Automotive Adaptive Front Lighting System Market Size 2024-2028

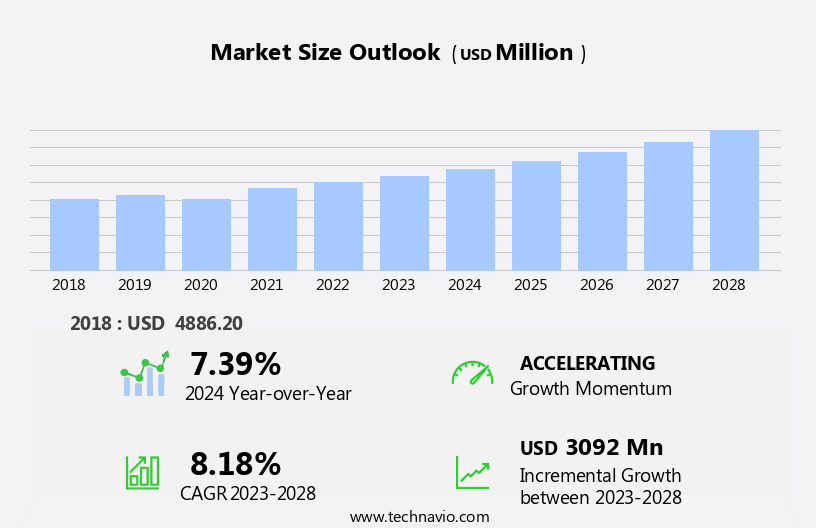

The automotive adaptive front lighting system market size is forecast to increase by USD 3.09 billion at a CAGR of 8.18% between 2023 and 2028.

- The Automotive Adaptive Front Lighting System (AFLS) market is experiencing significant growth due to the increasing use of these systems as product differentiators in the highly competitive automotive industry. This trend is driven by the advanced features offered by adaptive front lighting systems, such as improved visibility, enhanced safety, and improved night vision capabilities. Another trend influencing market growth is the development of AI-enabled advanced driver-assistance systems (ADAS) solutions, including those used in self-driving cars, which are increasingly integrating adaptive front lighting systems to provide a more comprehensive driving experience. The rise of electric vehicles further necessitates advanced lighting solutions for enhanced safety and efficiency. However, the high cost associated with repairing ADAS technologies poses a challenge to market growth. Despite this, the market is expected to continue expanding as automakers seek to offer more advanced and differentiated products to consumers.

What will be the Size of the Automotive Adaptive Front Lighting System Market During the Forecast Period?

- Headlights play a crucial role in ensuring vehicle safety during nighttime driving. Adaptive control systems in lighting systems have gained significant traction in recent years due to their ability to adjust headlight intensity and direction based on driving circumstances. These systems are increasingly being integrated into various types of vehicles, including electric and hybrid vehicles, lightweight passenger vehicles, and commercial vehicles. The adaptive front lighting system market is driven by several factors, including the growing demand for vehicle safety features, the increasing popularity of autonomous automobile sector, and the need to enhance road safety in adverse weather conditions such as rain, fog, and curve roads.

- Image sensors and climatic factors significantly influence the performance of adaptive front lighting systems. The adaptive front lighting system market is expected to witness substantial growth due to the increasing number of automobile collisions during nighttime and the need to improve passenger safety. Moreover, the integration of LED technology in lighting systems has led to the development of more efficient and cost-effective adaptive front lighting systems. The adaptive front lighting system market is also influenced by road networks, traffic, and automobile maintenance.

How is this Automotive Adaptive Front Lighting System Industry segmented and which is the largest segment?

The automotive adaptive front lighting system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

