North America Arachidonic Acid Market Size 2024-2028

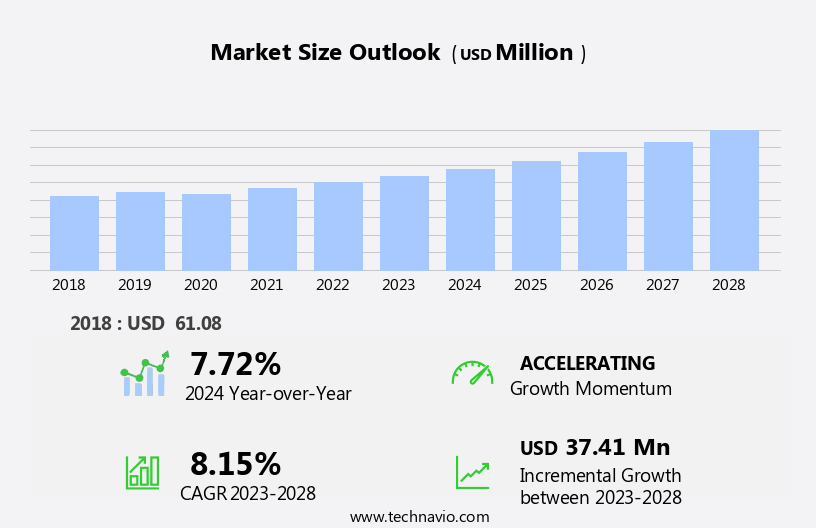

The North America arachidonic acid market size is forecast to increase by USD 37.41 million at a CAGR of 8.15% between 2023 and 2028. The market is witnessing significant growth due to the increasing demand for nutritional supplements, particularly those containing Docosahexaenoic acid (DHA) and other polyunsaturated fatty acids. Arachidonic acid plays a crucial role in brain cell development and muscle function in mammals, making it an essential nutrient for infants and athletes. The availability of various sources, such as fish, poultry meat, and phospholipids, has expanded the market's reach. Moreover, the esterified form of arachidonic acid in glycerol is gaining popularity due to its improved bioavailability. Additionally, the gallbladder membrane and proteins containing arachidonic acid are used in various applications, including pharmaceuticals and cosmetics.

Furthermore, the e-commerce channels' growing popularity and the availability of several alternatives, such as linoleic acid and eicosapentaenoic acid, pose challenges to the market's growth. Nonetheless, the market's potential for innovation and the rising awareness of the health benefits of arachidonic acid are expected to drive its growth in the coming years.

Arachidonic acid, an omega-6 fatty acid, plays a crucial role in the production of eicosanoids, which are essential signaling molecules with anti-inflammatory properties. In North America, arachidonic acid is widely used in various applications, including infant nutrition products. It is available in different forms such as solid form, powder form, crystalline form, and liquid form. Arachidonic acid is vital for brain development and visual acuity in infants. It is a key component of phospholipids in cell membranes, including those in brain cells and the gallbladder membrane. The omega-6 group, which includes arachidonic acid, is essential for cell survival and maintenance of cellular functions.

Furthermore, Mortierella alpine, a microorganism, is used for the commercial production of arachidonic acid. Arachidonic acid is found naturally in various food sources such as poultry, meat, fish, and eggs proteins. It is also used as a dietary supplement in the form of phosphate or calcium levels to enhance its bioavailability. Arachidonic acid is also used in the production of docosahexaenoic acid (DHA) for various applications.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Infant formula

- Others

- Source

- Plant source

- Animal source

- Geography

- North America

- Canada

- Mexico

- US

- North America

By Application Insights

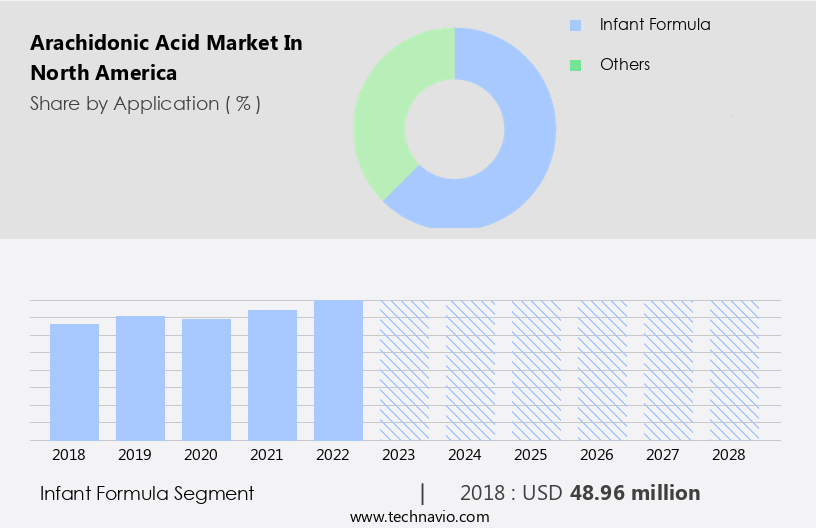

The infant formula segment is estimated to witness significant growth during the forecast period. Arachidonic acid, a vital fatty acid belonging to the Omega-6 group, holds significant importance in various end-use industries, particularly in North America. This essential fatty acid plays a crucial role in brain development and visual acuity, making it an integral component of numerous nutritional products. It is a key constituent of phospholipids in cell membranes and is essential for neuron growth and cell survival. Mortierella alpine, a unicellular organism, is a primary source for commercial production of arachidonic acid. The solvent segment dominates the production process due to its high efficiency and cost-effectiveness. In the health and nutrition sector, arachidonic acid finds extensive applications in sports supplements and infant food.

Furthermore, in 2023, infant food was the leading application segment, driven by the growing use in infant formula products and the increasing demand for these products. Arachidonic acid is essential for infant growth and development, as it is an integral part of human milk and cannot be produced by the human body. Thus, infant formula manufacturers incorporate arachidonic acid to meet the metabolic requirements of infants. Additionally, calcium levels in the brain are regulated by arachidonic acid, making it a vital nutrient for brain health.

Get a glance at the market share of various segments Request Free Sample

The infant formula segment accounted for USD 48.96 million in 2018 and showed a gradual increase during the forecast period.

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Rising demand for sports supplements is the key driver of the market. Arachidonic acid, an Omega-6 fatty acid, is a crucial component of eicosanoids, which possess anti-inflammatory properties. The rising awareness regarding health and wellness among individuals aged 20-40 years, particularly those engaged in fitness training, bodybuilding, and sports specialization, is fueling the demand for arachidonic acid in North America.

Furthermore, this essential fatty acid is utilized in the production of infant formula and various infant nutrition products, available in solid form, powder form, crystalline form, liquid form, and oil-based solutions. The sources of arachidonic acid include plant-based sources like algae and fungi, as well as animal-derived products. The increasing preference for plant-based diets and the growing interest in natural health supplements are expected to boost the demand for arachidonic acid derived from plant sources during the forecast period.

Market Trends

E-commerce channels gaining popularity is the upcoming trend in the market. Arachidonic acid, an omega-6 fatty acid, is a crucial component of eicosanoids, which are essential for inflammatory and immune responses. Arachidonic acid is available in various forms, including solid form (powder), crystalline form, liquid form (oil-based solutions), and plant-based sources such as algae and fungi, as well as animal-derived products. In North America, arachidonic acid is extensively used in infant formula and nutrition products due to its anti-inflammatory properties. The market for arachidonic acid in North America is growing due to increasing consumer awareness of its health benefits and the expanding application base in various industries, including food and beverages, pharmaceuticals, and cosmetics.

Furthermore, online platforms have become a popular channel for selling arachidonic acid-containing products due to their convenience and the ability to reach a large consumer base directly. Consumers can purchase arachidonic acid in various forms, including powder, crystalline, oil-based solutions, and liquid form, from reputable companies online. The market is expected to witness steady growth in the coming years, driven by increasing demand for functional foods and beverages and the expanding application base in various industries.

Market Challenge

Availability of several alternatives for arachidonic acid is a key challenge affecting the market growth. Arachidonic acid is a significant Omega-6 polyunsaturated fatty acid with essential roles in various physiological functions, primarily due to its role in the production of eicosanoids, which exhibit anti-inflammatory properties. Arachidonic acid is found in both animal-derived and plant-based sources, including fish, eggs, and meat, as well as in some plant sources like algae and fungi. In the food industry, arachidonic acid is available in various forms, such as solid form, powder form, crystalline form, liquid form, and oil-based solutions, for use in infant formula and other infant nutrition products. However, arachidonic acid faces competition from its substitutes like linoleic acid, alpha-linolenic acid, Y-linolenic acid, leukotriene, and docosapentaenoic acid.

Furthermore, these substitutes, which can be easily sourced from plant-based sources, can replace arachidonic acid in various applications, including food and beverage and pharmaceutical products. Despite this competition, the demand for arachidonic acid remains strong due to its unique properties and applications.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Avantor Inc. - The company offers arachidonic acid with high purity and consistent quality for research purposes.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BASF SE

- Bio Techne Corp.

- Biosynth Ltd.

- Cargill Inc.

- Cayman Chemical

- Croda International Plc

- Koninklijke DSM NV

- LGC Science Group Holdings Ltd.

- Merck KGaA

- Parchem Fine and Specialty Chemicals Inc.

- PerkinElmer Inc.

- Selleck Chemicals LLC

- Sisco Research Laboratories Pvt. Ltd.

- Spectrum Laboratory Products Inc.

- Thermo Fisher Scientific Inc.

- Tokyo Chemical Industry Co. Ltd.

- Wanrun Co. Ltd.

- Xiamen Jindawei Group Co. Ltd.

- Zhejiang Tianhecheng Bio technology Shares Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Arachidonic acid is a polyunsaturated omega-6 fatty acid with an essential role in the production of eicosanoids, which are signaling molecules involved in various physiological processes. It is found in cell membranes of mammals, including the brain and eyes, and plays a crucial role in brain development, visual acuity, neuron growth, and cell survival. Arachidonic acid is available in various forms, including solid form (powder), crystalline form, liquid form (oil-based solutions), and oil-based products. Plant-based sources of arachidonic acid include algae, fungi, and certain plant-based oils such as those derived from Mortierella alpine. Animal-derived products, such as poultry, meat, eggs, and seafood, are also rich sources of arachidonic acid.

Furthermore, arachidonic acid is used in infant formula and infant nutrition products for its role in brain and nervous system development. Arachidonic acid is also used in sports supplements and nutritional products for its anti-inflammatory properties, muscle hypertrophy, muscle gain, and muscle inflammation. It is used in bodybuilding supplements, sports drinks, and other health supplements for various health benefits, including memory, eyesight, cognitive function, and immune system support. Arachidonic acid is also used in the treatment of brain diseases, depression, and other health conditions. Arachidonic acid is produced from the metabolism of linoleic acid, an essential fatty acid found in various plant-based sources such as nuts, seeds, legumes, grains, and vegetable oils.

Moreover, it is also found in phospholipids in the gallbladder membrane and proteins in various tissues. The solvent segment is the major market for arachidonic acid, with demand coming from various industries, including sports nutrition, newborn nutrition, baby nutrition, and diabetes treatment.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

146 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.15% |

|

Market growth 2024-2028 |

USD 37.41 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.72 |

|

Key companies profiled |

Avantor Inc., BASF SE, Bio Techne Corp., Biosynth Ltd., Cargill Inc., Cayman Chemical, Croda International Plc, Koninklijke DSM NV, LGC Science Group Holdings Ltd., Merck KGaA, Parchem Fine and Specialty Chemicals Inc., PerkinElmer Inc., Selleck Chemicals LLC, Sisco Research Laboratories Pvt. Ltd., Spectrum Laboratory Products Inc., Thermo Fisher Scientific Inc., Tokyo Chemical Industry Co. Ltd., Wanrun Co. Ltd., Xiamen Jindawei Group Co. Ltd., and Zhejiang Tianhecheng Bio technology Shares Co. Ltd. |

|

Market dynamics |

Parent market analysis, market forecast, market growth inducers and obstacles,market forecast , fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -