Assembly Automation Market Size 2026-2030

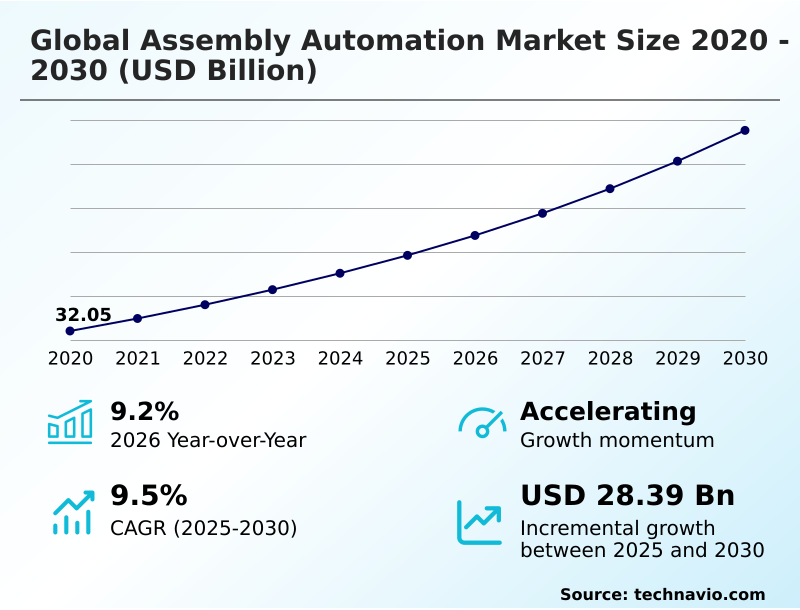

The assembly automation market size is valued to increase by USD 28.39 billion, at a CAGR of 9.5% from 2025 to 2030. Labor shortages and strategic shift to workforce augmentation will drive the assembly automation market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 54.9% growth during the forecast period.

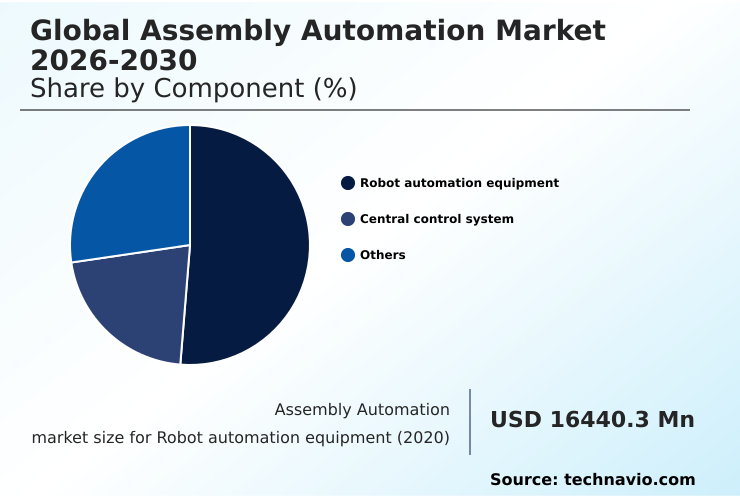

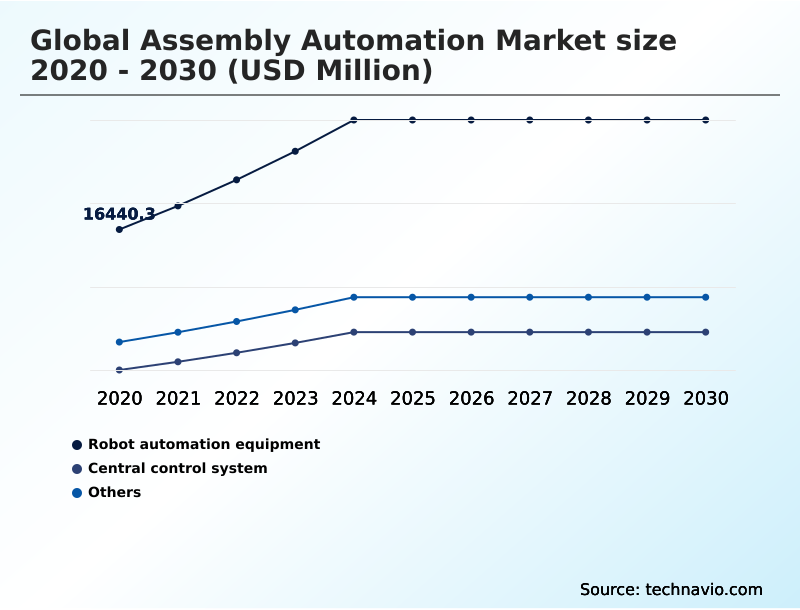

- By Component - Robot automation equipment segment was valued at USD 23.91 billion in 2024

- By End-user - Automotive segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 45.58 billion

- Market Future Opportunities: USD 28.39 billion

- CAGR from 2025 to 2030 : 9.5%

Market Summary

- The Assembly Automation market is defined by the strategic convergence of mechanized equipment, robotic systems, and advanced software to perform the aggregation of discrete components into finished goods. This process relies on a synchronized infrastructure of programmable logic controllers, sensors, and actuators that coordinate material logistics and joining tasks.

- The adoption of Assembly Automation is propelled by the need for greater operational efficiency and quality, as human assembly capabilities are exceeded by the miniaturization of electronics and the complexity of modern products. In one business scenario, an automotive OEM implements autonomous mobile robots and digital twin technology to create a flexible, high-mix, low-volume production line.

- This allows the facility to assemble multiple electric vehicle models on the same floor, reducing retooling downtime and responding dynamically to shifts in consumer demand. The integration of generative AI and software-defined automation is further democratizing access to these advanced systems, moving the industry toward more intelligent and resilient manufacturing ecosystems.

What will be the Size of the Assembly Automation Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Assembly Automation Market Segmented?

The assembly automation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Robot automation equipment

- Central control system

- Others

- End-user

- Automotive

- Electronics

- Healthcare

- Aerospace and defense

- Others

- Business segment

- Large enterprises

- Small and medium enterprises

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Component Insights

The robot automation equipment segment is estimated to witness significant growth during the forecast period.

The robot automation equipment segment is driven by the deployment of high-performance collaborative robots and industrial arms to address labor shortages. A key shift is the integration of physical AI, enabling robotic systems to operate in unstructured environments.

For instance, advanced models combining high-payload capacity with mechatronics deliver up to a 30% improvement in cycle times for machine tending and palletizing. This evolution from simple motion control systems to intelligent, adaptive machines underscores a move toward workforce augmentation.

The focus is on robots that are not only stronger and faster but also leverage predictive maintenance and kinematics to adapt to variable production needs, facilitating the growth of flexible manufacturing without extensive reprogramming.

The Robot automation equipment segment was valued at USD 23.91 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 54.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Assembly Automation Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by APAC, which accounts for over 54% of the market, driven by large-scale manufacturing in China and the technological sophistication of Japan and South Korea.

This region is a hub for high-speed pick-and-place robotics and is pioneering dark factories. North America, representing nearly 20% of the market, is focused on reshoring manufacturing, leveraging AI-enabled control systems for manufacturing and collaborative robots to counter labor shortages.

Europe emphasizes Industry 4.0 principles, with a strong focus on functional safety, sustainability, and software-defined automation.

European firms are leaders in developing greenfield projects and advanced system integration, with digital twin for process simulation used to reduce ramp-up time by up to 30%, showcasing a mature market that intertwines physical automation with rigorous digital and compliance standards.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the market is vividly illustrated through the application of specific, advanced technologies. For instance, robotic drilling and fastening systems are becoming indispensable in the aerospace sector, where precision and structural integrity are paramount.

- In parallel, the rise of flexible manufacturing is enabled by automated guided vehicles for material logistics, which are the backbone of modern matrix production layouts. These systems allow for dynamic workflows, a stark contrast to rigid conveyor-based lines. The intelligence layer is provided by AI-enabled control systems for manufacturing, which optimize processes in real time.

- In the electronics sector, high-speed pick-and-place robotics are essential for handling miniaturized components, while collaborative robots for machine tending are filling critical labor gaps in general industry. The commissioning phase has been revolutionized by using a digital twin for process simulation, which has been shown to reduce physical installation errors and ramp-up times more effectively than traditional trial-and-error methods.

- Real-time adaptive motion control and vision-guided robotic assembly ensure that robots can handle product variations without manual reprogramming. Automated quality inspection systems and a unified software-defined control architecture are now standard for achieving zero-defect production. This modular production for electric vehicles, which require heavy payload and precision joining, further highlights the need for adaptable systems.

- Predictive maintenance for robotic arms, cybersecurity for industrial control systems, and advanced end-of-arm tooling for delicate handling are all critical for ensuring uptime and security. Autonomous logistics in manufacturing and adherence to human-robot collaboration safety standards are also key considerations, while generative AI for plc code generation democratizes access to complex automation.

What are the key market drivers leading to the rise in the adoption of Assembly Automation Industry?

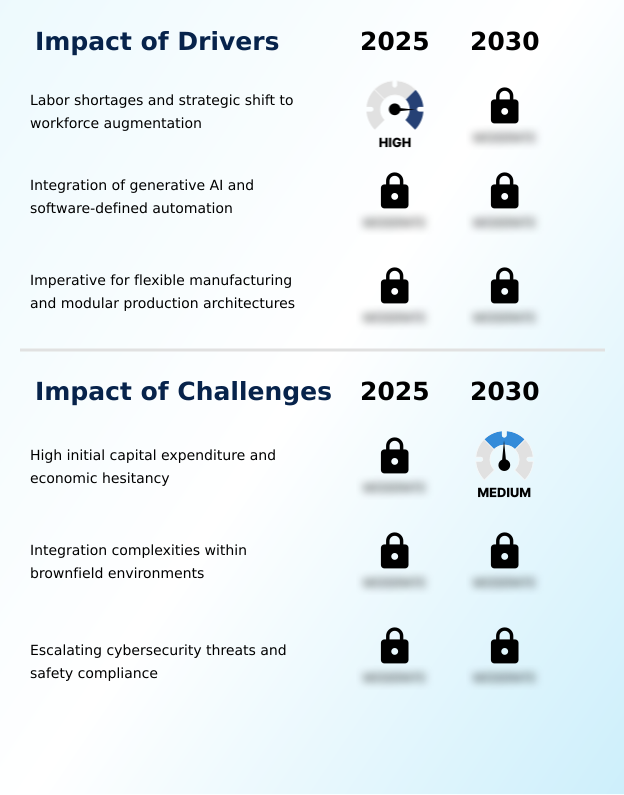

- Persistent labor shortages and a strategic shift toward workforce augmentation are key drivers fueling growth in the assembly automation market.

- Market growth is primarily driven by the need to address critical labor shortages through workforce augmentation. Manufacturers are deploying collaborative robots and autonomous mobile robots (AMRs) to fill gaps in manual assembly and logistics.

- For instance, new cobot models offer a 15-kilogram payload capacity and a 30% improvement in joint speed, effectively augmenting human capabilities. A second major driver is the integration of AI and software-defined automation, which lowers the barrier to entry.

- The advent of generative AI copilots can reduce PLC programming development time by up to 40%. This is complemented by the imperative for flexible manufacturing, particularly in industries with high-mix, low-volume production.

- Modular production architectures, replacing linear conveyors, allow for rapid reconfiguration to accommodate new product models without extensive downtime or capital expenditure.

What are the market trends shaping the Assembly Automation Industry?

- The emergence of generative copilots within engineering workflows represents a significant market trend. These AI-powered tools are streamlining the design and commissioning of complex automation systems.

- Key market trends are reshaping assembly line architecture and engineering workflows. The emergence of generative AI for PLC code generation is democratizing advanced automation, with some tools reducing software development time by approximately 40%. This is part of a broader shift toward a software-defined control architecture.

- Concurrently, the industry is moving from rigid linear conveyors to modular production for electric vehicles, enabled by autonomous mobile robots (AMRs) and automated guided vehicles. This allows for matrix production layouts, enhancing flexibility. Finally, physical AI is transforming collaborative robots from slow assistants into high-performance machines.

- Next-generation cobots now feature industrial-grade speed and payload capabilities, such as a 15-kilogram capacity, combined with advanced perception systems for complex tasks like bin picking, blurring the line with traditional 6-axis articulated arms.

What challenges does the Assembly Automation Industry face during its growth?

- High initial capital expenditure, compounded by economic hesitancy in key manufacturing sectors, presents a primary challenge affecting industry growth.

- Significant challenges constrain market adoption, led by high initial capital expenditure and economic hesitancy, particularly among small and medium enterprises. A second major hurdle involves integration complexities within brownfield environments. Legacy factories often feature heterogeneous machinery and outdated communication protocols, with analyses showing that over 60% of implementation time can be spent on writing custom interfaces for this operational technology.

- This issue creates data silos and inflates deployment costs. A third critical challenge is the dual threat of escalating cybersecurity risks and stringent safety compliance. The increased connectivity of industrial control systems has led to a 300% rise in targeted cyberattacks in some periods, while evolving human-robot collaboration safety standards add complexity and potential liability to deployments.

Exclusive Technavio Analysis on Customer Landscape

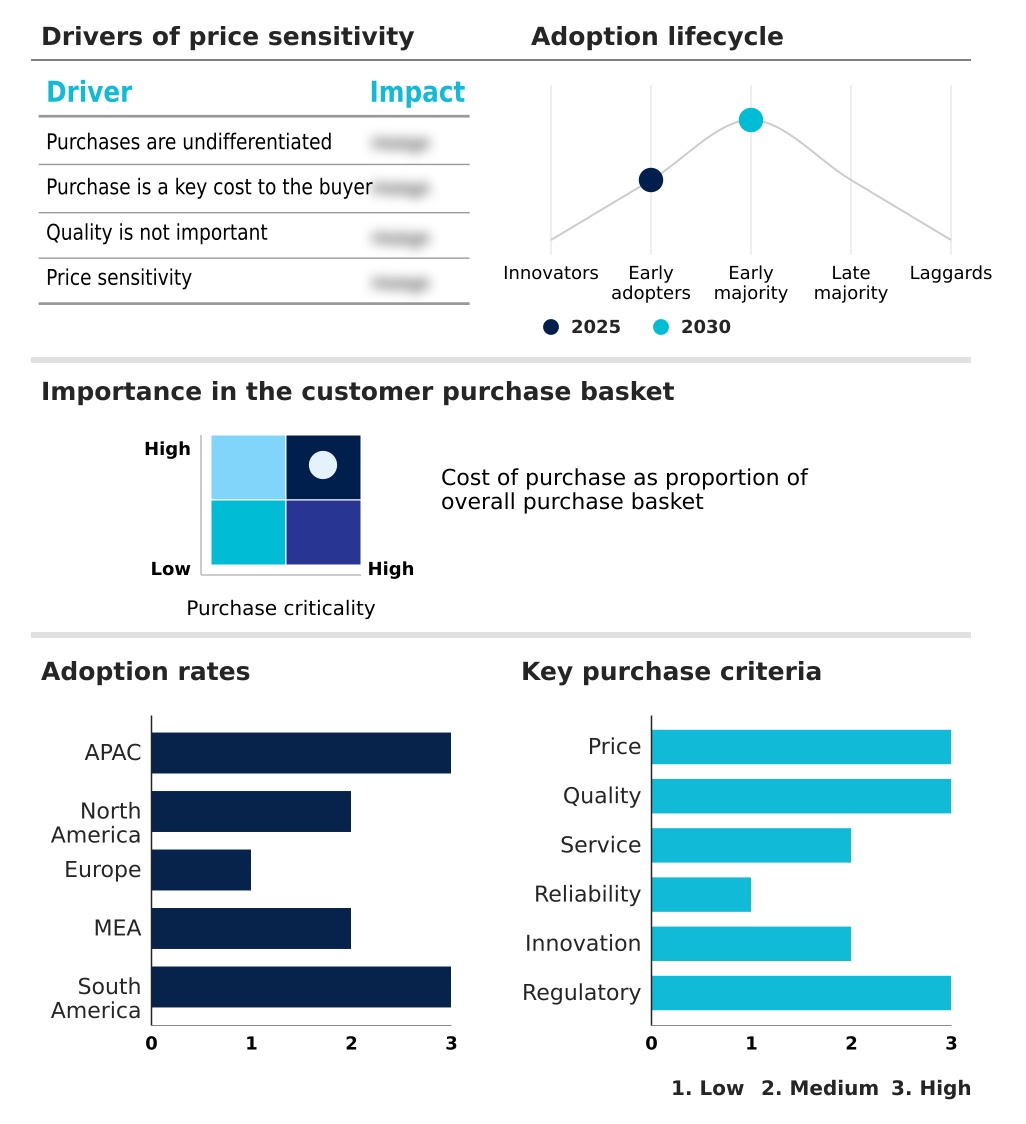

The assembly automation market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the assembly automation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Assembly Automation Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, assembly automation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Offerings center on advanced industrial robots, including collaborative and 6-axis arms, alongside integrated automation systems and software for the automotive, electronics, and manufacturing sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Comau Spa

- DENSO Corp.

- Durr AG

- Emerson Electric Co.

- Epson Corp.

- FANUC Corp.

- GROB WERKE GmbH

- Honeywell International Inc.

- Keyence Corp.

- KUKA AG

- Mitsubishi Electric Corp.

- OMRON Corp.

- Panasonic Holdings Corp.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Staubli International

- Universal Robots AS

- YASKAWA ELECTRIC CO.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Assembly automation market

- In May, 2025, Universal Robots AS launched the AI-ready UR15 collaborative robot at Automate 2025, featuring a 15-kilogram payload and delivering faster cycle times for machine tending and palletizing applications.

- In April, 2025, OMRON Corp. announced the establishment of a new global robotics organization to accelerate the development and delivery of localized automation solutions for key regional markets, particularly in Asia.

- In March, 2025, KUKA AG unveiled the KMP 3000P, an autonomous mobile platform capable of carrying loads up to three tons, designed to replace chain conveyors in automotive body shops.

- In February, 2025, Becton, Dickinson and Company completed the retrofit of its European production facilities with high-speed, aseptic assembly cells for pre-filled syringes to ensure rapid scalability and sterility.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Assembly Automation Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.5% |

| Market growth 2026-2030 | USD 28393.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.2% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a significant transformation, moving beyond simple hardware deployment to the integration of intelligent, interconnected technologies. The adoption of multi-axis robotic arms, SCARA robots, and other robotic systems is now standard, but the key differentiator is the software layer.

- Technologies such as digital twin technology, generative AI, and physical AI are reshaping what is possible in automated assembly. The entire ecosystem, built on programmable logic controllers and machine vision systems, is becoming smarter. This shift toward software-defined automation and cloud robotics presents a strategic challenge at the boardroom level, forcing a re-evaluation of capital expenditure.

- Investment decisions now weigh the long-term value of a flexible, data-driven software platform against the immediate cost of hardware. The use of advanced simulation tools has demonstrated a capability to reduce project ramp-up times by up to 30%, fundamentally altering ROI calculations.

- This evolution is driven by the need to manage complex kinematics and motion control systems while ensuring functional safety and enabling predictive maintenance, with decentralized architecture and IIoT facilitating this change.

What are the Key Data Covered in this Assembly Automation Market Research and Growth Report?

-

What is the expected growth of the Assembly Automation Market between 2026 and 2030?

-

USD 28.39 billion, at a CAGR of 9.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Robot automation equipment, Central control system, and Others), End-user (Automotive, Electronics, Healthcare, Aerospace and defense, and Others), Business Segment (Large enterprises, and Small and medium enterprises) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Labor shortages and strategic shift to workforce augmentation, High initial capital expenditure and economic hesitancy

-

-

Who are the major players in the Assembly Automation Market?

-

ABB Ltd., Comau Spa, DENSO Corp., Durr AG, Emerson Electric Co., Epson Corp., FANUC Corp., GROB WERKE GmbH, Honeywell International Inc., Keyence Corp., KUKA AG, Mitsubishi Electric Corp., OMRON Corp., Panasonic Holdings Corp., Rockwell Automation Inc., Schneider Electric SE, Siemens AG, Staubli International, Universal Robots AS and YASKAWA ELECTRIC CO.

-

Market Research Insights

- Market dynamics are shaped by a strategic pivot toward operational resilience and advanced digital technologies. The imperative for supply chain resilience is accelerating the adoption of modular production, which shows a greater ROI compared to rigid, linear systems. This shift is supported by real-time data processing and a focus on asset performance management.

- Key technologies underpinning this transition include vision-guided robotic assembly and software-defined control architecture, which have collectively reduced development time by over 30% in certain applications. This advancement in industrial control systems is crucial as manufacturers seek to optimize assembly sequences dynamically, lowering energy consumption by as much as 20% in newly deployed systems.

- The focus is no longer solely on speed but also on creating an intelligent, interconnected smart factory environment.

We can help! Our analysts can customize this assembly automation market research report to meet your requirements.

RIA -

RIA -