Call Center Artificial Intelligence (Ai) Market Size 2025-2029

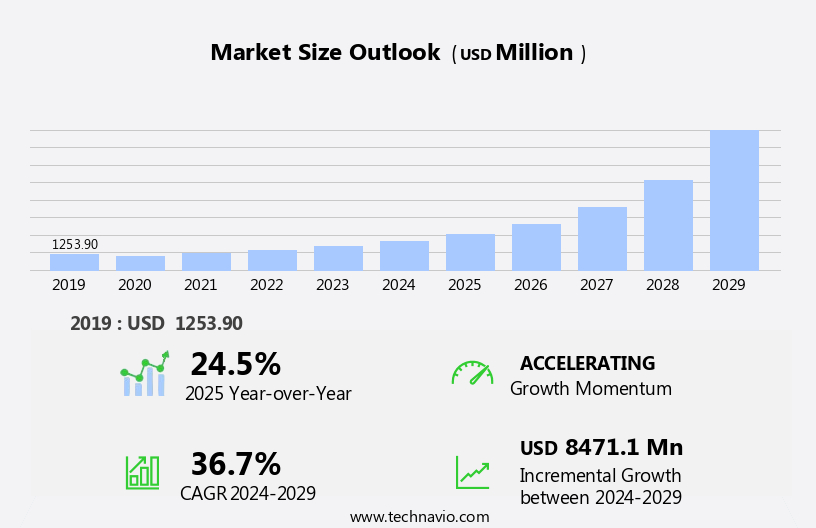

The call center artificial intelligence (ai) market size is forecast to increase by USD 8.47 billion, at a CAGR of 36.7% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing adoption of cloud-based call centers and the integration of chatbots for improved turnaround times. Cloud-based call centers offer numerous advantages, including cost savings, scalability, and flexibility, making them an attractive option for businesses seeking to enhance their customer service capabilities. Furthermore, the integration of AI-powered chatbots enables faster response times, reducing the workload on human agents and improving overall efficiency. However, the integration of AI in call centers also presents challenges. One such challenge is the complexities involved in integrating front-end and back-end knowledge bases.

- Ensuring seamless communication between these systems is essential for delivering a positive customer experience. Additionally, maintaining the accuracy and effectiveness of AI algorithms in understanding and responding to customer queries remains a significant hurdle. Companies must invest in continuous improvement and refinement of their AI technologies to stay competitive in the market. Overall, the Call Center AI market offers significant opportunities for businesses looking to streamline their customer service operations and enhance the customer experience, while also presenting challenges that require careful planning and investment to overcome.

What will be the Size of the Call Center Artificial Intelligence (Ai) Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and the increasing demand for efficient and personalized customer interactions. Call center training and software solutions are integrating AI technologies such as automated call routing, outbound call centers, and customer journey mapping to streamline processes and enhance customer experience. Outbound call centers leverage AI-powered predictive dialing and speech recognition to increase call connect rates and improve agent productivity. Inbound call centers employ AI-driven interactive voice response systems and sentiment analysis to provide quick and accurate responses to customer queries. Automated call routing and customer segmentation help prioritize calls based on customer data, ensuring first call resolution and reducing call volume.

AI-powered chatbots offer multi-channel support, handling simple queries and freeing up agents for more complex issues. Agent assist tools use natural language processing and speech recognition to provide real-time suggestions and improve agent performance management. Cloud-based call centers enable remote work and offer scalability, while call analytics and quality assurance tools ensure continuous optimization. Virtual assistants and voice biometrics add a layer of convenience and security, enhancing the overall customer experience. Call center automation, average handle time, and call quality monitoring are essential metrics that AI technologies help optimize, ensuring efficient and effective customer interactions. The call center AI market is a dynamic and evolving landscape, with ongoing advancements in technology and shifting customer expectations driving market activities.

Continuous innovation and adaptation to new trends and patterns are essential for call center businesses to remain competitive and provide exceptional customer service.

How is this Call Center Artificial Intelligence (Ai) Industry segmented?

