Automotive Fuel Delivery System Market Size 2025-2029

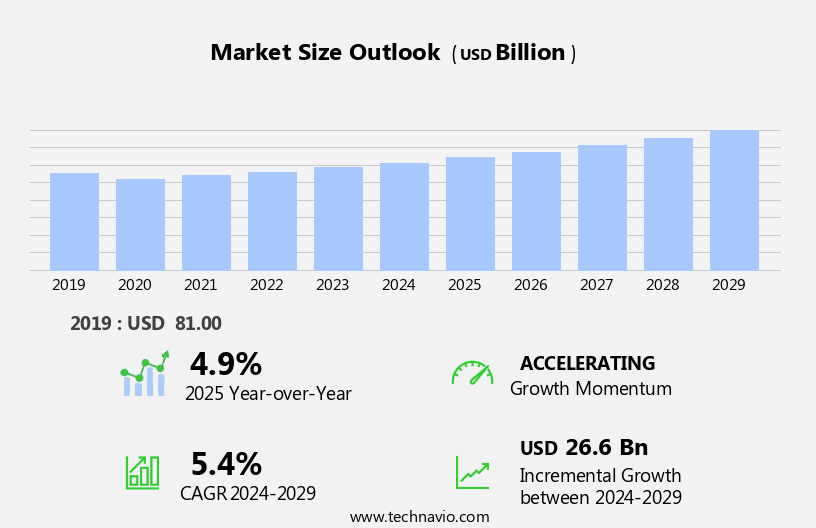

The automotive fuel delivery system market size is forecast to increase by USD 26.6 billion, at a CAGR of 5.4% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing production of vehicles and the shift toward gasoline direct injection systems. This trend is expected to continue as automakers seek to improve engine efficiency and reduce emissions. However, the market also faces challenges, including the growing adoption of electric vehicles. This shift poses a significant obstacle for traditional fuel delivery system manufacturers, as electric vehicles do not require the same intricate fuel delivery systems as their gasoline counterparts. Fuel quality, additives, and stability are crucial considerations, as is fuel system safety and security. This shift towards sustainable transportation solutions is gaining momentum, with many governments offering incentives to both consumers and businesses to adopt electric vehicles (EVs) and invest in charging infrastructure.

- Effective strategic planning and operational agility will be essential for companies seeking to capitalize on market opportunities and navigate challenges in the evolving automotive fuel delivery system landscape. To remain competitive, companies must adapt to this changing landscape by exploring opportunities in the electric vehicle market or developing hybrid fuel delivery systems. AI-powered tensioners and finite element analysis are the future, offering advanced capabilities for predictive maintenance and improved operational efficiency.

What will be the Size of the Automotive Fuel Delivery System Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market encompasses various aspects, including fuel system design, architecture, and compatibility. Fuel delivery rate is a crucial factor in optimizing engine performance, while fuel system integration ensures seamless interaction between components. Fuel rail pressure and fuel injection pressure significantly influence fuel atomization and spray pattern. In the realm of fuel system modeling and simulation, advancements in technology facilitate more accurate predictions and enhance system efficiency.

- The fuel system aftermarket caters to the demand for replacement parts and upgrades, driven by consumer preferences and regulatory requirements. Fuel system design innovations, such as advanced fuel system patents, continue to shape the industry landscape. Key industries, including the passenger car, 2-wheeler, and commercial vehicle sectors, rely on belt drives, V-belts, variable belts, synchronous timing belts, and accessory drive belts for power transmission.

How is this Automotive Fuel Delivery System Industry segmented?

The automotive fuel delivery system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

