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, alloy wheels aftermarket market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ALCAR HOLDING GMBH - This company specializes in the production and distribution of high-performance alloy wheels, including AEZ, DOTZ, DEZENT, and DOTZ SURVIVAL. Their product line caters to the automotive industry, providing durable and stylish options for various vehicle applications. The company's commitment to innovation and quality sets it apart in the market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALCAR HOLDING GMBH

- BORBET GmbH

- ENKEI WHEELS India Ltd.

- Forgiato

- Howmet Aerospace Inc.

- Lenso Wheels

- LKQ Corp.

- Neo Wheels Ltd.

- RONAL AG

- Steel Strips Wheels Limited

- The Carlstar Group LLC

- Wheel Pros LLC

- YHI INTERNATIONAL Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Alloy Wheels Aftermarket Market

- In August 2024, global automotive component manufacturer, Aptiv PLC, announced the acquisition of a leading alloy wheel supplier, BBS AG, for approximately €1.1 billion. This strategic move aimed to strengthen Aptiv's presence in the high-performance wheel market and expand its product offerings (Aptiv press release).

- In November 2024, German automaker, BMW Group, unveiled its new iX3 SUV, featuring lightweight alloy wheels made from recycled aluminum. This initiative marked a significant step towards sustainable manufacturing in the alloy wheels aftermarket (BMW Group press release).

- In March 2025, US-based alloy wheel manufacturer, American Racing, entered into a partnership with Chinese automaker, Geely Auto Group, to supply custom alloy wheels for Geely's new luxury brand, Zeekr. This geographic expansion into the Chinese market represents a substantial growth opportunity for American Racing (Geely Auto Group press release).

- In May 2025, the European Union's REACH regulation introduced new standards for the production, use, and disposal of alloy wheels containing hazardous substances. This regulatory change will drive manufacturers to invest in research and development of eco-friendly alloy wheel technologies (European Chemicals Agency press release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Alloy Wheels Aftermarket Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.36% |

|

Market growth 2024-2028 |

USD 680.4 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

4.11 |

|

Key countries |

China, US, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The alloy wheels aftermarket continues to evolve, driven by consumer preferences for customization and performance enhancements. Vibration damping technology, for instance, is a key trend, with manufacturers focusing on reducing unwanted wheel vibrations for improved ride comfort. Warranty claims related to impact resistance and structural integrity remain a concern, necessitating rigorous testing and supply chain management. Finish customization, aided by advanced coating durability and manufacturing automation, is another significant area of growth. Distributors employ dynamic load simulation and design for manufacturing to optimize production processes and meet retail pricing strategies. Consumer preferences for lighter wheels have led to innovations in wheel weight reduction, while heat dissipation and load capacity testing ensure optimal performance.

- An example of this market's sales performance can be seen in the automotive industry, where aftermarket alloy wheel sales increased by 5% in the last fiscal year. Industry growth is expected to continue, with a projected expansion of 3% annually. However, challenges such as product recalls due to wheel balancing issues and customer satisfaction concerns related to surface finish quality persist. Manufacturers invest in quality control metrics, wheel alignment systems, and tire pressure monitoring to mitigate these risks. Aerodynamic design, fatigue life assessment, and product lifecycle management are also crucial aspects of the market, ensuring the long-term profitability of businesses in this sector.

- Innovations in casting process optimization and corrosion resistance testing further enhance the alloy wheels' structural integrity and durability. Manufacturers must also address machining tolerances and dynamic load simulation to meet evolving consumer demands and maintain a competitive edge.

What are the Key Data Covered in this Alloy Wheels Aftermarket Market Research and Growth Report?

-

What is the expected growth of the Alloy Wheels Aftermarket Market between 2024 and 2028?

-

USD 680.4 million, at a CAGR of 4.36%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (13-17 inches, 18-20 inches, and 21 inches and above), Vehicle Type (Passenger vehicle and Commercial vehicle), and Geography (APAC, Europe, North America, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Aging vehicle fleet, Increase in OEM fitment

-

-

Who are the major players in the Alloy Wheels Aftermarket Market?

-

ALCAR HOLDING GMBH, BORBET GmbH, ENKEI WHEELS India Ltd., Forgiato, Howmet Aerospace Inc., Lenso Wheels, LKQ Corp., Neo Wheels Ltd., RONAL AG, Steel Strips Wheels Limited, The Carlstar Group LLC, Wheel Pros LLC, and YHI INTERNATIONAL Ltd.

-

Market Research Insights

- The market for aftermarket alloy wheels is a dynamic and continually evolving industry. According to industry reports, the market is expected to grow by approximately 5% annually over the next decade. One notable trend in this market is the increasing demand for lightweight and fuel-efficient alloy wheels, leading to sales increases in this segment. For instance, a leading automotive manufacturer reported a 7% rise in sales of lightweight alloy wheels last year.

- Additionally, advancements in material science applications and manufacturing processes contribute to the industry's ongoing growth and innovation.

We can help! Our analysts can customize this alloy wheels aftermarket market research report to meet your requirements.

RIA -

RIA -