Automotive Crankcase Ventilation System Market Size 2025-2029

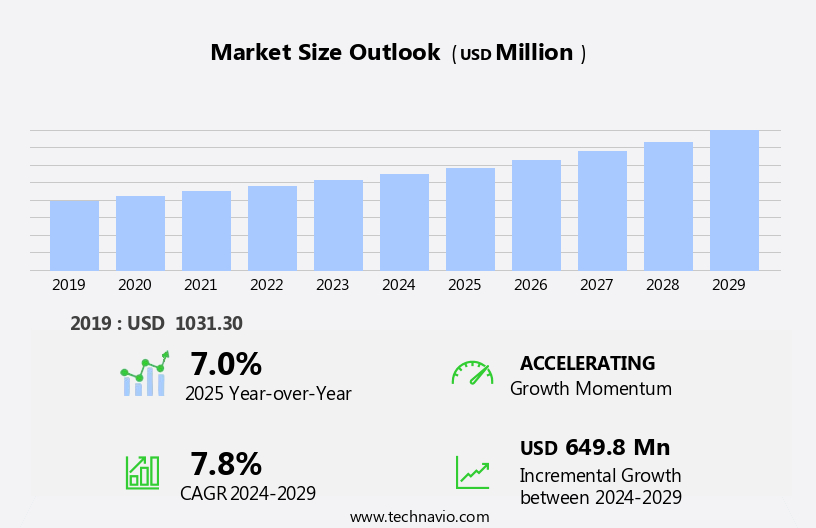

The automotive crankcase ventilation system market size is forecast to increase by USD 649.8 million, at a CAGR of 7.8% between 2024 and 2029.

- The market is experiencing significant growth due to the increasing demand for SUVs and pick-up trucks. These vehicle types often have larger engines and require effective crankcase ventilation systems to minimize emissions and improve fuel efficiency. Another key trend driving market growth is the emergence of additive manufacturing in automotive manufacturing. This technology enables the production of complex components at a lower cost and with greater design freedom, leading to more advanced crankcase ventilation systems. However, the market also faces challenges, including the increasing adoption of electric vehicles. These vehicles do not require traditional crankcase ventilation systems, as they do not have internal combustion engines.

- Additionally, stringent emission regulations are pushing automakers to develop more efficient systems, which may increase the cost of crankcase ventilation systems. Electric vehicles (EVs) and alternative fuel vehicles present unique challenges for crankcase ventilation systems due to their distinct engine cooling requirements. Companies seeking to capitalize on market opportunities should focus on developing advanced, cost-effective crankcase ventilation systems for gasoline-powered vehicles and exploring new applications in electric vehicles. Navigating the challenges will require continuous innovation and collaboration with suppliers and regulatory bodies.

What will be the Size of the Automotive Crankcase Ventilation System Market during the forecast period?

The market is an intricate web of continuous evolution and dynamic market activities. This system, integral to internal combustion engines, plays a pivotal role in managing crankcase pressure, controlling air flow, and reducing emissions. The system's applications extend beyond vacuum control and emissions reduction, encompassing engine performance, durability, and fuel economy. Fuel economy regulations and emissions standards have fueled the market's growth, necessitating advanced crankcase ventilation technologies. These include positive crankcase ventilation (PCV) systems, crankcase ventilation lines, and oil separators. The integration of air-to-oil separators and intake manifolds further optimizes the system's functionality. Engine design, combustion chamber, and crankcase breather are crucial components of the crankcase ventilation system.

Key components of crankcase ventilation systems include valves, hoses, and filters. These elements work in tandem to minimize engine wear, oil degradation, and oil consumption. The system's efficiency is further enhanced by oil separators, oil catch cans, and crankcase ventilation filters. The market's landscape is shaped by the ongoing quest for engine life extension, improved fuel efficiency, and reduced exhaust emissions. As such, the crankcase ventilation system market continues to unfold, with innovations in technology and design shaping its future trajectory. The integration of these advancements into the broader automotive components sector underscores the system's significance in the automotive industry.

How is this Automotive Crankcase Ventilation System Industry segmented?

The automotive crankcase ventilation system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Channel

- OEM

- Aftermarket

- Application

- PC

- LCV

- HCV

- Technology

- Positive crankcase ventilation

- Closed crankcase ventilation

- Negative crankcase ventilation

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

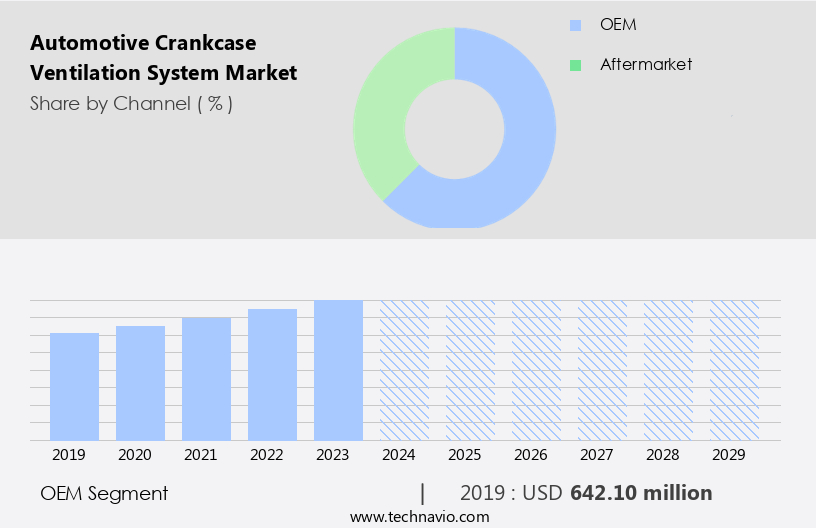

By Channel Insights

The OEM segment is estimated to witness significant growth during the forecast period. The market encompasses the sales of components that manage crankcase pressure and regulate the flow of oil vapor and blowby gases in internal combustion engines. These systems, which include Positive Crankcase Ventilation (PCV) and crankcase breather, are essential for engine performance and emissions reduction. Manufacturers of automotive crankcase ventilation systems are Tier-1 suppliers, supplying directly to automobile manufacturers. Some OEMs, such as Ford Motor Co. and General Motors Co., also produce and sell their own systems under different brand names. Market growth is primarily driven by the expanding automotive industry and increasing demand for advanced engine technology to meet emissions standards and improve fuel efficiency.

Automotive crankcase ventilation systems play a crucial role in engine management, controlling air flow and maintaining engine lubrication. They help reduce oil consumption, prevent engine wear, and minimize oil degradation. The systems also ensure proper combustion chamber function and maintain engine durability by filtering out oil mist and separating oil from the intake air stream. Environmental regulations and fuel economy standards further fuel market growth, as these systems contribute to emissions reduction and improved fuel efficiency. The market is expected to continue evolving with advancements in automotive technology, such as air-to-oil separators and crankcase ventilation filters, enhancing the overall performance and longevity of internal combustion engines.

The OEM segment was valued at USD 642.10 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

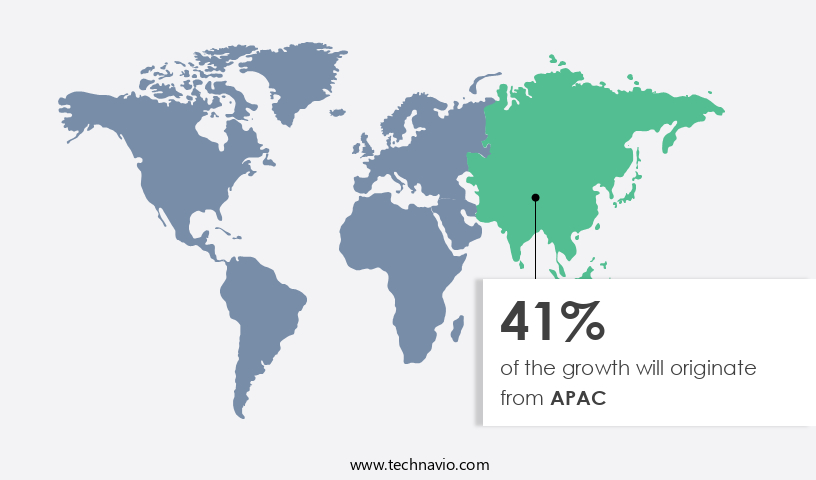

APAC is estimated to contribute 41% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The automotive industry in the Asia Pacific (APAC) region is experiencing significant growth, driven by improving economic conditions and increased consumer purchasing power. This economic expansion, led by countries such as China, India, Thailand, Indonesia, and South Korea, has resulted in increased sales of both passenger and commercial vehicles. The market is diverse, with applications in buses and coaches, heavy commercial vehicles (HCV), and light commercial vehicles (LCV). The region's industrial and infrastructural development has also contributed to the demand for commercial vehicles. Automotive technology plays a crucial role in this market, with advancements in engine management systems, emissions reduction, and engine performance being key areas of focus. Positive crankcase ventilation (PCV) systems, crankcase ventilation lines, oil separators, and air-to-oil separators are essential components in maintaining engine durability and reducing emissions.

