Bone Wax Market Size 2024-2028

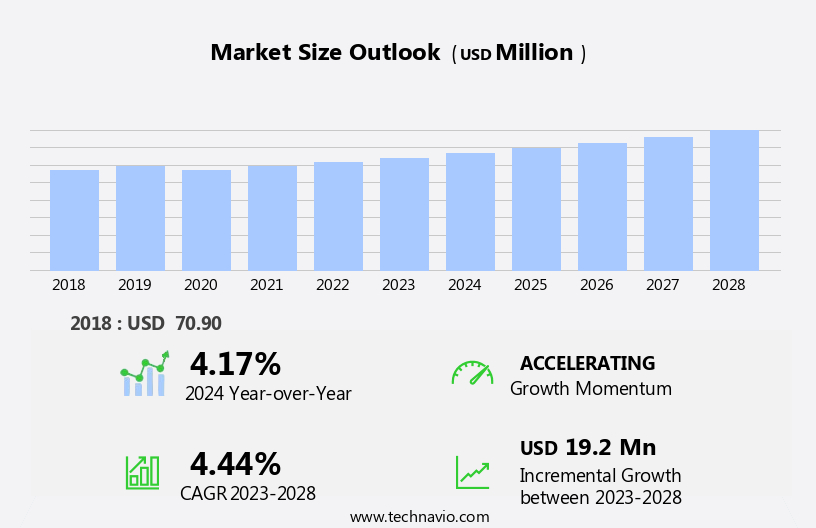

The bone wax market size is forecast to increase by USD 19.2 million, at a CAGR of 4.44% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing prevalence of orthopedic conditions and the subsequent rise in surgical procedures. This trend is driven by an aging population, increasing obesity rates, and sedentary lifestyles, all of which contribute to the development of orthopedic diseases. Moreover, the adoption of minimally invasive orthopedic surgeries is on the rise, as they offer numerous benefits, such as reduced post-operative pain, faster recovery times, and lower infection rates. However, the use of bone wax in these procedures presents certain challenges. Side effects of bone wax, including allergic reactions, infection, and granuloma formation, can complicate patient recovery and increase healthcare costs.

- As a result, there is a growing demand for alternative bone grafting materials that offer comparable efficacy with fewer side effects. Companies seeking to capitalize on market opportunities should focus on developing innovative bone grafting solutions that address these challenges and meet the evolving needs of healthcare providers and patients.

What will be the Size of the Bone Wax Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in medical technology and the expanding scope of its applications. Wax-based hemostats, including beeswax and paraffin bone wax, serve as essential tools in various surgical procedures for controlling bleeding and sealing bone cavities. These waxes offer surgical sealant properties, making them indispensable in orthopedic, neuro, and maxillofacial surgeries. Manufacturers are continually refining bone wax formulations to enhance efficacy, improve handling, and ensure biocompatibility. Paraffin bone wax, for instance, is gaining popularity due to its lower melting point and easier application. However, the market is not without challenges. Bone wax residue and absorption rates remain areas of concern, necessitating ongoing research and development.

Bone wax removal and sterilization methods are also under scrutiny, with manufacturers exploring new techniques to minimize toxicity and ensure standardization. Additionally, bone wax specifications, such as viscosity, consistency, and composition, are subject to rigorous testing and quality control measures. The market for bone wax alternatives is growing, with synthetic and biodegradable options gaining traction. These substitutes offer advantages such as reduced risk of infection, improved patient outcomes, and reduced environmental impact. However, they face challenges in terms of cost, availability, and regulatory approval. In summary, the market is a dynamic and evolving landscape, with ongoing research and development shaping its future.

From formulation refinements to alternative solutions, the focus remains on improving patient outcomes while addressing challenges related to residue, absorption, and toxicity.

How is this Bone Wax Industry segmented?

The bone wax industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

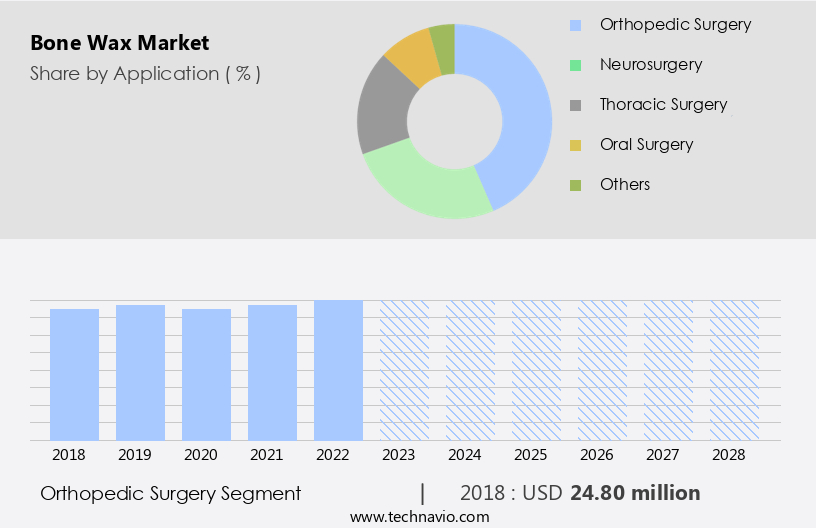

- Orthopedic surgery

- Neurosurgery

- Thoracic surgery

- Oral surgery

- Others

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Application Insights

The orthopedic surgery segment is estimated to witness significant growth during the forecast period.

The market caters to the production and supply of wax-based hemostats used in orthopedic surgeries for controlling bleeding and sealing bone cavities. These products, available in various forms such as beeswax bone wax and paraffin bone wax, are essential in procedures addressing disorders of the bones, ligaments, joints, tendons, and muscles. Bone wax formulations offer surgical sealant properties, ensuring efficient hemostasis and facilitating proper bone healing. Manufacturers focus on standardizing bone wax composition and specifications, ensuring biocompatibility and minimizing toxicity. Bone wax handling and sterilization are crucial aspects of the production process to maintain product efficacy. Absorption, viscosity, and consistency are key considerations in the formulation of bone wax.

Alternatives to bone wax, such as adhesives and synthetic sealants, are gaining popularity due to their ease of use and potential cost savings. However, bone wax remains a preferred choice for many surgeons due to its proven efficacy in controlling bleeding and sealing bone cavities. Bone wax removal and degradation are areas of ongoing research to minimize complications and optimize patient outcomes. Additives and advanced formulations are being explored to enhance the performance and versatility of bone wax in various surgical applications.

The Orthopedic surgery segment was valued at USD 24.80 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

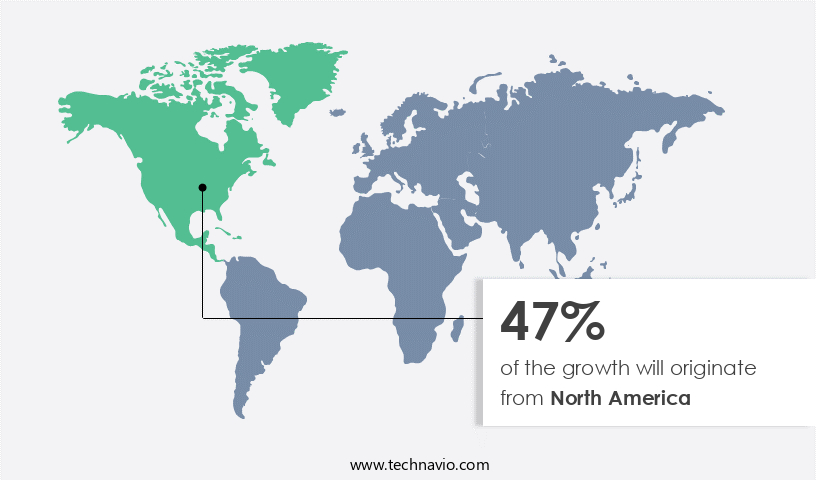

North America is estimated to contribute 47% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is driven by the increasing prevalence of orthopedic procedures and the need for effective hemostasis during surgeries. In 2023, North America held the largest market share due to the high incidence of obesity and aging populations in the region. These factors contribute to a higher demand for bone wax in surgical applications. Bone wax, available in various formulations such as beeswax and paraffin, offers surgical sealant properties and aids in bone cavity sealant during procedures. However, concerns regarding bone wax residue and toxicity have led to the development of bone wax alternatives and additives to enhance absorption and biocompatibility.

Manufacturers prioritize standardization and sterilization methods to ensure the efficacy of bone wax. The market is expected to grow as advancements in bone wax formulation and handling techniques continue to address the challenges of bone wax degradation and consistency.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Bone wax, a crucial surgical material in orthopedic procedures, is a wax-like substance used to seal bone gaps during surgeries. Its melting point properties allow it to be easily applied and melt into bone marrow, promoting effective bone healing. The biocompatibility of bone wax is rigorously tested through various methods, including in vitro cytotoxicity tests and implantation studies in animals. Application techniques for bone wax involve melting the wax and applying it to the bone gap using a bone wax applicator. Compositionally, bone wax consists of beeswax, paraffin wax, and other additives, which promote bone healing and prevent the ingrowth of soft tissue into the bone gap. Bone wax degrades gradually in the human body, allowing new bone growth to occur. Its viscosity plays a significant role in surgery, as a lower viscosity allows for easier application and better sealing of the bone gap. Sterilization and packaging requirements are essential for bone wax, with methods including autoclaving and gamma irradiation. Quality control and standardization are crucial to ensure consistent product performance, and regulatory compliance and certifications, such as ISO 13485 and FDA 510(k), are mandatory. Bone wax has a shelf life of up to five years when stored at room temperature and protected from light. Alternatives to bone wax, such as fibrin glue and synthetic bone graft substitutes, have emerged, but their effectiveness varies. Handling and application guidelines must be followed to ensure optimal results, and residue removal techniques include irrigation with saline solution or the use of bone wax removal tools. Manufacturing processes involve strict quality checks to ensure consistency and purity. Bone wax is used in various surgical procedures, including spinal fusion, joint reconstruction, and trauma surgery. Its functional roles include promoting bone healing, preventing bone gap infection, and reducing the risk of bone graft failure. Efficacy and performance evaluation metrics include bone healing rate, bone gap sealing efficiency, and biocompatibility. Material properties and characterization techniques, such as Fourier transform infrared spectroscopy (FTIR) and scanning electron microscopy (SEM), are used to understand bone wax's behavior in the body and optimize its performance. Biocompatibility studies and safety protocols are essential to ensure bone wax's market adherence to regulatory standards, providing surgeons and patients with confidence in the product's safety and effectiveness.

What are the key market drivers leading to the rise in the adoption of Bone Wax Industry?

- The orthopedic market is primarily driven by the increasing prevalence of orthopedic conditions resulting in a rise in surgical cases.

- Every year, approximately 37.3 million severe falls worldwide necessitate medical attention, resulting in substantial medical expenses, with the US incurring over USD50 billion for both fatal and non-fatal falls. The lengthy healing process of fractured bones necessitates effective solutions for enhancing bone repair. The Arthritis Foundation anticipates that degenerative joint diseases, including osteoarthritis, will affect around 130 million people globally by 2050, leading to increased demand for bone healing products. Ambulatory Surgical Centers (ASCs), which are day surgical facilities, have gained popularity among patients due to their cost-saving advantages over hospital stays.

- However, the choice between ASCs and inpatient departments depends on the nature of the orthopedic condition. The growing number of cases requiring bone healing solutions and the shift towards cost-effective healthcare infrastructure are key market dynamics driving the demand for bone wax substitutes.

What are the market trends shaping the Bone Wax Industry?

- The increasing preference for minimally invasive orthopedic surgeries represents a significant market trend. This approach to orthopedic procedures offers numerous benefits, including reduced recovery time, minimal scarring, and fewer complications, making it an attractive option for patients and healthcare providers alike.

- The market for hemostatic bone wax, a type of surgical sealant, is experiencing significant growth due to the increasing adoption of minimally invasive surgeries. Minimally invasive procedures offer numerous advantages over traditional open surgeries, including shorter hospital stays, less pain and discomfort, lower infection and bleeding risks, and quicker recovery times. In orthopedic procedures, minimally invasive surgery is increasingly used for arthroscopy, knee and hip joint replacements, and spine fusion. Arthroscopy, a minimally invasive procedure, is commonly used to treat injuries in the shoulder, elbow, wrist, knee, and ankle. The preference for minimally invasive surgery in the treatment of sports-related injuries is also on the rise.

- The hemostatic properties of bone wax are crucial in minimally invasive surgeries to control bleeding and ensure proper bone alignment during the healing process. The formulation of bone wax plays a significant role in its effectiveness as a hemostatic agent, and its storage is essential to maintain its quality.

What challenges does the Bone Wax Industry face during its growth?

- The use of bone wax in the medical industry comes with significant side effects, posing a substantial challenge to the industry's growth.

- Bone wax, a traditional hemostatic agent, is primarily made up of beeswax and petroleum jelly. Its primary function is to control bleeding from bone surfaces by obstructing blood flow from vessels. However, it does not possess any biologic hemostatic effect. The use of bone wax is not recommended when bone union is necessary due to its inhibiting effect on bone healing. Furthermore, it can hinder bacterial clearance from cancellous bone and should be avoided in areas of contamination or infection. Despite its usage, bone wax comes with potential risks such as allergic reactions, granulomatous reactions, and embolization, which involves the lodging of an embolus within the bloodstream.

- These adverse effects have led to the exploration of bone wax alternatives. The efficacy of paraffin bone wax, a potential substitute, is under investigation due to its biocompatibility and reduced risk of adverse reactions. The manufacturing process of bone wax is intricate, and its removal can be challenging, necessitating the need for alternative bone cavity sealants that offer superior healing properties and ease of removal.

Exclusive Customer Landscape

The bone wax market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the bone wax market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, bone wax market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abyrx Inc. - The company introduces a bone wax solution comprised of two putties. Upon mixing for 45 seconds, this product is ready for application to bleeding bone tissue. Marketed under the brand name Abyrx, it provides an effective response for surgical procedures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abyrx Inc.

- B.Braun SE

- Baxter International Inc.

- Bentley Healthcare Pvt. Ltd.

- Futura Surgicare Pvt. Ltd.

- GPC Medical Ltd.

- Healthium Medtech Pvt. Ltd.

- Henry Schein Inc.

- Johnson and Johnson Services Inc.

- Lotus Surgicals Pvt. Ltd.

- LUXSUTURES

- Medline Industries LP

- Medtronic Plc

- Orion Sutures India Pvt. Ltd.

- Saintroy Lifescience

- Surgical Sutures Pvt. Ltd.

- Thermo Fisher Scientific Inc.

- Unisur Lifecare Pvt. Ltd.

- VWR International LLC

- World Precision Instruments

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Bone Wax Market

- In January 2024, Stryker Corporation, a leading medical technology company, announced the launch of their new bone wax product, Vidax Plus, in the European market. Vidax Plus is an advanced bone wax formulation designed to minimize bone fragment displacement during surgery, enhancing surgical outcomes (Stryker Corporation Press Release).

- In March 2024, Medtronic plc, another major player in the medical technology industry, entered into a strategic partnership with Arthrex, Inc., a leading manufacturer of orthopedic and sports medicine products, to co-develop and commercialize a novel bone wax product. The partnership aims to leverage Medtronic's global reach and Arthrex's expertise in bone wax technology (Medtronic plc Press Release).

- In May 2024, Ethicon, a Johnson & Johnson company, secured regulatory approval from the U.S. Food and Drug Administration (FDA) for its new bone wax product, Surgicel Bone Wax. This approval marks Ethicon's entry into the market, expanding their portfolio of surgical products (Johnson & Johnson Press Release).

- In April 2025, Smith & Nephew, a leading global medical device manufacturer, completed the acquisition of Osiris Therapeutics, a regenerative medicine company. The acquisition includes Osiris' bone wax product, OsteoFuse, which utilizes a unique combination of bone wax and bone graft to promote bone healing (Smith & Nephew Press Release).

Research Analyst Overview

- The market encompasses a range of medical devices used for bone cavity filling and surgical hemostasis during orthopedic procedures. These products, serving as wound sealing agents, play a crucial role in ensuring effective bleeding control and promoting tissue adhesion. The regulatory aspects surrounding bone wax processing are stringent due to the biomedical material's inherent risks. Material characterization and quality assurance are essential for ensuring product safety and sterility assurance. Clinical applications of bone wax extend beyond orthopedics, with surgical techniques employing these materials in various medical procedures. Biological sealants, including bone wax, undergo rigorous efficacy testing and performance evaluation to meet the demands of medical regulation.

- Material properties, such as setting time and adhesion strength, significantly impact the success of surgical procedures. Ingredients used in bone wax production must adhere to stringent safety guidelines, with hemostatic agents and tissue sealants ensuring optimal surgical outcomes. The market for bone wax and related biomedical materials continues to evolve, driven by advancements in material science and the pursuit of improved surgical techniques.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Bone Wax Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

140 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.44% |

|

Market growth 2024-2028 |

USD 19.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.17 |

|

Key countries |

US, Germany, China, UK, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Bone Wax Market Research and Growth Report?

- CAGR of the Bone Wax industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the bone wax market growth of industry companies

We can help! Our analysts can customize this bone wax market research report to meet your requirements.

RIA -

RIA -