Brazil Oil and Gas Market Size and Trends

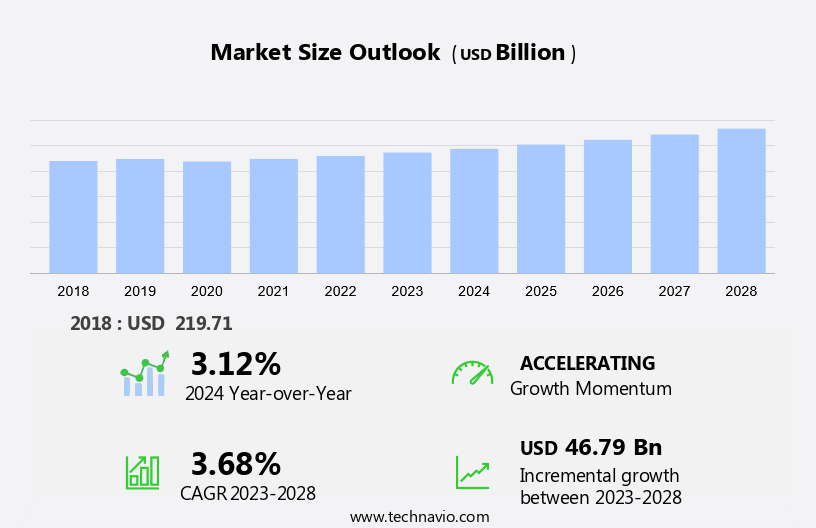

The Brazil oil and gas market size is forecast to increase by USD 46.79 billion at a CAGR of 3.68% between 2023 and 2028. The market is experiencing significant growth, driven by technological advancements in drilling techniques and the increasing adoption of natural gas vehicles (NGVs). These trends are contributing to the expansion of the market, particularly in the upstream sector. Furthermore, the increasing use of renewable fuel sources, such as offshore wind power and solar, is creating opportunities for the integration of renewable energy into the oil and gas industry. This integration is expected to reduce the carbon footprint of oil and gas companies and help them meet sustainability goals. However, challenges such as regulatory issues, high operational costs, and geopolitical risks continue to pose threats to market growth. Despite these challenges, the market is expected to grow at a steady pace, driven by the aforementioned trends and the vast potential for oil and gas exploration in Brazil.

The market has been a significant hydrocarbon investment destination due to its vast reserves of crude oil and natural gas. The country is the tenth-largest producer of crude oil in the world and the eighth-largest consumer of petroleum products. The exploration and production sector, including refineries, is a capital-intensive industry that contributes significantly to the country's gross domestic product. Free cash flows from oil and gas operations have been a driving force for shareholders and investors in the market. However, the industry faces challenges such as emissions reduction targets and the shift towards low-carbon energies. Regulators play a crucial role in implementing policies to balance the economic benefits of hydrocarbon production with environmental concerns. Brazil's oil refining capacity stands at approximately 1.6 million barrels per day, making it the seventh-largest refining country in the world. The country's non-OECD petroleum consumption is expected to increase due to growing demand for petrol products. The International Energy Agency (IEA) forecasts that Brazil will remain a significant consumer of oil and natural gas as fuel sources for processes and systems in various industries. The market's future growth depends on continued investment in exploration and production and the development of new technologies to reduce emissions and improve efficiency.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion " for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Application Outlook

- Industrial

- Commercial

- Residential

- Deployment Outlook

- Offshore

- Onshore

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

By Application Insights

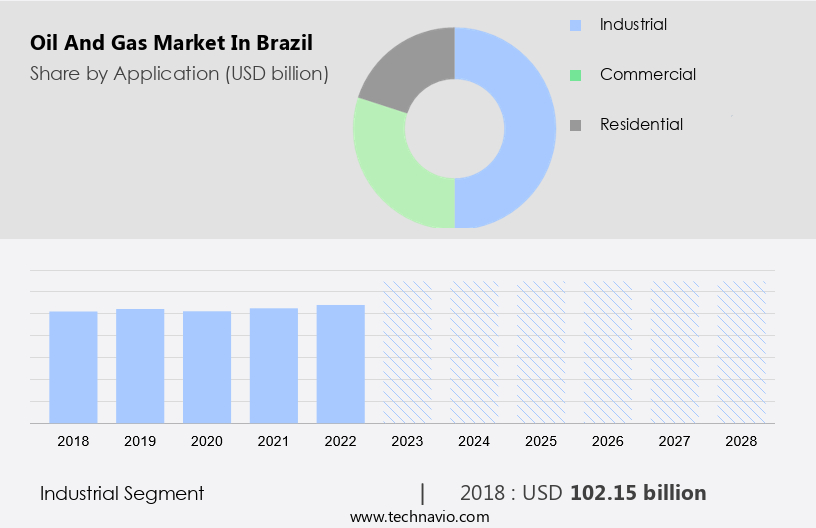

The industrial segment is estimated to witness significant growth during the forecast period. The market is characterized by processing concentration and the presence of critical mineral resources, including nickel, graphite, lithium, cobalt, and rare earth elements. Occidental Petroleum and TerraLithium are among the companies exploring these resources in the country.

Get a glance at the market share of various regions Download the PDF Sample

The industrial segment was the largest segment and valued at USD 102.15 billion in 2018. Control of critical mineral rights and regulatory knowledge are crucial for companies in the clean energy manufacturing sector, given the increasing demand for lithium for EV battery production. Brine deposits are a significant source of lithium in Brazil, and companies are focusing on optimizing water resources and reducing lead times to gain a competitive edge. Hence, such factors are fuelling the growth of this segment during the forecast period.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Brazil Oil and Gas Market Driver

Technological advancements in drilling techniques is notably driving market growth. The market has witnessed significant advancements in exploration and production techniques, particularly in the areas of shale formations. Horizontal drilling technology, which enables drillers to access a wider section of shale rock from a single wellbore, has become a game-changer. This is achieved by drilling vertically to the target depth and then turning the drill bit horizontally within the shale formation. This technique has significantly increased productivity and overall resource recovery.

Another crucial development is the application of hydraulic fracturing, which involves injecting a high-pressure fluid mixture into the shale formation to create fractures, thereby allowing natural gas to flow more freely. Innovations in fracking technology, such as multi-stage fracking, have led to more efficient and effective methods by isolating and stimulating specific sections of the wellbore. Thus, such factors are driving the growth of the market during the forecast period.

Brazil Oil and Gas Market Trends

Growing adoption of NGVs is the key trend in the market. The market is witnessing significant growth in the adoption of natural gas as a cleaner alternative fuel, particularly in the transportation sector. The Net-Zero Industry Act and other clean energy policies have encouraged the use of natural gas as a more sustainable fuel option.

The popularity of natural gas vehicles (NGVs) has prompted companies like Ford and GM to introduce certified natural gas conversion systems, enabling consumers to convert internal combustion engines to natural gas-powered engines without voiding the warranty. Thus, such trends will shape the growth of the market during the forecast period.

Brazil Oil and Gas Market Challenge

Increasing use of renewable energy sources is the major challenge that affects the growth of the market. The market is facing significant challenges due to the global shift towards clean energy and net-zero emission targets. The declining costs of renewable energy technology and equipment are making solar and wind power increasingly competitive with traditional gas-fired power plants.

Consequently, the high capital investments required for oil and gas projects may divert towards renewables, potentially hindering the growth of the oil and gas industry in Brazil. Hence, the above factors will impede the growth of the market during the forecast period

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

ALYA CONSTRUTORA: The company offers oil and gas through its subsidiary Enauta Participacoes in Manati wells which are connected by subsea lines to the PMNT-1 platform, a fixed production unit installed at a water depth of 35 m, 10 km offshore.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bechtel Corp.

- BP Plc

- Chevron Corp.

- Equinor ASA

- Exxon Mobil Corp.

- MITSUI and CO. LTD.

- Murphy Oil Corp.

- Petroleo Brasileiro SA

- Shell plc

- TotalEnergies SE

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Analyst Overview

The market is witnessing significant investments in hydrocarbon exploration and production, driven by high free cash flows and operational efficiency. However, the industry is also facing the challenge of reducing emissions and transitioning to low-carbon energies. The Brazilian government has set renewable energy targets, leading to an increase in renewable power projects and renewable energy auctions. The supply chain for low-carbon fuels, such as natural gas, biofuels, hydrogen, and renewable energy, is gaining importance. Critical minerals mining is a crucial aspect of this supply chain, as these minerals are essential for the production of clean energy technologies. The adoption of clean energy avenues, including CCS development and green initiatives, offers benefits such as reduced emissions and improved environmental sustainability. However, there are risks associated with these advancements, including capital allocation strategies, feedstock supply, and scalability. Internal considerations, such as operational efficiency and backward integration, are essential for the progression of the oil and gas industry in Brazil. External considerations, including consumer preferences and regulatory frameworks, also play a significant role in the industry's development. Coalitions between industry players and governments are essential for the commercial viability of clean energy projects. The long-term contracts for renewable energy and natural gas are crucial for securing capital and ensuring the scalability of these projects. The market is at a critical juncture, with opportunities for high-return capex strategies in both traditional and clean energy sectors. The industry must balance internal considerations with external pressures to ensure a sustainable and profitable future.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

141 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.68% |

|

Market growth 2024-2028 |

USD 46.79 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

3.12 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ALYA CONSTRUTORA, Bechtel Corp., BP Plc, Chevron Corp., Equinor ASA, Exxon Mobil Corp., MITSUI and CO. LTD., Murphy Oil Corp., Petroleo Brasileiro SA, Shell plc, and TotalEnergies SE |

|

Market dynamics |

Parent market analysis, market report , market forecast , Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Brazil

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -