Backup-as-a-service Market Size 2026-2030

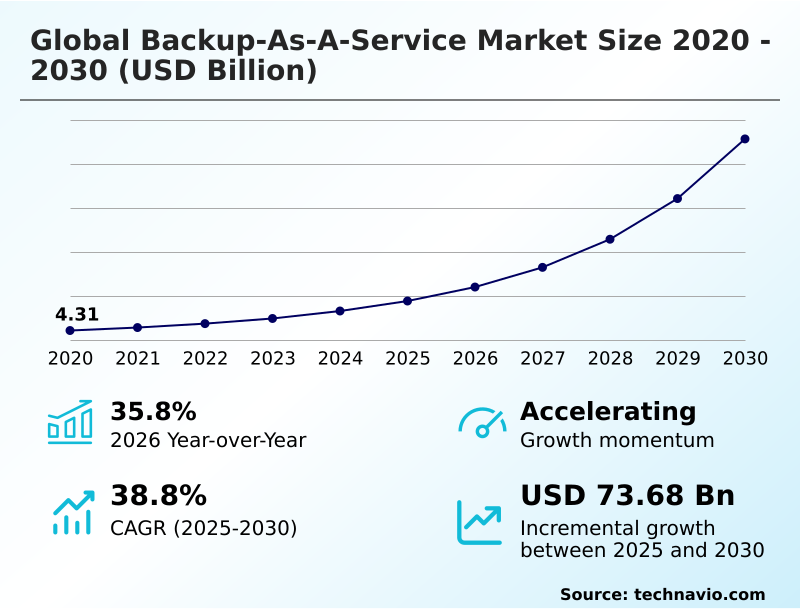

The backup-as-a-service market size is valued to increase by USD 73.68 billion, at a CAGR of 38.8% from 2025 to 2030. Rising cybersecurity threats and sophisticated ransomware campaigns will drive the backup-as-a-service market.

Major Market Trends & Insights

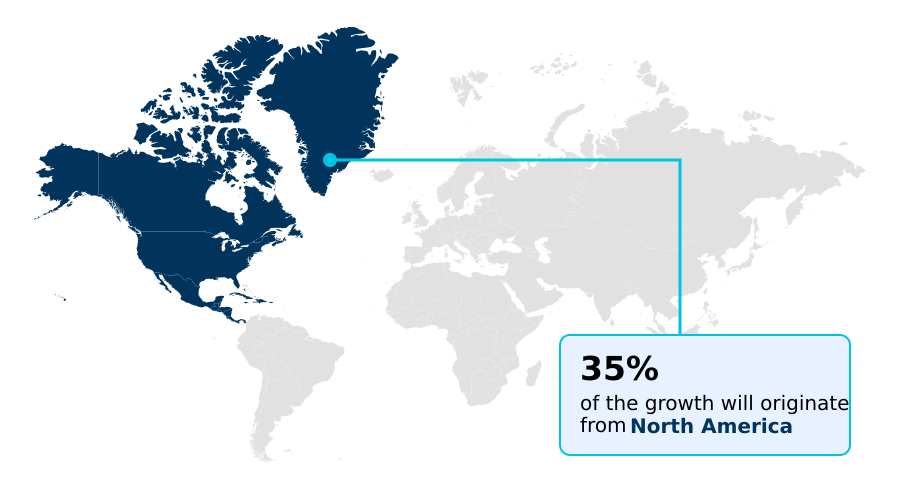

- North America dominated the market and accounted for a 35.1% growth during the forecast period.

