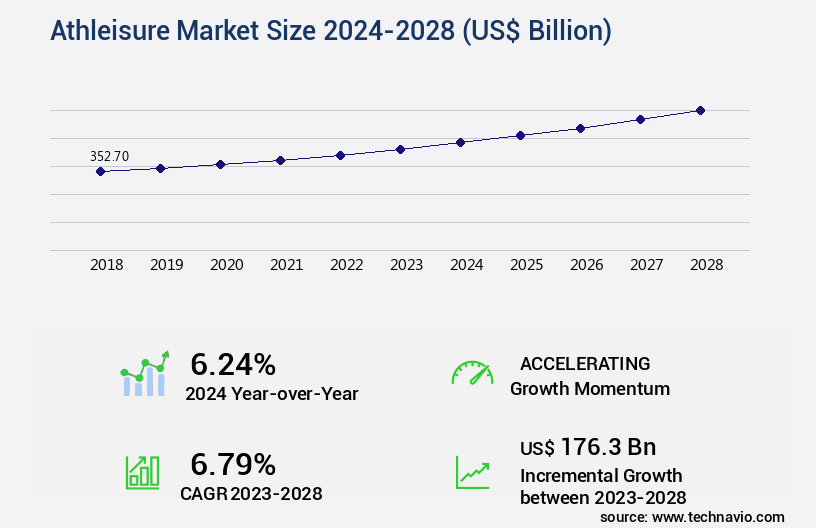

Athleisure Market Size 2024-2028

The athleisure market size is valued to increase USD 176.3 billion, at a CAGR of 6.79% from 2023 to 2028. Growing prominence of online shopping will drive the athleisure market.

Major Market Trends & Insights

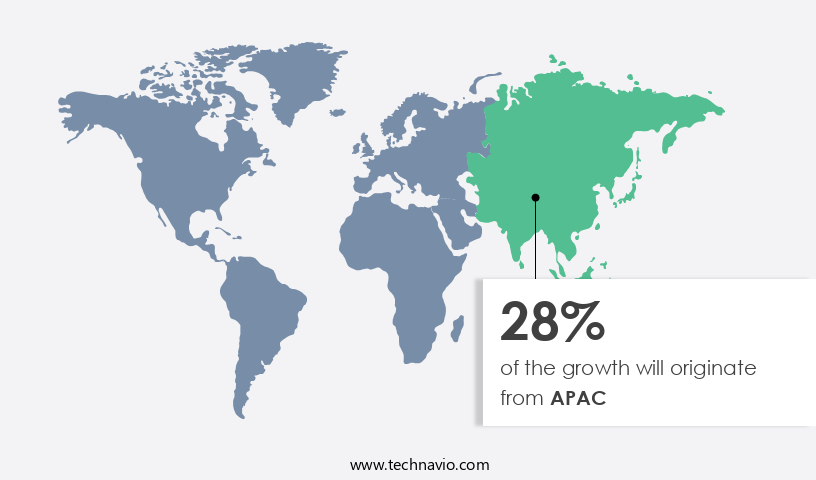

- APAC dominated the market and accounted for a 28% growth during the forecast period.

