Automotive Clutch Actuator Market Size 2025-2029

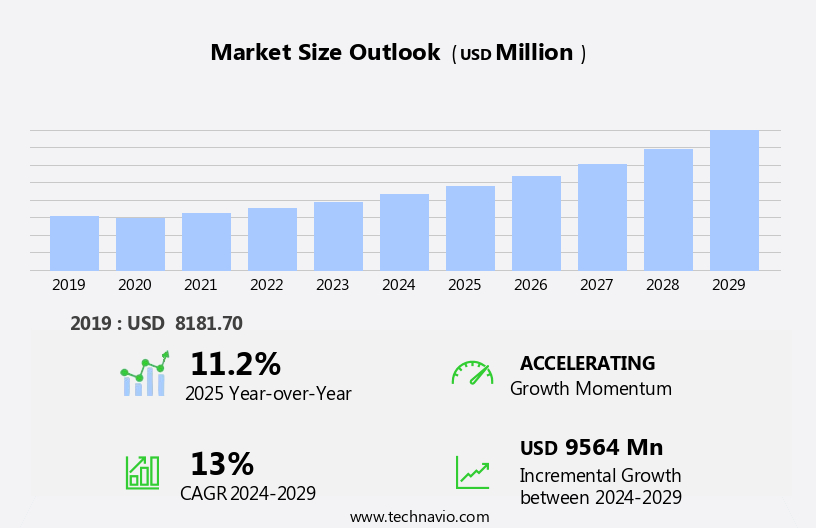

The automotive clutch actuator market size is forecast to increase by USD 9.56 billion at a CAGR of 13% between 2024 and 2029.

- The market is experiencing significant growth, driven primarily by the increasing adoption of automatic transmission systems in vehicles. This trend is being fueled by consumer preferences for smooth and efficient driving experiences, leading to an increase in demand for advanced clutch actuators that enhance transmission performance. Additionally, technological advancements in actuator design and manufacturing processes are enabling the production of more precise, durable, and cost-effective components. However, the market is not without challenges. The market encompasses the production and supply of clutch actuators for various automotive applications, including automatic transmission systems in passenger cars and commercial vehicles. Tier-1 suppliers are under increasing cost pressure to reduce manufacturing costs while maintaining high-quality standards. This is leading to intense competition and a focus on innovation to differentiate offerings and maintain market share. Despite these challenges, the market presents significant opportunities for companies that can effectively navigate the competitive landscape and meet the evolving demands of OEMs and consumers for advanced, cost-effective clutch actuator solutions.

What will be the Size of the Automotive Clutch Actuator Market during the forecast period?

- The market encompasses the production and supply of clutch actuators for various automotive applications, including automatic transmission systems in passenger cars and commercial vehicles. Clutch actuators play a crucial role In the engagement and disengagement of clutch plates in manual and automatic transmissions, enabling seamless gear shifting and power transmission. The market is driven by the growing demand for advanced automatic transmission systems in premium vehicles, as well as the increasing adoption of electronic clutch actuators for improved fuel economy and reduced CO2 emissions.

- Furthermore, the integration of clutch actuators in autonomous vehicles and adaptive cruise control systems is expected to fuel market growth. Despite these growth opportunities, market dynamics are influenced by factors such as the increasing popularity of manual transmission systems in certain regions and the ongoing development of more efficient and cost-effective clutch actuator technologies.

How is this Automotive Clutch Actuator Industry segmented?

The automotive clutch actuator industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Passenger cars

- Commercial vehicles

- Type

- Mechanical

- Hydraulic

- Geography

- North America

- US

- Canada

- APAC

- China

- India

- Japan

- Europe

- France

- Germany

- Italy

- UK

- South America

- Brazil

- Middle East and Africa

- North America

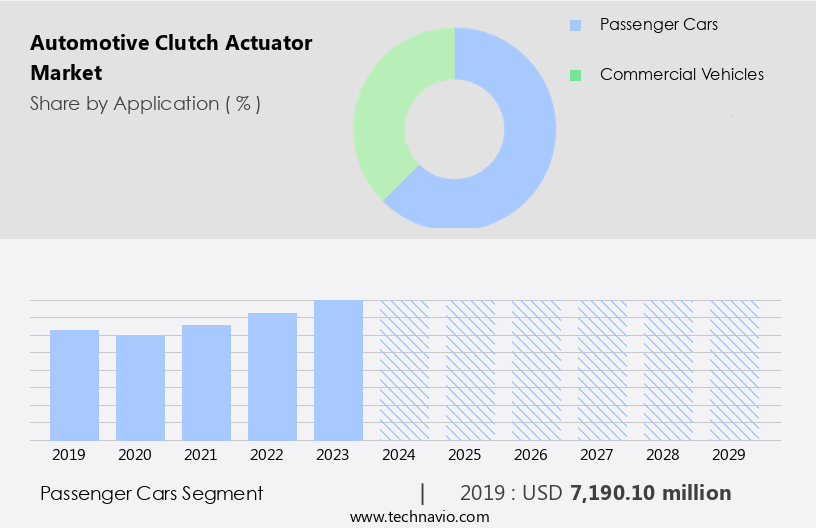

By Application Insights

The passenger cars segment is estimated to witness significant growth during the forecast period. The market is primarily driven by the widespread adoption of automatic transmission systems in passenger cars. This trend is attributed to the increasing preference for convenience and fuel efficiency in personal transportation. Automatic transmission systems have become increasingly sophisticated, with the integration of electronic components such as clutch actuators, throttle actuators, closure actuators, and engine couplings. These systems enable features like adaptive cruise control, automated brake assist, and lane keep assist, enhancing safety and comfort. Commercial vehicles, including heavy commercial vehicles and light commercial vehicles, also utilize clutch actuator modules for their transmission systems.

Get a glance at the market report of share of various segments Request Free Sample

The passenger cars segment was valued at USD 7.19 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

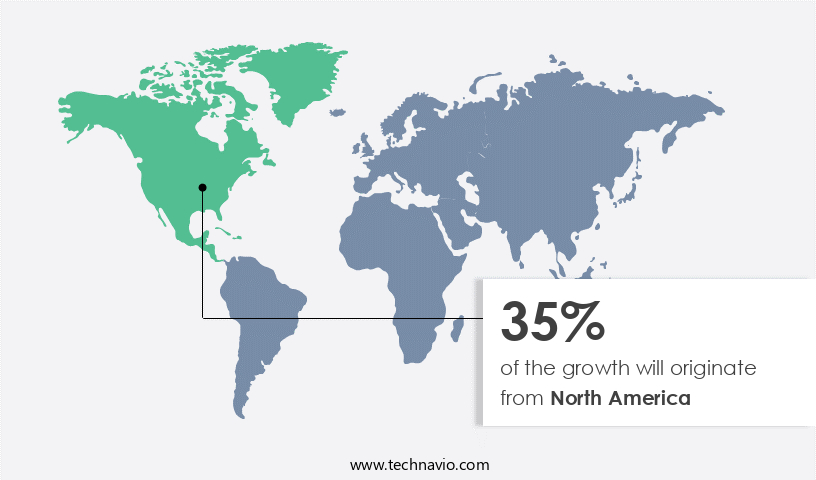

North America is estimated to contribute 35% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The North American automotive market leads the global clutch actuator industry due to the highest penetration rate of automatic transmission systems in passenger cars and commercial vehicles. Notable automakers, such as General Motors and Ford Motor, are based In the region, driving market growth. Advanced technologies, including electronic clutch actuators, adaptive cruise control, Automotive Advanced Driver Assistance System (ADAS), and lane keep assist, are increasingly incorporated into automatic transmission systems. These innovations contribute to fuel-efficient vehicles and reduced CO2 emissions, aligning with consumer preferences and regulatory requirements.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Automotive Clutch Actuator Industry?

