Articulated Robots Market Size 2024-2028

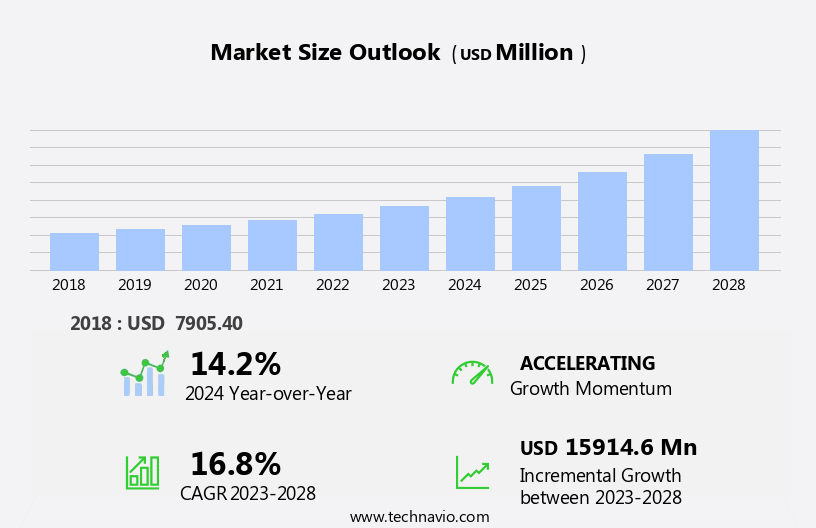

The articulated robots market size is forecast to increase by USD 15.91 billion, at a CAGR of 16.8% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing benefits they offer over traditional industrial robots. Articulated robots, with their high degree of flexibility and ability to move in complex workspaces, are increasingly being adopted for applications in industries such as automotive, electronics, and food and beverage. A notable trend in the market is the emergence of open-source articulated robots, which are driving innovation and reducing entry barriers for small and medium-sized enterprises. However, the market is not without challenges. Increased competition from SCARA (Selective Compliance Assembly Robot Arm) robots, which offer simpler and more cost-effective solutions for specific applications, is putting pressure on articulated robot manufacturers to differentiate their offerings.

- Additionally, the complexity of articulated robots, which require more advanced programming and maintenance, presents a challenge for some organizations. Companies seeking to capitalize on the opportunities in the market must focus on offering unique value propositions, investing in research and development, and providing robust support services to customers.

What will be the Size of the Articulated Robots Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and increasing demand for automation across various sectors. Articulated robots, with their high degrees of freedom, are particularly well-suited for applications in pick and place, machine tending, painting, welding, and assembly lines. These robots are integral to industrial automation, enabling productivity gains and cost reduction. Deep learning algorithms and computer vision systems enhance the capabilities of articulated robots, enabling human-robot collaboration and improving safety features. Motion control and joint torque technologies enable more precise and efficient operations, while industry associations and academic institutions drive research and innovation in robotics.

Robotics research focuses on improving payload capacity, ease of use, and intuitive programming, as well as developing collaborative robots and artificial intelligence (AI) applications. Quality control and safety standards are essential considerations, with safety features and collision detection systems ensuring a safe work environment. Material handling applications, such as pallet handling, benefit from the flexibility and adaptability of articulated robots. Simulation software and offline programming enable efficient design and commissioning, while SCADA systems and PLC control provide real-time monitoring and control. Government funding and standards organizations support the ongoing development of the market, ensuring its continued growth and evolution.

How is this Articulated Robots Industry segmented?

The articulated robots industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

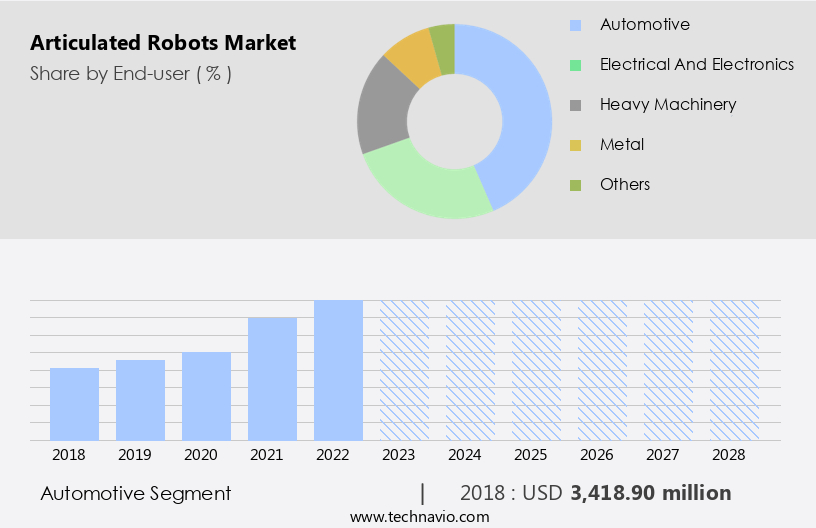

- Automotive

- Electrical and electronics

- Heavy machinery

- Metal

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

.

By End-user Insights

The automotive segment is estimated to witness significant growth during the forecast period.

The market continues to gain momentum in the US industrial sector, particularly in the automotive industry, which remains a significant contributor. Articulated robots offer several advantages over traditional tooling and fixtures, including cost reduction, increased productivity, and improved ease of use. These robots are renowned for their high degrees of freedom, enabling them to execute complex tasks with precision and flexibility. Articulated robots are integral to various applications within the automotive industry, such as welding, pallet handling, machine tending, and painting. Collaborative robots, a subset of articulated robots, facilitate human-robot interaction, enhancing productivity and safety.

Machine learning and artificial intelligence (AI) technologies are increasingly integrated into these robots, enabling advanced capabilities like deep learning and computer vision. Safety features and standards, such as force feedback and collision detection, ensure a safe work environment. Offline programming and virtual commissioning streamline the setup process, while SCADA systems and PLC control provide seamless integration with industrial automation systems. Additionally, data analytics, digital twins, and cloud connectivity enable remote monitoring and predictive maintenance. The global market for articulated robots is expected to grow, driven by the increasing demand for automation in various industries, including material handling, assembly lines, and quality control.

Robotics research and government funding further fuel the innovation and development of advanced robotic technologies.

The Automotive segment was valued at USD 3.42 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

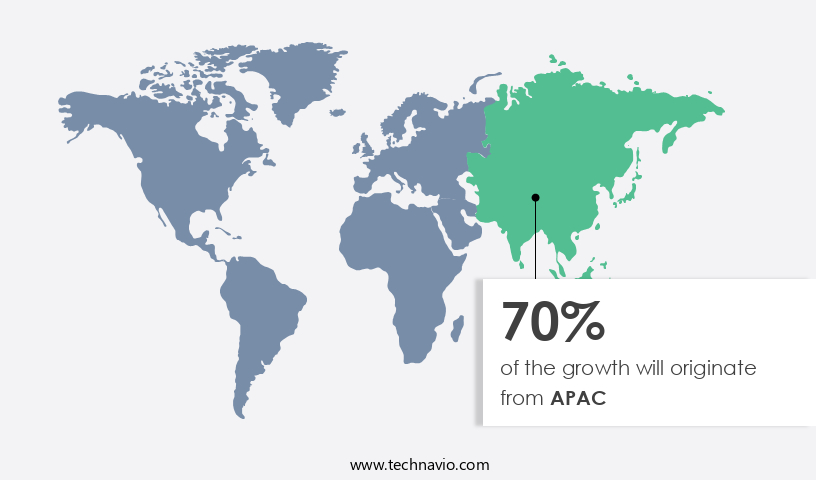

APAC is estimated to contribute 70% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The global market for articulated robots is witnessing significant growth, particularly in the Asia Pacific (APAC) region. APAC is currently the largest market for articulated robots, driven by countries such as China, Japan, South Korea, Singapore, and India. This region is home to several established players in the market, including FANUC, Yaskawa Electric, Kawasaki Heavy Industries Ltd., Mitsubishi Electric Corp., and Seiko Holdings. The adoption of articulated robots is predominantly driven by industries such as automotive, electronics, and metal in APAC. Articulated robots offer numerous benefits, including productivity gains, ease of use, and intuitive programming. They come with varying degrees of freedom and payload capacities, making them suitable for a wide range of applications.

End-of-arm tooling, force feedback, and human-robot collaboration are essential features that are increasingly being integrated into articulated robots. Machine learning, machine tending, offline programming, virtual commissioning, and plc control are some of the advanced technologies that are transforming the market. Collaborative robots, artificial intelligence, and computer vision are also gaining popularity in various industries. Safety standards, industrial automation, scada systems, and safety features are crucial considerations in the adoption of articulated robots. Data analytics, digital twins, and cloud connectivity are some of the emerging trends in the market. Cost reduction, return on investment, and collision detection are key factors that influence the purchasing decisions of businesses.

Government funding and robotics research are also playing a significant role in the growth of the market. Applications in painting, welding, pallet handling, pick and place, and deep learning are some of the areas where articulated robots are being increasingly used. The market is expected to continue growing, driven by the increasing demand for automation and the need for greater efficiency and productivity.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Articulated Robots Industry?

- The significant advantages of articulated robots serve as the primary catalyst for market growth.

- Articulated robots have become increasingly popular in the industrial automation sector due to their ability to enhance production efficiency, improve product quality, and ensure safety standards. With labor costs rising and competition intensifying from low-wage overseas locations, the demand for automation solutions, particularly articulated robots, is on the rise. These robots offer several advantages over traditional manufacturing methods, including increased precision, reliability, and performance. Safety is a significant concern in industrial automation, and articulated robots are equipped with advanced safety features such as collision detection systems and work envelope protection. SCADA systems and data analytics enable real-time monitoring and optimization of production processes, while digital twins provide a virtual representation of the manufacturing environment for predictive maintenance and troubleshooting.

- Articulated robots are extensively used in various industries, including assembly lines, pallet handling, and material handling, to streamline operations and reduce manual labor. Cloud connectivity enables remote monitoring and control, providing greater flexibility and reducing the need for on-site personnel. The investment in articulated robots offers a substantial return on investment through increased productivity, reduced downtime, and improved product quality. In conclusion, the adoption of articulated robots in the industrial sector is driven by the need for faster, more efficient, and precise manufacturing processes. These robots offer several advantages, including safety features, advanced technology, and cost savings.

- As the industrial landscape continues to evolve, the use of articulated robots is expected to become even more widespread.

What are the market trends shaping the Articulated Robots Industry?

- Open-source articulated robots are currently gaining popularity in the market. This trend reflects the increasing demand for flexible and customizable automation solutions.

- The market is witnessing significant advancements, with a focus on enhancing capabilities in areas such as pick and place, deep learning, and motion control. Robots are increasingly being integrated into industries for material handling, quality control, and research purposes. Academic institutions and industry associations are collaborating to drive innovation in robotics, with a particular emphasis on computer vision and simulation software. Government funding and industry investments are propelling research in this field, leading to improvements in payload capacity and the development of more immersive and harmonious robot designs.

- Open-source articulated robots, such as those developed by Comau Spa, are gaining popularity due to their compatibility with third-party applications and open development environments. These robots offer a unique opportunity for businesses to test and simulate various applications before implementation. Overall, the market is poised for continued growth and innovation.

What challenges does the Articulated Robots Industry face during its growth?

- The growth of the industry is being significantly impacted by the intensified competition from SCARA robots, which has emerged as a key challenge.

- Articulated robots, a type of industrial robot, have long been utilized for various manufacturing processes due to their flexibility and ability to move in multiple axes. However, the industrial robotics market has seen significant advancements, leading to the rise of SCARA (Selective Compliance Assembly Robot Arm) robots. SCARA robots offer several advantages, making them increasingly popular in industries. These robots are well-suited for assembly, welding, and packaging applications. They can operate continuously at a maximum speed of 120 cycles per minute in a 24-hour work cycle, ensuring compliance in the X-Y axes and the Z direction, making them six-degree compatible.

- The use of DC servomotors and associated gears helps actuate the rotary joints. SCARA robots are versatile and can perform various tasks such as welding, sealing, assembling, material handling, picking, cutting, painting and spraying, and machine-tending. They are often used as a replacement for articulated robots in Small and Medium Enterprises (SMEs) due to their ease of use and cost reduction. Robotics software and training programs are essential for effective implementation and operation of these robots. Force feedback and human-robot collaboration are critical features that enhance productivity gains. Programming languages like C, C++, and proprietary languages are used for programming these robots.

- With their intuitive programming and ease of use, SCARA robots have become an indispensable tool for increasing efficiency and reducing labor costs in manufacturing processes.

Exclusive Customer Landscape

The articulated robots market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the articulated robots market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, articulated robots market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - This company specializes in providing advanced robotic solutions, featuring a comprehensive 6-axis articulated robot portfolio.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Comau Spa

- Daihen Corp.

- DENSO Corp.

- Epson Europe B.V

- FANUC America Corp.

- Hirata Corp.

- Hiwin Corpo.

- HYUNDAI ROBOTICS

- IAI Industrieroboter GmbH

- Kawasaki Heavy Industries Ltd.

- MIDEA Group Co. Ltd.

- Mitsubishi Electric Corp.

- NACHI FUJIKOSHI Corp.

- NIMAK GmbH

- OMRON Corp.

- Shibaura Machine Co. Ltd.

- Staubli International AG

- Yamaha Motor Co. Ltd.

- Yaskawa Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Articulated Robots Market

- In March 2024, Fanuc Corporation, a leading manufacturer of industrial robots, introduced the CR-35iA, an articulated robot with a reach of 35 inches and a payload capacity of 110 pounds. This new offering expanded Fanuc's product line and catered to the growing demand for versatile automation solutions in various industries (Fanuc Corporation Press Release).

- In July 2024, ABB Robotics and Bosch Rexroth announced a strategic partnership to integrate ABB's robots with Bosch Rexroth's automation components, creating seamless, end-to-end manufacturing solutions. This collaboration aimed to enhance the competitiveness of both companies in the market and provide customers with more comprehensive automation offerings (ABB Robotics Press Release).

- In November 2024, Teradyne, a leading automated test equipment manufacturer, acquired AutoGuide Mobile Robots, a leading provider of autonomous mobile robots, for approximately USD 115 million. This acquisition enabled Teradyne to expand its portfolio and enter the growing market for autonomous mobile robots, which are increasingly being used in conjunction with articulated robots for flexible automation solutions (Teradyne Press Release).

- In February 2025, the European Union introduced the Industrial Strategy for the Single Market: Robotics, which includes a â¬1.5 billion investment in robotics research and development over the next seven years. This initiative is expected to drive innovation in the market, particularly in areas such as human-robot collaboration, energy efficiency, and adaptability to various industries (European Commission Press Release).

Research Analyst Overview

- The market is experiencing significant advancements, driven by the integration of technology such as data acquisition, augmented reality (AR), and virtual reality (VR) in robotics. Remote control capabilities enable operators to manage field robotics from a distance, enhancing efficiency and productivity. Safety is prioritized through emergency stops, vision systems, and safety controllers, while predictive analytics and process monitoring optimize performance and ensure quality assurance. Drive systems with joint types and torque sensors provide precise movement, and haptic feedback offers a more human-like interaction.

- Protective caging and force sensors ensure safety in industrial applications. Cloud platforms and data visualization facilitate remote access and real-time process optimization. Medical robotics and agricultural robotics are also gaining traction, with applications ranging from surgical procedures to crop management. Service robotics offer human-machine interfaces (HMIs) for seamless interaction, further expanding the market's reach.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Articulated Robots Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

156 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.8% |

|

Market growth 2024-2028 |

USD 15914.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

14.2 |

|

Key countries |

US, China, Germany, UK, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Articulated Robots Market Research and Growth Report?

- CAGR of the Articulated Robots industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the articulated robots market growth of industry companies

We can help! Our analysts can customize this articulated robots market research report to meet your requirements.

RIA -

RIA -