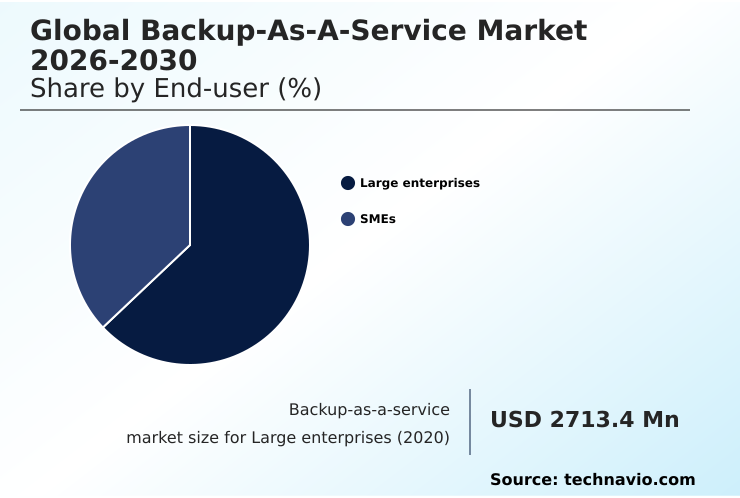

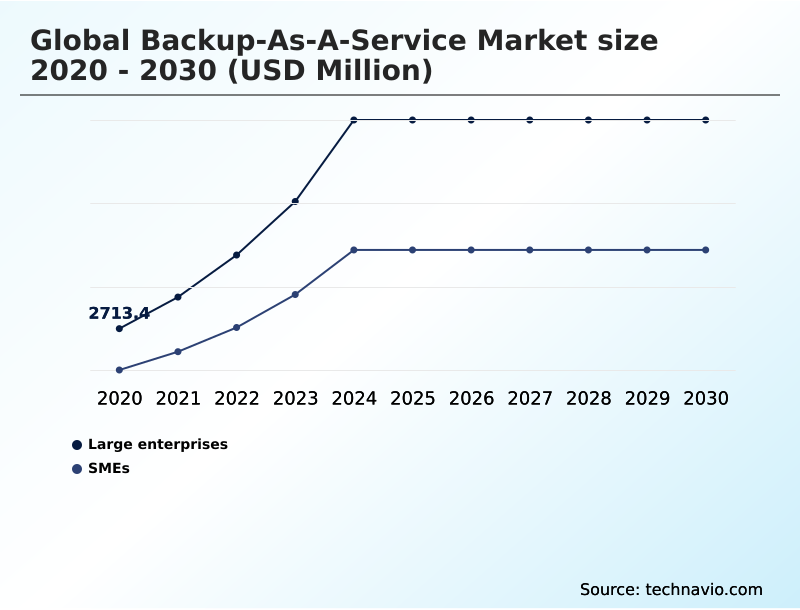

- By End-user - Large enterprises segment was valued at USD 8.34 billion in 2024

- By Application - Online backup segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 87.09 billion

- Market Future Opportunities: USD 73.68 billion

- CAGR from 2025 to 2030 : 38.8%

Market Summary

- The backup-as-a-service market is fundamentally shaped by the escalating need for cyber resilience in an era of digital persistence. Beyond simple data storage, modern solutions provide a critical defense layer, incorporating features like immutable storage, air-gapped backups, and automated recovery testing to counter sophisticated ransomware campaigns that target backup repositories.

- A key trend is the integration of AI-driven anomaly detection analytics, which allows for proactive threat identification. This shift from passive backup to active defense is crucial for business continuity.

- For instance, a healthcare organization leverages a sovereign-aware platform to ensure patient data is not only backed up but also complies with localized data residency mandates, enabling full recovery within minutes of a detected breach.

- This focus on rapid, reliable cyber recovery, combined with the financial agility of operational expenditure (OpEx) models and the necessity of centralized backup management for complex hybrid infrastructures, defines the industry's trajectory. Enterprises now demand a unified data protection platform that ensures enterprise data resiliency across all workloads, from cloud-native applications to on-premises systems.

What will be the Size of the Backup-as-a-service Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Backup-as-a-service Market Segmented?

The backup-as-a-service industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Large enterprises

- SMEs

- Application

- Online backup

- Cloud backup

- Deployment

- Public cloud

- Hybrid cloud

- Private cloud

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- UK

- Germany

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By End-user Insights

The large enterprises segment is estimated to witness significant growth during the forecast period.

Large enterprises require robust data management strategies to ensure business continuity across complex, petabyte-scale environments.

The transition to a consumption-based data protection model is driven by the need for a resilient data fabric that can handle thousands of virtual machines and massive datasets across multiple clouds.

These organizations prioritize disaster recovery as a service (DRaaS) and comprehensive workload protection to safeguard against threats.

Advanced data lifecycle management and business continuity assurance are critical, with many achieving a reduction in recovery times of over 30% by implementing automated and unified data management solutions.

This focus on security, availability, and enterprise data resiliency is essential for managing data sovereignty and privacy challenges in global operations.

The Large enterprises segment was valued at USD 8.34 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Backup-as-a-service Market Demand is Rising in North America Get Free Sample

The global backup-as-a-service market exhibits distinct regional dynamics, with North America emphasizing mature cyber recovery capabilities while APAC focuses on scalable cloud workload protection to support rapid digitalization.

