Automotive Rear Seat Infotainment Market Size 2025-2029

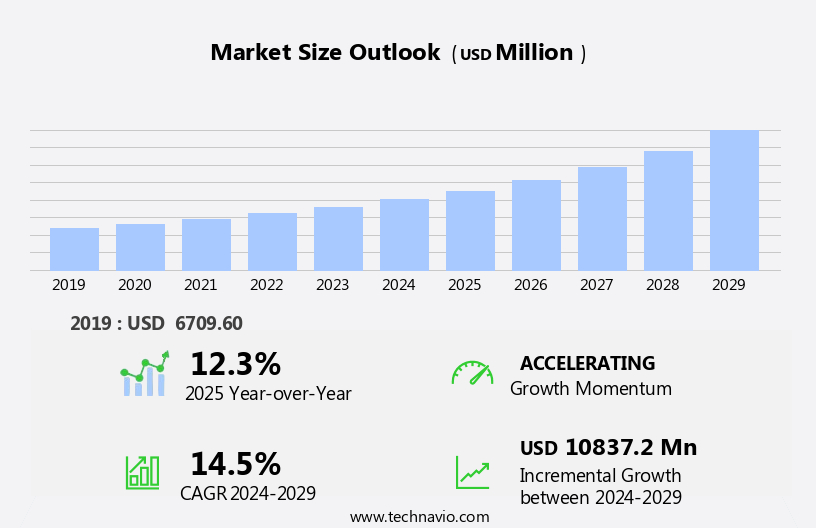

The automotive rear seat infotainment market size is forecast to increase by USD 10.84 billion, at a CAGR of 14.5% between 2024 and 2029.

- The market is experiencing significant growth due to the increasing consumer preference for enhanced in-car entertainment. This trend is driven by the desire for a more comfortable and engaging travel experience, particularly for long journeys. Another key driver is the adoption of AI-powered rear seat infotainment systems, which offer personalized entertainment and convenience features for passengers. However, the high initial costs of advanced infotainment systems present a significant challenge for market growth. Manufacturers must find ways to reduce costs while maintaining quality and functionality to make these systems accessible to a wider consumer base.

- To capitalize on this market opportunity, companies should focus on developing cost-effective solutions that offer superior entertainment and convenience features, while also addressing the challenge of high initial costs through financing options or partnerships with automakers. Effective strategic planning and operational efficiency will be essential for companies seeking to navigate this dynamic market landscape.

What will be the Size of the Automotive Rear Seat Infotainment Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, with innovations in technology and consumer preferences shaping its dynamics. Touchscreen controls and customizable settings offer passengers a personalized experience, while gaming consoles and parental controls cater to family needs. USB charging ports and speaker systems ensure comfort, with subwoofer integration and internet connectivity enhancing the passenger experience. Over-the-air updates maintain software compatibility, and sound quality is a priority through headrest monitors, OEM integration, and streaming video content. Privacy protection and data security are crucial considerations, with real-time traffic information and navigation systems ensuring seamless connectivity. Bluetooth connectivity and streaming services compatibility enable a convenient and entertaining journey.

Installation complexity varies, making aftermarket compatibility and audio system integration essential for fleet vehicles. Child safety features and family vehicles prioritize passenger well-being, with wireless streaming, audio amplifiers, HDMI ports, and software updates enhancing the overall experience. The market's continuous unfolding is marked by advancements in user interface design, multimedia playback, voice control, and integration with various vehicle models and systems.

How is this Automotive Rear Seat Infotainment Industry segmented?

The automotive rear seat infotainment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Aftermarket

- OEM

- Technology

- Multimedia player

- Navigation systems

- Type

- Overhead system

- Headrest monitor system

- Plug and play system

- OS

- QNX

- Linux

- Microsoft

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

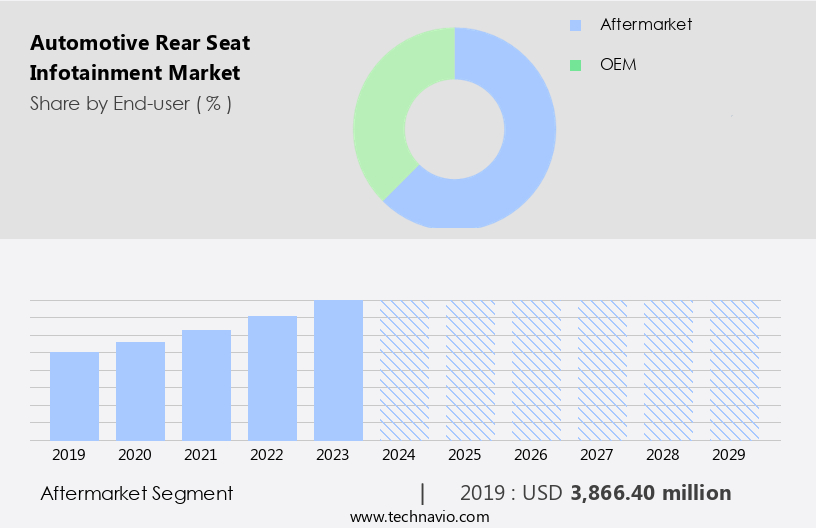

The aftermarket segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth, driven by the increasing demand for enhanced passenger experience and comfort. Touchscreen controls, customizable settings, and gaming consoles are becoming increasingly popular features in rear seat infotainment systems. Parental controls, USB charging ports, and speaker systems are other essential components that cater to the needs of families and fleet vehicles. OEM integration, streaming video content, and smartphone mirroring are key trends in the market, providing seamless connectivity and multimedia playback. Internet connectivity, over-the-air updates, and real-time traffic information enable users to stay connected and informed. Luxury vehicles often feature high-end speaker systems, subwoofer integration, and headrest monitors for an immersive and harmonious passenger experience.

The aftermarket segment dominates the market due to its flexibility and affordability. Popular aftermarket players, such as Pioneer and Alpine, offer a wide range of rear seat infotainment solutions. However, the increasing penetration of OEM-fitted rear seat infotainment systems may impact the aftermarket segment's growth. Navigation systems, data security, and voice control are essential features that ensure user convenience and privacy protection. Integrated screens, Bluetooth connectivity, and software updates are necessary for seamless system integration. Apple CarPlay and Android Auto are popular solutions for wireless streaming and intuitive navigation. The market's evolution includes advancements such as HDMI ports, audio amplifiers, and sound insulation for superior sound quality.

Fleet vehicles and family vehicles require additional features like child safety and wireless streaming capabilities. In conclusion, the market is witnessing continuous growth due to the increasing demand for enhanced passenger experience and comfort. The market's dynamics include trends such as OEM integration, streaming video content, and smartphone mirroring, as well as the dominance of the aftermarket segment and the importance of features like navigation systems, data security, and voice control.

The Aftermarket segment was valued at USD 3.87 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

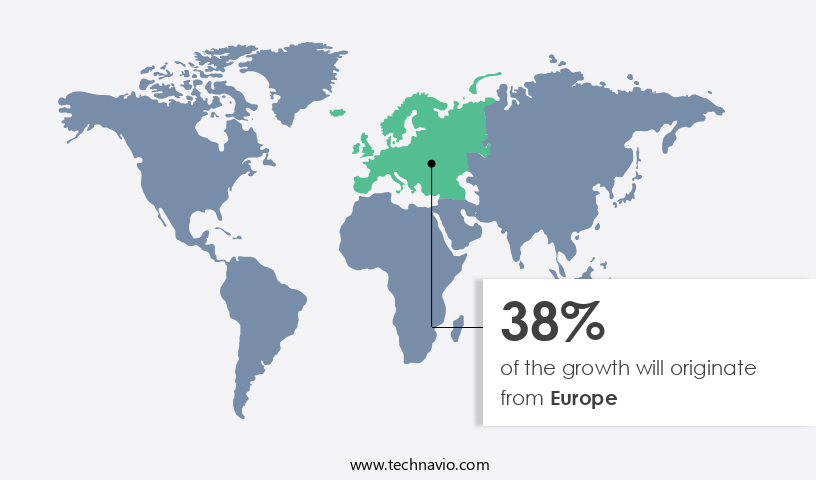

Europe is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the evolving automotive landscape, the rear seat infotainment market is gaining significant traction. This market is marked by advanced features such as touchscreen controls, customizable settings, gaming consoles, parental controls, USB charging ports, speaker systems, and more. Europe, specifically countries like Germany, France, Italy, Spain, and the UK, are major contributors to this market due to the increasing popularity of luxury vehicles. OEMs like Audi, BMW, and Mercedes-Benz, based in these regions, integrate high-end infotainment systems in their luxury cars. Rear seat infotainment enhances passenger experience, offering comfort and entertainment during long journeys. Technological innovations, including internet connectivity, over-the-air updates, real-time traffic information, streaming video content, smartphone mirroring, and voice control, are driving the market's growth.

Furthermore, integration of advanced features like subwoofer integration, privacy protection, and wireless streaming adds to the market's dynamism. Fleet vehicles and family cars also benefit from these advanced infotainment systems, catering to diverse consumer needs. Installation complexity is a factor, but the market offers solutions for aftermarket compatibility and audio system integration. Data security and navigation systems are essential considerations, ensuring a seamless and enjoyable user experience.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Automotive Rear Seat Infotainment Industry?

- The surge in consumer preference for advanced in-car entertainment systems serves as the primary market catalyst.

- The market is experiencing substantial growth due to increasing consumer demand for enhanced in-car entertainment experiences. Passengers seek more engaging and entertaining trips, leading automakers to prioritize the integration of advanced rear seat infotainment systems. These systems offer various functions, such as multimedia streaming, gaming, internet access, and interactive displays, to enhance the overall passenger experience. The market's expansion is further fueled by the rising trend of smart and connected vehicles. To cater to the growing need for immersive and interactive in-car entertainment options, the market is expected to grow rapidly.

- Headrest monitors, OEM integration, streaming video content, smartphone mirroring, video game integration, 4G LTE, GPS navigation, Wi-Fi hotspot, and user interface design are some essential features of these advanced systems. The market's growth is driven by the integration of these technologies, providing passengers with a multimedia playback experience that is both harmonious and immersive.

What are the market trends shaping the Automotive Rear Seat Infotainment Industry?

- The increasing prevalence of artificial intelligence (AI) in rear seat infotainment systems represents a significant market trend. This technological advancement enhances the in-vehicle experience for passengers by providing them with advanced features and functionalities.

- The market is experiencing significant growth due to the integration of advanced technologies that cater to passenger comfort and entertainment. One of the key trends is the adoption of voice control, allowing passengers to access various features without taking their hands off the wheel or looking away from the road. Additionally, privacy protection measures are being implemented to secure personal data and ensure confidentiality. Integrated screens are becoming standard in modern vehicles, providing access to real-time traffic information, streaming services compatibility, and navigation systems. Bluetooth connectivity enables seamless connectivity to personal devices, while data security features protect sensitive information.

- Fleet vehicles and family vehicles are major segments of the market, as they prioritize passenger comfort and entertainment during long trips. Child safety features are also essential considerations for family vehicles, ensuring the well-being of young passengers. Installation complexity is a factor in the market, with some systems requiring professional installation and others offering plug-and-play convenience. As technology continues to evolve, the market is poised to offer more immersive and harmonious experiences for all passengers.

What challenges does the Automotive Rear Seat Infotainment Industry face during its growth?

- The high initial costs associated with implementing advanced infotainment systems represent a significant challenge to the industry's growth trajectory.

- The market presents significant opportunities for growth, driven by consumer demand for advanced in-car entertainment and connectivity solutions. Wireless streaming capabilities, such as Bluetooth and Wi-Fi, enable passengers to access their favorite media content without the need for physical connections. HDMI ports offer high-definition video output for enhanced visual experience, while software updates ensure the systems remain current with the latest features. Aftermarket compatibility and audio system integration are essential considerations for consumers seeking to retrofit their vehicles with advanced infotainment systems.

- Sound insulation and noise reduction technologies contribute to a more harmonious and immersive in-car environment. Apple CarPlay and Android Auto enable seamless smartphone integration, offering intuitive navigation and hands-free control. Despite the high initial costs, the market is expected to grow as these advanced features become increasingly important to consumers.

Exclusive Customer Landscape

The automotive rear seat infotainment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive rear seat infotainment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive rear seat infotainment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AISIN Corp. - This company specializes in advanced automotive rear seat infotainment systems. Our offerings include cutting-edge technologies such as ultrasonic parking sensors and cameras. These features enhance the driving experience by providing real-time information for improved safety and convenience. By integrating these solutions seamlessly into the vehicle, we cater to the growing demand for connected and technologically advanced in-car experiences.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN Corp.

- Alps Alpine Co. Ltd.

- Aptiv Plc

- Continental AG

- DENSO Corp.

- Forvia SE

- Garmin Ltd.

- Hyundai Motor Co.

- JVCKENWOOD Corp.

- LG Corp.

- Mitsubishi Electric Corp.

- Panasonic Holdings Corp.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Sony Group Corp.

- TomTom NV

- Valeo SA

- Visteon Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Rear Seat Infotainment Market

- In March 2023, Mercedes-Benz unveiled its latest innovation, the MBUX Hyperscreen, an expansive infotainment system for the rear seats of its E-Class sedan. This 56-inch curved display integrates multiple functions, including navigation, media, climate control, and communication (Mercedes-Benz press release, 2023).

- In August 2024, Apple and BMW announced a strategic partnership to bring Apple CarPlay integration to the rear seat infotainment systems of select BMW models. This collaboration allows rear-seat passengers to access Apple Music, Apple Maps, and other Apple services directly from the BMW iDrive system (BMW Group press release, 2024).

- In January 2025, Panasonic Corporation and Tesla Motors announced a significant investment of USD1.6 billion in Panasonic's automotive battery plant in Nevada. This collaboration aims to support the production of batteries for Tesla's electric vehicles and the development of advanced infotainment systems for Tesla's rear seats (Reuters, 2025).

- In May 2025, Ford Motor Company received approval from the National Highway Traffic Safety Administration for its SYNC 4 infotainment system, which features an upgraded rear seat entertainment system with 15-inch touchscreens and improved connectivity options (Ford press release, 2025).

Research Analyst Overview

- The market is witnessing significant advancements, with ADAS integration becoming a key trend. Facial recognition and voice recognition software enhance user experience, while machine learning and predictive analytics offer personalized content. Virtual reality and augmented reality technologies provide immersive experiences, and haptic feedback adds tactile sensation. Touchscreen sensitivity and high screen resolution improve interface customization. Audio-video receivers, digital media players, and subscription services deliver diverse content, while wireless charging and long battery life ensure uninterrupted use. Content delivery networks and cloud storage facilitate access to vast media libraries.

- Biometric authentication and driver monitoring systems ensure security and convenience. Accessibility features cater to diverse user needs. AI and remote control capabilities offer advanced functionality. Multi-zone audio and surround sound systems cater to passengers' entertainment preferences. Wireless connectivity and data usage monitoring maintain efficiency and cost-effectiveness.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Rear Seat Infotainment Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

250 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.5% |

|

Market growth 2025-2029 |

USD 10837.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

12.3 |

|

Key countries |

US, Germany, Canada, China, UK, France, India, Japan, Italy, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Rear Seat Infotainment Market Research and Growth Report?

- CAGR of the Automotive Rear Seat Infotainment industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, APAC, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive rear seat infotainment market growth of industry companies

We can help! Our analysts can customize this automotive rear seat infotainment market research report to meet your requirements.

RIA -

RIA -