- Rise in demand for automatic transmission systems is the key driver of the market. The automatic transmission market is experiencing significant growth due to the increasing preference for more efficient, comfortable, and safer driving experiences. Automatic transmission systems offer several advantages over manual transmission systems, including the elimination of the need to apply the clutch in stop-and-go traffic, improved fuel economy, and enhanced comfort and convenience.

- Transmission Control Units (TCUs) are a crucial component of automatic transmission systems, allowing for seamless shifting and improved driving dynamics. The global shift towards automatic transmissions is driven by the growing demand for comfort and safety features in vehicles, making it an attractive market for investors and manufacturers alike. Automatic transmissions provide a better driving experience by reducing driver effort and improving vehicle performance, making them an essential component of modern vehicles.

What are the market trends shaping the Automotive Clutch Actuator Industry?

- Advancements in actuator technology is the upcoming market trend. The market is witnessing substantial growth due to advancements in actuator technology. Actuators are essential components of clutch systems, facilitating efficient power transfer and enabling smooth gear shifts. In response to the evolving automotive industry, manufacturers are investing in enhancing actuator technology to cater to the rising demands for performance, precision, and reliability.

- One significant advancement is the integration of intelligent control units, sensors, and high-response actuators. This innovation leads to improved clutch engagement and disengagement, resulting in seamless gear transitions and superior driving experiences. For instance, BorgWarner, a prominent automotive supplier, has introduced the integrated clutch control (ICT) actuator system. This technology embodies the industry's commitment to delivering advanced solutions that cater to the ever-evolving automotive landscape.

What challenges does the Automotive Clutch Actuator Industry face during its growth?

- Increasing cost pressure on Tier-1 suppliers is a key challenge affecting the industry growth. The automotive industry's value chain dynamics have shifted in recent years, with Original Equipment Manufacturers (OEMs) passing on liabilities and cost pressures to Tier-1 suppliers. In response, these suppliers have relayed these pressures to component manufacturers, including those producing clutch actuators and transmission electronics.

- The adoption of advanced technologies such as transmission control units (TCUs) and clutch actuators has led to a decrease in vehicle demand in emerging markets due to increasing vehicle prices. Additionally, stringent emission regulations have forced engine and drivetrain designers and manufacturers to consistently update their designs and technologies. These factors have created a challenging business environment for clutch actuator manufacturers.

Exclusive Customer Landscape

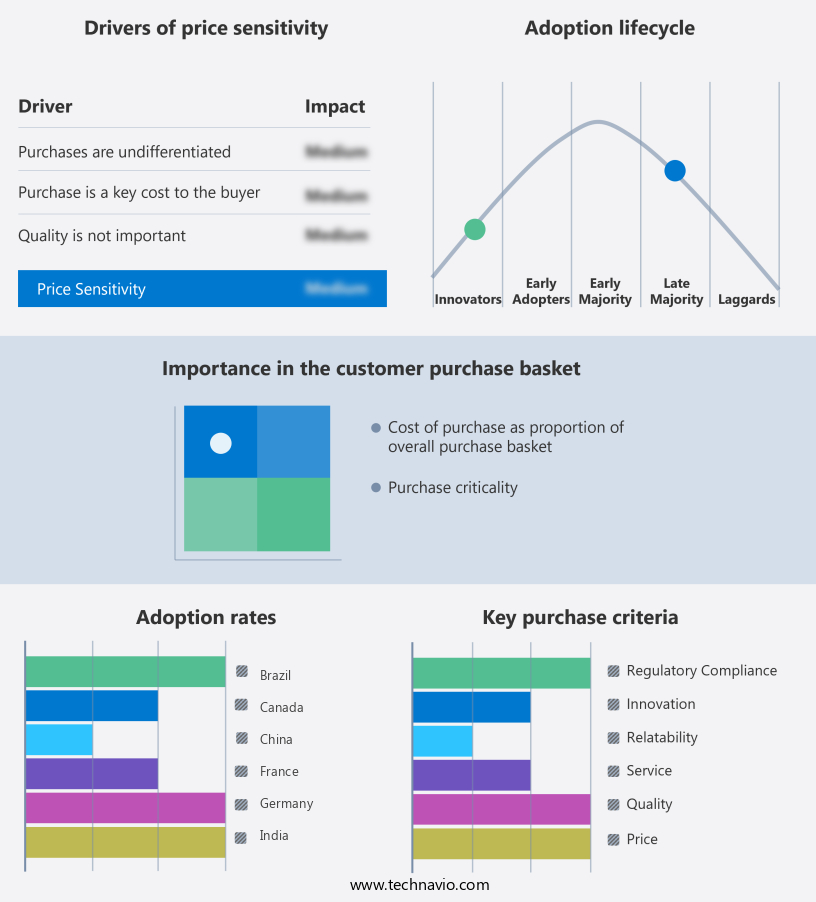

The automotive clutch actuator market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive clutch actuator market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive clutch actuator market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

ATESTEO GmbH and Co. KG - The company offers automotive clutch actuators for use in test benches for transmissions, gearboxes, drivetrains, and powertrains.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AVTEC Ltd.

- BorgWarner Inc.

- Buhler Motor GmbH

- Continental AG

- CTS Corp.

- Eaton Corp. plc

- Infineon Technologies AG

- Johnson Electric Holdings Ltd.

- Kendrion NV

- Knorr Bremse AG

- Kongsberg Automotive ASA

- Magna International Inc.

- Nidec Corp.

- Robert Bosch GmbH

- Schaeffler AG

- Taizhou Juhang Automation Equipement Technology Co. Ltd.

- Valeo SA

- Wabtec Corp.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market plays a significant role In the functionality of automatic transmission systems in various vehicle types, including premium passenger cars and commercial vehicles. Clutch actuators are essential components that facilitate the engagement and disengagement of clutch plates In these transmissions, enabling smooth power transfer from the engine to the transmission. In recent years, the automotive industry has witnessed a shift towards electronic clutch actuators, which offer improved performance and efficiency compared to traditional clutch pedal systems. These advanced actuators are integrated into various vehicle systems, such as adaptive cruise control, automated brake assist, and lane keep assist, to ensure seamless vehicle operation.

In addition, the growing popularity of fuel-efficient and low-emission vehicles has driven the demand for clutch actuators that contribute to optimized powertrain performance. The integration of electric motors, such as BLDC actuators, into clutch actuator modules has been instrumental in enhancing fuel economy and reducing CO2 emissions in both passenger cars and commercial vehicles. Moreover, the increasing adoption of frictionless coupling technology in transmission systems has led to the development of advanced adaptive control systems. These systems enable the clutch actuator to adjust clutch engagement and disengagement based on driving conditions, ensuring optimal power transfer and improved vehicle performance.

Furthermore, the market is expected to experience significant growth due to the increasing production volume of automatic transmission systems in both passenger cars and commercial vehicles. The integration of clutch actuators in autonomous vehicles is also anticipated to boost market growth, as these vehicles require precise powertrain control for seamless operation. Furthermore, the development of engine coupling systems that integrate clutch actuators has led to advancements in transmission technology. These systems enable the engine and transmission to operate as a single unit, improving overall vehicle efficiency and performance. The integration of electronic and adaptive control technologies, the increasing demand for fuel-efficient vehicles, and the growing adoption of autonomous vehicles are some of the key factors driving market growth. The future of the market is promising, with numerous opportunities for innovation and advancements in powertrain technology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

207 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13% |

|

Market growth 2025-2029 |

USD 9.56 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

11.2 |

|

Key countries |

US, China, Canada, Germany, Japan, UK, India, France, Brazil, and Italy |

|

Competitive landscape |

Leading Companies, market growth and forecasting, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Clutch Actuator Market Research and Growth Report?

- CAGR of the Automotive Clutch Actuator industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive clutch actuator market growth of industry companies

We can help! Our analysts can customize this automotive clutch actuator market research report to meet your requirements.

RIA -

RIA -