Bone Densitometer Market Size 2024-2028

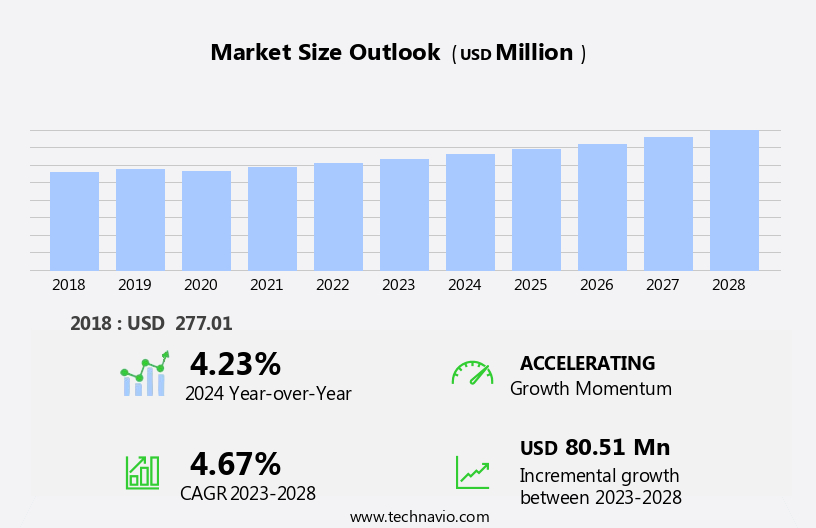

The bone densitometer market size is forecast to increase by USD 80.51 billion at a CAGR of 4.67% between 2023 and 2028.

- The market is experiencing significant growth due to several key trends. The rising prevalence of osteoporosis, particularly among the geriatric population worldwide, is driving market demand. Additionally, the increasing preference for point-of-care (POC) testing is contributing to market growth. However, the high cost of bone densitometers remains a major challenge for market expansion. Despite this, advancements in technology and increasing awareness about the importance of early diagnosis and treatment of osteoporosis are expected to provide opportunities for market growth. Overall, the market is poised for steady growth In the coming years.

What will be the Size of the Bone Densitometer Market During the Forecast Period?

- The market In the US is witnessing significant growth due to the increasing prevalence of bone disorders such as osteoporosis, osteopenia, osteomalacia, and osteoarthritis among the geriatric population. These conditions, characterized by weakened bones and increased risk of fractures, are a major health concern for older adults. Bone densitometry, also known as osteodensitometry, is a medical imaging technique used to measure bone density and assess bone health. DXA scanners and axial bone densitometers are the most commonly used bone densitometer types in clinical settings. The rising awareness of the importance of preventive measures for bone health, as well as the increasing incidence of osteoporotic fractures, hip fractures, and other age-related bone disorders, are key drivers fueling market expansion.

- Additionally, the growing prevalence of kidney disease, which can lead to bone loss, is also contributing to market growth.

How is this Bone Densitometer Industry segmented and which is the largest segment?

The bone densitometer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- Axial BDM

- Peripheral BDM

- End-user

- Hospitals

- Specialty clinics

- Diagnostic and imaging centers

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

By Technology Insights

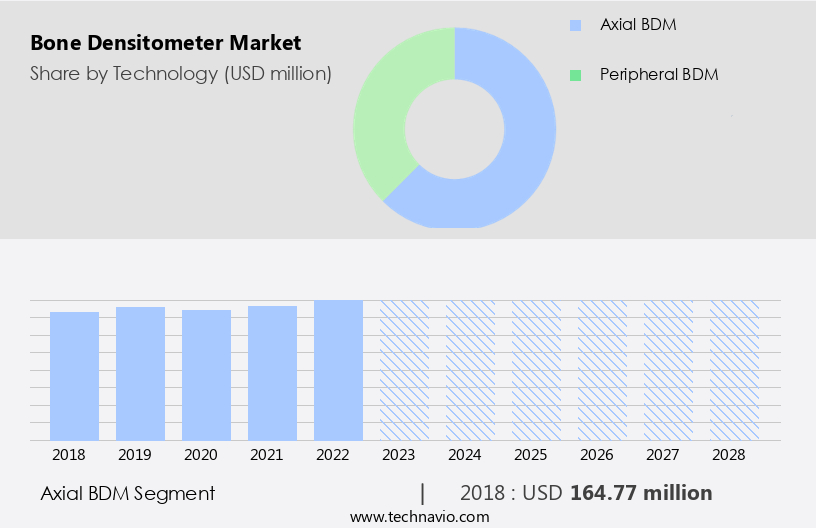

- The axial bdm segment is estimated to witness significant growth during the forecast period.

Axial bone densitometry (BDM) technology plays a significant role In the global market for bone densitometers. Utilizing DEXA as its primary method, axial BDM provides precise assessments of bone mineral density (BMD) in critical areas, such as the spine and hip, which are most susceptible to osteoporosis-related fractures. DEXA is widely accepted as the diagnostic standard for osteoporosis and assessing fracture risks. The demand for axial BDM technology is fueled by the rising incidence of osteoporosis and related bone disorders, particularly among older adults. Early detection and effective management of bone health are crucial for preventing fractures and associated complications.

The precision of axial BDM technology enables healthcare professionals to develop preventive measures and treatment strategies tailored to individual patients.

Get a glance at the Bone Densitometer Industry report of share of various segments Request Free Sample

The Axial BDM segment was valued at USD 164.77 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

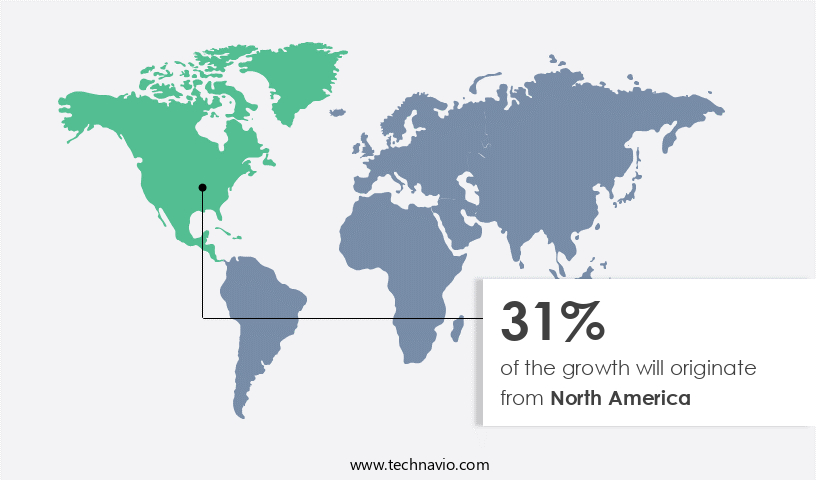

- North America is estimated to contribute 31% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American the market is experiencing significant growth due to the rising incidence of osteoporosis, osteomalacia, and osteoarthritis, as well as the increasing prevalence of aging and kidney disease. According to the National Osteoporosis Foundation, approximately 10 million Americans have osteoporosis, and an additional 44 million are at risk due to low bone density. This demographic trend highlights the importance of early bone health detection and monitoring, leading to increased demand for bone densitometry technology in healthcare facilities across North America. Advancements in medical imaging technology further contribute to market growth. The growing number of cases of osteoporotic fractures, including hip fractures, is another significant factor driving market expansion.

This trend is expected to continue as the population ages and the prevalence of related conditions increases.

Market Dynamics

Our bone densitometer market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Bone Densitometer Industry?

Rising prevalence of osteoporosis due to growing geriatric population worldwide is the key driver of the market.

- The market is experiencing significant growth due to the increasing incidence of osteoporosis and the expanding geriatric population. Osteoporosis, a condition characterized by low bone density and strength, affects an estimated 200 million people worldwide, with postmenopausal women and older adults being the most susceptible. One in three women over the age of 50 and one in five men over the age of 50 are at risk of osteoporosis-related fractures. The geriatric population is also on the rise, with the world's demographic landscape skewing toward older age groups. Bone densitometers are essential medical devices used to measure bone density and assess bone health.

- These devices play a crucial role in diagnosing and monitoring bone disorders, including osteoporosis, osteopenia, osteomalacia, and osteoarthritis. They are also used In the diagnosis of conditions such as cystic fibrosis and rheumatoid arthritis. Bone densitometers come in various forms, including dual-energy X-ray absorptiometry (DXA) scanners, ultrasonic densitometers, digital detectors, and quantitative ultrasound (QUS). DXA scanners are the most common type of bone densitometer and are used to measure bone density In the hip, spine, and forearm. Portable bone densitometers are also available, making bone health assessment more accessible. The market for bone densitometers is driven by the need for preventive measures and treatment strategies for bone disorders.

