Beryllium Market Size 2024-2028

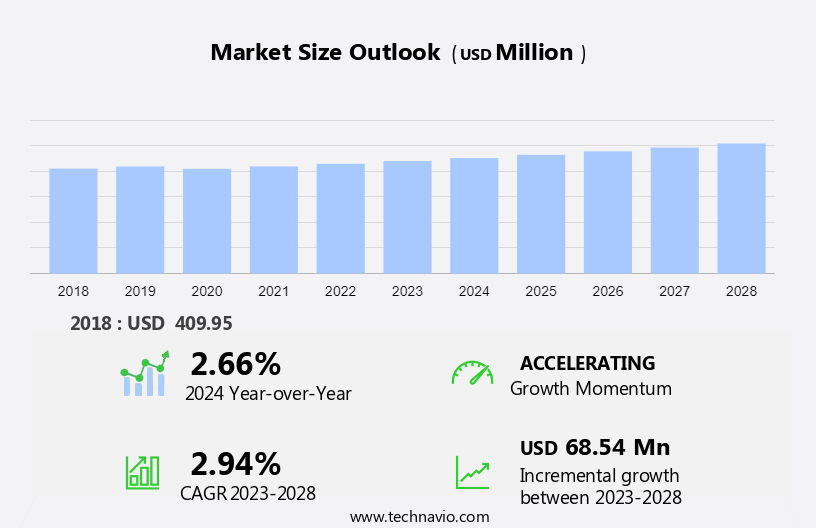

The beryllium market size is forecast to increase by USD 68.54 billion at a CAGR of 2.94% between 2023 and 2028. The market is driven by the significant demand for beryllium in the production of precision instruments, particularly in the aerospace and defense industries. This demand is fueled by the material's unique properties, including its high strength-to-weight ratio and excellent thermal conductivity. However, challenges in the market include the easy availability of substitutes for beryllium hydrochloride, such as beryllium aluminum silicate and beryllium silicate, derived from minerals like phenakite and chrysoberyl. Commercial ores of beryllium are primarily found in the United States, China, and Russia. Market growth may also be influenced by the increasing preference for lightweight materials in various industries, including automotive and telecommunications.

Beryllium is a steel-gray, light, and brittle metal naturally found in the earth's crust. Its chemical symbol is Be, and it is a relatively rare element, making up only 0.0001-0.0005% of the earth's crust. Beryllium is not found in its free state but is primarily extracted from minerals. Beryllium is known for its unique chemical properties, making it a valuable component in various industries. It is a lightweight metal with a high melting point and excellent thermal conductivity. Beryllium is also highly resistant to corrosion and has a low coefficient of thermal expansion.

Furthermore, beryllium is chemically similar to aluminum and shares some of its properties. However, beryllium is more brittle and has a lower density. Beryllium is found in various minerals, including beryl, emerald (green variety), phenakite, and chrysoberyl. The primary commercial ores of beryllium are beryl and beryllium silicate. Beryllium is extracted from these minerals through a process that involves crushing and grinding the ore, followed by heating it in the presence of oxygen to form beryllium oxide. The oxide is then dissolved in concentrated nitric acid to produce beryllium nitrate, which is further processed to obtain pure beryllium. Beryllium is used in various applications due to its unique properties.

Moreover, it is used in the aerospace industry as a structural material due to its high strength-to-weight ratio and excellent thermal properties. Beryllium is also used in the nuclear industry as a moderator in nuclear reactors due to its ability to slow down neutrons. Beryllium is also used in the electronics industry as a component in high-frequency transistors and in the production of beryllium oxide, which is used as a catalyst in the production of certain chemicals. Beryllium hydroxide is used in the pharmaceutical industry as a medication for certain respiratory diseases. Beryllium is a relatively rare element, with the largest producers being China, Russia, and the United States.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Automotive

- Healthcare

- Aerospace and defense

- Others

- Type

- Alloys

- Metals

- Ceramics

- Geography

- North America

- US

- APAC

- China

- India

- Europe

- Middle East and Africa

- South America

- Brazil

- North America

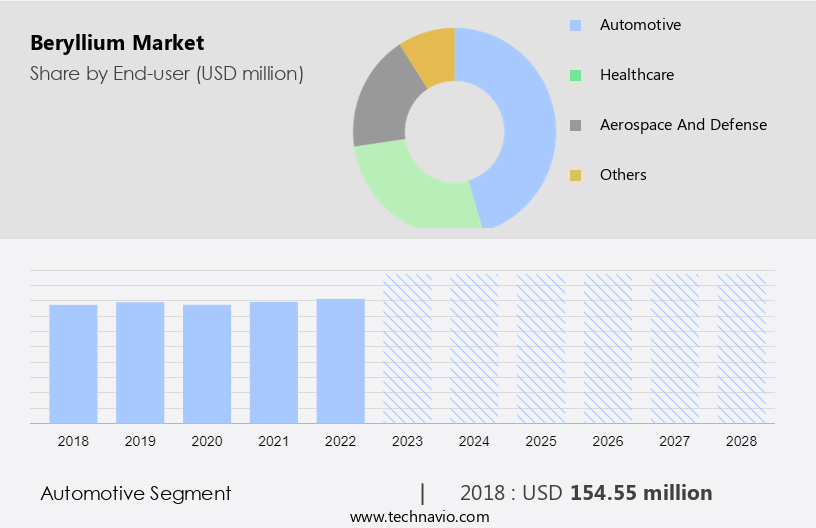

By End-user Insights

The automotive segment is estimated to witness significant growth during the forecast period. Beryllium is a lightweight and strong metal that is increasingly used in the automotive industry due to its superior properties. This element is known for its high thermal conductivity, making it an effective material for enhancing the performance of automotive components. The process of extracting beryllium involves oxidizing it with oxygen, followed by a reaction with concentrated nitric acid. Beryllium oxide, the resulting compound, is then used to produce beryllium alloys. These alloys are valued for their exceptional strength, durability, and ability to withstand high temperatures without degrading. In the automotive sector, beryllium is employed in various applications, including engine components and exhaust systems, where its corrosion resistance is particularly beneficial.

Furthermore, the use of beryllium in automotive manufacturing contributes to reduced vehicle weight, which in turn leads to improved fuel efficiency and enhanced performance. Its high thermal conductivity also ensures that automotive components remain cool under extreme operating conditions, contributing to overall safety and reliability. Beryllium's exceptional properties make it an indispensable material in the automotive industry. Its ability to enhance the structural integrity of parts while reducing weight is a significant factor in the development of more efficient and effective vehicles. Additionally, its resistance to corrosion helps to extend the lifespan of automotive components and reduce maintenance costs.

Get a glance at the market share of various segments Request Free Sample

The automotive segment was valued at USD 154.55 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

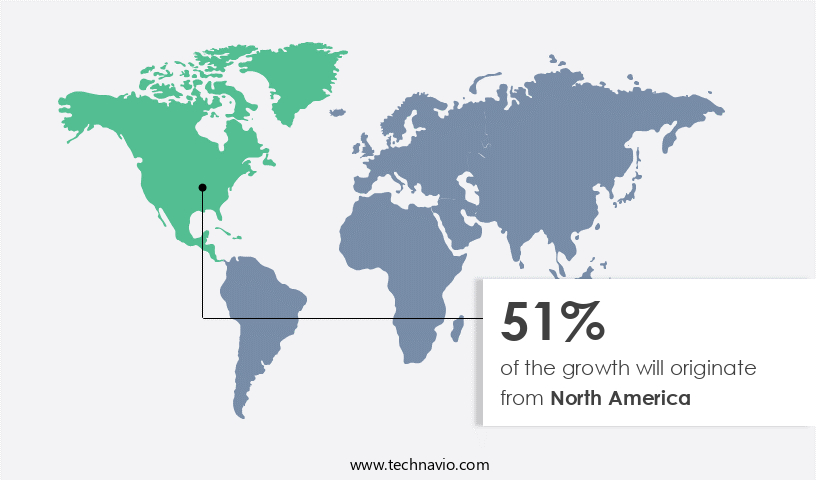

North America is estimated to contribute 51% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In North America, the aerospace and defense industries are major consumers of beryllium alloys due to their desirable properties, such as high strength and dimensional stability. These industries require lightweight materials to reduce fuel consumption and improve overall performance. Beryllium's unique characteristics make it an ideal choice for aerospace applications, including aircraft structures, satellite components, and defense equipment. Additionally, the medical device sector in North America utilizes beryllium alloys for specialized equipment due to their lightweight, high strength, and biocompatibility properties. Furthermore, the region's electronics industry relies on beryllium-copper alloys for their superior electrical and thermal conductivity, as well as corrosion resistance. Furthermore, the increasing investments in modernization projects for these industries will likely boost the demand for beryllium alloys in North America.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

High demand for beryllium in precision instruments is the key driver of the market. Beryllium, a steel-gray metal with brittle nature, is renowned for its unique chemical properties at room temperature. Its minimal thermal expansion ensures that precision instruments retain their dimensions, crucial for accurate measurements and optimal optical performance. The metal's exceptional stiffness and lightweight quality enable precision instruments to maintain structural integrity while minimizing weight, leading to enhanced precision and improved performance.

Furthermore, beryllium's non-magnetic property makes it an ideal choice for applications where magnetic interference could negatively impact performance or accuracy, such as magnetic resonance imaging (MRI) machines, electron microscopes, and magnetic sensors. Lastly, beryllium's excellent thermal conductivity facilitates efficient heat dissipation in precision instruments. This metal's desirable properties make it a valuable component in various industries, including aerospace, defense, and healthcare.

Market Trends

Rising preference for lightweight materials is the upcoming trend in the market. The United States is home to several significant producers of beryllium, a lightweight and strong mineral used extensively in the aerospace and defense industries. Beryllium is primarily found in minerals such as beryllium aluminum silicate and beryllium silicate, with notable finds including phenakite and chrysoberyl. Commercial ores of beryllium are mined and processed to extract beryllium hydroxide, which is then further refined into various forms for industrial applications. Given the importance of weight reduction and enhanced performance in the aerospace and defense sectors, beryllium-containing materials have gained significant traction. These materials are increasingly utilized in aerospace for manufacturing lightweight, high-strength components, such as connectors and fasteners, thereby contributing to improved aircraft performance and fuel efficiency.