These systems help control crankcase pressure, manage oil vapor, and prevent blowby gases from entering the engine. Environmental regulations and emissions standards continue to influence engine design, with a focus on fuel economy and fuel efficiency. The use of PCV valves, oil catch cans, and crankcase ventilation filters help improve engine life and reduce oil consumption. Exhaust systems are also undergoing advancements to minimize emissions and improve overall engine performance. Air flow control and engine lubrication systems are essential for maintaining engine performance and reducing wear and oil degradation. The integration of these technologies with crankcase ventilation systems helps ensure efficient engine operation and prolong engine life. Technological advancements in engine management systems, emissions reduction, and engine performance are key factors contributing to this growth. The integration of crankcase ventilation systems, oil management components, and exhaust systems is essential for maintaining engine durability and reducing emissions, making them crucial components in the evolving automotive landscape.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Automotive Crankcase Ventilation System Industry?

- The increasing preference for SUVs and pick-up trucks among consumers serves as the primary market catalyst. The market is driven by the increasing demand for internal combustion engines, particularly in the production of SUVs and pick-up trucks. These vehicles require robust crankcase ventilation systems to ensure engine durability by preventing oil mist formation and maintaining proper engine lubrication. Crankcase ventilation systems, including air-to-oil separators, crankcase breathers, PCV valves, and oil catch cans, play a crucial role in minimizing oil consumption and prolonging engine life. The crankcase, a vital component of the engine, houses the pistons and connecting rods. Seals, such as piston rings, prevent the escape of engine oil and combustion gases into the crankcase.

- The market growth can be attributed to the rising preference for larger vehicles and the need for improved engine performance and fuel efficiency. As a result, manufacturers are investing in advanced crankcase ventilation technologies to meet the evolving demands of consumers and regulatory bodies.

What are the market trends shaping the Automotive Crankcase Ventilation System Industry?

- Additive manufacturing, also known as 3D printing, is gaining significant traction in the automotive industry, marking a notable market trend in this sector. This innovative technology allows for the production of complex and lightweight components, offering potential benefits in terms of reduced production time, increased design freedom, and potential cost savings. The market is experiencing significant growth due to the increasing focus on fuel economy regulations and fuel efficiency. This trend is driving the demand for advanced crankcase ventilation systems that effectively control blowby gases while maintaining a reasonable maintenance interval. Manufacturers are responding by innovating engine designs and incorporating crankcase ventilation filters to improve overall engine performance and reduce emissions. Advancements in technology, such as additive manufacturing, are playing a crucial role in the development of lightweight and cost-effective crankcase ventilation components. Additive manufacturing, also known as 3D printing, enables the production of intricate components with precise material composition.

- This results in reduced raw material waste and lower production costs, making it an attractive option for automotive manufacturers. The implementation of stringent emission norms and the growing emphasis on fuel efficiency are expected to continue fueling the growth of the market. As manufacturers strive to meet these regulations and consumer demands, they will continue to invest in research and development to create more efficient and effective crankcase ventilation systems.

What challenges does the Automotive Crankcase Ventilation System Industry face during its growth?

- The escalating adoption of electric vehicles poses a significant challenge to the growth of the automotive industry. The automotive industry is increasingly focusing on engine management systems to minimize engine emissions and enhance fuel efficiency. One such technology is the Crankcase Ventilation System (CVS), which plays a crucial role in reducing harmful emissions and maintaining crankcase pressure. The CVS is an integral part of the Positive Crankcase Ventilation (PCV) system, which recirculates unburnt hydrocarbons from the crankcase back into the engine for combustion. Vacuum control in the CVS system helps regulate the flow of gases, ensuring optimal engine performance and emissions reduction. The system's importance is further boosted by stringent environmental regulations that mandate reduced vehicle emissions.

- Automotive technology continues to evolve, with a focus on improving components' efficiency and reducing environmental impact. Crankcase Ventilation Systems are a critical component in this regard, as they help minimize oil vapor emissions and contribute to overall emissions reduction. The growing emphasis on reducing vehicular pollution and complying with environmental regulations is driving the demand for advanced CVS technology. As the market for automotive technology continues to grow, so too will the demand for efficient and eco-friendly crankcase ventilation systems.

Exclusive Customer Landscape

The automotive crankcase ventilation system market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive crankcase ventilation system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive crankcase ventilation system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aisan Industry Co. Ltd. - The company specializes in advanced crankcase ventilation systems, including positive crankcase ventilation valves.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aisan Industry Co. Ltd.

- Alfdex AB

- Cummins Inc.

- Donaldson Co. Inc.

- Eaton Corp. plc

- Hengst SE

- korens

- MAHLE GmbH

- MANN HUMMEL International GmbH and Co. KG

- Mikuni Corp.

- Parker Hannifin Corp.

- Polytec Holding AG

- Robert Bosch GmbH

- Sogefi Spa

- Tenneco Inc.

- Wartsila Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Crankcase Ventilation System Market

- In February 2023, Continental AG, a leading automotive technology company, introduced its latest crankcase ventilation system, the CVT-10, which features advanced filtration technology to reduce harmful emissions. This system is expected to significantly improve fuel efficiency and reduce carbon footprint in vehicles (Continental AG press release).

- In July 2024, Magna International, a global automotive supplier, announced a strategic partnership with Bosch to develop next-generation crankcase ventilation systems. This collaboration aims to enhance Magna's product portfolio and strengthen its position in the automotive industry (Magna International press release).

- In October 2024, Valeo, a leading automotive components and systems manufacturer, unveiled its new generation crankcase ventilation system, which incorporates an electric motor to improve efficiency and reduce emissions. This system is expected to be adopted by major automakers, including Volkswagen and Peugeot (Valeo press release).

- In March 2025, the European Union passed a new regulation mandating the installation of advanced crankcase ventilation systems in all new passenger cars from 2027. This regulation aims to reduce harmful emissions and improve air quality, driving demand for advanced crankcase ventilation systems in Europe (European Union press release).

Research Analyst Overview

- The market is experiencing significant growth, driven by the increasing demand for engine durability testing and engine life extension in various vehicle types, including electric, hybrid, and conventional engines. The integration of electronic control units (ECUs) in engine management systems has led to advanced engine performance optimization and emission control, necessitating effective crankcase ventilation systems. Engine air intake systems and oil additives play crucial roles in maintaining engine efficiency and reducing engine noise and vibration.

-

The Automotive Crankcase Ventilation System Market is witnessing steady growth due to increasing concerns over engine reliability and emissions control. A well-functioning system ensures efficient removal of gases from the crankcase, reducing engine vibration and enhancing overall performance. Factors like oil change interval, maintenance of the engine cooling system, and regular automotive service play a crucial role in prolonging engine life. Advanced electronic control unit technologies are being integrated to optimize performance and emissions. Additionally, components like the EGR valve and oxygen sensor contribute to cleaner emissions and improved efficiency.

- Engine sensors, such as oxygen sensors and EGR valves, monitor exhaust gas recirculation and optimize engine oil viscosity for improved engine maintenance and reliability. In the automotive aftermarket, engine oil quality and automotive parts manufacturers focus on developing innovative solutions to cater to the evolving needs of the industry. Engine repair and service providers leverage crankcase ventilation technology to diagnose and address issues related to engine performance and vehicle emission control. As the market continues to evolve, the integration of advanced technologies and materials will further enhance the efficiency and effectiveness of crankcase ventilation systems.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Crankcase Ventilation System Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

224 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.8% |

|

Market growth 2025-2029 |

USD 649.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.0 |

|

Key countries |

China, US, Japan, India, South Korea, Germany, UK, Canada, Italy, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Crankcase Ventilation System Market Research and Growth Report?

- CAGR of the Automotive Crankcase Ventilation System industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive crankcase ventilation system market growth of industry companies

We can help! Our analysts can customize this automotive crankcase ventilation system market research report to meet your requirements.

RIA -

RIA -