Autoinjectors Market Size 2024-2028

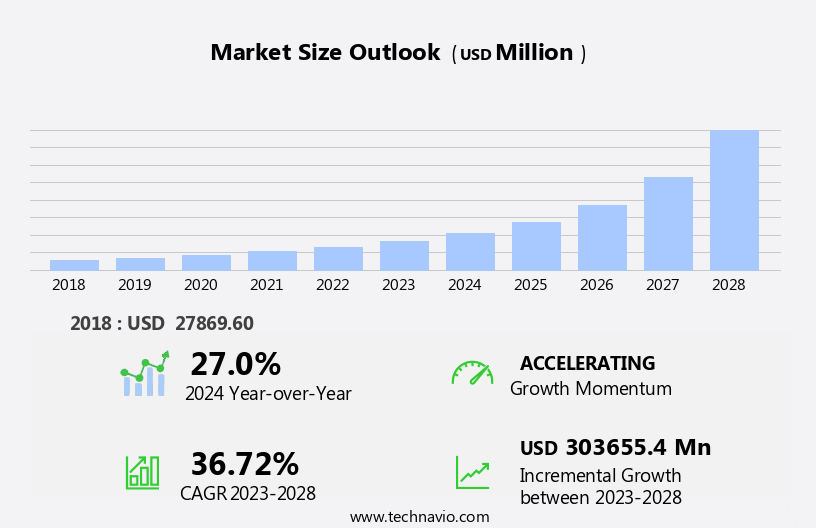

The autoinjectors market size is forecast to increase by USD 303.66 billion, at a CAGR of 36.72% between 2023 and 2028.

- The market is driven by the increasing prevalence of allergies and the growing need for immediate, self-administered care. Allergic conditions, such as anaphylaxis, asthma, and diabetes, necessitate the use of autoinjectors for timely medication delivery. This trend is further fueled by the rising awareness of self-administration and the convenience offered by these devices. However, the market faces challenges, including the potential side-effects of autoinjectors. These devices, while effective, can cause adverse reactions such as pain, bruising, and injection site reactions.

- Addressing these issues through technological advancements and improved design could help mitigate these challenges and enhance patient satisfaction. Strategic alliances between companies are also shaping the market landscape, as collaborations lead to innovation and expanded product offerings. Companies seeking to capitalize on market opportunities should focus on developing user-friendly, safe, and effective autoinjectors, while addressing the challenges of side-effects and competition.

What will be the Size of the Autoinjectors Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The autoinjector market continues to evolve, driven by advancements in drug delivery systems and material science. Electronic actuators and hydraulic actuators are increasingly utilized to ensure dose accuracy, while drug eluting systems offer controlled release for various applications, including autoimmune diseases and hormone therapy. Temperature sensitivity is a critical factor, necessitating stringent storage conditions for certain medications. Material science plays a pivotal role in the development of autoimmune disease treatments, with polymer selection influencing patient compliance and product lifecycle management. Allergic reactions and injection site reactions necessitate safety features such as needle shields and needle protection.

Pricing strategies, regulatory approvals, and clinical trials are ongoing considerations for manufacturers, with intellectual property and quality control ensuring product differentiation and compliance with standards. Reusable devices, spring mechanisms, and user interface design are essential for ease of use and patient acceptance. Connected devices, deployment mechanisms, and compliance tracking enable remote monitoring and data logging, enhancing patient care and supply chain management. Pneumatic actuators, liquid medications, and pain management applications expand the market's reach, with distribution channels and healthcare providers crucial for successful market penetration. The autoinjector market's dynamic nature is further highlighted by the ongoing development of combination products, which integrate various components to streamline drug administration.

How is this Autoinjectors Industry segmented?

The autoinjectors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Anaphylaxis

- Multiple sclerosis

- Rheumatoid arthritis

- Diabetes

- End-user

- Hospitals and clinics

- Self-administration

- Product Type

- Disposable Autoinjectors

- Reusable Autoinjectors

- Distribution Channel

- Retail Pharmacies

- Online Pharmacies

- Hospital Pharmacies

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

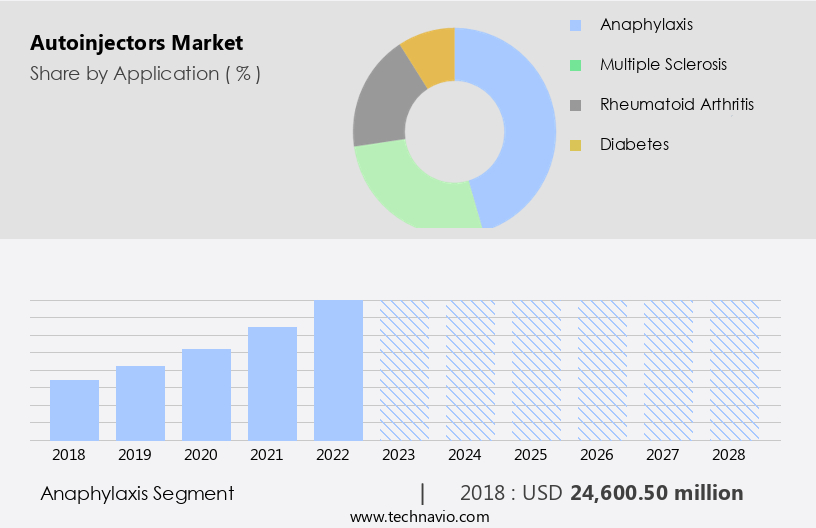

By Application Insights

The anaphylaxis segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth due to the increasing prevalence of chronic diseases, particularly anaphylaxis and food allergies, requiring self-administered injectable drugs. The anaphylaxis segment dominates the market revenue-wise, driven by the rising number of anaphylactic episodes and the effectiveness of epinephrine, a common treatment for this condition. The adoption of advanced technologies, such as electronic actuators and connected devices, enhances the user experience and ensures dose accuracy. Manufacturers prioritize quality control, needle protection, and safety features to address patient concerns. Regulatory approvals for disposable and reusable devices, along with clinical trials, are crucial for market entry. Shelf life and temperature sensitivity are critical factors influencing the market dynamics.

In military applications, autoinjectors offer ease of use and portability, making them essential for emergency responders. Pricing strategies and supply chain management play a significant role in market growth. Hormone therapy, heart conditions, and autoimmune diseases are among the key applications driving the market. The use of controlled release, drug eluting systems, and hydraulic actuators further expands the market scope. Material science and polymer selection are essential considerations for manufacturing processes. Patient compliance and product lifecycle management are vital aspects of market success. Combination products, liquid medications, and powder medications cater to diverse therapeutic areas. Regulatory approvals, intellectual property, and distribution channels are essential elements of market growth.

The Anaphylaxis segment was valued at USD 24.6 billion in 2018 and showed a gradual increase during the forecast period.

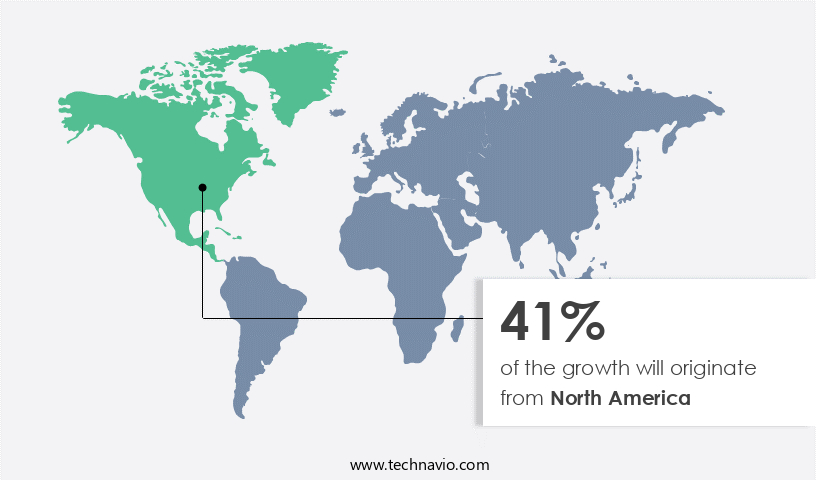

Regional Analysis

North America is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is witnessing significant growth due to the increasing prevalence of chronic diseases such as autoimmune diseases, heart conditions, and hormone therapy. Dose accuracy is a critical factor driving market expansion, with electronic actuators and advanced drug delivery systems ensuring precise medication administration. The market encompasses various types of autoinjectors, including spring mechanism, pneumatic, and hydraulic actuators, catering to diverse medication requirements. Manufacturing processes employing material science advancements and intellectual property protections ensure product quality and safety. Regulatory approvals and clinical trials are essential steps in bringing new autoinjectors to market, with regulatory bodies stringently evaluating needle protection, safety features, and needle shields to minimize injection site reactions.

Pricing strategies play a crucial role in market penetration, with disposable devices offering cost-effectiveness and reusable devices ensuring long-term savings. Connected devices, patient portals, and compliance tracking enable remote monitoring and ease of use, enhancing patient compliance and improving product lifecycle management. Autoinjectors find applications in emergency response situations, military applications, veterinary medicine, and controlled release systems. Temperature sensitivity and drug stability are essential considerations in storage conditions. Allergic reactions and temperature sensitivity are significant challenges, necessitating careful formulation selection and polymer engineering. The market landscape is diverse, with combination products, liquid medications, and powder medications catering to various therapeutic areas.