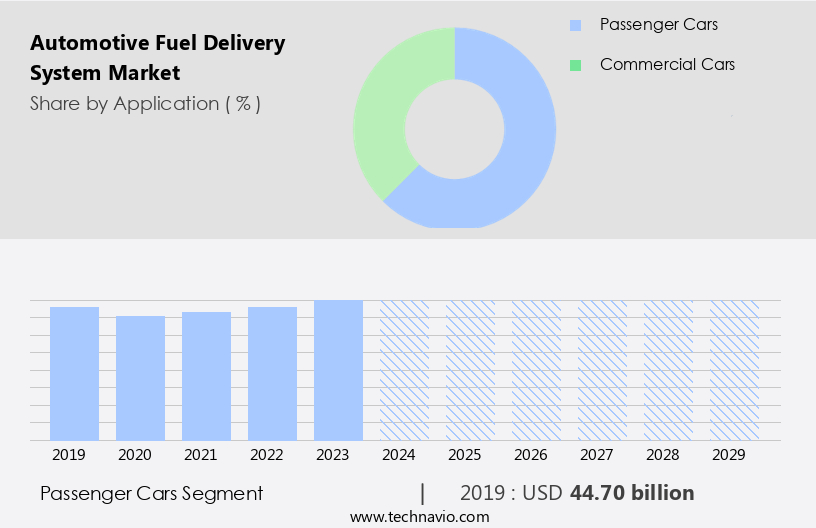

- Passenger cars

- Commercial cars

- Fuel Type

- Gasoline

- Diesel

- Others

- Component

- Fuel pump

- Fuel injector

- Fuel pressure regulator

- Fuel rail

- Others

- Geography

- North America

- US

- Mexico

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The passenger cars segment is estimated to witness significant growth during the forecast period. The passenger car segment in The market showcases advanced technologies and specialized engineering. Encompassing compact urban models to luxury automobiles, these systems prioritize performance, efficiency, and reliability while adhering to stringent environmental regulations, such as Euro 6 and Bharat Stage VI. Modern fuel delivery systems predominantly incorporate Gasoline Direct Injection (GDI) and Electronic Fuel Injection (EFI) technologies. These innovations optimize fuel atomization and combustion, reducing emissions and enhancing fuel economy. Fuel system advancements extend to fuel lines, calibration, rails, sensors, diagnostics, and management systems. Direct injection, common rail injection, port injection, and hybrid fuel systems are key trends.

Fuel efficiency, corrosion, and delivery timing are ongoing concerns. High-pressure fuel pumps, fuel filters, and injectors ensure system durability. Fuel system regulations and maintenance are essential for market growth. The automotive, mining, and aerospace sectors heavily utilize tensioners in engines, automotive tensioners, and hydraulically operated systems.

The Passenger cars segment was valued at USD 44.70 billion in 2019 and showed a gradual increase during the forecast period.

The Automotive Fuel Delivery System Market is evolving with advancements in fuel tanks that enhance storage efficiency and durability. Improving fuel stability ensures optimal engine performance and reduced emissions. Manufacturers prioritize fuel system reliability, integrating cutting-edge materials and technologies for enhanced safety. Regular fuel system maintenance is crucial for longevity, minimizing risks of contamination and degradation. Compliance with fuel system standards ensures operational efficiency and environmental responsibility. Strengthened fuel system security measures protect against leaks and theft, promoting safer fuel management. Continuous fuel system innovations drive market growth, incorporating intelligent monitoring solutions for precision fuel regulation.

The Automotive Fuel Delivery System Market is evolving with advancements in fuel spray pattern optimization, enhancing combustion efficiency and engine performance. Innovations in fuel system architecture improve integration across vehicle types, ensuring seamless compatibility. Manufacturers focus on fuel system compatibility, enabling versatile applications across different powertrains, including traditional and hybrid models. Advanced fuel system simulation plays a crucial role in testing and refining fuel delivery mechanisms, supporting real-time analysis and system improvements. China is projected to lead the region's industrial growth, particularly in sectors like industrial machinery, mining, agriculture, and construction.

