Bulk Food Ingredient Market Size 2026-2030

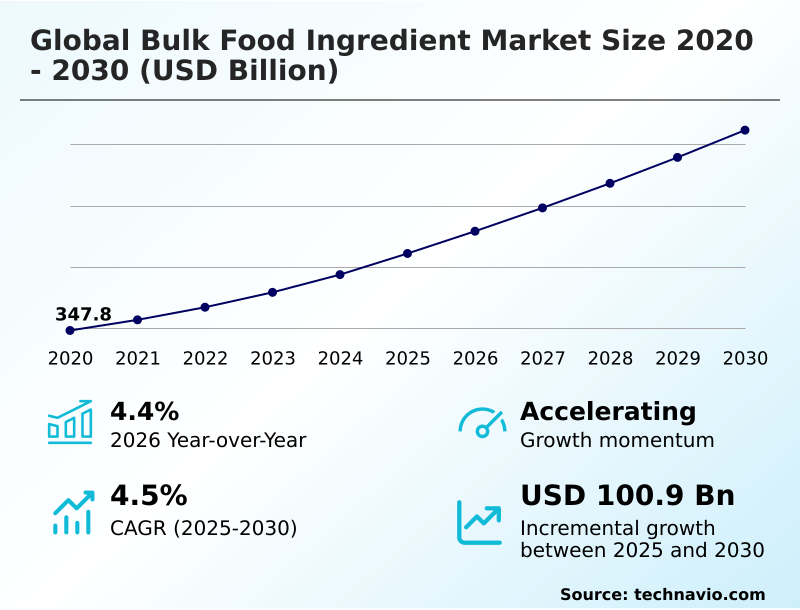

The bulk food ingredient market size is valued to increase by USD 100.9 billion, at a CAGR of 4.5% from 2025 to 2030. Escalating consumer demand for clean label and natural ingredients will drive the bulk food ingredient market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 44.8% growth during the forecast period.

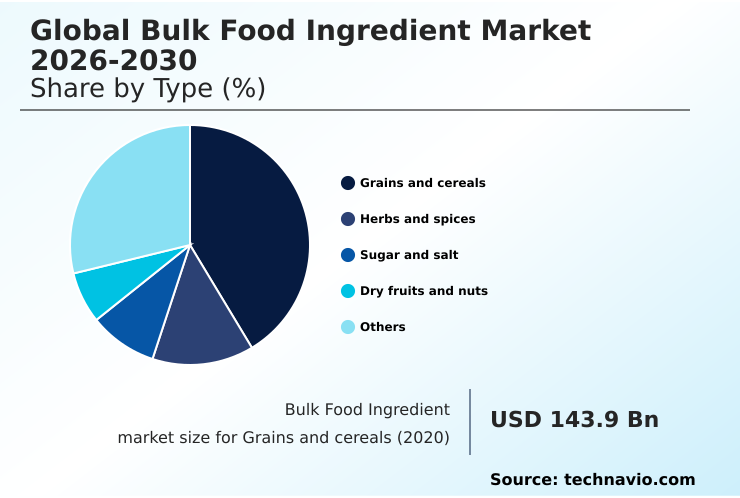

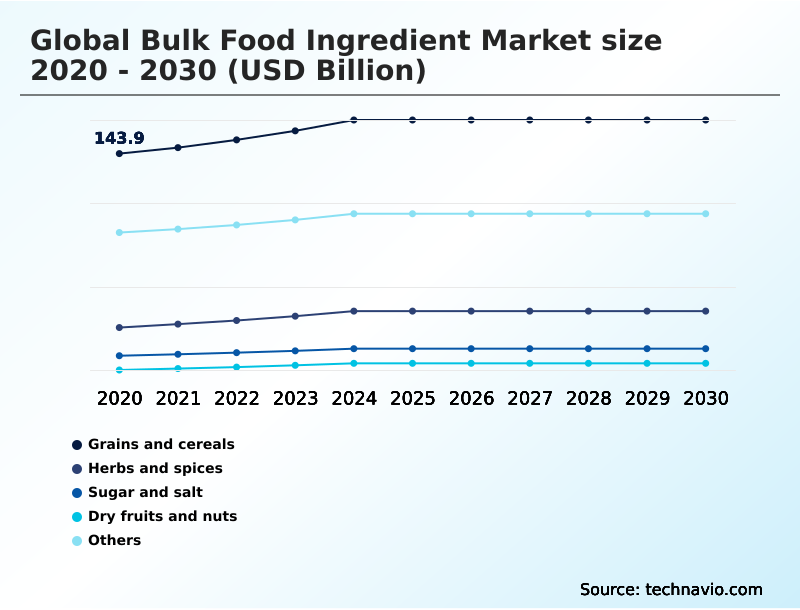

- By Type - Grains and cereals segment was valued at USD 162.5 billion in 2024

- By Application - Bakery and confectionery segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 163.9 billion

- Market Future Opportunities: USD 100.9 billion

- CAGR from 2025 to 2030 : 4.5%

Market Summary

- The bulk food ingredient market serves as the foundational layer of the food supply chain, providing essential components for industrial food production. This market is undergoing a significant transformation, driven by evolving consumer ethics that favor clean-label products, plant-based diets, and functional foods.

- For instance, a major consumer packaged goods company aiming to launch a healthier snack line must navigate this landscape by reformulating products. This involves replacing artificial additives with natural preservatives, enriching items with plant proteins and fibers, and reducing sugar content with novel sweeteners. This process highlights the market's core dynamics: balancing innovation and health trends against persistent challenges.

- These include navigating complex international regulations that differ by region and managing severe supply chain disruptions caused by geopolitical events and climate change. The industry's ability to innovate with ingredients that are sustainable, functional, and ethically sourced, while maintaining cost-effectiveness and supply resilience, will determine its future trajectory.

- This strategic balancing act defines the operational reality for participants in the bulk food ingredient market.

What will be the Size of the Bulk Food Ingredient Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Bulk Food Ingredient Market Segmented?

The bulk food ingredient industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Grains and cereals

- Herbs and spices

- Sugar and salt

- Dry fruits and nuts

- Others

- Application

- Bakery and confectionery

- Beverages

- Snacks and spreads

- Ready meals

- Others

- Distribution channel

- Direct from manufacturers

- Distributors

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Type Insights

The grains and cereals segment is estimated to witness significant growth during the forecast period.

The bulk food ingredient market is segmented by type, where grains and cereals are foundational, and by application, where demand from bakery, beverage, and ready meal sectors is strong.

The consumer shift toward on-the-go convenience drives the nutrient-dense snacks and shelf-stable meals categories, creating demand for functional components. This includes soy protein concentrates for protein enrichment and polydextrose for added fiber.

In beverages, ingredients like L-theanine and ashwagandha are gaining traction for functional benefits. The need for dairy alternatives and gluten-free alternatives is reshaping the use of traditional ingredients.

Furthermore, food manufacturers are incorporating yeast extracts and potassium chloride for sodium reduction, while a focus on wellness boosts demand for collagen peptides. Corporate commitments increasingly require deforestation-free supply chains, impacting sourcing strategies globally.

The Grains and cereals segment was valued at USD 162.5 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 44.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Bulk Food Ingredient Market Demand is Rising in APAC Get Free Sample

The APAC region is the fastest-growing market, contributing over 44% of the incremental growth, driven by an expanding food processing sector in countries like China and India.

This fuels demand for a wide range of ingredients, from commodity native starches to specialty flavorings and savory flavor systems.

In contrast, mature markets in Europe and North America focus on value-added products, driving innovation in sugar reduction solutions using stevia and monk fruit. European regulations are pushing for environmental social governance (ESG) compliance, making sustainable sourcing a prerequisite.

This has accelerated the adoption of steam sterilization and non-eto treatment for spices and rosemary extract for preservation.

Investment in cold chain infrastructure remains critical globally, improving the supply of ingredients like chicory root fiber and plant-based gelling systems, which are essential for many upcycled food byproducts.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic formulation is at the forefront of the global bulk food ingredient market 2026-2030, with a significant emphasis on clean label ingredients for bakery and functional ingredients for beverages. This drives the adoption of plant protein isolates for meat analogues and specialized hydrocolloids for dairy alternative texture, addressing consumer demand for healthier options.

- Sourcing strategies are also evolving, highlighted by the push for sustainable sourcing of cocoa ingredients and the adoption of regenerative agriculture for grain sourcing. This has increased the importance of traceability technology in food supply chains, where firms that have implemented such systems report a 25% faster response to quality inquiries compared to those using manual methods.

- The industry is also focused on innovation, with natural sweeteners versus artificial sweeteners being a key consideration in product development, leading to the wider use of options like allulose and stevia for sugar replacement. The use of upcycled ingredients in circular economy models is growing, and fortification with micronutrient premixes addresses public health goals.

- However, significant challenges in the bulk food ingredient supply chain, including the impact of geopolitics on commodity prices and complex sodium reduction strategies in processed foods, require constant strategic management. The use of clean label texturizers replacing modified starches, probiotics in functional food formulation, and botanical extracts for stress relief beverages showcases the market's innovative direction.

- Companies must balance cost-effective ingredients for ready meals with the need to meet stringent halal certified ingredients for export markets.

What are the key market drivers leading to the rise in the adoption of Bulk Food Ingredient Industry?

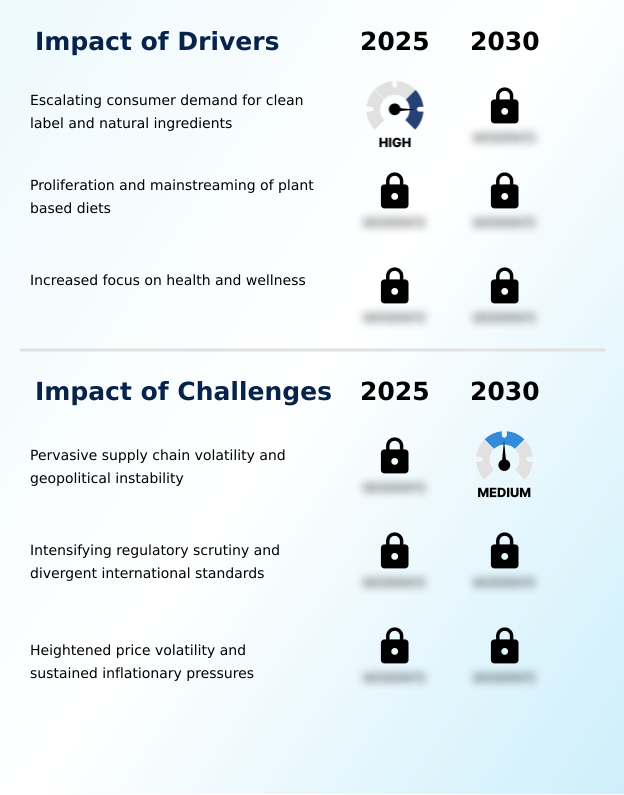

- The escalating consumer demand for clean label and natural ingredients serves as a key driver for growth and innovation within the market.

- The 'food as medicine' movement is a major driver, creating robust demand for ingredients that support wellness.

- Formulations now incorporate probiotics and prebiotics for gut health modulation, a segment where clinical studies have shown specific dietary fibers can improve outcomes by up to 25%.

- This has led to the mainstreaming of botanical extracts and nootropic compounds in functional beverages.

- The push for healthier products also fuels the market for sodium reduction solutions and sugar reduction solutions, with regulatory goals targeting a 15% decrease in sodium in certain food categories.

- Manufacturers are actively reformulating to create allergen-free products and prioritize non-gmo ingredients, using technologies like cold-pressure processing and natural preservatives such as cultured dextrose to deliver cleaner, safer products.

What are the market trends shaping the Bulk Food Ingredient Industry?

- The increasing importance of sustainable and ethically sourced ingredients represents a significant emerging market trend. This shift is reshaping procurement strategies and influencing consumer purchasing decisions across the food industry.

- A dominant trend is the pivot to sustainable sourcing, with corporate initiatives committing to regenerative agriculture on over 10 million acres of farmland. This emphasis on ethical transparency requires advanced supply chain traceability systems. Concurrently, innovation in upcycled ingredients is turning manufacturing byproducts into valuable functional ingredients, with some firms achieving a 20% waste reduction.

- The expansion of plant-based analogues is driving demand for plant protein isolates and hydrocolloids for texture. Manufacturers are adopting clean label texturizers and natural colorants to meet consumer demand for simple products, a core tenet of clean label formulation.

- This aligns with the food as medicine concept, where ingredient choice is linked to health outcomes, a preference cited by over 60% of consumers.

What challenges does the Bulk Food Ingredient Industry face during its growth?

- Pervasive supply chain volatility, compounded by geopolitical instability, presents a key challenge affecting the growth and stability of the industry.

- Pervasive supply chain volatility presents a significant challenge, with geopolitical events causing transit time increases of 10-15 days and freight cost surges of over 200% on key routes. This instability affects the reliable supply of commodities, including textured vegetable protein and demineralized whey.

- Concurrently, divergent international standards for food fortification with micronutrient premixes and approvals for novel ingredients like allulose create complexity. Navigating requirements for halal certification and kosher certification adds further operational overhead. While technologies such as high-pressure processing aid in natural preservation, the high capital investment is a barrier.

- Meanwhile, nascent sectors like cellular agriculture and other food-tech ventures face long-term uncertainty regarding regulatory pathways for ingredients such as gellan gum and methylcellulose.

Exclusive Technavio Analysis on Customer Landscape

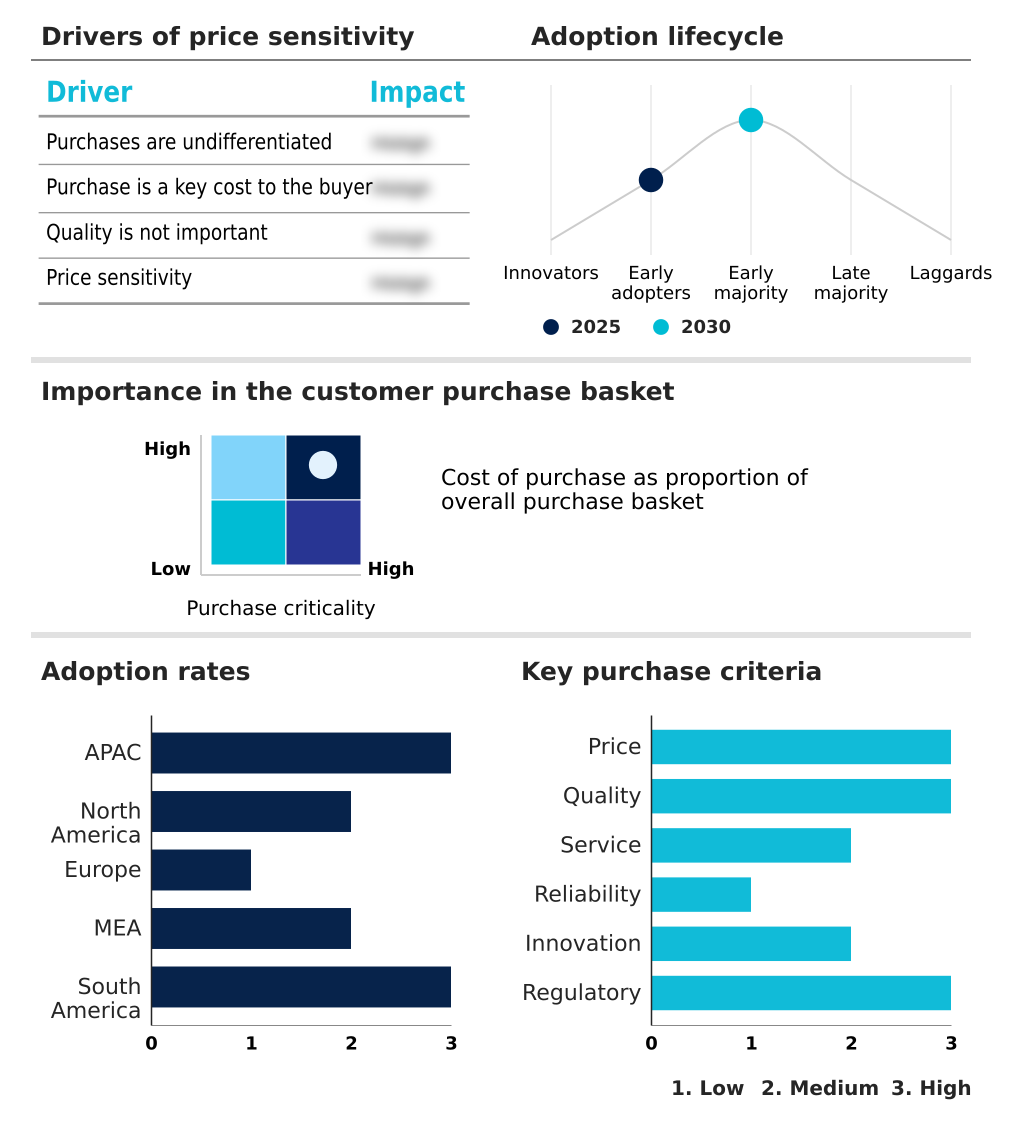

The bulk food ingredient market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the bulk food ingredient market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Bulk Food Ingredient Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, bulk food ingredient market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ajinomoto Co. Inc. - The landscape is defined by diversified agribusinesses and specialized firms providing a vast portfolio of commodity, functional, and value-added ingredients to the food and beverage sector.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ajinomoto Co. Inc.