Market players invest in research and development to introduce innovative autoinjectors, such as drug eluting systems and prefilled syringes, addressing unmet medical needs. In the US, the market is driven by significant investments in healthcare infrastructure, advanced medical facilities, and a large patient population requiring chronic disease management. Key players include Amgen, Merck & Co., and Eli Lilly and Company, among others, with Amgen's ENBREL SureClick autoinjector being a notable revenue generator.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global autoinjectors market size and forecast projects growth, driven by autoinjectors market trends 2024-2028. B2B autoinjector supply solutions leverage advanced drug delivery technologies for safety. Autoinjectors market growth opportunities 2025 include autoinjectors for chronic diseases and disposable autoinjectors, meeting patient needs. Autoinjector supply chain software optimizes operations, while autoinjectors market competitive analysis highlights key manufacturers. Sustainable autoinjector practices align with eco-friendly medical trends. Autoinjectors regulations 2024-2028 shapes autoinjector demand in Europe 2025. User-friendly autoinjector solutions and premium autoinjector insights boost adoption. Autoinjectors for home use and customized autoinjector designs target niches. Autoinjectors market challenges and solutions address usability, with direct procurement strategies for autoinjectors and autoinjector pricing optimization enhancing profitability. Data-driven autoinjector market analytics and smart drug delivery trends drive innovation.

What are the key market drivers leading to the rise in the adoption of Autoinjectors Industry?

- The escalating incidence of allergies and the resulting demand for prompt medical intervention serve as the primary market catalysts.

- The global market for autoinjectors, which deliver precise doses of medication using electronic actuators, is witnessing significant growth due to the increasing prevalence of chronic conditions requiring regular drug delivery. Allergies, affecting over 50 million people in North America alone, are a major driver of this market. Anaphylaxis, a severe allergic reaction, necessitates immediate treatment with precise doses of epinephrine. The market's growth is further fueled by its applications in emergency response situations and military applications. Manufacturing processes for autoinjectors prioritize dose accuracy and shelf life, ensuring the efficacy and safety of the drug delivery systems.

- Clinical trials are essential for the approval of new autoinjector designs and formulations. Veterinary medicine is another growing application area for autoinjectors. Storage conditions and controlled release are critical factors in the market. Pricing strategies are also under consideration to make these life-saving devices more accessible. The needle shield technology in autoinjectors enhances user safety and convenience. In summary, the global autoinjector market is experiencing growth due to the increasing prevalence of chronic conditions, the need for emergency treatment, and the advancements in drug delivery systems. Manufacturers focus on maintaining dose accuracy, ensuring shelf life, and developing user-friendly designs to cater to diverse applications, including veterinary medicine.

What are the market trends shaping the Autoinjectors Industry?

- Strategic alliances have emerged as a significant market trend among companies, reflecting a growing recognition of the benefits derived from collaborative business relationships. By forming strategic partnerships, organizations can expand their reach, enhance their capabilities, and improve their competitive position.

- The market has witnessed significant growth, driven by strategic alliances and collaborations. Companies are partnering to expand their business and introduce new offerings. For instance, Novartis AG collaborated with Adamis Pharmaceuticals to commercialize and distribute SYMJEPI, an epinephrine autoinjector, in the US market. This partnership enhanced Novartis AG's commercial presence and maximized the value of SYMJEPI. In another development, Halozyme Therapeutics, Inc. And Antares Pharma, Inc. Signed an agreement in April 2022, with Halozyme acquiring Antares. Similarly, Pfizer Inc. Is working with Antares Pharma to develop an autoinjector pen for an undisclosed Pfizer drug. Connected devices, safety features, and needle protection are key trends in the market.

- Quality control and user interface are essential considerations for manufacturers. Regulatory approvals and intellectual property rights are crucial for market entry and product differentiation. The market caters to various dosage forms, including reusable and disposable devices. Spring mechanism and deployment mechanism are critical components of autoinjectors. Injection site reactions are a concern, and safety features are increasingly prioritized to mitigate risks. Overall, the market is dynamic, with continuous innovation and advancements in technology shaping its landscape.

What challenges does the Autoinjectors Industry face during its growth?

- The side effects associated with autoinjectors represent a significant challenge to the growth of the industry, requiring continuous research and innovation to mitigate their impact and ensure patient safety and efficacy.

- Autoinjectors, a critical injection device used in the administration of various medications, particularly those for autoimmune diseases and drug eluting systems, have gained significant importance in the healthcare industry. However, these devices are not without challenges. Patients using autoinjectors may experience side effects such as infection, hypertension, hypotension, myalgia, headache, and diarrhea. Patients with chemotherapy-induced anemia may exhibit additional symptoms like fatigue, edema, nausea, vomiting, fever, and increased occurrence of hypertension. Multiple sclerosis patients, when administered with interferon beta-1b-filled autoinjectors, are at risk of severe hepatic injury, including cases of hepatic failure. In some instances, these autoinjectors can cause anaphylaxis, leading to dyspnea, bronchospasm, tongue edema, skin rash, and urticaria.

- These side effects can hinder the adoption of autoinjectors and encourage patients to explore alternatives with fewer adverse effects. Material science plays a crucial role in the development of autoinjectors, with polymer selection being a significant consideration for product lifecycle management. Hydraulic actuators are commonly used in autoinjectors due to their ability to deliver precise dosages. Temperature sensitivity is another critical factor, as autoinjectors must maintain the required temperature range to ensure proper functionality. Prefilled syringes and injection devices are essential components of autoinjectors, and their compatibility with various drugs is a key factor in their success.

- Combination products, which integrate multiple functions into a single device, are gaining popularity due to their convenience and ease of use. Ensuring patient compliance with the use of autoinjectors is essential, as improper administration can lead to ineffective treatment or adverse effects.

Exclusive Customer Landscape

The autoinjectors market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the autoinjectors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, autoinjectors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - The company specializes in providing autoinjector technology for various biologic medications, including Adalimumab. Their innovative solutions enable simplified self-administration of treatments, enhancing patient convenience and adherence.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Amgen Inc.

- Bayer AG

- Becton Dickinson and Co.

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- GlaxoSmithKline Plc

- Halozyme Therapeutics Inc.

- Johnson and Johnson Services Inc.

- Johnson Medtech LLC

- medmix Ltd.

- Merck KGaA

- Owen Mumford Ltd.

- Pfizer Inc.

- RAVIMED Sp. zoo

- Recipharm AB

- SHL Medical AG

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

- Ypsomed Holding AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Autoinjectors Market

- In January 2024, pharmaceutical company AstraZeneca announced the launch of its new autoinjector device, "Easus," for the administration of Fasenra, an asthma treatment (AstraZeneca press release). This innovative device features a reusable design and a connected mobile application to facilitate better medication adherence and dosing management.

- In March 2024, pharmaceutical giants Pfizer and Eli Lilly entered into a strategic collaboration to co-develop and commercialize a portfolio of biosimilars using Pfizer's advanced autoinjector technology (Pfizer press release). This partnership is expected to significantly expand the reach and impact of both companies in the biosimilars market.

- In May 2024, pharmaceutical company Novo Nordisk received FDA approval for its new insulin pen, the NovoPen 6, featuring a redesigned user interface and a thinner needle for improved patient experience (FDA press release). This approval marks a significant step forward in the company's efforts to enhance its diabetes care portfolio.

- In April 2025, Danish medtech company, Orion Corporation, secured a â¬100 million investment from a leading European investment firm to expand its production capacity for autoinjectors and pen injectors (Orion Corporation press release). This investment will enable Orion to meet the growing demand for its products and strengthen its position in the global injector market.

Research Analyst Overview

- The autoinjector market is experiencing significant activity and trends, shaping the future of healthcare access for chronic disease management. Clinical studies continue to prioritize user experience, focusing on supply chain optimization and packaging design to enhance patient safety. Performance metrics and product labeling are essential for healthcare professional education and inventory management, ensuring regulatory compliance and ethical considerations. Environmental impact is a growing concern, with waste management and recycling programs becoming increasingly important. Sales and marketing strategies emphasize emergency preparedness and training programs for proper use, while quality assurance and maintenance requirements ensure device reliability and longevity. Post-market surveillance, adverse event reporting, and value-based care are key considerations for market access, with technology advancements and preventive medicine driving product differentiation.

- Human factors engineering and design for manufacturing contribute to user instructions and patient safety, while safety regulations and risk management maintain a balance between innovation and safety. Global health initiatives and public health priorities influence market trends, with a focus on chronic disease management, disaster relief, and ethical considerations. Health economics and technology advancements shape marketing strategies, while product lifespan and design innovations extend the value of autoinjectors in the healthcare landscape.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Autoinjectors Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

176 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 36.72% |

|

Market growth 2024-2028 |

USD 303655.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

27.0 |

|

Key countries |

US, UK, Germany, Canada, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Autoinjectors Market Research and Growth Report?

- CAGR of the Autoinjectors industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the autoinjectors market growth of industry companies

We can help! Our analysts can customize this autoinjectors market research report to meet your requirements.

RIA -

RIA -