Simultaneously, the automotive industry is witnessing a growing demand for beryllium-containing alloys due to their superior properties. Automakers are focusing on meeting stringent fuel efficiency standards and enhancing vehicle performance, leading to the adoption of these alloys in components like brake rotors, pistons, and structural parts. In summary, the increasing demand for lightweight, high-performance materials across the aerospace and defense, as well as automotive industries, is driving the growth of the market in the United States. The use of beryllium-containing materials in components such as connectors, fasteners, brake rotors, pistons, and structural parts is expected to continue, underpinning the market's expansion.

Market Challenge

The easy availability of substitutes for beryllium is a key challenge affecting the market growth. Beryllium, an element with distinctive properties, is extensively utilized in various industries due to its high strength-to-weight ratio and other desirable characteristics. However, alternatives exist for certain beryllium-based materials. In applications where lightweight and strong materials are essential, aluminum alloys serve as viable substitutes. Although they do not exactly replicate beryllium's specific strength-to-weight ratio, aluminum alloys are more accessible, cost-effective, and safer to handle. In specific aerospace and defense applications, titanium alloys emerge as suitable alternatives to beryllium. These alloys boast impressive strength-to-weight ratios and exceptional corrosion resistance, making them suitable for beryllium replacement. Carbon fiber composites are another attractive option for industries focusing on weight reduction.

Furthermore, these materials exhibit remarkable strength properties, making them suitable substitutes for beryllium in the aerospace and automotive sectors. Chemical confirmation of beryllium's presence is crucial in various applications, including its use in the Earth's crust, igneous rocks, and cosmic abundance. Green varieties of beryllium, such as beryllium oxide and chloride, are essential in various industries. Potassium compounds are often used in the production of beryllium. Beryllium's chemical properties and applications are subject to ongoing research and development. Understanding the role of beryllium and its alternatives in various industries is vital for chemical and material scientists, engineers, and businesses.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

American Elements: The company offers beryllium, such as BeO, which is used in advanced ceramic components and compounded materials.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Beryllia Inc.

- American Elements

- AMETEK Inc.

- Aviva Metals Inc.

- Belmont Metals Inc.

- Bob Martin Co.

- Coiling Technologies Inc.

- ENS Technology

- ESPI Metals

- IBC Advanced Alloys Corp.

- IRISO Electronics co. ltd.

- Materion Corp.

- Modison Metals Ltd.

- National Atomic Co. Kazatomprom Joint Stock Co.

- NGK INSULATORS LTD.

- Texas Mineral Resources Corp.

- Xiamen Beryllium Copper Technologies Co. Ltd.

- Alloy Wire International Ltd.

- Knight Strip Metals Ltd

- Wieland Werke AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The steel-gray metal, beryllium, is a brittle element with unique chemical properties that make it valuable in various industries. Beryllium is found in nature associated with minerals like beryl, emerald, and other beryllium aluminum silicates and beryllium silicates. The green variety of beryl, known as emerald, undergoes chemical confirmation to identify the presence of beryllium. Beryllium is a light, silvery-white, alkali earth metal with a cosmic abundance similar to aluminum. It is the 11th element in the earth's crust and is extracted from igneous rocks. The largest producer countries include China, Russia, and the United States. Beryllium has an amphoteric nature and reacts with oxides, chlorides, and hydroxides.

Furthermore, it forms covalent compounds and has a high positive charge density and polarizing power. Beryllium oxide (BeO) is a significant commercial ore used in various applications due to its high thermal conductivity and hardness. Beryllium is used as an alloying agent in high-strength materials, providing better resistance and dimensional stability. It is essential in defence and aerospace industries due to its lightweight and high-performance properties. Beryllium hydroxide and beryllium oxide are commonly used forms of the metal, extracted through processes involving concentrated nitric acid, oxygen, and air. Beryllium is soluble in dilute acid and water and reacts with hydrogen to form metal hydrides. It is a soft metal that reacts with oxygen at room temperature, forming oxides. Other minerals like bertrandite and chrysoberyl contain beryllium in soluble forms. Despite its brittleness, beryllium's unique properties make it an indispensable element in various industries.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.94% |

|

Market Growth 2024-2028 |

USD 68.54 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.66 |

|

Regional analysis |

North America, APAC, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

North America at 51% |

|

Key countries |

US, China, India, Russia, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

American Beryllia Inc., American Elements, AMETEK Inc., Aviva Metals Inc., Belmont Metals Inc., Bob Martin Co., Coiling Technologies Inc., ENS Technology, ESPI Metals, IBC Advanced Alloys Corp., IRISO Electronics co. ltd., Materion Corp., Modison Metals Ltd., National Atomic Co. Kazatomprom Joint Stock Co., NGK INSULATORS LTD., Texas Mineral Resources Corp., Xiamen Beryllium Copper Technologies Co. Ltd., Alloy Wire International Ltd., Knight Strip Metals Ltd, and Wieland Werke AG |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -