Analog Semiconductor Market Size 2026-2030

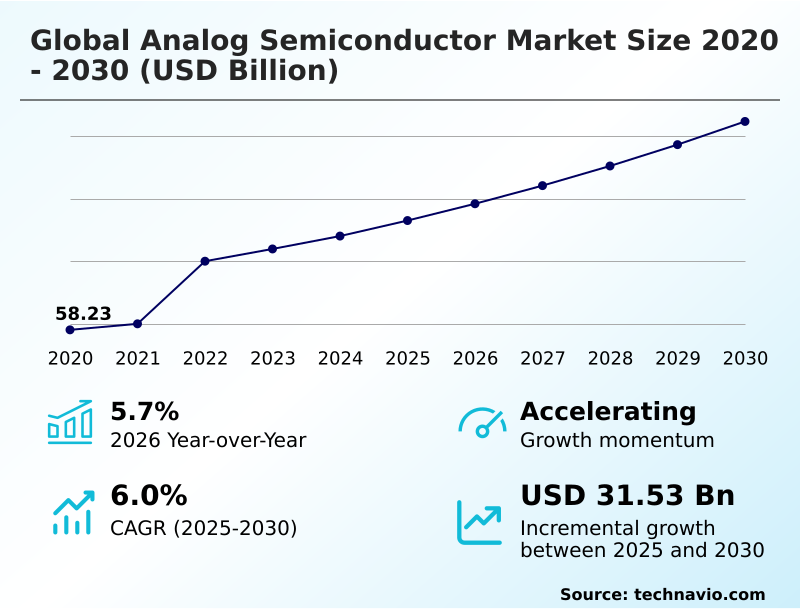

The analog semiconductor market size is valued to increase by USD 31.53 billion, at a CAGR of 6% from 2025 to 2030. Acceleration of automotive electrification and zonal architectures will drive the analog semiconductor market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 47.3% growth during the forecast period.

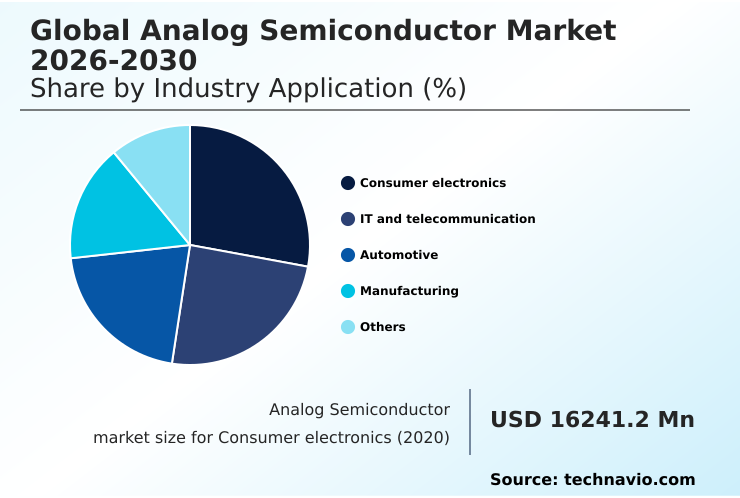

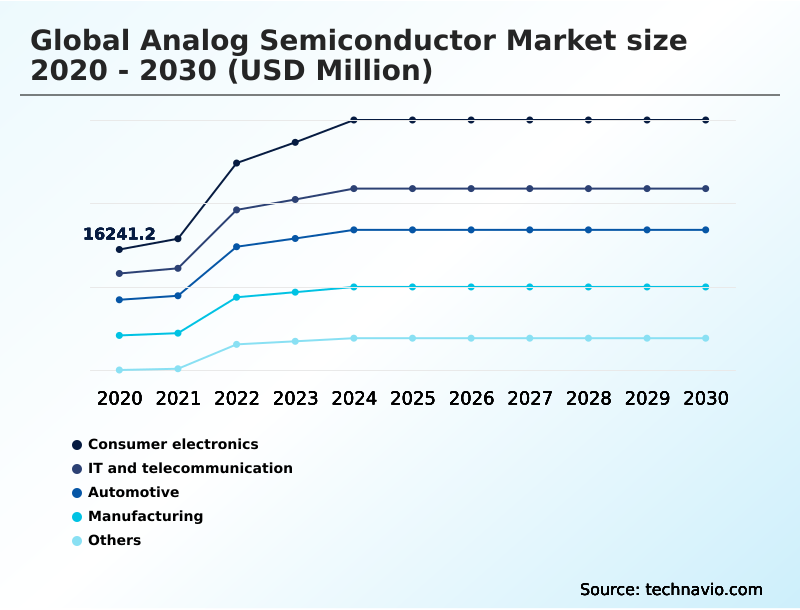

- By Industry Application - Consumer electronics segment was valued at USD 26.84 billion in 2024