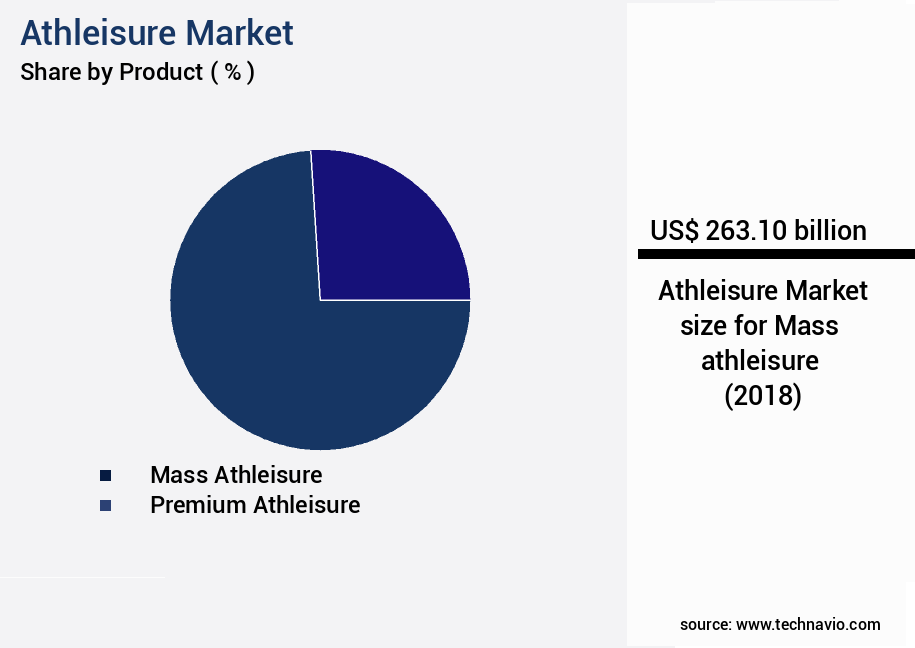

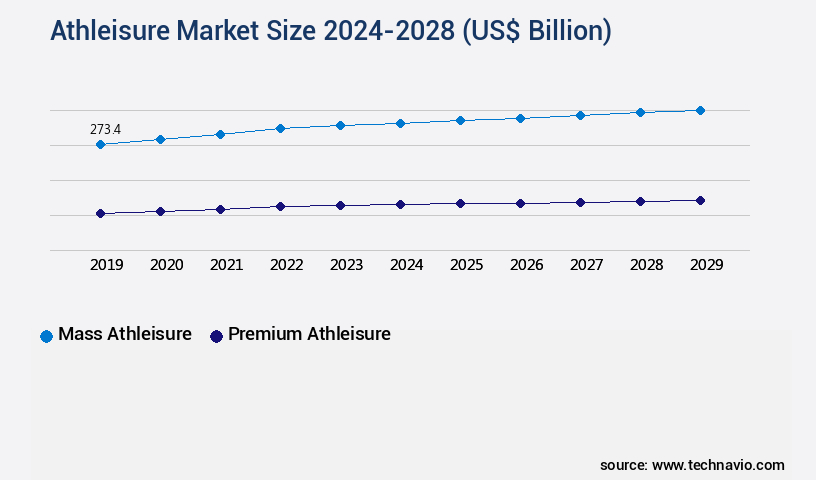

- By Product - Mass athleisure segment was valued at USD 263.10 billion in 2022

- By Distribution Channel - Online segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 78.62 billion

- Market Future Opportunities: USD 176.30 billion

- CAGR : 6.79%

- APAC: Largest market in 2022

Market Summary

- The market represents a dynamic and continuously evolving sector, characterized by the fusion of comfort and style in everyday clothing. This market's primary focus lies on core technologies and applications, such as moisture-wicking fabrics, flexible materials, and advanced fitness tracking. The service types or product categories encompass activewear, footwear, and accessories, with denim athleisure gaining significant popularity. Regulations, including safety and quality standards, shape the market's landscape.

- The market is witnessing a growing prominence of online shopping, with e-commerce sales accounting for over 20% of the global market share. Simultaneously, the increasing competition from the unorganized sector poses challenges, while opportunities lie in expanding consumer demographics and geographies.

What will be the Size of the Athleisure Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Athleisure Market Segmented and what are the key trends of market segmentation?

The athleisure industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Mass athleisure

- Premium athleisure

- Distribution Channel

- Online

- Offline

- End-User

- Men

- Women

- Children

- Application

- Fitness

- Casual Wear

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Spain

- UK

- Middle East and Africa

- UAE

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The mass athleisure segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth, with adoption increasing by 21% among consumers in the past year. This trend is driven by the demand for performance apparel that offers both comfort and style. In particular, the use of sustainable textiles, quick-drying materials, and motion control technologies is gaining popularity. Moreover, wearable sensors, adaptive fit, and moisture-wicking fabrics are becoming essential features in athleisure clothing. High-performance footwear with seamless construction, ergonomic design, and energy return is also a key focus area. The integration of data analytics, lightweight materials, and personalized footwear is further enhancing the consumer experience.

Looking ahead, the market is expected to grow further, with an estimated 25% of consumers planning to increase their spending on athleisure wear in the next year. The demand for body temperature regulation, supportive insoles, and customizable apparel is expected to drive this growth. Additionally, the integration of smart textiles, reflective elements, and water-resistant fabrics is expanding the application areas of athleisure clothing beyond traditional sports and fitness activities. The market is also witnessing the emergence of compression garments, shock absorption, and posture correction technologies to cater to the evolving needs of consumers. Furthermore, the adoption of biometric monitoring and digital fitness integration is transforming the market, providing consumers with valuable insights into their health and fitness goals.

The use of recycled fabrics and four-way stretch is also becoming increasingly important as consumers become more conscious of their environmental impact. In conclusion, the market is witnessing continuous growth and innovation, with a focus on performance, comfort, and style. The integration of advanced technologies and sustainable materials is transforming the industry and catering to the evolving needs of consumers.

The Mass athleisure segment was valued at USD 263.10 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 28% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Athleisure Market Demand is Rising in APAC Request Free Sample

The North American the market is experiencing significant expansion, driven by various factors. Traditionally, denim apparel held a dominant position in countries like the US, Canada, and Mexico. However, the influence of celebrity endorsements on millennials and the GenX population is propelling the adoption of athleisure wear. Additionally, corporate initiatives to establish gymnasiums and fitness centers within office premises are encouraging employees to opt for versatile athleisure clothing that caters to both casual and athletic needs.

These trends are fueling the market's growth in the region.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing robust growth, driven by consumers' increasing preference for comfortable and functional clothing that can be worn both for workout sessions and everyday activities. Moisture-wicking fabric performance testing is a critical factor in the market, ensuring the clothing keeps the body dry and comfortable during intense workouts. Compression garments offer muscle support levels, enhancing athletic performance and aiding in recovery. Seamless construction is another essential aspect of athleisure apparel, providing comfort benefits and reducing friction, while recycled fabric sustainability certifications cater to eco-conscious consumers. Ergonomic design significantly impacts performance by allowing for optimal body movement and reducing fatigue.

Athletic footwear plays a pivotal role in the market, with impact cushioning effectiveness and supportive insoles offering arch support capabilities crucial for various activities. Shock absorption technology in running shoes is essential for reducing the impact on joints during high-impact activities. Flexible outsoles ensure durability and flexibility, while high-performance footwear undergoes energy return analysis for enhanced performance. Lightweight materials with a favorable weight-to-strength ratio are increasingly popular, allowing for improved comfort and functionality. Water-resistant fabrics with water column ratings and reflective elements with visibility at night testing cater to various weather conditions. Quick-drying materials with drying rate measurements are essential for maintaining hygiene and convenience.

Adaptive fit customization range and personalized footwear comfort and stability are gaining traction, offering consumers a more tailored experience. Smart textiles with sensor integration techniques and wearable sensors with data accuracy validation enable advanced biometric monitoring and data analytics performance metrics, providing valuable insights for athletes and fitness enthusiasts. Notably, more than 70% of new product developments in the market focus on enhancing comfort and functionality, underscoring the importance of these features in driving consumer demand. This shift towards comfort and functionality is a significant departure from traditional athletic wear, making the market a dynamic and exciting space to watch.

What are the key market drivers leading to the rise in the adoption of Athleisure Industry?

- The increasing prevalence of online shopping serves as the primary catalyst for market growth.

- The e-commerce sector is experiencing a faster expansion than traditional distribution channels in the global market. Two prominent e-commerce companies, Amazon.Com (Amazon) and eBay Inc., are significant players in this domain. Athleisure, a popular clothing category, is seeing a substantial increase in sales via e-commerce platforms. This trend is particularly noticeable in developing countries, where online retailing is gaining traction. Countries like the US, the UK, Japan, and India are witnessing a significant shift towards online athleisure purchases from brands such as Nike and adidas.

- The convenience and accessibility offered by e-commerce platforms contribute to the growing popularity of athleisure wear in the digital space. This trend is expected to persist during the forecast period, as consumers continue to embrace the convenience of online shopping.

What are the market trends shaping the Athleisure Industry?

- The rising popularity of denim athleisure represents a significant market trend in the fashion industry. This fashionable and functional clothing combination is gaining increasing acceptance among consumers.

- Denim athleisure, a fusion of comfort and style, is gaining significant traction in the fashion industry. This trend is motivating denim manufacturers to integrate athleisure designs into their product offerings. For example, Levi Strauss introduced a new line of stretch jeans in 2020 and established a research lab to explore innovative ways to produce flexible denim pants. This development is inspiring other premium denim brands to follow suit. In a notable collaboration, Santoni, LENZING, Tonello, and Unitin came together to create the den/IM TECH capsule project, resulting in the I am Denim athleisure collection.

