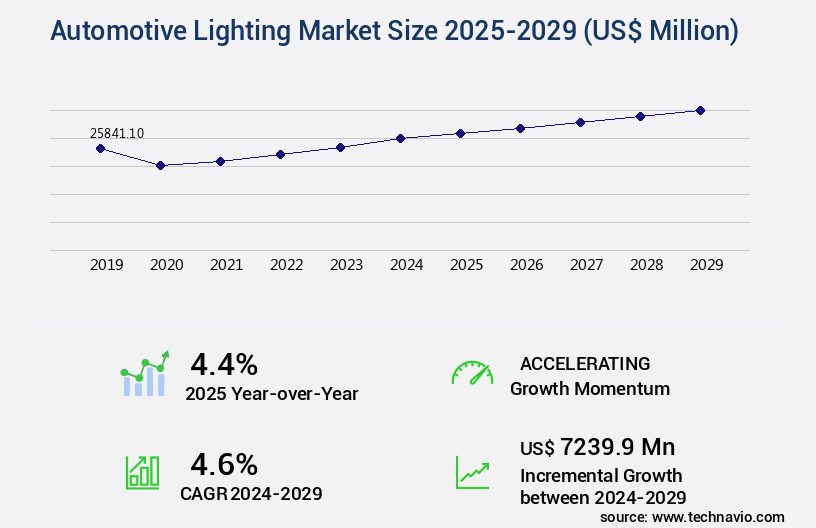

Automotive Lighting Market Size 2025-2029

The automotive lighting market size is valued to increase USD 7.24 billion, at a CAGR of 4.6% from 2024 to 2029. Increasing demand for effective interior lighting will drive the automotive lighting market.

Major Market Trends & Insights

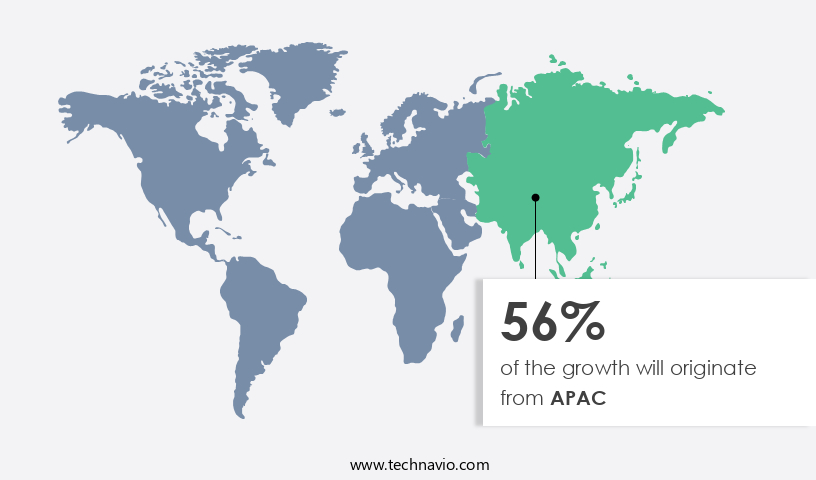

- APAC dominated the market and accounted for a 56% growth during the forecast period.