In Europe, strict data sovereignty compliance is paramount, with adoption of sovereign-aware platforms being 50% higher than in other regions. This has fueled demand for localized data residency and policy-driven data protection.

Enterprises are increasingly implementing air-gapped backups and low-latency data replication to secure data across borders. The strategic use of a cyber-resilient architecture allows businesses in regulated markets to reduce compliance-related risks by over 40%.

The market's geographic evolution is driven by these regional priorities, shaping demand for tailored data protection for containers and forensic data analysis capabilities.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the backup-as-a-service market requires careful evaluation of diverse offerings tailored to specific organizational needs. The decision between backup-as-a-service for smes vs large enterprises often hinges on scalability and the complexity of management. While smaller businesses prioritize ease of use, larger organizations focus on managing multi-cloud backup-as-a-service complexity and ensuring robust disaster recovery orchestration with backup-as-a-service.

- The cost of backup-as-a-service for saas applications, particularly for securing office 365 with backup-as-a-service, is a critical budgetary consideration, as is the total expense for long-term data retention with backup-as-a-service. From a technical standpoint, the choice between hybrid cloud vs public cloud backup-as-a-service impacts data control and latency.

- Security remains a dominant theme, with ransomware recovery with backup-as-a-service and achieving cyber resilience with backup-as-a-service being top priorities. This involves implementing zero trust security for backup-as-a-service and utilizing immutable backup storage for financial services. Furthermore, data sovereignty in backup-as-a-service solutions and ensuring backup-as-a-service compliance with gdpr are non-negotiable for global operations.

- Organizations are leveraging AI in backup-as-a-service for anomaly detection and integrating solutions with SIEM tools. Optimizing RTO and RPO with backup-as-a-service, along with endpoint protection using backup-as-a-service, is essential. Following best practices for backup-as-a-service implementation, including for Kubernetes and VMware environments, and closely evaluating backup-as-a-service vendor SLAs, can improve recovery success rates by over 25% compared to ad-hoc approaches.

What are the key market drivers leading to the rise in the adoption of Backup-as-a-service Industry?

- Rising cybersecurity threats and sophisticated ransomware campaigns are a key driver for the market.

- The market is primarily driven by the urgent need for robust cyber risk mitigation in the face of escalating threats. The adoption of immutable storage and advanced ransomware detection capabilities is now a baseline requirement for achieving ransomware readiness.

- Organizations using these technologies report successful data recovery in over 96% of ransomware incidents.

- A secondary driver is the financial shift toward an operational expenditure (OpEx) model, which reduces initial data protection investments by up to 70% compared to traditional hardware procurement.

- This pay-as-you-go backup model, coupled with the imperative for effective cyber recovery and business continuity assurance, makes backup-as-a-service a critical component of modern IT strategy, ensuring threat-aware data management across the enterprise.

What are the market trends shaping the Backup-as-a-service Industry?

- The integration of artificial intelligence and automation into backup processes is an emerging market trend. This development enables predictive analytics, intelligent anomaly detection, and streamlined recovery orchestration.

- Key market trends are centered on the integration of intelligence and automation to enhance data resilience. The adoption of AI-driven recovery analytics and intelligent tiering is enabling the creation of self-optimizing backup platforms. These systems can reduce unnecessary storage costs by up to 30% through automated data lifecycle management.

- Another significant trend is the move toward flexible deployment models that support data governance integration and scalable data safeguarding. The use of cloud data management with sophisticated recovery orchestration allows organizations to meet stringent recovery point objectives (RPOs) with 99% consistency.

- Furthermore, the emphasis on auditable recovery workflows and data protection for containers is becoming standard as enterprises modernize their application architectures.

What challenges does the Backup-as-a-service Industry face during its growth?

- The complexity of managing multi-cloud and hybrid environments presents a key challenge affecting industry growth.

- A primary challenge in the backup-as-a-service market is the inherent difficulty of multi-cloud data management, which can increase administrative overhead by 40% without a unified data management approach. Organizations struggle to achieve a true single-pane-of-glass management view for hybrid cloud recovery and cross-cloud data recovery.

- This complexity is exacerbated by the need for centralized backup management across disparate systems, often leading to gaps in workload protection.

- While automated failover orchestration and intelligent data services aim to simplify operations, the lack of standardized APIs across cloud providers means that achieving seamless, zero-disruption data mobility remains a significant hurdle, complicating efforts to maintain a cohesive data protection strategy.

Exclusive Technavio Analysis on Customer Landscape

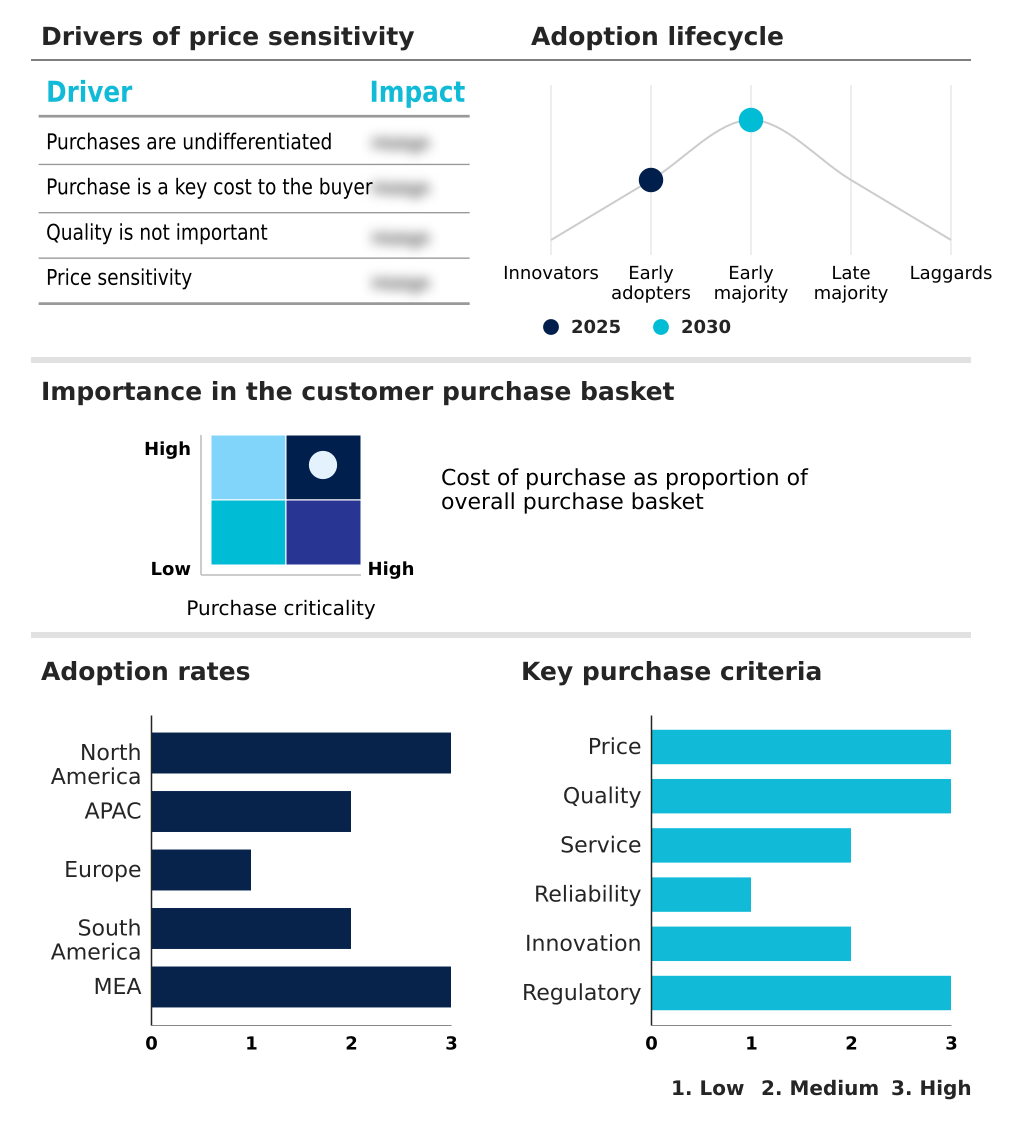

The backup-as-a-service market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the backup-as-a-service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Backup-as-a-service Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, backup-as-a-service market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acronis International GmbH - Offers integrated backup-as-a-service (BaaS) solutions, combining cloud-based data protection and cyber security for enterprises and managed service providers (MSPs).

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acronis International GmbH

- Alphabet Inc.

- Amazon Web Services Inc.

- Arcserve USA LLC

- Broadcom Inc.

- Cisco Systems Inc.

- Commvault Systems Inc.

- Dell Technologies Inc.

- Fujitsu Ltd.

- IBM Corp.

- Insight Enterprises Inc.

- Microsoft Corp.

- NetApp Inc.

- NxtGen Cloud Technologies Ltd.

- Quantum Corp.

- Rubrik Inc.

- Veeam Software Group GmbH

- Vembu Technologies Pvt. Ltd.

- Viatel Technology Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Backup-as-a-service market

- In April, 2025, Veeam announced significant platform enhancements, including new integrations that support AI-driven use cases like natural language querying of backup data to streamline operations.

- In August, 2025, Sophos and Rubrik collaborated to launch an integrated Microsoft 365 backup and recovery solution, embedding restoration workflows into managed detection and response (MDR) services to accelerate incident response.

- In September, 2025, Veeam launched its Veeam Data Cloud in Indonesia, offering a locally hosted platform for Microsoft 365 backup to address data sovereignty and performance requirements.

- In December, 2025, Veeam expanded its strategic alliance with Hewlett Packard Enterprise, introducing new plug-ins and optimized image-level backups to improve hybrid cloud recovery processes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Backup-as-a-service Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 38.8% |

| Market growth 2026-2030 | USD 73679.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 35.8% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, UK, Germany, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The backup-as-a-service market has evolved from a simple storage function to a cornerstone of modern enterprise data resiliency. The core focus is now on delivering a comprehensive data protection platform that ensures continuous data protection and swift cyber recovery.

- This shift is driven by the need for a robust cyber resilience blueprint that integrates ransomware detection, recovery orchestration, and automated recovery testing. At the boardroom level, the adoption of a zero trust data security model directly influences cyber insurance eligibility and budgeting, as it demonstrates proactive risk mitigation.

- Advanced solutions offer multi-cloud data management and hybrid cloud recovery, providing a unified view of data assets. The implementation of immutable storage and air-gapped backups has proven critical, with platforms offering these features reducing recovery time objectives (RTOs) by up to 60%. Key technologies such as data deduplication technology, image-level backups, and synthetic full backups optimize both performance and cost.

- As organizations adopt more SaaS applications, specialized software-as-a-service data backup and endpoint data protection have become essential. The emphasis on data sovereignty compliance and data immutability reinforces the market's alignment with stringent regulatory landscapes, making cloud-native data protection an indispensable component of enterprise strategy.

What are the Key Data Covered in this Backup-as-a-service Market Research and Growth Report?

-

What is the expected growth of the Backup-as-a-service Market between 2026 and 2030?

-

USD 73.68 billion, at a CAGR of 38.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Large enterprises, and SMEs), Application (Online backup, and Cloud backup), Deployment (Public cloud, Hybrid cloud, and Private cloud) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising cybersecurity threats and sophisticated ransomware campaigns, Complexity of managing multi-cloud and hybrid environments

-

-

Who are the major players in the Backup-as-a-service Market?

-

Acronis International GmbH, Alphabet Inc., Amazon Web Services Inc., Arcserve USA LLC, Broadcom Inc., Cisco Systems Inc., Commvault Systems Inc., Dell Technologies Inc., Fujitsu Ltd., IBM Corp., Insight Enterprises Inc., Microsoft Corp., NetApp Inc., NxtGen Cloud Technologies Ltd., Quantum Corp., Rubrik Inc., Veeam Software Group GmbH, Vembu Technologies Pvt. Ltd. and Viatel Technology Group

-

Market Research Insights

- The backup-as-a-service market is defined by a rapid shift toward intelligent, consumption-based data protection models that prioritize cyber risk mitigation. Organizations leveraging AI-powered platforms for predictive failure analysis report a 35% reduction in unplanned downtime. The adoption of a pay-as-you-go backup model allows mid-market firms to reduce capital expenditure (CapEx) reduction by over 60%, aligning costs directly with usage.

- This dynamic is further influenced by managed detection and response (MDR) integration, which has been shown to shorten incident response times by up to 50%. The focus is on achieving a resilient data fabric through scalable data safeguarding and zero-disruption data mobility, ensuring business continuity assurance in increasingly complex IT environments.

We can help! Our analysts can customize this backup-as-a-service market research report to meet your requirements.

RIA -

RIA -