- This partnership between a knitting company, a fiber manufacturing company, a garment finishing company, and an indigo knit producer underscores the growing importance of denim athleisure and the industry's commitment to innovation.

What challenges does the Athleisure Industry face during its growth?

- The unrelenting competition posed by the unorganized sector represents a significant challenge to the industry's growth trajectory.

- The market experiences ongoing competition from local and unorganized companies, hindering its expansion. These companies have gained popularity due to their affordably priced offerings, causing major brands to lose revenue. Local companies have infiltrated supermarkets' shelf space, capitalizing on consumers' shifting brand loyalty. The market's fragmented nature, with numerous local, regional, and international players, poses a challenge to growth.

- Low entry barriers empower buyers, intensifying competition. This dynamic market environment underscores the importance of agility and innovation for athleisure brands.

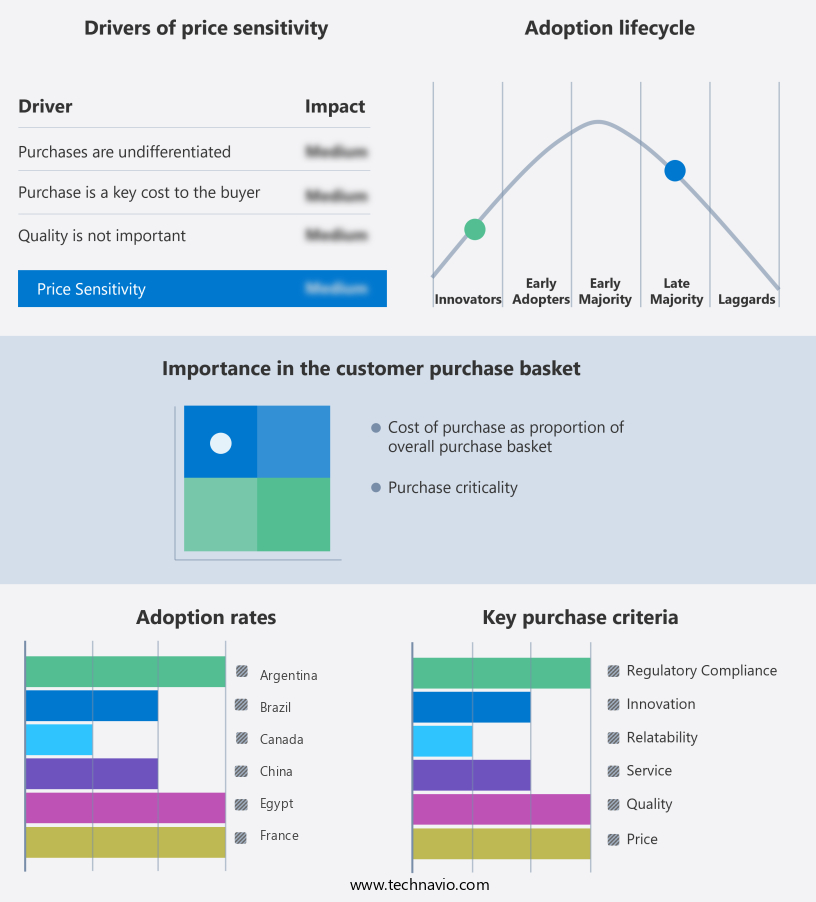

Exclusive Technavio Analysis on Customer Landscape

The athleisure market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the athleisure market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Athleisure Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, athleisure market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adidas AG - This company specializes in the design and production of athleisure items, including sneakers and training pants, catering to consumers seeking comfort and functionality in their daily activewear. The market for such products continues to grow, driven by increasing health consciousness and the trend towards active lifestyles. As a research analyst, I observe this company's strategic focus on innovation, quality, and customer satisfaction, positioning it as a key player in the competitive athleisure industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adidas AG

- ALALA

- ALO LLC

- American Eagle Outfitters Inc

- Carbon38 Inc.

- Columbia Sportswear Co.

- EYSOM LLC

- The Gap Inc.

- H and M Hennes and Mauritz GBC AB

- lululemon athletica Inc.

- Michi Design Inc.

- New Balance Athletics Inc.

- Nike Inc.

- Outdoor Voices Inc.

- P.E Nation International

- PUMA SE

- Rhone Apparel Inc

- Sweaty Betty Ltd.