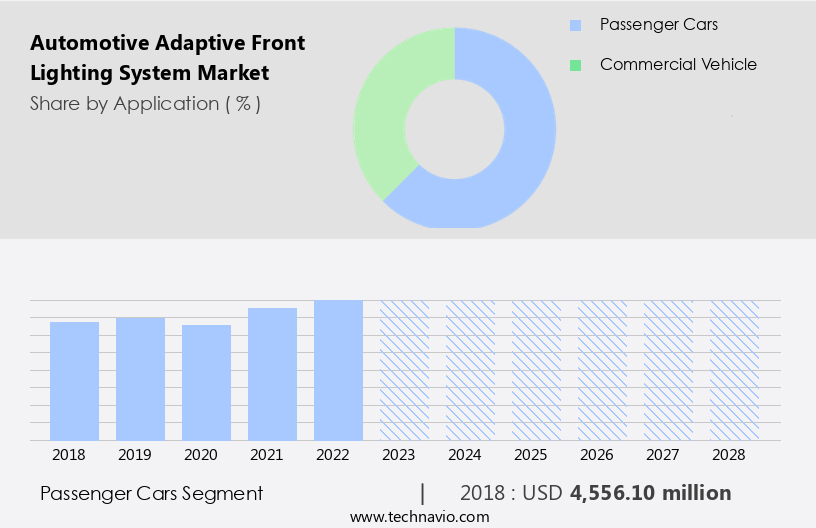

- Passenger cars

- Commercial vehicle

- Channel

- OEM

- Aftermarket

- Vehicle Type

- Mid-Segment Passenger Cars

- Sports Cars

- Premium Vehicles

- Component

- Controller

- Sensors/Camera

- Lamp Assembly

- Others

- Geography

- Europe

- Germany

- UK

- North America

- US

- Canada

- APAC

- China

- Japan

- India

- South America

- Brazil

- Middle East and Africa

- South Africa

- UAE

- Europe

By Application Insights

- The passenger cars segment is estimated to witness significant growth during the forecast period.

AFLS have gained significant traction In the market due to their ability to enhance vehicle safety and improve driving experience, especially during nighttime. These systems employ adaptive control systems that adjust Headlights based on driving circumstances, including vehicle speed, road view, and driving conditions such as rain, fog, and incoming traffic. Electric vehicles and hybrid vehicles are increasingly adopting AFLS , leveraging LED technology for energy efficiency and enhanced visibility. Premium cars are integrating advanced lighting systems like Laser headlights and OLED lighting systems, which utilize Artificial intelligence (AI) and machine learning technologies, sensors, and cameras to optimize light distribution and ensure visual comfort.

Adaptive Front Lighting Systems also cater to interior and exterior lighting needs, including LEDs for Headlamps, Rear combination lamps, and LIDAR sensors for 3D maps. These systems offer enhanced safety features, such as detecting and illuminating pedestrians and obstacles, while mitigating glare and ensuring energy efficiency. The integration of Adaptive Front Lighting Systems significantly enhances the driving experience, making nighttime driving safer and more comfortable.

Get a glance at the Automotive Adaptive Front Lighting System Industry report of share of various segments Request Free Sample

The Passenger cars segment was valued at USD 4.56 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

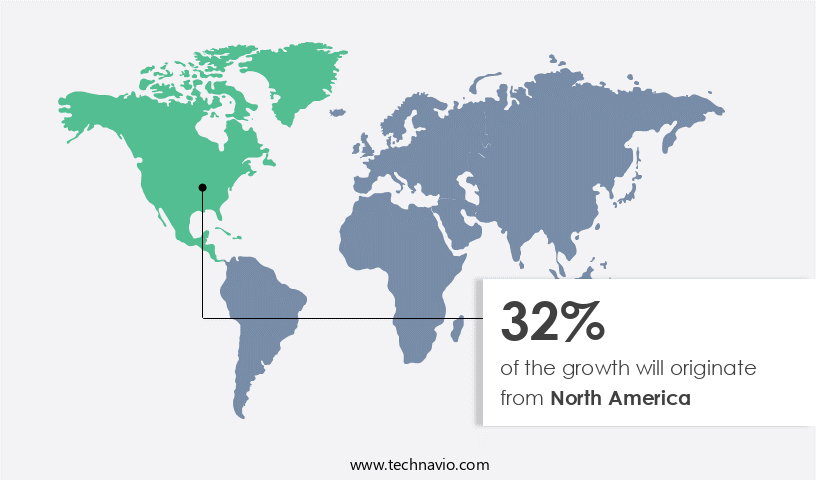

- North America is estimated to contribute 32% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The global market for AFLS is experiencing significant growth due to various factors, including advancements in vehicle technology and the increasing prioritization of passenger safety and road safety. This system, which utilizes image sensors to adjust headlight intensity and direction based on vehicle speed, road conditions, and environmental factors, is increasingly being adopted in both lightweight passenger vehicles and commercial vehicles. In the autonomous automobile sector, adaptive front lighting systems play a crucial role in enhancing nighttime safety features, reducing driver fatigue, and preventing automobile collisions. Road networks, image sensors, and LED illumination technologies are key components driving market growth.

Additionally, adaptive front lighting systems contribute to emission control, pedestrian safety, and improved safety during curve roads and traffic. Climatic factors and traffic conditions further emphasize the importance of this technology in ensuring passenger safety and reducing fatal accidents.

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive adaptive front lighting system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ams OSRAM AG

- Continental AG

- De Amertek Corp.

- Ford Motor Co.

- Hyundai Motor Group

- Johnson Electric Holdings Ltd.

- Koito Manufacturing Co. Ltd.

- Koninklijke Philips N.V.

- LG Corp.

- Lumax Industries Ltd

- Marelli Holdings Co. Ltd.

- Mazda Motor Corp.

- Robert Bosch GmbH

- SL Corp.

- Stanley Electric Co. Ltd.

- Stellantis NV

- Tata Motors Ltd.

- Texas Instruments Inc.

- Valeo SA

- Varroc Engineering Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Dynamics

Our automotive adaptive front lighting system market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Automotive Adaptive Front Lighting System Industry?

Use of AFL systems as product differentiators is the key driver of the market.

- The market is witnessing significant growth due to the increasing demand for advanced safety features in passenger cars. These systems enhance visibility during nighttime driving by adapting to various driving circumstances. Adaptive control systems, such as Cadillac's Adaptive Forward Lighting System, Hyundai's AFL System, Mercedes-Benz Active Curve Illumination, and Volkswagen's AFL System, utilize sensors, cameras, and artificial intelligence (AI) or machine learning technologies to adjust headlight intensity and direction based on driving conditions. Electric and hybrid vehicles are also incorporating these systems, with LED technology and OLED lighting systems becoming popular choices. These lighting systems offer energy efficiency, improved visibility, and visual comfort, even in challenging conditions like rain, fog, or incoming traffic.

- Additionally, AFL systems contribute to the aesthetic appeal of premium cars, with features like LIDAR sensors, 3D maps, and stylish LED headlamps, rear combination lamps, and interior lighting enhancing the overall driving experience. Pedestrian and obstacle detection, as well as glare reduction, are essential safety features offered by these systems, making them an essential component of modern vehicles.

What are the market trends shaping the Automotive Adaptive Front Lighting System Industry?

Development of AI-enabled ADAS solutions is the upcoming market trend.

- In the automotive industry, headlights have evolved significantly with the integration of adaptive control systems. These advanced lighting systems cater to various driving circumstances, enhancing vehicle safety features during nighttime. Electric and hybrid vehicles are incorporating these technologies, including LED and OLED lighting systems, to improve energy efficiency. Premium cars are increasingly adopting laser headlights and AI-driven lighting systems for superior visibility and visual comfort. AI technology plays a pivotal role in adaptive front lighting systems. These systems use sensors, cameras, and machine learning technologies to detect and respond to driving conditions, such as rain, fog, night, and incoming traffic.

- By continuously learning from these surroundings, the system can adapt to various situations, ensuring optimal lighting and enhancing the driving experience. AI-based adaptive front lighting systems can detect and recognize multiple objects, including pedestrians and obstacles, and adjust the lighting accordingly. They also reduce glare and improve visual comfort. These systems consume less power and reduce development time compared to traditional ADAS systems. Prominent automotive manufacturers are investing in AI-based adaptive front lighting systems to cater to the growing demand for personalized solutions and advanced safety features. The integration of sensors, such as LIDAR, 3D maps, and vehicle speed, further enhances the capabilities of these systems.

- They can detect the road view and adjust the headlamps and rear combination lamps accordingly. AI-based adaptive front lighting systems offer a more personalized and efficient driving experience, making them a significant impact in the automotive adaptive front loghting trends.

What challenges does the Automotive Adaptive Front Lighting System Industry face during its growth?

High cost associated with repairing ADAS technologies is a key challenge affecting the industry growth.

- The market is witnessing significant growth due to the increasing demand for advanced vehicle safety features, particularly in headlights. Adaptive control systems, which include AFL, are becoming increasingly popular as they enhance visibility during nighttime driving conditions. Electric and hybrid vehicles, as well as premium cars, are incorporating these systems due to their energy efficiency and advanced lighting technologies such as LED, laser, and OLED. However, the high repair costs associated with these systems pose a challenge to their widespread adoption. In particular, the repair cost of an AFL system can exceed USD1,000 in developed countries like the US.

- This high repair cost can negatively impact customer satisfaction and hinder the adoption of AFL systems. To address this challenge, advancements in AI and machine learning technologies are being integrated into AFL systems. Sensors, cameras, and LIDAR sensors are being used to detect driving conditions such as rain, fog, night, and incoming traffic. These systems can adjust the headlight intensity and angle in real-time, providing optimal visibility while ensuring energy efficiency. Moreover, 3D maps and vehicle speed data are being used to enhance the driving experience by providing better road view and improving pedestrian and obstacle detection. The integration of these technologies is expected to reduce repair costs and increase the adoption of AFL systems in both emerging and developed markets.

- In summary, the market is poised for growth due to the increasing demand for advanced lighting systems in passenger cars. However, high repair costs remain a significant challenge. The integration of AI, machine learning technologies, and advanced sensors is expected to address this challenge and enhance the overall driving experience.

Exclusive Customer Landscape

The automotive adaptive front lighting system market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive adaptive front lighting system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Lastest News and Recent Developments

-

In January 2024, Bosch announced the launch of its new "Smart Vision" headlamp system, featuring integrated laser technology and enhanced AI capabilities. This system significantly improves night vision, pedestrian detection, and overall driving safety, particularly in challenging weather conditions.

-

In March 2023, Valeo partnered with Luminar Technologies to develop next-generation LiDAR-based adaptive front lighting systems for autonomous vehicles. This collaboration aims to create highly integrated solutions that enhance object detection, localization, and navigation for self-driving cars.

-

In June 2022, Hyundai Motor Group unveiled its "Digital Light" system, featuring millions of micro-LEDs that can dynamically adjust to create highly precise and customizable lighting patterns, enhancing safety and driver experience while enabling unique visual expressions.

-

In September 2021, Osram launched its Eviyos Pixel LED, a high-resolution lighting system that enables precise light beam control for enhanced safety and efficiency. This technology is designed to be integrated into various vehicle types, including electric vehicles, and supports advanced driver-assistance systems (ADAS) functionalities.

Research Analyst Overview

The global headlights market is expected to experience significant growth due to the increasing adoption of adaptive control systems in passenger cars. These systems, which include LED technology, laser headlights, and OLED lighting systems, provide superior visibility during nighttime driving circumstances. Adaptive front lighting systems use sensors, cameras, and machine learning technologies to adjust headlight intensity and direction based on driving conditions, such as rain, fog, night, and incoming traffic. Electric vehicles and hybrid vehicles are also driving the market's growth, as they require advanced lighting systems for improved safety features. The integration of artificial intelligence (AI) and machine learning technologies enables headlights to learn driving patterns and adjust accordingly, enhancing the driving experience.

Premium cars are leading the adoption of advanced headlighting systems, including interior and exterior LEDs, headlamps, rear combination lamps, and LIDAR sensors. These systems offer energy efficiency, visibility, and visual comfort, making them essential for both passenger safety and comfort. Adaptive control systems are also being integrated into 3D maps and real-time road views to detect pedestrians, obstacles, and glare, ensuring a safer driving environment. Overall, the headlights market is expected to grow significantly due to the increasing demand for advanced lighting systems in passenger vehicles.

|

Automotive Adaptive Front Lighting System Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

177 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.18% |

|

Market growth 2024-2028 |

USD 3092 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.39 |

|

Key countries |

US, China, Germany, UK, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Adaptive Front Lighting System Market Research and Growth Report?

- CAGR of the Automotive Adaptive Front Lighting System industry during the forecast period

- Detailed information on factors that will drive the Automotive Adaptive Front Lighting System growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive adaptive front lighting system market growth of industry companies

We can help! Our analysts can customize this automotive adaptive front lighting system market research report to meet your requirements.

RIA -

RIA -