- By Type - General purpose segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 66.31 billion

- Market Future Opportunities: USD 31.53 billion

- CAGR from 2025 to 2030 : 6%

Market Summary

- The analog semiconductor market is foundational to modern electronics, acting as the critical interface between the digital and physical worlds. Its trajectory is defined by increasing demand from the automotive, industrial, and communications sectors, where precision and reliability are paramount.

- The transition to electric vehicles, for instance, requires a host of advanced analog components, including robust power management units and high-fidelity signal chain components to manage battery systems and powertrain controls. Similarly, the expansion of 5G infrastructure and AI-driven data centers fuels the need for sophisticated mixed-signal ICs and power management ICs that deliver high performance with exceptional energy efficiency.

- In industrial automation, sensor interface chips and precise operational amplifiers are essential for robotics and process control. The industry continually innovates with materials like silicon carbide (SiC) and gallium nitride (GaN), alongside advanced system-in-package designs, to meet the complex requirements of these evolving applications.

- This focus on integrating more functionality into smaller footprints while improving power density and signal integrity underscores the market's enduring importance.

What will be the Size of the Analog Semiconductor Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Analog Semiconductor Market Segmented?

The analog semiconductor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Industry application

- Consumer electronics

- IT and telecommunication

- Automotive

- Manufacturing

- Others

- Type

- General purpose

- Application specific

- Form factor

- Integrated circuits

- Discrete components

- Geography

- APAC

- China

- South Korea

- Japan

- Europe

- UK

- Germany

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Industry Application Insights

The consumer electronics segment is estimated to witness significant growth during the forecast period.

The consumer electronics segment remains a foundational pillar, driven by the demand for energy efficiency and feature integration in portable devices. The role of analog components is critical, handling functions from sound amplification to data conversion.

A key trend is the miniaturization of power management integrated circuits (PMICs) to fit shrinking device form factors. Manufacturers are developing high-efficiency regulators to minimize thermal dissipation, a crucial factor for wearable technology.

The proliferation of IoT has also spurred demand for ultra-low-power analog interfaces and power management units for extended battery life.

Furthermore, haptic feedback integration, where precise analog drivers and signal chain components create tactile sensations, has improved user engagement in gaming applications by over 15%, requiring advanced analog signal processing and display drivers.

The Consumer electronics segment was valued at USD 26.84 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 47.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Analog Semiconductor Market Demand is Rising in APAC Get Free Sample

The geographic landscape is undergoing significant realignment, with APAC emerging as the central driver of both production and demand, accounting for nearly 47.3% of the market's incremental growth.

This dominance is reinforced by a strategic diversification of supply chains, exemplified by the establishment of India's first commercial semiconductor fabrication facility to produce power management units and sensor interface chips on legacy technology nodes.

This 'China Plus One' strategy creates a resilient, multi-polar network. While established hubs in Taiwan and South Korea focus on high-end mixed-signal ICs and power transistors, emerging regions are building capacity.

The region’s growth rate, projected to be 1.1 times that of North America, underscores its pivotal role.

This evolution away from a monolithic manufacturing bloc toward specialized regional hubs is reshaping global supply dynamics for essential components like power regulation chips.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global analog semiconductor market is navigating a complex landscape shaped by several strategic imperatives. The intense focus on analog semiconductors for automotive electrification is a primary growth engine, driving innovation in areas like high-voltage gate drivers for SiC and imaging radar processors for autonomous driving.

- This demand highlights the impact of zonal architectures on semiconductors, pushing for more integrated and efficient designs. Concurrently, the industry is grappling with the talent gap in analog semiconductor design and the high capital expenditure for analog fabs, which are significant analog IC design complexity challenges. In response, some firms are exploring open-source hardware for analog design to foster innovation.

- A key trend is the transition to 300mm wafer manufacturing for analog, which promises cost per die reduction 300mm wafer. This shift is critical for addressing power density in data center ICs and enabling high-volume production of power management ICs in consumer electronics.

- The adoption of wide-bandgap materials in power conversion and development of power architectures for AI infrastructure are also vital. In mobile applications, the RF front end for mobile devices and mixed-signal ICs for 5G communication are key focus areas. For medical technology, the analog front-end for medical imaging remains a specialized growth segment.

- Strategically, OEMs that prioritize the localization of automotive chip supply are reporting lead time reductions of over 30%, showcasing the benefits of regionalized manufacturing, which complements efforts in legacy node manufacturing for industrial ICs and enhancing high-speed video connectivity in vehicles.

What are the key market drivers leading to the rise in the adoption of Analog Semiconductor Industry?

- The acceleration of automotive electrification and the adoption of zonal architectures are primary drivers, creating exponential demand for high-performance analog components in vehicle systems.

- The primary driver for the market is the accelerating transition to automotive electrification. The shift to electric vehicles increases the analog semiconductor content per vehicle by more than 50% compared to internal combustion engine models.

- This surge is due to the complex requirements of battery management systems, traction inverters, and on-board chargers, all of which depend on high-performance analog ICs such as precision data converters and operational amplifiers.

- The adoption of wide-bandgap materials is also critical; specialized gate drivers for silicon carbide (SiC) components, for instance, enable a 10% gain in powertrain efficiency.

- Furthermore, the migration toward zonal architectures is increasing the need for smart power distribution and high-speed analog communication transceivers, including those supporting advanced automotive networking protocols.

What are the market trends shaping the Analog Semiconductor Industry?

- A strategic shift toward 300mm wafer manufacturing is fundamentally reshaping the market. This transition drives economies of scale and creates significant competitive advantages for capital-rich leaders.

- A fundamental trend reshaping the competitive landscape is the strategic shift to 300-millimeter wafer manufacturing. This move enables massive economies of scale, with manufacturing on 300mm wafers more than doubling the chip output per wafer compared to legacy 200mm facilities. This transition is critical for meeting volume demand from the automotive and industrial sectors for components like power management units.

- Furthermore, this advanced manufacturing process allows for the integration of more complex digital logic with analog circuits, a key requirement for modern mixed-signal ICs and system-in-package designs. The adoption of advanced mixed-signal ICs is improving system-level power efficiency by up to 15%, a crucial metric for battery-powered devices and data centers.

- This trend enables the production of sophisticated power transistors and signal chain components with enhanced performance.

What challenges does the Analog Semiconductor Industry face during its growth?

- A widening talent gap, compounded by increasing technical complexity in analog design, presents a significant challenge to innovation and growth across the industry.

- A critical challenge constraining market growth is the severe shortage of specialized engineering talent for analog design. Unlike digital design, which is highly automated, analog design remains a manual, experience-driven process. This talent deficit is extending product development timelines by an average of 15% for complex system-on-chip projects.

- In response, some companies are resorting to 'acqui-hiring,' a strategy that can accelerate project kick-off times by over 40% compared to traditional recruitment cycles. This issue is compounded by the high capital expenditure associated with manufacturing, as building a new 300mm fab can cost upwards of 2.5 times more than a 200mm equivalent.

- These factors create significant barriers to entry and innovation, particularly for developing complex sensor interface chips and RF transceivers.

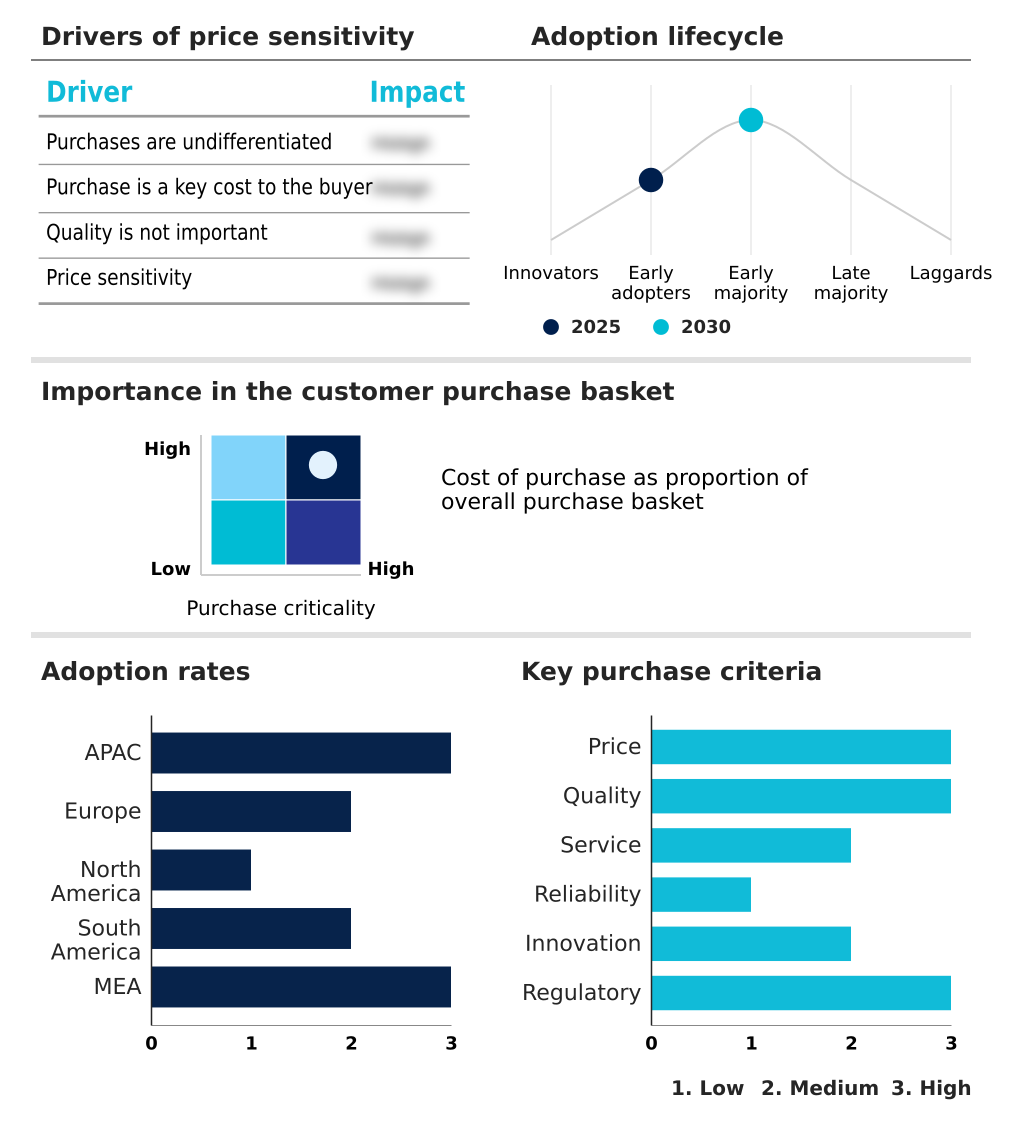

Exclusive Technavio Analysis on Customer Landscape

The analog semiconductor market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the analog semiconductor market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Analog Semiconductor Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, analog semiconductor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Analog Devices Inc. - Offerings include high-performance analog and mixed-signal integrated circuits, encompassing precision data converters, amplifiers, and power management solutions for critical industrial and communication applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Analog Devices Inc.

- Applied Materials Inc.

- Chiplogic Technologies

- Continental Device India Ltd.

- eInfochips Pvt. Ltd.

- Emerson Electric Co.

- Infineon Technologies AG

- Kistler Group

- MediaTek Inc.

- Microchip Technology Inc.

- Micron Technology Inc.

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Qorvo Inc.

- Qualcomm Inc.

- Renesas Electronics Corp.

- Semtech Corp.

- Taiwan Semiconductor Co. Ltd.

- Texas Instruments Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Analog semiconductor market

- In August, 2025, Infineon Technologies AG acquired a specialized engineering unit to create a new Ethernet Solutions business line, bringing in approximately 400 skilled employees to strengthen its automotive capabilities.

- In June, 2025, Texas Instruments Inc. strategically increased prices across more than 3,000 analog integrated circuit part numbers, signaling a focus on profitability and market stabilization.

- In May, 2025, NXP Semiconductors NV launched the S32R47 imaging radar processor, a device specifically engineered to enhance detection capabilities for Level 2+ autonomous driving systems.

- In March, 2025, STMicroelectronics launched a new series of high-voltage galvanically isolated gate drivers engineered to optimize the performance of silicon carbide MOSFETs in electric vehicle traction inverters.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Analog Semiconductor Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6% |

| Market growth 2026-2030 | USD 31527.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.7% |

| Key countries | China, Taiwan, South Korea, Japan, India, Indonesia, UK, Germany, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The analog semiconductor market is defined by a strategic push toward technological sovereignty and higher-value applications. Boardroom decisions are increasingly focused on mitigating supply chain risks through investments in 300-millimeter wafer fabrication, which directly impacts long-term cost structures and competitive positioning.

- This is driven by the need for advanced components like high-voltage galvanically isolated gate drivers and imaging radar processors, particularly for automotive applications utilizing silicon carbide (SiC) and gallium nitride (GaN). The core of product development revolves around precision data converters, power management ICs, operational amplifiers, and other signal chain components.

- Innovations in analog design, supported by electronic design automation, are essential to manage high-speed signal integrity in automotive networking. The market encompasses everything from RF transceivers, sensor interface chips, and microcontrollers to discrete power transistors and transient voltage suppressors. Advanced packaging, including wafer-level chip-scale packaging, ball grid arrays, and system-in-package on a monolithic substrate, is critical.

- Key products such as power management units, gate drivers, display drivers, and power regulation chips are in high demand.

- Strategic repricing on legacy interface chips and low-dropout regulators has improved margins by an average of 10% on select product families, reflecting a mature market balancing volume and profitability for items like automotive-grade gate drivers, high-speed video connectivity solutions, and analog front-end for CMOS image sensors.

What are the Key Data Covered in this Analog Semiconductor Market Research and Growth Report?

-

What is the expected growth of the Analog Semiconductor Market between 2026 and 2030?

-

USD 31.53 billion, at a CAGR of 6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Industry Application (Consumer electronics, IT and telecommunication, Automotive, Manufacturing, and Others), Type (General purpose, and Application specific), Form Factor (Integrated circuits, and Discrete components) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Acceleration of automotive electrification and zonal architectures, Widening talent gap and technical complexity

-

-

Who are the major players in the Analog Semiconductor Market?

-

Analog Devices Inc., Applied Materials Inc., Chiplogic Technologies, Continental Device India Ltd., eInfochips Pvt. Ltd., Emerson Electric Co., Infineon Technologies AG, Kistler Group, MediaTek Inc., Microchip Technology Inc., Micron Technology Inc., NXP Semiconductors NV, ON Semiconductor Corp., Qorvo Inc., Qualcomm Inc., Renesas Electronics Corp., Semtech Corp., Taiwan Semiconductor Co. Ltd. and Texas Instruments Inc.

-

Market Research Insights

- The market's momentum is propelled by automotive electrification and the adoption of zonal architectures, which improve vehicle efficiency, with some implementations reducing wiring complexity by over 20%. Demand from AI-driven data centers for efficient data center power management and from 5G/6G communications for high-speed connectivity is also a key factor.

- Trends include a shift toward open-source analog design and the use of automotive analog solutions and industrial power control. Innovations in healthcare technology sensing and manufacturing sensing solutions are expanding applications. Key components include automotive mixed signal devices, RF power amplifiers, and connectivity front end modules. Technology drivers like 3D radars, MEMS microphones, and 3D ToF image sensors are crucial.

- Development of electric vehicle traction inverters for 800-volt architectures and advanced power management integrated circuits (PMICs) that improve battery life by 15% are notable. The market relies on embedded processing chips, signal integrity ICs, and specialty memory components, all supported by an expanding semiconductor fabrication facility infrastructure focused on both advanced and legacy technology nodes.

We can help! Our analysts can customize this analog semiconductor market research report to meet your requirements.

RIA -

RIA -