Autonomous Crop Management Market Size 2024-2028

The autonomous crop management market size is forecast to increase by USD 5.76 billion at a CAGR of 10.45% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing focus on productivity and efficiency in the agriculture sector. The integration of Artificial Intelligence (AI) and Machine Learning (ML) technologies into autonomous crop management systems is driving this trend, enabling farmers to optimize crop yields and reduce operational costs. However, the high initial investment required for implementing these advanced technologies poses a significant challenge for many farmers and agricultural businesses. Despite this hurdle, the market's potential for innovation and improved agricultural outcomes is substantial. Companies seeking to capitalize on this opportunity should focus on developing cost-effective solutions that cater to the unique needs of various farming sectors and geographies.

- Additionally, collaborations and partnerships with technology providers, agricultural institutions, and government organizations can help facilitate the adoption of autonomous crop management systems and mitigate the initial investment barrier. Overall, the market represents an exciting and dynamic landscape for businesses and investors alike, offering significant opportunities for innovation and growth in the agriculture sector.

What will be the Size of the Autonomous Crop Management Market during the forecast period?

- The market continues to evolve, driven by advancements in technology and the growing demand for sustainable agriculture. Farmers are increasingly adopting solutions that leverage artificial intelligence, machine learning, and computer vision to optimize crop yield, improve harvest efficiency, and enhance farm management. Precision spraying and fertilizer management systems enable farmers to apply inputs more effectively, reducing waste and increasing profitability. autonomous vehicles and automated irrigation systems streamline farm operations, while soil health monitoring and variable rate application help improve crop production and reduce environmental impact. Farm management software and digital farming solutions offer real-time data integration, data visualization, and data-driven decision making, allowing farmers to optimize their operations and respond to changing conditions.

- Drones and satellite imagery provide valuable insights into crop health and growth patterns, enabling farmers to make informed decisions and improve overall farm efficiency. The market for agricultural innovation is diverse, with a range of entities focusing on yield optimization, water conservation, and labor reduction. Smart sensors and GPS guidance systems enable farmers to monitor and manage their fields more effectively, while weather forecasting and disease management solutions help mitigate risks and protect crops. As the market for autonomous crop management continues to unfold, new applications and integrations are emerging. data security and data integration are becoming increasingly important, as farmers seek to protect their valuable agricultural data and leverage it to improve their operations.

- The integration of carbon sequestration and sustainable agriculture solutions is also gaining momentum, as farmers seek to reduce their environmental footprint and enhance the long-term sustainability of their operations.

How is this Autonomous Crop Management Industry segmented?

The autonomous crop management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Component

- Hardware

- Software

- Services

- Deployment

- On-premises

- Cloud-based

- Technology

- IoT-Based Systems

- AI and Machine Learning

- Robotics

- Application

- Precision Irrigation

- Weed Control

- Harvesting

- Crop Type

- Cereals

- Fruits and Vegetables

- Oilseeds

- Farm Size

- Large Farms

- Small and Medium Farms

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

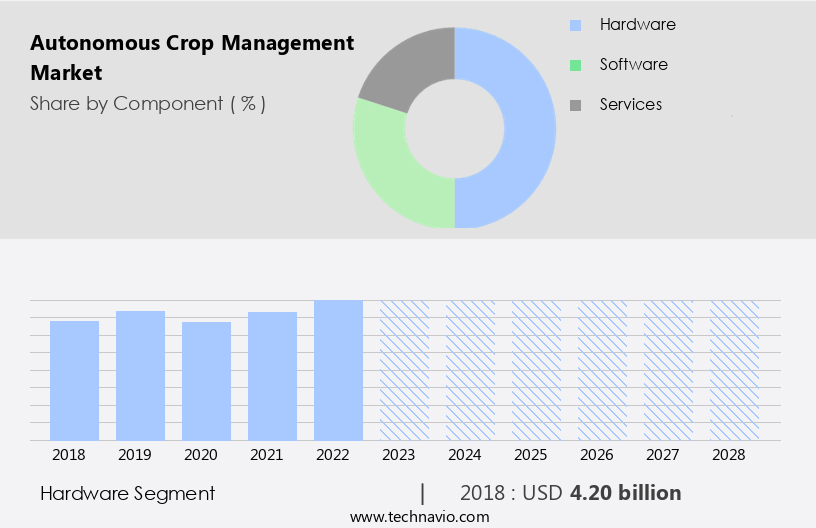

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

Autonomous crop management is revolutionizing agriculture through advanced technologies such as yield forecasting, carbon sequestration, and precision farming solutions. Agtech startups leverage satellite imagery and agricultural data to develop crop modeling and Farm Equipment automation, enhancing crop production and optimizing farm profitability. Farmers utilize machine learning, automated irrigation, and precision spraying to implement data-driven decision making, while smart sensors monitor agronomic practices and soil health. Autonomous vehicles and drones enable remote sensing and weather forecasting, reducing labor requirements and optimizing operational cost savings. Computer vision and digital farming facilitate sustainable agriculture through variable rate application, disease management, and pest control.

Farm management software and data visualization tools streamline farm operations and improve farm efficiency. The integration of data security and water conservation technologies ensures the protection of valuable agricultural data and the efficient use of water resources. Overall, the adoption of these innovative technologies propels The market, enhancing crop yield increase, harvest optimization, and fertilizer management.

The Hardware segment was valued at USD 4.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

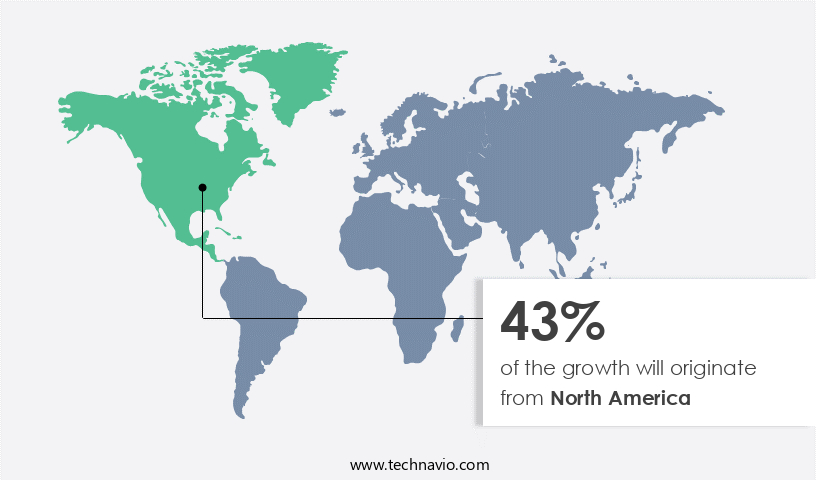

North America is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is currently leading the global landscape, driven by advanced agricultural technologies, government initiatives, and the rising demand for food production. Cloud-based technology and smart farming techniques are increasingly adopted to boost productivity and efficiency. The National Institute of Food and Agriculture (NIFA), a part of the USDA, promotes geospatial, sensor, and precision technology projects to support farmers. Additionally, the use of artificial intelligence, machine learning, and computer vision in digital farming is gaining traction. Autonomous vehicles, automated irrigation, and precision spraying are transforming farm operations, while variable rate application, soil health monitoring, and fertilizer management optimize crop yield.

Farm management software, data visualization, and data-driven decision making are essential tools for farmers to optimize their farm operations. Data integration and security are crucial aspects of the market, ensuring sustainable agriculture practices. Water conservation, agricultural inputs, and weather forecasting are other key factors contributing to the market's growth. The market's evolution is further fueled by the integration of drone technology, satellite imagery, and precision agriculture solutions. Labor reduction, remote sensing, and pest control are additional benefits that farmers derive from autonomous crop management systems. Overall, the market's future looks promising, with a focus on farm profitability, crop production, and operational cost savings.

Market Dynamics

The Autonomous Crop Management Market is transforming agriculture with AI-driven crop health diagnostics, autonomous weeding robots, and drone-based crop spraying for sustainable farming. Smart irrigation systems and weather-adaptive robots optimize resources, while carbon-neutral farming solutions and eco-friendly automation support organic farming. Blockchain-verified crop data ensures traceability, and low-cost autonomous tractors empower emerging markets. Hyperspectral imaging, real-time yield forecasting, and predictive pest control enhance efficiency for large-scale farms and greenhouse operations. Modular robotic systems with multi-crop robotic compatibility and sustainable sensor networks drive precision agriculture. Digital advisory services and autonomous crop phenotyping benefit research institutes, positioning best autonomous crop management systems for 2025 as leaders in high-yield autonomous farming equipment for cooperatives.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Autonomous Crop Management Industry?

- The agriculture sector's relentless drive towards enhancing productivity and efficiency serves as the primary catalyst for market growth.

- Autonomous crop management is revolutionizing farm operations management by performing tasks with minimal labor, leading to increased productivity and efficiency. This innovation enables farmers to focus on other essential duties and improve their overall business efficiency. The integration of remote sensing, weather forecasting, and precision agriculture technologies in autonomous crop management systems allows for real-time monitoring and analysis of agronomy data, pest control, and field operations. By deploying multiple self-driving vehicles, farmers can benefit from operational cost savings through economies of scale. Agricultural mechanization, including autonomous crop management, is a critical aspect of modernizing agriculture. The efficient utilization of farm implements directly impacts farm productivity.

- Autonomous crop management systems utilize advanced technologies such as field data analytics to optimize crop yields and reduce the need for human intervention in various farming tasks. These systems also facilitate disease management and pest control, ensuring optimal crop health and reducing the reliance on manual labor. In conclusion, the adoption of autonomous crop management is a significant step towards enhancing farm operations and improving overall business performance.

What are the market trends shaping the Autonomous Crop Management Industry?

- The integration of Artificial Intelligence (AI) and Machine Learning (ML) technologies is becoming increasingly essential in the field of autonomous crop management. This trend reflects the growing recognition of the potential benefits these technologies offer in optimizing agricultural processes and improving crop yields.