The call center artificial intelligence (ai) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- BFSI

- Retail and e-commerce

- IT and telecom

- Media and entertainment

- Others

- Channel

- Phone

- Chat

- Email or text

- Social media

- Website

- Deployment

- On-premises

- Cloud

- Source

- Large enterprises

- SMEs

- Component

- Solutions

- Services

- Application

- Predictive Call Routing

- Sentiment Analysis

- Workforce Optimization

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Russia

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

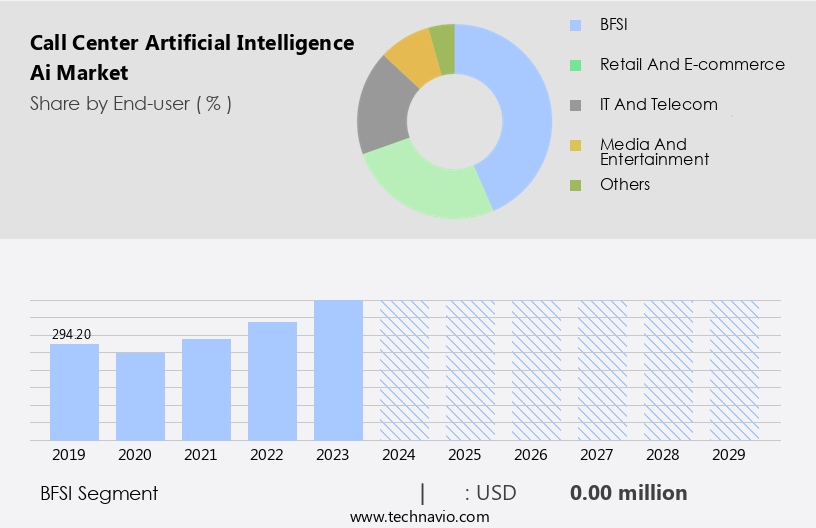

The bfsi segment is estimated to witness significant growth during the forecast period.

The market in the Banking, Financial Services, and Insurance (BFSI) sector has witnessed significant growth due to the industry's large customer base and increasing adoption of mobile technology. Banks such as Bank of America, J.P. Morgan Chase, and Capital One have integrated AI technologies to enhance customer engagement, streamline operations, and improve overall customer experience. AI-powered solutions have revolutionized various call center functions, including lead generation, sales support, appointment scheduling, voice biometrics, customer segmentation, and call analytics. AI-driven chatbots have become an essential component of customer service and customer relationship management, providing multi-channel support and handling routine inquiries efficiently.

Predictive dialing, speech recognition, and natural language processing have improved agent performance management, call quality monitoring, and first call resolution, reducing average handle time and abandonment rate. Omnichannel support, call center optimization, and quality assurance have become essential for providing a seamless customer journey. Virtual assistants and agent assist tools have enhanced call center training, enabling agents to handle complex queries and providing real-time assistance. Cloud-based call center solutions and call center automation have enabled remote work and improved operational efficiency. Technical support and call center software have been instrumental in managing customer feedback, mapping customer journeys, and ensuring customer satisfaction.

Interactive voice response and sentiment analysis have helped in understanding customer needs and preferences, enabling personalized engagement and improved customer experience. In conclusion, the BFSI sector's call center AI market is evolving rapidly, with a focus on enhancing customer experience, reducing operational costs, and improving overall efficiency. AI-powered solutions have become essential for providing personalized, efficient, and effective customer support, enabling banks to stay competitive in the highly competitive financial services market.

The BFSI segment was valued at USD billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