- The high risk of fractures associated with osteoporosis and the increasing cancer incidence, particularly in older adults, are significant factors driving market growth. Additionally, the rising prevalence of kidney disease and the importance of preventive healthcare have led to an increase in routine bone density checks. Bone densitometers are used in various healthcare settings, including hospitals, clinics, and specialty centers. The market for bone densitometers is expected to continue growing due to the increasing awareness of bone health and the availability of refurbished devices, making these essential medical devices more affordable. In conclusion, The market is experiencing significant growth due to the increasing incidence of osteoporosis, the expanding geriatric population, and the importance of preventive healthcare.

What are the market trends shaping the Bone Densitometer Industry?

Rising demand for point-of-care (POC) testing is the upcoming market trend.

- The market In the US is experiencing significant growth due to the increasing preference for point-of-care (POC) testing solutions. Traditionally, bone densitometry tests were conducted in specialized clinics or hospitals, necessitating patients to travel long distances for assessments. However, the importance of convenience and accessibility in healthcare delivery is gaining recognition, leading to a shift towards POC testing. Portable and handheld bone densitometry devices offer several advantages over traditional clinic-based testing. These devices enable bone density assessments to be performed at the patient's bedside, in primary care offices, pharmacies, or even in community health centers. The geriatric population, who are at a higher risk of bone disorders such as osteoporosis and fractures, can benefit significantly from these devices' accessibility.

- Bone densitometry is essential for diagnosing and monitoring bone health conditions such as osteoporosis, osteopenia, osteomalacia, and osteoarthritis. These conditions are prevalent in older adults, and their incidence increases with age, making preventive measures and treatment strategies crucial. Vitamin D deficiency, a common risk factor for bone disorders, can also be identified through bone densitometry tests. Bone densitometry devices are used in various medical facilities, including hospitals, clinics, and specialty centers. They are also used for diagnosing conditions such as cystic fibrosis and rheumatoid arthritis. In addition, these devices are used for cancer cells diagnosis, body composition measurement, and monitoring the effectiveness of treatment plans.

- The market for bone densitometry devices includes various types of medical devices, such as ultrasonic densitometers, digital detectors, computer-assisted densitometers, and radiographic absorptiometry (RA) scanners. Some of the popular brands include AccuDexa bone densitometer, Axial bone densitometers, and portable bone densitometers. The market for bone densitometry devices is expected to grow due to the rising incidence of osteoporosis and fractures, especially In the geriatric population. The increasing awareness of preventive healthcare and the availability of refurbished devices at affordable prices are also contributing to the market's growth. Quantitative ultrasound (QUS) and radiographic absorptiometry (RA) are the two primary techniques used in bone densitometry.

- QUS measures bone density by analyzing the speed of sound waves passing through the bone, while RA measures bone density by analyzing the amount of X-rays absorbed by the bone. Both techniques have their advantages and are used depending on the specific application and patient needs. In conclusion, the market In the US is experiencing significant growth due to the increasing demand for point-of-care testing solutions, the rising incidence of bone disorders, and the availability of various types of bone densitometry devices. These devices offer several advantages over traditional clinic-based testing, including convenience, accessibility, and affordability. The market is expected to continue growing due to the increasing awareness of preventive healthcare and the availability of refurbished devices at affordable prices.

What challenges does Bone Densitometer Industry face during the growth?

High cost of bone densitometers is a key challenge affecting the industry growth.

- The market faces a notable challenge due to the high cost of these medical devices. Bone densitometers are essential tools for diagnosing bone disorders, including osteoporosis, which affects older adults and increases the risk of fractures. These conditions are prevalent among the geriatric population, with an estimated incidence of osteoporosis being over 53 million In the US alone. Bone densitometers use various technologies, such as Dual-energy X-ray absorptiometry (DXA), ultrasonic densitometers, and quantitative ultrasound (QUS), to measure bone density and strength. DXA scanners are the most commonly used bone densitometers, with prices ranging from USD16,000 to USD45,000 for new models.

- Refurbished units offer a more affordable alternative, costing between USD5,000 and USD25,500. However, even refurbished devices require a significant investment. The high cost of bone densitometers is a significant barrier to widespread adoption, particularly in developing regions and specialty centers. The initial investment for these devices, along with ongoing maintenance and replacement costs for components like X-ray tubes, can add up to a substantial financial burden. Despite these challenges, bone densitometers remain crucial for preventive healthcare, treatment planning, and monitoring bone health in older adults and those at risk of bone disorders, including osteoporosis, osteopenia, osteomalacia, osteoarthritis, and osteoporotic fractures.

- Bone densitometers are also used for diagnosing other conditions, such as cystic fibrosis and rheumatoid arthritis, and for measuring body composition. These devices are used in hospitals, clinics, and other medical facilities, including diagnostic and imaging centers. In the US, Medicare covers bone densitometry services for certain individuals, making these tests more accessible to some populations. However, the high cost of bone densitometers remains a significant barrier to widespread adoption, particularly in developing regions and specialty centers.

Exclusive Customer Landscape

The bone densitometer market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the bone densitometer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, bone densitometer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Aarna Systems And Wellness Pvt. Ltd. - Our company provides a range of advanced bone densitometry solutions for medical professionals In the US market. These include DEXA (Dual-energy X-ray Absorptiometry) Bone Densitometers, Ultrasound Bone Densitometers, BMD (Bone Mineral Density) Machines, and Portable Bone Densitometers. These technologies enable accurate assessment of bone health and density, aiding In the early detection and diagnosis of conditions such as osteoporosis. Our commitment to innovation and quality ensures that our bone densitometers meet the highest industry standards.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aarna Systems And Wellness Pvt. Ltd.

- BeamMed Ltd.

- BMTech Co. Ltd.

- CompuMed Inc.

- CyberLogic inc.

- Demetech AB

- Dentsply Sirona Inc.

- Echolight SpA

- Eurotec Medical Systems s.r.l.

- Furuno Electric Co. Ltd.

- GE Healthcare Technologies Inc.

- Hologic Inc.

- Koninklijke DSM NV

- Medonica Co. Ltd.

- Osteosys Corp.

- Scanflex Healthcare AB

- Shenzhen Aikerui Electric Co. Ltd.

- Swissray International Inc.

- Trivitron Healthcare

- Anjue Medical Equipment Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Understanding the Dynamics of the market the market represents a significant segment of the medical device industry, catering to the growing demand for tools that assess bone density and strength. This market is driven by the increasing prevalence of bone disorders, particularly osteoporosis, and the need for effective preventive measures and treatment strategies. Bone densitometry is a crucial diagnostic tool for evaluating bone health, particularly in older adults. The geriatric population is at a higher risk of developing bone disorders due to age-related bone loss and other factors. Osteoporosis, a condition characterized by low bone density and increased risk of fractures, affects millions of people worldwide.

Bone densitometry plays a vital role In the diagnosis and monitoring of osteoporosis. The technology uses various methods, such as dual energy X-ray absorptiometry (DXA) and quantitative ultrasound (QUS), to measure bone density and assess bone health. DXA scanners are the most commonly used bone densitometry devices, providing accurate measurements of bone density In the hip and spine. Preventive healthcare is a growing trend In the market, with routine checks becoming increasingly important for early detection and intervention. Medicaid and Medicare, among other healthcare programs, cover bone densitometry tests for eligible individuals, making it an accessible and essential diagnostic tool.

The market for bone densitometers is diverse, with various types of devices catering to different needs. Portable bone densitometers offer convenience and mobility, making them suitable for use in specialty centers and diagnostic & imaging centers. Axial bone densitometers, such as the AccuDexa bone densitometer, measure bone density In the axial skeleton, while peripheral bone densitometers assess bone density In the arms and legs. The use of bone densitometry extends beyond the diagnosis and monitoring of osteoporosis. These devices are also used In the diagnosis of other bone disorders, such as osteopenia, cystic fibrosis, rheumatoid arthritis, and certain types of cancer.

Additionally, bone densitometry is used for body composition measurement and the assessment of bone loss in individuals with kidney disease or those undergoing orthopaedic procedures. The market is expected to grow significantly due to the increasing incidence of osteoporosis and other bone disorders. Factors contributing to this growth include an aging population, the rising prevalence of vitamin D deficiency, and the need for effective treatment planning and monitoring. In conclusion, the market is a dynamic and growing segment of the medical device industry. These devices play a crucial role In the diagnosis, monitoring, and treatment of various bone disorders, making them an essential tool for healthcare providers and patients alike.

The market is diverse, with various types of bone densitometers catering to different needs and applications. The growing trend towards preventive healthcare and the increasing incidence of bone disorders are expected to drive the growth of the market In the coming years.

|

Bone Densitometer Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.67% |

|

Market growth 2024-2028 |

USD 80.51 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, UK, Germany, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Bone Densitometer Market Research and Growth Report?

- CAGR of the Bone Densitometer industry during the forecast period

- Detailed information on factors that will drive the Bone Densitometer growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the bone densitometer market growth of industry companies

We can help! Our analysts can customize this bone densitometer market research report to meet your requirements.

RIA -

RIA -