Automotive Chromium Market Size 2024-2028

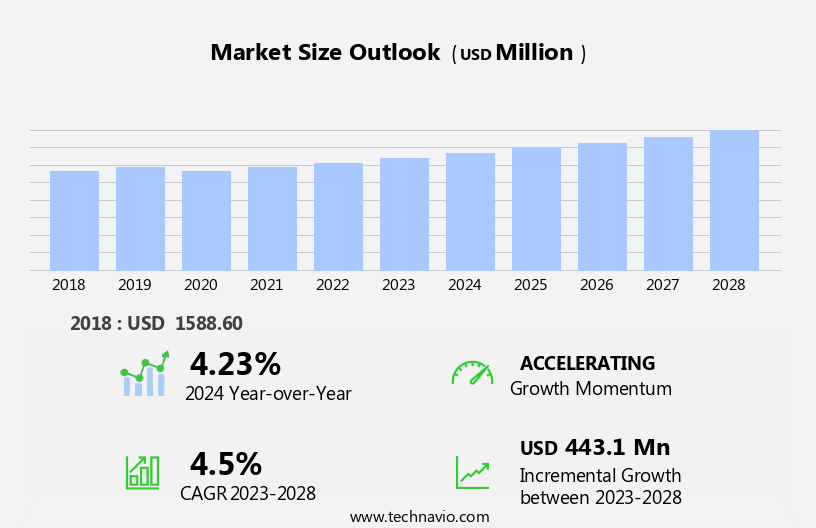

The automotive chromium market size is forecast to increase by USD 443.1 million at a CAGR of 4.5% between 2023 and 2028.

What will be the Size of the Automotive Chromium Market During the Forecast Period?

How is this Automotive Chromium Industry segmented and which is the largest segment?

The automotive chromium industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Decorative plating

- Functional plating

- Geography

- Europe

- Germany

- UK

- APAC

- China

- India

- North America

- US

- South America

- Middle East and Africa

- Europe

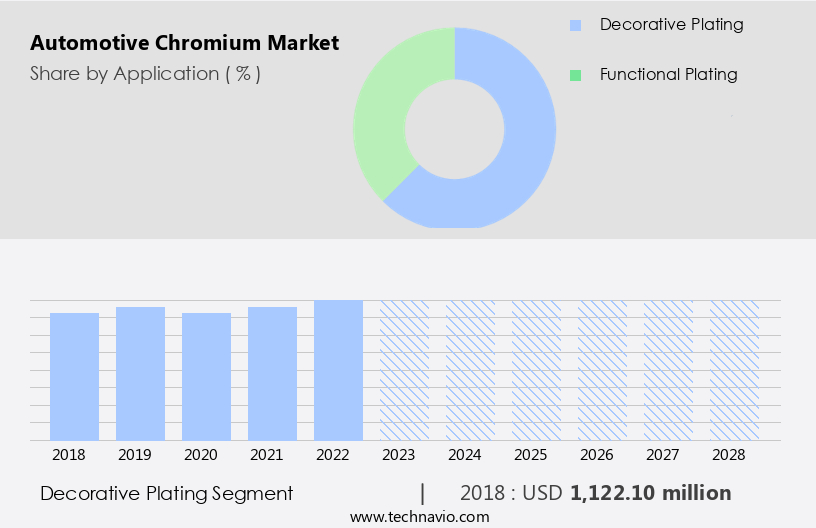

By Application Insights

- The decorative plating segment is estimated to witness significant growth during the forecast period.

Decorative chromium plating is a common practice In the automotive sector, providing both aesthetic appeal and functional benefits. This plating process enhances the visual appeal of various components, such as bumper covers, grilles, headlight bezels, interior parts, door handles, fog light housings, wheels, and truck trim, among others. It offers protection against stains, abrasion, and corrosion, thereby increasing the longevity of these parts. Additionally, chromium plating improves the performance of several automotive components, including tool and die molds, printing wear roll surfaces, brake discs, engine and suspension parts, motor shafts, machinery parts, medical devices, fasteners, and commercial firearm components. The plating process involves the deposition of chromium atoms onto a base material, typically nickel or copper, using techniques like magnetron sputtering or electroplating.

The result is a shiny, luxurious finish that adds to the brand identity of vehicles.

Get a glance at the Automotive Chromium Industry report of share of various segments Request Free Sample

The Decorative plating segment was valued at USD 1122.10 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

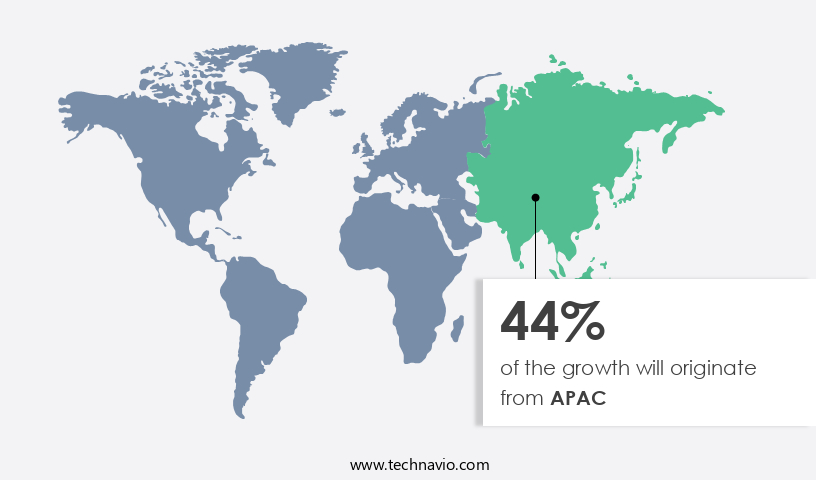

- APAC is estimated to contribute 44% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The European automotive industry, a significant contributor to the EU economy, is witnessing growth due to increased R&D investments. The European the market is experiencing growth, driven by the increasing sales of luxury vehicles. Chrome plating is extensively used for aesthetic enhancement, particularly in premium vehicles. This trend is fueling the demand for luxurious automobiles in Europe, where high-net-worth individuals are on the rise. The use of chrome for exterior components such as fins, lights, and rocket exhausts, as well as interior components, adds visual highlights and a luxurious finish. Manufacturers employ various techniques like electroplating, magnetron sputtering, and PVD to apply chromium.

Despite the toxic nature of hexavalent chromium compounds, regulations ensure safe disposal of waste materials. The automotive sector's focus on durability and visual appeal necessitates continuous production lines and batch processes. Key components like side-view mirrors, grilles, and digital display panels are often chromed for brand identity and design excellence.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Automotive Chromium Industry?

Increasing demand for decorative chrome plating is the key driver of the market.

What are the market trends shaping the Automotive Chromium Industry?

Rising demand for thin coatings in automotive industry is the upcoming market trend.

What challenges does the Automotive Chromium Industry face during its growth?

Hazardous effects of chrome plating is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The automotive chromium market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive chromium market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive chromium market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

American Electroplating Co. - The automotive industry utilizes chrome plating as a premium finishing solution for engine components and bumpers. This process involves electroplating chromium onto a base metal to enhance durability, corrosion resistance, and aesthetic appeal. Chrome plating significantly improves the longevity of these parts, ensuring optimal functionality under harsh operating conditions. The application of chromium in automotive manufacturing not only enhances the vehicle's visual appeal but also provides essential protective benefits.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Electroplating Co.

- Arlington Plating Co.

- Ashford Chroming Ltd.

- Atotech

- Borough

- Douglas Metal Finishing Ltd.

- Element Solutions Inc.

- Elsyca NV

- Galva Decoparts Pvt. Ltd.

- Kakihara Industrial Co. Ltd.

- Koch Industries Inc.

- Metzka GmbH

- Novex cz

- Plamingo Ltd.

- Royal Plating

- SARREL

- SYNERGIES CASTINGS Ltd.

- TFC Group LLC

- US Chrome Corp.

- Valley Chrome Plating Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses the production and application of chromium and chromium-containing materials In the manufacturing of various components for vehicles. Chromium, a transition metal, is known for its lustrous and resilient properties, making it an ideal choice for automotive applications. The demand for chromium In the automotive industry is driven by several factors. Firstly, its ability to create a visually appealing finish, enhancing the aesthetic value of vehicles. Chromium plating is often used on exterior components such as grilles, side-view mirrors, and trim, as well as interior finishes. The production process for chromium-plated components involves several steps. The base material is first prepared, and a layer stack is created, which includes a plastic layer, a base coating, and a topcoat.

The topcoat is typically a transparent lacquer that protects the chromium layer. The chromium is then applied through a process known as vacuum deposition or magnetron sputtering. During the vacuum deposition process, chromium atoms are ejected from a target in a high vacuum chamber. An electric field is applied, ionizing the gas molecules, which then form a plasma. The plasma is accelerated towards the component, where the chromium atoms adhere. Magnets are used to control the direction of the plasma, ensuring precise application. The densified plasma created during this process results in a durable and uniform chromium layer.

However, challenges remain In the production process, including the use of toxic materials such as hexavalent chromium compounds, which can be carcinogenic. Regulations governing the use of these materials are strict, and waste management is a significant concern. The automotive suppliers play a crucial role In the production and application of chromium-plated components. They work closely with designers and carmakers to create concepts that meet the evolving needs of consumers. For instance, the increasing popularity of electric cars has led to the development of new chromium-plated components for electric drivetrains and radiator grilles. In recent years, there has been a trend towards the use of alternative materials, such as PVD (Physical Vapor Deposition), which offers a more eco-friendly alternative to traditional chromium plating.

PVD uses less energy and produces less waste, making it an attractive option for automotive suppliers looking to reduce their environmental impact. The market is dynamic and constantly evolving, driven by advancements in technology and changing consumer preferences. The use of chromium in automotive applications is expected to continue, as it offers a durable and visually appealing finish that enhances the overall value of vehicles. However, the industry must continue to address the challenges associated with the production and disposal of chromium-containing materials to ensure sustainability and compliance with regulations.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

140 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 443.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, Germany, China, UK, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Chromium Market Research and Growth Report?

- CAGR of the Automotive Chromium industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, APAC, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive chromium market growth of industry companies

We can help! Our analysts can customize this automotive chromium market research report to meet your requirements.

RIA -

RIA -