- Archer Daniels Midland Co.

- Barry Callebaut AG

- BASF SE

- Beneo GmbH

- Bunge Global SA

- CP Kelco US Inc.

- DSM Firmenich AG

- Fonterra Cooperative Group Ltd.

- Givaudan SA

- Glanbia plc

- Ingredion Inc.

- International Flavors Inc.

- Kerry Group Plc

- Novonesis Group

- Roquette Freres SA

- Royal Friesland Campina NV

- Symrise Group

- Tate and Lyle PLC

- Wilmar International Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Bulk food ingredient market

- In September 2024, Archer Daniels Midland Co. announced the acquisition of a European food-tech startup specializing in precision fermentation for USD 150 million, aiming to scale up production of novel dairy-alternative proteins.

- In November 2024, Tate & Lyle PLC launched its new 'Sweeten-Pro' line, an advanced allulose-based sweetening system designed to replicate the mouthfeel and browning of sucrose in bakery applications with 90% fewer calories.

- In January 2025, the US Food and Drug Administration (FDA) issued final guidance requiring mandatory supply chain traceability for high-risk bulk food ingredients, including certain spices and nuts, to combat foodborne illness outbreaks.

- In April 2025, Cargill Inc. announced a major expansion of its regenerative agriculture program in South America, partnering with local cooperatives to transition 5 million acres of soy and corn farmland to sustainable practices by 2030.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Bulk Food Ingredient Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 315 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.5% |

| Market growth 2026-2030 | USD 100.9 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.4% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The bulk food ingredient market is defined by a strategic pivot from commodity supply to science-backed solutions. Boardroom-level decisions now center on balancing investment in R&D for high-value functional ingredients against the need to secure volatile raw material supply chains. The market is increasingly rewarding innovation in clean label texturizers, plant protein isolates, and specialized hydrocolloids.

- Companies focusing on these areas report that their new product development cycles are up to 30% faster than those centered on traditional commodities. This shift is driven by consumer demand for healthier products featuring probiotics, prebiotics, and natural colorants.

- Consequently, suppliers must offer not just ingredients like dietary fibers and botanical extracts but also the formulation expertise to integrate them effectively. Success now depends on providing a portfolio of advanced components, including nootropic compounds, cold-pressure processing compatible items, and natural preservatives like cultured dextrose, to meet the complex demands of modern food manufacturing.

What are the Key Data Covered in this Bulk Food Ingredient Market Research and Growth Report?

-

What is the expected growth of the Bulk Food Ingredient Market between 2026 and 2030?

-

USD 100.9 billion, at a CAGR of 4.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Grains and cereals, Herbs and spices, Sugar and salt, Dry fruits and nuts, and Others), Application (Bakery and confectionery, Beverages, Snacks and spreads, Ready meals, and Others), Distribution Channel (Direct from manufacturers, and Distributors) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating consumer demand for clean label and natural ingredients, Pervasive supply chain volatility and geopolitical instability

-

-

Who are the major players in the Bulk Food Ingredient Market?

-

Ajinomoto Co. Inc., Archer Daniels Midland Co., Barry Callebaut AG, BASF SE, Beneo GmbH, Bunge Global SA, CP Kelco US Inc., DSM Firmenich AG, Fonterra Cooperative Group Ltd., Givaudan SA, Glanbia plc, Ingredion Inc., International Flavors Inc., Kerry Group Plc, Novonesis Group, Roquette Freres SA, Royal Friesland Campina NV, Symrise Group, Tate and Lyle PLC and Wilmar International Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by strategic pivots toward value-added offerings. The demand for plant-based analogues and ingredients supporting sustainable sourcing is compelling suppliers to innovate beyond commodities, with firms leveraging advanced supply chain traceability reporting a 15% improvement in meeting ESG compliance metrics. This shift toward ethical transparency is not just consumer-driven; it enhances operational resilience.

- The focus on food as medicine is expanding the use of specialized ingredients, while a commitment to clean label formulation is now a baseline expectation. As a result, suppliers that offer robust technical support for reformulation and can verify claims through transparent sourcing command a competitive advantage, achieving up to a 10% higher customer retention rate compared to commodity-focused peers.

We can help! Our analysts can customize this bulk food ingredient market research report to meet your requirements.

RIA -

RIA -