- Artificial intelligence (AI) and machine learning (ML) are transforming the market by providing advanced capabilities for data collection, processing, and analysis. These technologies enable more precise and effective pest management through real-time interpretation of complex scenarios. In addition, AI and ML can optimize resource usage, maximize crop yields, and analyze soil data. Furthermore, they automate farm management, optimize workflow, and offer valuable insights into animal health and species management. The integration of these technologies is essential for the efficient operation of autonomous tractors and other farm equipment. With the increasing emphasis on agricultural innovation, yield forecasting, carbon sequestration, and precision planting, the use of AI and ML in autonomous crop management is becoming increasingly important for farm profitability and sustainable crop production.

- Smart sensors and satellite imagery are also key components of autonomous crop management systems, providing real-time data on crop growth and health. Overall, the integration of AI, ML, and other agtech solutions is driving the future of agricultural innovation.

What challenges does the Autonomous Crop Management Industry face during its growth?

- The high initial investment required for autonomous crop management represents a significant challenge to the industry's growth trajectory. Incorporating advanced technologies such as drones, sensors, and machine learning algorithms into farming operations comes with a substantial upfront cost, potentially hindering the expansion and profitability of agricultural businesses.

- Autonomous crop management is gaining traction globally due to its potential to increase crop yield and optimize harvest through advanced technologies. However, the high cost of investment is a significant barrier for farmers, particularly in adopting precision spraying, fertilizer management, automated irrigation, and machine learning-driven farm management software. These tools, while offering benefits such as variable rate application, soil health monitoring, computer vision, and digital farming, come with substantial expenses for software integration, data analytics tools, and training.

- Consequently, many farmers are hesitant to transition from traditional farming methods due to the financial burden. The cost of these technologies can differ among companies, making it essential for farmers to carefully consider their options before investing.

Exclusive Customer Landscape

The autonomous crop management market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the autonomous crop management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, autonomous crop management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGCO Corp. - The company delivers advanced crop management solutions through the integration of digital technologies, including the Internet of Things, big data analytics, and industry expertise.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGCO Corp.

- AgJunction Inc.

- BASF SE

- Bayer AG

- CNH Industrial NV

- CropX Inc.

- Deere & Company

- DJI

- Farm-ng

- Kubota Corp.

- Monsanto Co.

- Naio Technologies

- PrecisionHawk Inc.

- Raven Industries Inc.

- Syngenta AG

- TeeJet Technologies

- Topcon Corp.

- Trimble Inc.

- XAG Co. Ltd.

- Yanmar Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Autonomous Crop Management Market

- In February 2024, John Deere, a leading agriculture machinery manufacturer, introduced its new Autonomous Tractor System, marking a significant leap in autonomous crop management technology (John Deere press release). This system, which utilizes GPS guidance and machine learning algorithms, enables tractors to operate without human intervention, reducing labor costs and increasing efficiency.

- In May 2025, Microsoft and Trimble, a technology provider for agriculture, announced a strategic partnership to integrate Microsoft's Azure IoT and AI capabilities with Trimble's AgSense platform (Microsoft News Center). This collaboration aims to provide farmers with real-time insights and predictive analytics, enhancing crop management and yield optimization.

- In August 2024, Bosch and PrecisionHawk, a drone technology company, announced a strategic partnership to offer integrated drone solutions for precision agriculture (Bosch press release). This collaboration combines Bosch's sensor technology with PrecisionHawk's Drone Services, providing farmers with high-resolution imagery and data analysis for crop health monitoring and management.

- In November 2024, the European Union approved the use of fully autonomous tractors in agricultural operations, marking a major regulatory milestone for the market (European Commission press release). This approval is expected to accelerate the adoption of autonomous technology in European agriculture, driving market growth.

Research Analyst Overview

The market is experiencing significant growth, driven by the integration of precision agriculture technologies and data-driven agronomy. Farmers are increasingly adopting solutions like precision tillage, inventory management, and automated harvesting to optimize crop yields and reduce operational costs. smart agriculture practices, including pest identification, harvest timing, and soil moisture monitoring, are also gaining popularity. Autonomous tractors, agricultural robotics, and drones are revolutionizing farm consulting, enabling data-driven agriculture and sustainable farming practices. Precision irrigation, field mapping, and anagricultural technology trends, such as agronomic modeling and automated spraying, are essential components of this transformation. Indoor agriculture and vertical farming are emerging trends, offering opportunities for year-round production and climate change mitigation.

Disease diagnosis, plant health analysis, and animal health monitoring are critical aspects of precision livestock management. Supply chain optimization is another area of focus, with farmers leveraging technology to streamline operations and improve farm sustainability. The future of farming lies in the integration of these advanced technologies and the adoption of sustainable farming practices.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Autonomous Crop Management Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

178 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.45% |

|

Market growth 2024-2028 |

USD 5.76 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.95 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Autonomous Crop Management Market Research and Growth Report?

- CAGR of the Autonomous Crop Management industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the autonomous crop management market growth of industry companies

We can help! Our analysts can customize this autonomous crop management market research report to meet your requirements.

RIA -

RIA -