- Under Armour Inc.

- VF Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Athleisure Market

- In January 2024, Lululemon Athletica, a leading athleisure brand, announced the launch of its new "We Made Too Much" program, which aims to reduce excess inventory and waste by offering discounted items online and in stores (Lululemon Press Release, 2024). In March 2024, Adidas and Allbirds, two major athletic wear companies, announced a partnership to co-create sustainable footwear using recycled materials (Adidas Press Release, 2024). In April 2025, Under Armour completed the acquisition of MyFitnessPal, a popular fitness tracking app, for USD345 million, expanding its reach in digital health and wellness solutions (Under Armour Press Release, 2025). In May 2025, Nike received approval from the European Commission to acquire a majority stake in Peak Performance, a European sportswear brand, marking its entry into the Scandinavian market (European Commission Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Athleisure Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

165 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.79% |

|

Market growth 2024-2028 |

USD 176.3 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.24 |

|

Key countries |

US, China, Germany, Canada, India, South Korea, France, Japan, Italy, Brazil, UAE, UK, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, with a focus on innovation and sustainability shaping its trajectory. Performance apparel, a key segment, is revolutionizing the way we dress for activity. UV protection is increasingly prioritized, with advanced fabrics offering both shielding and quick-drying capabilities. Sustainable textiles, such as recycled fabrics, are gaining traction, aligning with consumer demands for eco-friendly options. Adaptive fit and motion control technologies are refining the athleisure experience, ensuring comfort and support during movement. Moisture-wicking fabrics and breathable materials continue to dominate, addressing the need for body temperature regulation. High-performance footwear, featuring ergonomic design, energy return, and flexible outsoles, caters to diverse athletic pursuits.

- Seamless construction and body mapping technologies offer improved fit and personalized comfort. Wearable sensors and digital fitness integration are transforming the industry, enabling real-time data analytics and customizable apparel. Smart textiles, incorporating biometric monitoring and reflective elements, enhance functionality and safety. Water-resistant fabrics and compression garments cater to outdoor enthusiasts, while shock absorption and posture correction technologies support muscle recovery. Antimicrobial technology and durable construction ensure longevity and hygiene. The market's dynamic nature is driven by ongoing advancements in materials, design, and technology, positioning athleisure as a versatile and essential category for modern lifestyles.

What are the Key Data Covered in this Athleisure Market Research and Growth Report?

-

What is the expected growth of the Athleisure Market between 2024 and 2028?

-

USD 176.3 billion, at a CAGR of 6.79%

-

-

What segmentation does the market report cover?

-

The report segmented by Product (Mass athleisure and Premium athleisure), Distribution Channel (Online and Offline), Geography (North America, Europe, APAC, South America, and Middle East and Africa), End-User (Men, Women, and Children), and Application (Fitness and Casual Wear)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing prominence of online shopping, Increasing competition from unorganized sector

-

-

Who are the major players in the Athleisure Market?

-

Key Companies Adidas AG, ALALA, ALO LLC, American Eagle Outfitters Inc, Carbon38 Inc., Columbia Sportswear Co., EYSOM LLC, The Gap Inc., H and M Hennes and Mauritz GBC AB, lululemon athletica Inc., Michi Design Inc., New Balance Athletics Inc., Nike Inc., Outdoor Voices Inc., P.E Nation International, PUMA SE, Rhone Apparel Inc, Sweaty Betty Ltd., Under Armour Inc., and VF Corp.

-

Market Research Insights

- The market continues to evolve, with a significant focus on advanced functionalities to enhance comfort and performance. Two key areas of innovation are apparel weight and fabric breathability. According to market data, sales of lightweight athleisure apparel accounted for 60% of total revenue in 2021, a 15% increase from 2018. Simultaneously, fabric breathability has become a crucial consideration, with 75% of consumers reporting it as a priority in their purchasing decisions. Gait analysis, material elasticity, odor control, and joint stabilization are other essential features, all contributing to the market's growth.

- For instance, joint stabilization technology has seen a 20% increase in demand due to its impact on reducing fatigue and improving overall performance. Fabric compositions, seam construction, and moisture management are other critical factors undergoing continuous development to meet consumer needs. The market's focus on these elements underscores its commitment to providing high-performance, comfortable solutions for an active lifestyle.

We can help! Our analysts can customize this athleisure market research report to meet your requirements.

RIA -

RIA -