Regional Analysis

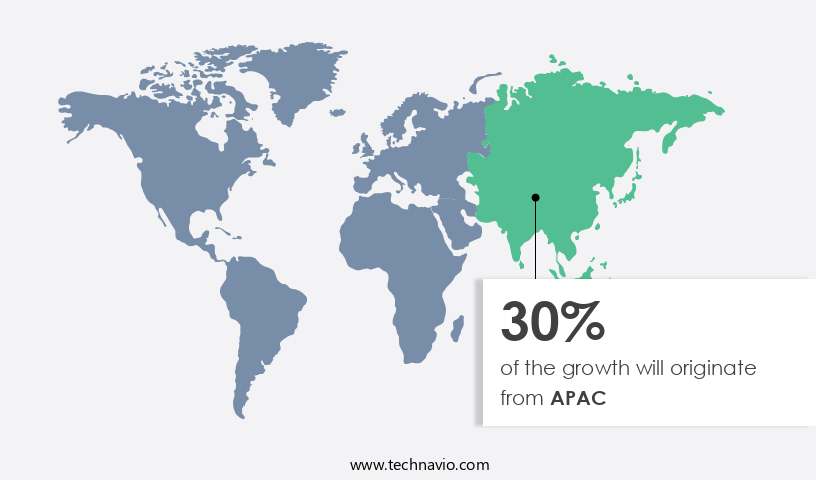

APAC is estimated to contribute 30% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The Asia-Pacific (APAC) region is at the forefront of the global automotive industry, driving market dynamics in fuel delivery systems. Countries such as China, India, Japan, and South Korea, leading in vehicle manufacturing and technological advancements, significantly influence the regional market. Fuel system advancements, including direct injection, common rail injection, and gasoline direct injection, are gaining popularity due to their ability to improve fuel efficiency and reduce emissions. Fuel system safety, calibration, and certification are crucial considerations, with high-pressure fuel pumps and fuel system durability ensuring reliable fuel delivery. Fuel quality, stability, and corrosion resistance are essential factors, leading to the use of fuel additives and fuel system optimizations.

Biofuel systems, hybrid fuel systems, and electric fuel pumps are emerging trends, reflecting the shift towards cleaner energy solutions. Regulatory mandates, consumer demand, and industrial strategies contribute to the unique evolution of fuel delivery systems in each APAC market. Government policies, such as emission standards and fuel subsidies, are encouraging the adoption of cleaner and more efficient fuel systems. The expanding middle class in the region is leading to increased car ownership, further fueling market growth. Biofuel systems and fuel cell technology represent future developments.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Automotive Fuel Delivery System market drivers leading to the rise in the adoption of Industry?

- The significant growth in vehicle production serves as the primary catalyst for market expansion. The market experiences significant growth due to the increasing global vehicle production. As automotive manufacturing volumes rise, the demand for fuel delivery components, including fuel pumps, injectors, rails, and regulators, also increases. These components are essential for the efficient and reliable operation of internal combustion engines and hybrid powertrains. In 2024, global motor vehicle production reached an impressive 92 million units, with China being the leading contributor, producing over 30 million vehicles and accounting for nearly one-third of the global output. Fuel system advancements, such as direct injection and common rail injection, continue to drive market growth.

- Fuel system calibration and fuel management systems ensure optimal engine performance and improved fuel efficiency. Fuel lines and fuel rails require high-quality materials to ensure safety and durability. Fuel quality and fuel additives play a crucial role in maintaining engine performance and longevity. Fuel system safety is a critical concern, with stringent regulations and standards in place to ensure the safety and reliability of fuel delivery systems. The market is a dynamic and growing industry, driven by the increasing global vehicle production and the need for advanced, efficient, and reliable fuel delivery components.

What are the Automotive Fuel Delivery System market trends shaping the Industry?

- The transition towards gasoline direct injection systems is an emerging market trend. This advanced technology offers improved fuel efficiency and reduced emissions, making it a preferred choice for automakers and consumers alike. The market is witnessing significant growth due to the adoption of advanced technologies such as gasoline direct injection (GDI). GDI systems enable fuel to be injected directly into the combustion chamber at high pressure, leading to improved fuel atomization, enhanced combustion efficiency, and reduced emissions. This transition is driven by the need to meet stringent emission regulations while maintaining engine performance and fuel economy. Recent advancements in the market include the introduction of high-pressure fuel injectors. For instance, on December 8, 2023, Stanadyne launched the Goliath 350-bar GDI performance fuel injector at the PRI Show in Indianapolis.

- Biofuel systems are another trend gaining traction in the market. These systems use renewable fuels such as ethanol and biodiesel, reducing reliance on fossil fuels and lowering carbon emissions. Fuel blending, emissions control, and fuel system diagnostics are other key areas of focus. Hybrid fuel systems, such as port fuel injection, are also gaining popularity due to their ability to improve fuel efficiency and reduce emissions. Fuel sensors play a crucial role in monitoring fuel quality and ensuring optimal engine performance. The market is undergoing significant changes, driven by the need for improved fuel efficiency, reduced emissions, and advanced technologies such as GDI and biofuel systems. Companies are investing in research and development to create innovative solutions that meet the evolving needs of the market.

How does Automotive Fuel Delivery System market faces challenges during its growth?

- The transition towards electric vehicles poses a significant challenge to the automotive industry, as this shift necessitates substantial investments in research and development, infrastructure development, and consumer education to ensure a smooth adoption of electric vehicles and foster industry growth. The market is experiencing significant shifts due to the growing adoption of electric vehicles (EVs). Traditional fuel delivery components, including fuel pumps, injectors, pressure regulators, and fuel rails, are becoming less relevant as EVs do not require internal combustion engines.

- These trends aim to improve fuel efficiency, reduce emissions, and enhance vehicle performance. Fuel corrosion remains a concern, necessitating ongoing research and development for corrosion-resistant materials and coatings. In 2024, global electric car sales surpassed 17 million units, representing a 25% increase from the previous year. This growth exceeded the total number of electric cars sold globally in 2020. Fuel system trends include fuel cell technology, diesel direct injection, fuel system optimization, fuel system certification, fuel metering, fuel system testing, fuel delivery timing, high-pressure fuel pumps, and fuel system durability.

Exclusive Customer Landscape

The automotive fuel delivery system market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive fuel delivery system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive fuel delivery system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AISIN Corp. - The company specializes in advanced automotive fuel delivery systems, encompassing components such as fuel injectors, fuel rails, and fuel pressure regulators.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN Corp.

- Astemo Ltd

- BorgWarner Inc.

- Continental AG

- DENSO Corp.

- Eaton Corp. plc

- Infineon Technologies AG

- Landi Renzo Spa

- Magna International Inc.

- Marelli Holdings Co. Ltd.

- Mikuni American Corp.

- Niterra Co. Ltd.

- Phinia Inc

- Rheinmetall AG

- Robert Bosch GmbH

- Stanadyne LLC

- TI Fluid Systems Plc

- UCAL Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Fuel Delivery System Market

- In February 2023, Bosch announced the launch of its latest fuel injection system, the Common Rail Direct Injection System 2.2, which promises improved fuel efficiency and reduced emissions for commercial vehicles (Bosch press release, 2023).

- In July 2024, Magna International and Delphi Technologies joined forces to create a new joint venture, Magna Delphi Powertrain, focusing on advanced fuel delivery systems and electrified powertrains (Magna International press release, 2024).

- In October 2024, the European Union passed new regulations mandating the installation of alternative fuel infrastructure in all new service stations by 2030, significantly expanding the market for automotive fuel delivery systems (European Parliament press release, 2024).

- In January 2025, Continental AG showcased its innovative Fuel Cell System, which integrates hydrogen fuel cells with the vehicle's fuel delivery system, at the Consumer Electronics Show (Continental AG press release, 2025).

Research Analyst Overview

The market is characterized by continuous advancements and evolving dynamics. Fuel system components, such as lines, calibration, rails, and injectors, are subject to ongoing innovation, with direct and common rail injection systems gaining popularity. Fuel system safety and security are paramount, with regulations emphasizing stringent standards. Biofuel systems, fuel pumps, tanks, and emissions control are integrated to optimize fuel efficiency and reduce environmental impact. Fuel sensors, diagnostics, and management systems enable real-time monitoring and adjustment. Hybrid fuel systems, fuel blending, and port injection are essential for vehicle electrification and improved fuel economy.

Fuel system trends include fuel cell technology, diesel direct injection, and optimization techniques. Fuel filters, pressure regulators, and reliability are crucial for maintaining fuel quality and system durability. The market's dynamic nature ensures a constant focus on fuel system innovation and certification. Fuel system advancements, fuel system calibration, fuel management systems, fuel lines, fuel rails, fuel quality, and fuel additives are all essential components of the market, with a focus on safety, efficiency, and performance.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Fuel Delivery System Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

230 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.4% |

|

Market growth 2025-2029 |

USD 26.6 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.9 |

|

Key countries |

China, US, India, Japan, South Korea, Germany, Mexico, Brazil, France, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Fuel Delivery System Market Research and Growth Report?

- CAGR of the Automotive Fuel Delivery System industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive fuel delivery system market growth of industry companies

We can help! Our analysts can customize this automotive fuel delivery system market research report to meet your requirements.

RIA -

RIA -