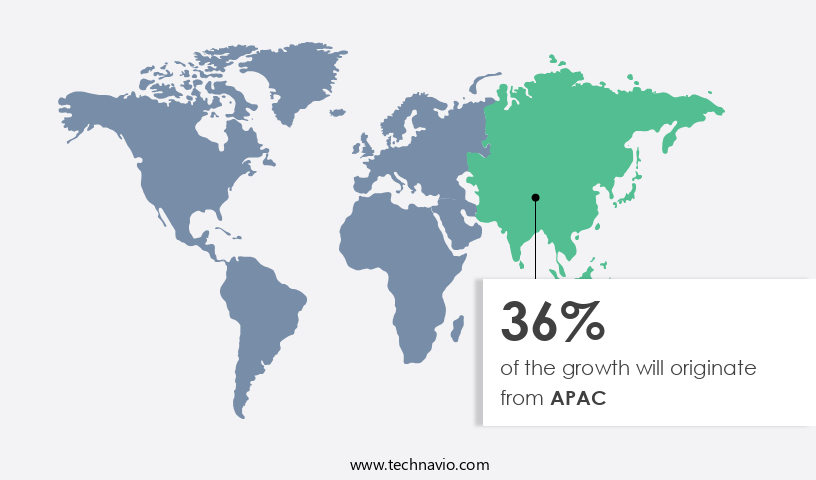

APAC is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is poised for significant growth due to the region's tech-savvy population and early adoption of chatbot technology. The use of bots is increasingly popular in various sectors, including finance and retail, to improve customer experience and foster brand loyalty. In the US, AI awareness and potential benefits are driving adoption, with leading banks such as Bank of America Corp. Utilizing bots like Erica and COIN for customer service. Multi-channel support, predictive dialing, speech recognition, natural language processing, and sentiment analysis are integral to AI-powered call centers, enhancing call center optimization, agent performance management, and customer relationship management.

Virtual assistants, call recording, customer segmentation, and call analytics further augment call center operations, while automated call routing and average handle time facilitate efficient service. Omnichannel support, quality assurance, and call center training ensure consistent customer satisfaction, and cloud-based call centers offer flexibility and scalability. Call volume, first call resolution, customer journey mapping, and customer feedback management are crucial metrics for call center success, with call quality monitoring and interactive voice response providing valuable insights for continuous improvement. Technical support and call center automation streamline processes, reducing abandonment rates and enhancing overall performance.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Call Center Artificial Intelligence (Ai) Industry?

- The significant growth in the implementation of cloud-based call center solutions is the primary market driver.

- In today's business landscape, cloud computing's increasing adoption is driving the growth of various software-as-a-service (SaaS) applications, such as customer relationship management (CRM), sales management, human resource management (HRM), and financial management. The advantages of cloud computing, including scalability, reliability, and high resource availability, are compelling enterprises to transition to cloud architecture. This shift eliminates the need for a dedicated IT support team and can significantly reduce operational costs. One specific area of application for cloud-based SaaS is call center operations. Advanced technologies like predictive dialing, speech recognition, natural language processing, call analytics, call center optimization, virtual assistants, and quality assurance are enhancing the customer experience and improving overall efficiency.

- Multi-channel support and omnichannel support are becoming essential to meet the diverse needs of customers. By adopting cloud-based call center solutions, businesses can leverage these advanced technologies on a pay-per-use basis, making it an affordable and effective solution. In conclusion, the adoption of cloud computing and its associated applications, including call center solutions, is a strategic move for businesses looking to optimize their operations and enhance their customer relationships.

What are the market trends shaping the Call Center Artificial Intelligence (Ai) Industry?

- The integration of chatbots is becoming a market trend due to their ability to significantly reduce turnaround times. This professional and efficient solution enhances customer experience by providing instant responses.

- Call centers play a crucial role in delivering excellent customer service, yet agents often face challenges in providing prompt solutions due to the need to retrieve relevant data or handle complex queries. This delay can lead to customer dissatisfaction and potential loss of business. To address this issue, call centers are increasingly adopting Artificial Intelligence (AI) technologies, such as chatbots, to handle routine inquiries and automate tasks. These AI solutions enable automated call routing, first call resolution, and customer journey mapping, enhancing the overall customer experience. Furthermore, AI-powered call center software facilitates cloud-based operations, enabling agents to access real-time data and customer history, ensuring personalized and efficient interactions.

- Additionally, AI tools like agent assist and customer feedback management enable continuous improvement and training, ensuring that human agents are equipped to handle more complex queries effectively. By integrating AI into call center operations, businesses can streamline processes, reduce call handling time, and improve overall customer satisfaction.

What challenges does the Call Center Artificial Intelligence (Ai) Industry face during its growth?

- The integration of front-end and back-end knowledge bases poses a significant challenge to the industry's growth, requiring professionals to possess a comprehensive understanding of both systems to ensure seamless data exchange and optimal performance.

- The integration of Artificial Intelligence (AI) in call center automation is revolutionizing the customer support industry. Advanced technologies like interactive voice response (IVR), sentiment analysis, and call quality monitoring are being adopted by various sectors, including finance, telecommunications, healthcare, and media. However, the implementation of these AI-driven solutions presents challenges, such as system integration and interoperability. To address this issue, companies need to provide unified IT solutions that can seamlessly integrate with different organizational IT infrastructures. Moreover, chatbots, a popular AI application in call center automation, require integration from both the front and back ends. The deployment of chatbots can overlap or create multiple knowledge bases, making it essential to ensure a unified and consistent knowledge base.