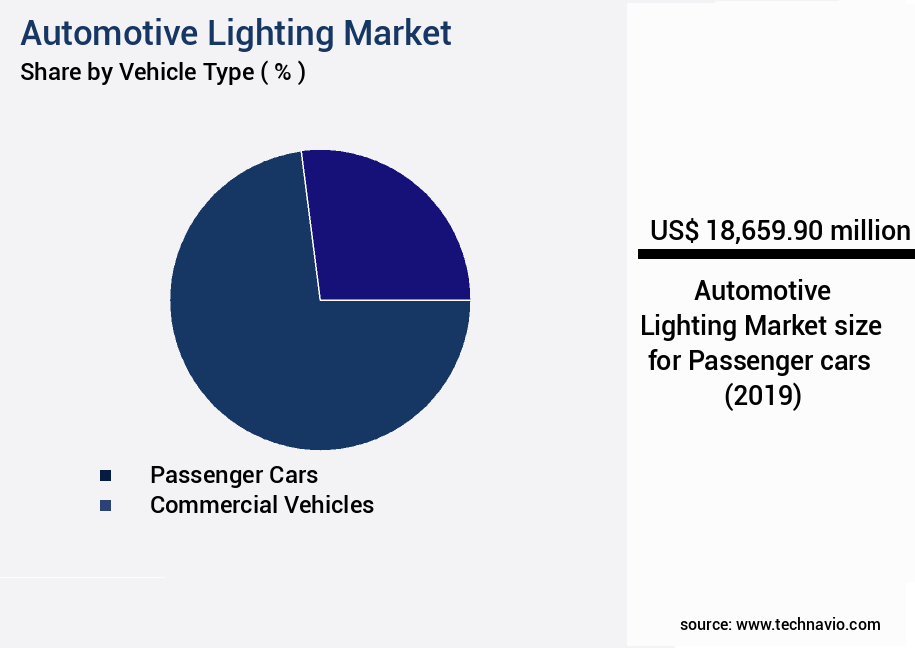

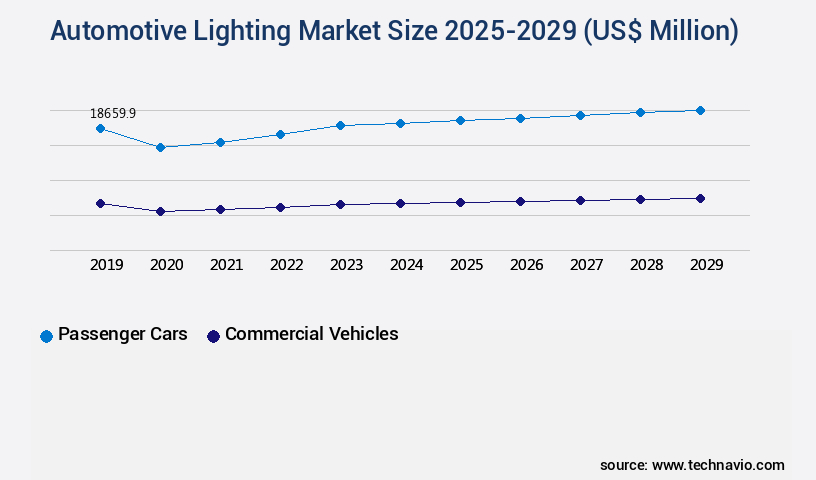

- By Vehicle Type - Passenger cars segment was valued at USD 18.66 billion in 2023

- By End-user - OEM segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 38.14 million

- Market Future Opportunities: USD 7239.90 million

- CAGR : 4.6%

- APAC: Largest market in 2023

Market Summary

- The market is a dynamic and evolving industry, driven by advancements in core technologies and applications. LED lighting, with its energy efficiency and long lifespan, is increasingly dominating the market, holding over 60% of the market share. The development of autonomous vehicles is another significant trend, as advanced lighting systems are essential for safety and functionality in self-driving cars.

- However, the high cost of LED lamps poses a challenge for market growth. In terms of applications, headlights and taillights are the largest product categories, while interior lighting is experiencing increasing demand. Regulations, such as European Union (EU) regulations on lighting systems, continue to shape the market landscape. These trends and challenges underscore the ongoing evolution of the market.

What will be the Size of the Automotive Lighting Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Automotive Lighting Market Segmented and what are the key trends of market segmentation?

The automotive lighting industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Vehicle Type

- Passenger cars

- Commercial vehicles

- End-user

- OEM

- Aftermarket

- Technology

- Halogen

- LED

- Xenon

- Application

- Front

- Rear

- Side and interior

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Vehicle Type Insights

The passenger cars segment is estimated to witness significant growth during the forecast period.

In the automotive industry, both exterior and interior lighting play essential roles in passenger cars. Exterior lighting, driven by advanced technologies such as laser headlight systems, reflector design optimization, and adaptive driving beams, has been a significant growth factor. These innovations offer improved visibility, safety, and enhanced driver experience. Moreover, the increasing adoption of advanced lighting controls, projection lens assemblies, matrix beam technology, and thermal management systems has led to dynamic cornering lights and dynamic headlight systems. Interior lighting, once a luxury feature, is now gaining popularity across various vehicle classes. Suppliers, OEMs, and aftermarket service providers are capitalizing on this trend by introducing energy-efficient LED headlight technology, color temperature control, and luminance uniformity testing.

Micro-LED display technology and OLED lighting systems are also emerging as promising alternatives, offering superior durability and illumination uniformity. Regulations play a crucial role in the market, ensuring safety and compliance with standards such as light distribution patterns, light source lifespan, and glare reduction techniques. As the market continues to evolve, component material selection, light emitting diode, and energy consumption metrics will remain critical factors. The market is expected to grow substantially, with an estimated 20% of the global passenger car production incorporating advanced lighting systems. Furthermore, the integration of driver assistance features and automotive lighting simulation in the design process is projected to accelerate market growth.

Headlamp design parameters, such as light intensity measurement and optical design software, will continue to be essential in this context. In summary, the market is witnessing continuous growth, driven by advancements in exterior and interior lighting technologies, regulatory requirements, and evolving consumer preferences. Companies must stay updated on the latest trends and innovations to remain competitive in this dynamic market.

The Passenger cars segment was valued at USD 18.66 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 56% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Lighting Market Demand is Rising in APAC Request Free Sample

The market in APAC is experiencing steady expansion due to the rising demand for LED lighting systems and the increase in automotive production. This trend is reflected in the significant investments being made by multinational companies, such as BMW Group's recent construction of a high-voltage battery production facility in Thailand, worth over 1.6 billion baht (approximately 43.5 USD million). This expansion marks BMW's entry into electric mobility in the region and is expected to support the production of their first BEV model in Thailand by the second half of 2025.

Additionally, the increasing demand for automobiles in APAC has led to the establishment of new manufacturing plants, underscoring the market's continuous growth. The region's the market is poised for continued expansion, driven by technological advancements and increasing consumer preferences for energy-efficient and advanced lighting systems.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and evolving industry, characterized by continuous advancements in technology and design. One of the significant trends shaping this market is the integration of advanced driver-assistance systems (ADAS), which necessitates innovative lighting solutions. LED technology, with its energy efficiency and long lifespan, is making a substantial impact on automotive lighting design, leading to the development of high-performance lighting systems. Thermal management strategies are crucial for optimizing the performance of high-intensity discharge (HID) lighting systems, ensuring consistent light output and longevity. Testing methods for automotive lighting system durability are rigorous, focusing on extreme temperatures, vibration, and UV resistance to ensure reliable performance.

Advanced optical design software for automotive headlamps enables the optimization of light distribution for improved driver visibility, while regulatory compliance for automotive exterior lighting systems is a critical consideration. Energy efficiency is another essential factor, with innovative lighting solutions focusing on reducing power consumption and carbon footprint. The role of simulation in automotive lighting system development is increasingly significant, allowing for cost-effective manufacturing of high-quality lighting components. Materials science plays a vital role in automotive lighting component design, with sustainable material selection becoming a priority to minimize environmental impact. Future trends in automotive lighting technology advancements include the integration of advanced algorithms for automotive lighting control systems and manufacturing process innovations for improved efficiency and reliability.

A comparative study of different automotive lighting technologies reveals that LED technology holds a significantly larger market share due to its energy efficiency and versatility. In conclusion, the market is a dynamic and innovative industry, driven by technological advancements, regulatory requirements, and consumer preferences. The integration of LED technology, optimization of light distribution, and regulatory compliance are key factors shaping the market's growth. The role of simulation, materials science, and manufacturing process innovations are crucial for driving cost-effective and sustainable solutions.

What are the key market drivers leading to the rise in the adoption of Automotive Lighting Industry?

- The escalating need for efficient and effective interior lighting solutions is the primary market driver.

- Automotive interior lights play a significant role in enhancing the visual appeal of vehicles for customers. These lights, which include dynamic internal lighting and ambient lighting, accentuate the space and create a premium feel in vehicle interiors. For instance, Chevrolet's Camaro 2LT and SS models boast 24 diverse lighting effects, illuminating various areas such as dashboards, door panels, and cup holders. However, excessive cabin lighting can be distracting for drivers. Consequently, manufacturers maintain the luminance value of automotive cabin lighting below a certain threshold.

- This balance between aesthetics and functionality underscores the continuous evolution of the automotive interior lighting market. Manufacturers are increasingly incorporating advanced lighting technologies to offer more customizable and energy-efficient options, catering to diverse customer preferences. This dynamic market landscape reflects the ongoing efforts to create visually appealing and functional vehicle interiors.

What are the market trends shaping the Automotive Lighting Industry?

- The development of autonomous vehicles represents a significant market trend. Autonomous vehicle technology is poised for substantial growth in the near future.

- Prominent automotive companies, including Delphi, Continental, Bosch, Daimler, Scania, and Volvo, are spearheading the expansion of autonomous driving technology in both passenger and commercial vehicles. This market trend has gained significant traction, leading to a substantial increase in the adoption of semi-autonomous features. By the end of the forecast period, self-driving cars are projected to become a reality, with a substantial number of these vehicles expected to be on the road within a decade. These companies have made considerable progress in their research and development of autonomous vehicles. Furthermore, the testing and implementation of advanced driver-assistance systems (ADAS) and telematics/connected vehicle applications and services are estimated to accelerate.

- The market for autonomous driving technology is continually evolving, with ongoing advancements and innovations shaping its future applications across various sectors. This dynamic market landscape underscores the importance of staying informed about the latest trends and developments to maintain a competitive edge.

What challenges does the Automotive Lighting Industry face during its growth?

- The escalating cost of LED lamps poses a significant challenge to the industry's growth trajectory.

- The global lighting market has experienced significant growth in the adoption of LED lamps due to their energy efficiency and advanced features, surpassing those of traditional lighting technologies. LED lamps last approximately 25 times longer than halogen bulbs and three times longer than compact fluorescent lamps (CFL). Despite their advantages, the high upfront cost remains a barrier to their widespread use. The price of LED lamps has decreased, but they still carry a premium compared to other automotive lighting options. Market participants are dedicated to reducing costs while enhancing quality and efficiency. LED lamps' energy efficiency, longevity, and advanced features have driven their widespread adoption in the global lighting market.

- These lamps last significantly longer than traditional lighting technologies, offering substantial cost savings over their lifetimes. However, the initial investment required for LED lamps remains a challenge for some consumers. Companies in the market are continuously innovating to address this issue and make LED lighting more accessible and cost-effective.

Exclusive Customer Landscape

The automotive lighting market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive lighting market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Lighting Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive lighting market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Continental AG - This company specializes in advanced automotive lighting solutions, including Ouster OS1 and ADB technologies. Their offerings enhance vehicle safety and visibility, utilizing cutting-edge optics and innovative design. These lighting systems cater to diverse automotive applications, contributing to improved roadway illumination and overall driving experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Continental AG

- FlexNGate Group of Companies

- General Electric Co.

- Hyundai Motor Group

- Koito Manufacturing Co. Ltd.

- Koninklijke Philips NV

- LG Corp.

- Lumax Industries Ltd

- Marelli Holdings Co. Ltd.

- Namyung Lighting Co. Ltd

- NXP Semiconductors NV

- OSRAM GmbH

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Seoul Semiconductor Co. Ltd.

- Stanley Electric Co. Ltd.

- Stellantis NV

- Suprajit Engineering Ltd.

- Valeo SA

- Varroc Engineering Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Lighting Market

- In January 2024, Magneti Marelli, a leading automotive technology provider, announced the launch of its innovative Adaptive Driving Beam (ADB) system, which optimizes high beam performance by adjusting the beam shape to avoid dazzling other drivers. (Magneti Marelli Press Release)

- In March 2024, Hella, a global lighting technology company, entered into a strategic partnership with LG Chem to develop and produce solid-state lighting solutions for automotive applications. This collaboration aims to improve energy efficiency and enhance the design flexibility of automotive lighting systems. (Hella Press Release)

- In May 2024, Signify, the world leader in lighting, completed the acquisition of Cooper Lighting Solutions, a leading North American provider of commercial, industrial, and residential lighting solutions. This acquisition strengthened Signify's position in the market and expanded its customer base. (Signify Press Release)

- In April 2025, the European Union announced new regulations mandating the use of adaptive driving beam systems in all new passenger cars by 2027. This regulatory approval is expected to boost the demand for advanced automotive lighting technologies and create significant growth opportunities for market players. (European Commission Press Release)

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Lighting Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

240 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2025-2029 |

USD 7239.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.4 |

|

Key countries |

China, US, Japan, Germany, India, France, UK, Italy, South Korea, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is a dynamic and evolving industry, characterized by continuous innovation and advancements in technology. Manufacturing process automation plays a crucial role in producing high-quality lighting components, enabling the mass production of complex systems such as laser headlight systems and exterior lighting modules. Laser headlight systems represent a significant shift from traditional halogen and LED headlights, offering improved brightness and longer range. Reflector design optimization and the use of advanced lighting controls, like adaptive driving beams and dynamic cornering lights, enhance visibility and safety. Projection lens assemblies and matrix beam technology are essential components in modern automotive lighting.

- These technologies allow for precise light distribution patterns and glare reduction techniques, contributing to improved illumination uniformity and light source lifespan. Thermal management systems are vital in maintaining optimal operating temperatures for lighting components, ensuring energy consumption metrics remain efficient. OLED lighting systems and micro-LED display technology are emerging trends, offering potential benefits in terms of energy efficiency and color temperature control. Regulations governing automotive lighting are stringent, requiring adherence to specific standards for light intensity measurement, luminance uniformity testing, and light distribution patterns. Component material selection and light emitting diode technology are essential considerations in designing headlamps that meet these requirements.

- Innovations in automotive lighting extend beyond exterior applications, with interior ambient lighting offering enhanced comfort and aesthetics. Driver assistance features and automotive lighting simulation tools further refine the design process, ensuring optimal headlamp design parameters and optimal performance. Overall, the market is a vibrant and ever-evolving landscape, driven by technological advancements and regulatory requirements. These trends shape the industry's future, with a focus on energy efficiency, durability, and enhanced visibility.

What are the Key Data Covered in this Automotive Lighting Market Research and Growth Report?

-

What is the expected growth of the Automotive Lighting Market between 2025 and 2029?

-

USD 7.24 billion, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report segmented by Vehicle Type (Passenger cars and Commercial vehicles), End-user (OEM and Aftermarket), Technology (Halogen, LED, and Xenon), Application (Front, Rear, and Side and interior), and Geography (APAC, Europe, North America, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for effective interior lighting, High cost of LED lamps

-

-

Who are the major players in the Automotive Lighting Market?

-

Key Companies Continental AG, FlexNGate Group of Companies, General Electric Co., Hyundai Motor Group, Koito Manufacturing Co. Ltd., Koninklijke Philips NV, LG Corp., Lumax Industries Ltd, Marelli Holdings Co. Ltd., Namyung Lighting Co. Ltd, NXP Semiconductors NV, OSRAM GmbH, Robert Bosch GmbH, Samsung Electronics Co. Ltd., Seoul Semiconductor Co. Ltd., Stanley Electric Co. Ltd., Stellantis NV, Suprajit Engineering Ltd., Valeo SA, and Varroc Engineering Ltd.

-

Market Research Insights

- The market encompasses a diverse range of technologies and applications, from reflective surface coatings and energy efficient lighting to advanced safety features such as driver fatigue reduction and pedestrian safety lighting. According to industry estimates, the market for automotive lighting is projected to reach USD35 billion by 2025, growing at a compound annual growth rate of 7% between 2020 and 2025. One key trend driving market growth is the increasing demand for energy efficient lighting solutions, with daytime running lights and LED module integration becoming increasingly common. In contrast, traditional halogen headlamps accounted for over 50% of the market share in 2020, highlighting the market's ongoing transition towards more advanced technologies.

- Manufacturers are also focusing on improving material durability through light scattering analysis and material testing, as well as optimizing manufacturing costs through supply chain management and smart lighting systems. Additionally, safety features such as automotive lighting safety, fog lamp performance, and night vision enhancement continue to gain importance, with turn signal visibility and color rendering index playing crucial roles in ensuring effective communication and enhancing visual acuity for drivers. Other emerging technologies include light pipe technology, smart lighting systems, and optical fiber technology, which offer improved brightness uniformity, signal processing algorithms, and environmental impact assessment, respectively.

- As the market continues to evolve, manufacturers will need to balance the demands of cost optimization, safety, and innovation to meet the evolving needs of consumers and regulatory bodies.

We can help! Our analysts can customize this automotive lighting market research report to meet your requirements.

RIA -

RIA -