- This integration complexity can lead to an increase in average handle time and abandonment rate, impacting customer satisfaction negatively. In conclusion, while AI adoption in call centers offers numerous benefits, organizations must consider the challenges and invest in comprehensive IT solutions to ensure a smooth and effective implementation.

Exclusive Customer Landscape

The call center artificial intelligence (ai) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the call center artificial intelligence (ai) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, call center artificial intelligence (ai) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alphabet Inc. - This company provides advanced call center AI solutions, enabling human agents to handle complex and specialized queries. Agents receive real-time data, streamlined workflows, and step-by-step guidance to optimize performance. By integrating AI technology, customer service teams can efficiently manage routine inquiries, allowing human agents to focus on more intricate issues. This approach enhances overall service quality and customer satisfaction.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alphabet Inc.

- Amazon.com Inc.

- Avaamo Inc.

- Avaya LLC

- Conversica Inc.

- Creative Virtual Ltd.

- EdgeVerve Systems Ltd.

- Inbenta Holdings Inc.

- Jio Haptik Technologies Ltd.

- Kore.ai Inc.

- Microsoft Corp.

- NICE Ltd.

- Nuance Communications Inc.

- Oracle Corp.

- Pypestream Inc.

- Rulai

- SAP SE

- Talkdesk Inc.

- Teneo AI

- Zendesk Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Call Center Artificial Intelligence (Ai) Market

- In March 2024, Genpact, a global professional services firm, announced the launch of its AI-driven customer experience platform, "Intelligent Digital Operations (IDO)." This solution uses natural language processing and machine learning algorithms to automate call center processes and enhance customer engagement (Genpact Press Release, 2024).

- In June 2024, Amazon Web Services (AWS) and Twilio announced a strategic partnership to integrate AWS's Amazon Connect contact center service with Twilio's Programmable Voice and Messaging APIs. This collaboration enables businesses to build omnichannel communication systems, combining voice, messaging, and AI capabilities (AWS Press Release, 2024).

- In October 2024, NICE Ltd., a leading provider of customer experience solutions, completed the acquisition of Invero, a German AI-based contact center analytics firm. This acquisition strengthens NICE's AI capabilities and enhances its offerings in predictive analytics and sentiment analysis (NICE Press Release, 2024).

- In February 2025, IBM announced the deployment of Watson Assistant in its cloud-based call center solution, IBM Watson Customer Care. This AI-powered assistant uses natural language processing and machine learning to understand customer queries and provide personalized responses, improving customer satisfaction and reducing call handling time (IBM Press Release, 2025).

Research Analyst Overview

- The call center AI market is witnessing significant advancements, driven by the integration of various technologies such as voice recognition, deep learning, and speech synthesis. These technologies enable more efficient and effective customer interactions, enhancing the user experience. Businesses are leveraging machine learning algorithms for data analytics, data mining, and intent recognition to gain valuable insights and improve customer profiling. Integration platforms are facilitating the seamless adoption of these technologies, ensuring mobile optimization and real-time analytics. Deep learning and neural networks are also being used for process optimization, predictive modeling, and fraud detection.

- Biometric authentication adds an extra layer of security, while natural language understanding and computer vision expand the capabilities of AI in call centers. Data privacy remains a crucial concern, with the implementation of user interface designs prioritizing data security. Cloud computing facilitates scalability and cost savings, making AI adoption more accessible to businesses of all sizes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Call Center Artificial Intelligence (Ai) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

244 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 36.7% |

|

Market growth 2025-2029 |

USD 8471.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

24.5 |

|

Key countries |

Germany, US, Canada, Russia, Brazil, UK, China, India, Japan, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Call Center Artificial Intelligence (Ai) Market Research and Growth Report?

- CAGR of the Call Center Artificial Intelligence (Ai) industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the call center artificial intelligence (ai) market growth of industry companies

We can help! Our analysts can customize this call center artificial intelligence (ai) market research report to meet your requirements.

RIA -

RIA -